Turn Off, Tune Out

The first quarter of 2021 comes to a close today, and as fast as time seems to fly, it’s been a long one. Take GameStop (GME). It may seem like months and months ago, but it wasn’t until late January that the stock started to go crazy as the ‘Reddit Rebellion’ launched and caused a mad scramble by hedge funds to cover any and all of their short positions. Think about it. In under three months, we’ve seen at least two large funds (Melvin Capital and Archegos), not to mention the collapse of supply chain finance giant Greensill Capital. Sometimes we go an entire year without blowups of this magnitude.

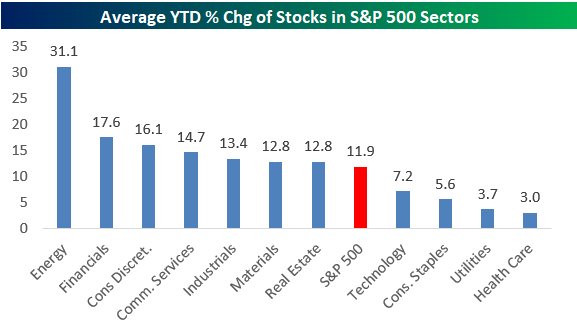

Despite the tumultuous headlines and market volatility along with the frustrating churn in the market lately, US equities are finishing off the quarter well. Stocks in the S&P 500 are up an average of 11.9% so far this year and grouped by sector they’re all averaging gains. Leading the way higher, stocks in the Energy sector stand apart from every other sector with an average gain of over 20%. After Energy, stocks in the Financials and Consumer Discretionary sectors are both up an average of over 15%. On the other side of the chart, sectors underperforming are generally defensive in nature with Health Care and Utilities both averaging YTD gains of less than 5%. One notable underperforming sector given its size is Technology. With an average gain of 7.2% YTD, stocks in the Technology sector are underperforming the broader market by more than 4.5 percentage points.

Given the underperformance of Technology YTD, we can’t help but remember some market ‘certainties’ over the years that never quite came to fruition. Remember after the initial surge off the lows coming out of the Credit Crisis in 2008 and 2009? While Financials were the best performing sector coming off the lows, the rally in the sector ran out of steam and stalled out. All we kept hearing at the time was that ‘the market couldn’t rally without the Financials’, but rally it did. Now, after Technology outperformed during COVID and through last Summer, the sector has stalled out, and we’re hearing the same phrase now as we did back then with the only difference being that Technology has replaced Financials as the sector that the market couldn’t rally without. Since September 2nd though, when we first started to see the ‘Big Shift’ in the market, the S&P 500 has nearly tripled the return of the Technology sector, and despite Tech’s underperformance, the S&P 500 has still managed double-digit percentage gains. When it comes to the old conventional wisdom of the market, investors would be best served by doing the opposite of Timothy Leary by ‘turning off’ and ‘tuning out’ all the noise.

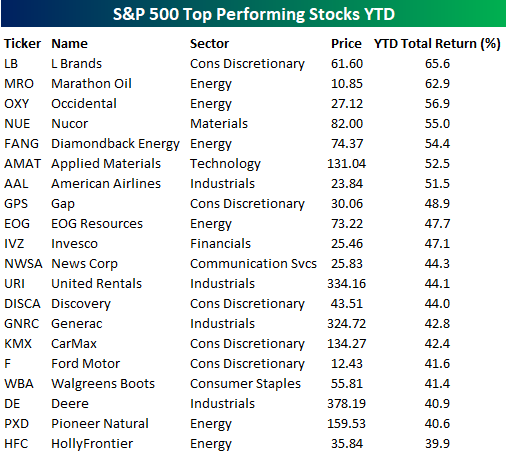

In the tables below, we list the top and bottom twenty performing S&P 500 stocks so far this year. Starting with the winners, L Brands (LB) and Marathon (MRO) are both already up over 60%, while another five stocks have rallied 50%+. With the exception of HollyFrontier (HFC), which is up 39.9%, every other one of the top 20 stocks is up over 40% – in just three months! What’s most notable about this table, though, isn’t what’s on it, but what isn’t. Technology has a larger number of components in the S&P 500 than any other sector, but only one stock from the sector – Applied Materials (AMAT) – made the list of top performers, and only one other besides AMAT (Hewlett Packard Enterprise) made the top 50.

At the other end of the spectrum, there are only 13 stocks in the S&P 500 that are down over 10% YTD, and the 20th worst-performing stock is down less than 9%. And while there was only little representation from the Technology sector on the list of biggest YTD winners above, there’s no shortage on the list of losers with eight of the twenty coming from that sector. It’s only been three months, but stretching back to early last September, the market has gotten along just fine without the help of Technology. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Consumer Pulse Report — April 2021

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke’s Morning Lineup – 3/31/21 – The Homestretch For Q1

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“End? No, the journey doesn’t end here.” – J.R.R. Tolkien

The first quarter is nearly in the books, but the year has only just begun, and with GameStop and Archegos already, it doesn’t look like 2021 will be a snoozer. Futures are inching higher this morning with the Nasdaq leading the way higher.

Economic data has generally been positive overnight with Chinese PMI and South Korean Industrial Production topping expectations, while inflation data in Europe remains relatively tame.

Read today’s Morning Lineup for a recap of all the major market news and events including a discussion of quarter-end trends, events in Brazil, a recap of international markets, the latest US and international COVID trends including our series of charts tracking vaccinations, and much more.

For all the churning in the market lately, it sounds hard to believe that every sector in the S&P 500 is on pace to finish Q1 in the black for the year. Granted, the gains aren’t evenly distributed, but it’s still impressive to see every sector positive on the year. Leading the way higher, Energy’s (XLE) 31% surge tops the list, but the double-digit percentage gains from Financials (XLF) and Industrials (XLI) are nothing to scoff at. Defensive-oriented sectors are unsurprisingly at the bottom of the list as Health Care (XLV), Utilities (XLU), and Consumer Staples (XLP) are all up 3% or less.

The most surprising sector to some, though, is Technology (XLK) which is at the absolute bottom of the list and just barely hanging on to positive territory for the year with a gain of under 1%. XLK is the only sector below its 50-DMA, and while it’s indicated to open higher today, closing out the quarter above its 50-DMA is going to be tough.

E.W. Scripps (SSP) Diverging From the Script of Media & Entertainment Stocks

Major media stocks caught up in the Archego margin call have found some respite today as Discovery (DISCA) and ViacomCBS (VIAC) both trade higher. Elsewhere in the Media and Entertainment industry, E.W. Scripps (SSP) came in at the top of our Stock Scores this week. Our Stock Scores ranks members of the S&P 1500 on their attractiveness based on a range of Fundamental, Technical, and Sentiment indicators. For access to our weekly Stock Scores screen, sign up here for access. SSP—which has a portfolio of local and national media outlets like TV stations and newspapers—came in this week with a perfect Technical score alongside high Fundamental and Sentiment scores.

At its multi-year highs earlier this month, E.W. Scripps (SSP) had broken out to multi-year highs before its sharp pullback in the second half of March which has brought the stock down around 20% from its closing high on March 12th. While that decline coincides with the big losses in VIAC and DISCA that resulted from prime brokers, who held positions equal to more than 5% of each company’s float, selling positions as hedge fund clients failed to meet margin calls on swap positions, in the case of SSP none of those same brokers like Credit Suisse or Morgan Stanley possess any significant stake. Additionally, the technical damage has not been quite as severe for SSP. Whereas the losses for VIAC or DISCA resulted in the stocks crashing through their 50-DMAs, SSP’s uptrend remains intact as it has so far managed to find support at its 50-DMA in the past week. SSP didn’t rally nearly as much as DISCA or VIAC, they haven’t dropped nearly as much either.

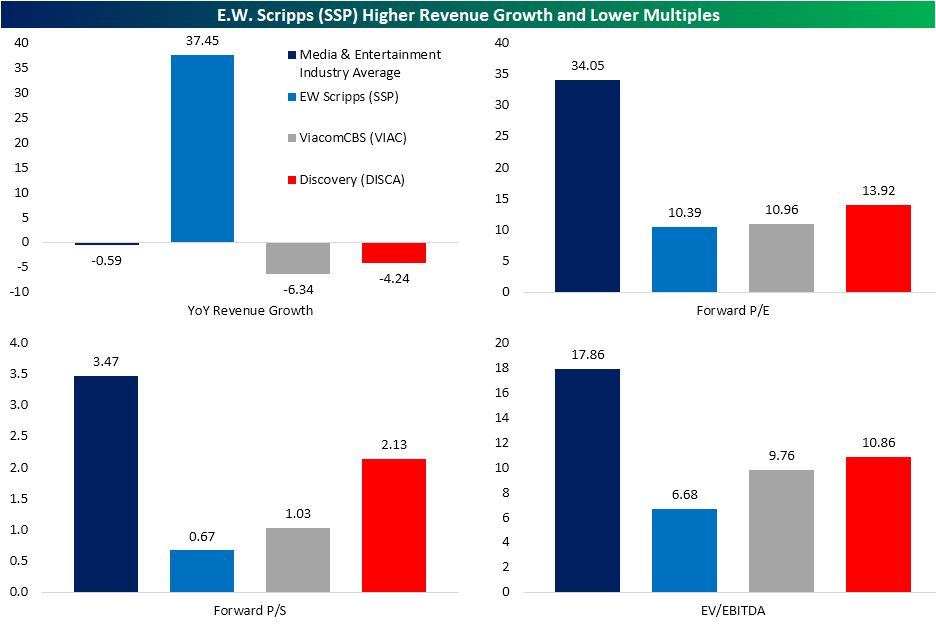

Not only is the technical picture positive, but an attractive valuation relative to its peers also played into EW Scripps’ high Stock Score this week. SSP showed much stronger revenue growth YoY, up 37.45% in 2020, when compared to the average for other stocks in the Media and Entertainment Industry. On top of that stronger revenue growth, SSP trades at a discount to the average stock in its industry on a forward P/E, P/S, and EV/EBITDA basis. Those are also more attractive valuations than VIAC and DISCA in spite of both of those stocks having seen their prices nearly cut in half recently. Respective of its own history, current valuations for SSP are also at the low end of the past decade’s range. Click here to view Bespoke’s premium membership options for our best research available.

Bank and Broker CDS After Archegos

On Friday, we noted massive share price declines for a handful of US media names and Chinese education technology stocks. Further details of the saga were released over the weekend and into this week which we reviewed in greater detail in yesterday’s Morning Lineup. Included in that news were announcements that two of the prime brokers for Archegos Capital Management — Credit Suisse (CS) and Nomura Holdings (NMR) — could incur significant losses as a result of the liquidation event. As a result, the two stocks were down double-digit percentage points yesterday with further losses today.

Some US firms have also been reported as involved as prime brokers in the ordeal including Morgan Stanley (MS) and Goldman Sachs (GS). In spite of their involvement, credit default swap (CDS) spreads have risen recently but are not necessarily at worrying levels for the time being. As shown in the charts below, the only major US investment banks’ CDS spread that has reached a new six-month high has been Morgan Stanley (MS). Across these four banks, CDS spreads range from Bank of America’s (BAC) low of 52.49 bps to Goldman Sachs’ (GS) high of 63.9 bps.

From an even longer time horizon, the recent tick higher in CDS is hardly even noticeable, especially relative to where they stood exactly one year ago. Back then, other than GS, each of these CDS spreads peaked above 200 bps. Again, although they have begun trending slightly higher, current levels across these four names are all below the five-year average.

By far the biggest move in CDS has been for the bank that appears to be the most affected: Credit Suisse. As shown in the first chart below, CDS for Credit Suisse have spiked to new six-month highs. Even still, CDS are only trading just above 70 basis points, which is significantly lower than the reading in the mid-100s seen during the COVID Crash last year. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 3/30/21 – Gloomy Gold

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The window to the world can be covered by a newspaper.” – Stanislaw Jerzy Lec

It’s more of the same this morning as futures are modestly negative, but higher interest rates are acting as a weight on the Nasdaq and growth stocks in general. The economic calendar is relatively light, with a report on home prices coming out at 9 AM eastern and Consumer Confidence at 10 AM. Crude oil and gold are both down sharply, but bitcoin is higher. In political news, President Biden will speak on Infrastructure this afternoon. In terms of the latest COVID trends, national declines have been inching higher, but the key as we discuss in the Morning Lineup is that among populations that have been widely vaccinated, case counts have remained contained.

Read today’s Morning Lineup for a recap of all the major market news and events including a discussion of the move higher in rates, a recap of international markets, some strong survey related economic data out of Europe, the latest US and international COVID trends including our series of charts tracking vaccinations, and much more.

Gold just hasn’t been able to get out of its way this quarter. Despite concerns over inflation, the yellow metal has been weak as interest rates rise. This morning alone, gold is trading down over 1.5% after trading down over 1% yesterday and on the verge of testing its recent lows.

With the quarter coming to a close tomorrow, gold is on pace for a double-digit percentage decline this quarter, making it the worst quarter in nearly five years and just the tenth quarterly decline of more than 10% in the last 45 years.

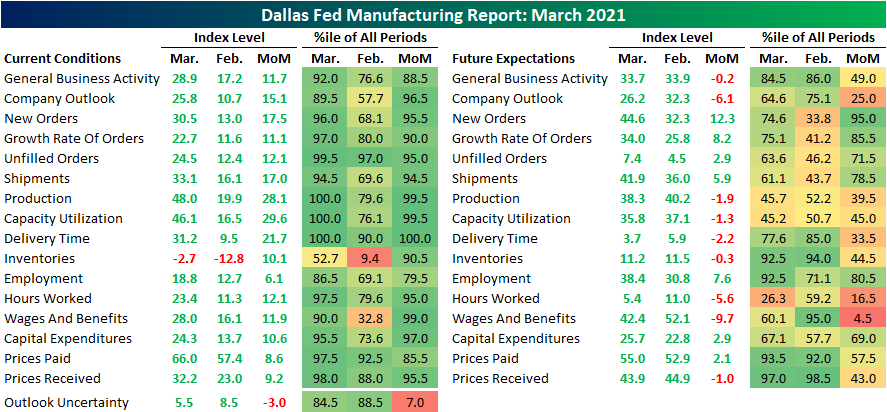

Dallas Manufacturing Bounces Back After the Storm

The reporting period for the Dallas Fed’s Manufacturing Outlook Survey for the month of February had some overlap with the region’s winter storms, but the extent of the damages were likely not fully captured. Fast forward a month to the March report and the region appears to have seen a strong bounce back. This morning’s release saw a huge beat relative to expectations just like other regions’ manufacturing surveys for the month of March. The Dallas Fed’s reading on the region’s manufacturing sector was actually expected to decline to 16.5 from last month’s reading of 17.2; the second-highest level of the index since the start of the pandemic. Instead of falling, the index surged to a new high post-pandemic high of 28.9. That is the best level since August 2018. Prior to 2018, the only other times that there has been as strong of readings was in the first few years of the index’s history.

The General Business Activity index was far from the only one to come in with an impressive reading. Across the 16 indices, 13 are in the top decile of readings with three of those at record highs. Expectations came in more mixed with most indices still positive but at less impressive levels historically while just over half fell month over month in March. Overall, the report showed that general conditions continue to improve with higher growth in orders, ramping up of production and employment, and higher prices. Granted, given the survey asks respondents to report on the change in activity from the prior month (i.e. when the winter storms had dampened activity), some of these strong readings could be a result of base effects.

New orders have consistently grown over the past several months, but since the fall, that pace of improvement had generally plateaued. But with activity bouncing back after the storms, the indices for New Orders and Order Growth Rate both ripped higher in March. New Orders topped a reading of 30 for the first time since June 2018 this month while Order Growth Rate reached the highest level since May of that same year. Thanks to that growth in new orders plus an inability to fulfill existing orders last month, the index for Unfilled Orders has experienced a more unprecedented spike higher. The 12.1 point rise month over month was in the top 5% of all monthly moves leaving the index at the second-highest level on record behind September 2005 when it was 10 points higher. Given that massive backlog, Shipments also have ramped up as the index rose 17 points to 33.1.

An even more impressive increase to gauge the effort being put in to meet that demand came from the indices for Production and Capacity Utilization. Both indices surged to new all-time highs.

Even though the region’s manufacturers have increased production significantly, supply chains are showing signs of stress. The index for Delivery Times soared by the highest amount in a single month on record to a new all-time high of 31.2, surpassing the previous record from September 2005 by almost 10 points.

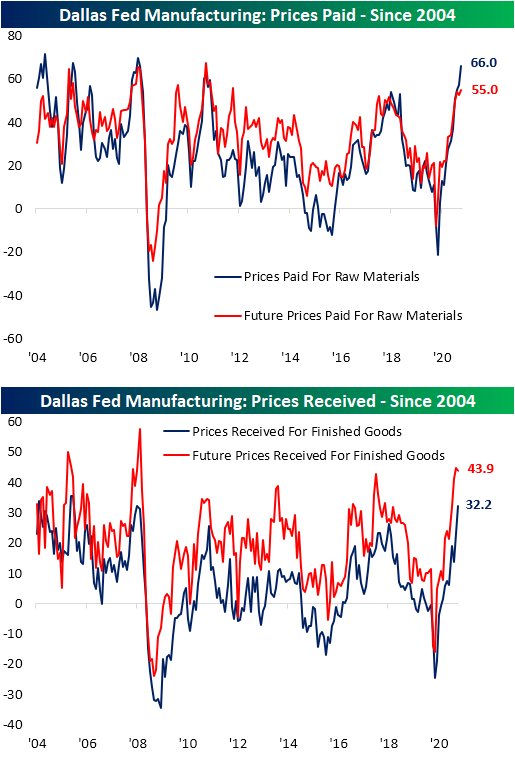

In addition to longer lead times, price growth is accelerating for both Prices Paid and Received. Prices Paid rose to 66 this month which is the sixth-highest level on record and a level that has not been seen since July 2008. The index for Prices Received is actually at a slightly higher end of its range (98th percentile versus 97.5th percentile for Prices Paid), but it too is at the highest level since 2008.

Finishing with a look at employment, although there was not a big pickup in the reading on firms increasing hiring, they appear to be making do with existing workers and are increasing incentives. The indices for Hours Worked and Wages & Benefits both saw increases in the top 5% of all months. In addition, Capital Expenditures also saw a big uptick in March. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 3/29/21 – Media Stocks in Focus

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“When you combine ignorance and leverage, you get some pretty interesting results.” – Warren Buffett

Media stocks are in focus this morning as the unwind of the Archegos hedge fund that began last week continues today. In today’s Morning Lineup, we provided a rundown of the situation and the key factors that will shape how things play out, so make sure to check that out (pg 4).

Futures are lower as financials that have been caught up in the liquidation look to open lower. Keep in mind also, that despite the weakness at the open, US equities saw major surges into the close on Friday.

Also in today’s report, check out updates on the latest market news and events from the US and around the world, including a summary of the Archegos hedge fund blow-up and its potential impact, profits in China, the rates market, the latest US and international COVID trends including our series of charts tracking vaccinations, and much more.

One bank being hit especially hard from the blow-up in the media stocks over the last week has been Nomura. Nomura has seen a lot in the last forty years. From the bursting of the Japanese stock bubble in 1989, the 1987 stock market crash, the failure of Long-Term Capital in the 1990s, and then the credit crisis just over 10 years ago, the bank has faced a number of crises. This morning, the Japanese bank disclosed that it faces $2 billion in losses tied to margin calls, and compared to those prior periods, $2 bln doesn’t have quite the shock value that it used to.

Don’t tell that to the stock though. Overnight, shares of Nomura fell more than 16%, which is the largest one-day decline the stock has experienced in at least 40 years.

Bespoke Brunch Reads: 3/28/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Policymaker Profiles

The Years of Work Behind Washington’s Best-Liked Man by Claudia Sahm (NYT)

An oral history of how a strait-laced Republican and former Wall Street executive has helped push the world’s most important central bank in a genuinely populist direction. [Link; soft paywall]

The Born Prophecy by Richard B. Schmitt (ABA Journal)

In the late-1990s, the nascent derivatives markets were starting to boom, and CFTC Chair Brooksley Born tried to set up prudential regulation. Her efforts were quashed by Clinton administration Treasury Secretary Bob Rubin, his top deputy Larry Summers, and Fed Chair Allan Greenspan. [Link]

Odd Marketing

Post Consumer Brands to repay shoppers for black-market Grape-Nuts purchases by Noah Manskar (NYP)

Consumers desperate for their fibrous favorite were willing to pay as much as $100 per box earlier this year, prompting parent company Post to offer to reimburse the biggest fans for their overpriced purchases. [Link; auto-playing video]

Read the Pentagon’s 20-Page Report on Its Own Meme by Matthew Gault (Vice)

An unimpressive effort to skewer Russian hackers spent three weeks filtering through an approval process at the Pentagon before winding up on the US Cyber Command’s Twitter feed. [Link]

Capex

A Van Fight Is Brewing by David Welch (Bloomberg)

Commercial vans typically travel less than 100 miles per day, so electric conversion of fleets that reduce operating costs thanks to fewer moving parts and fuel costs are compelling for operators…and that’s before considering big tax incentives. [Link; soft paywall]

Intel is spending $20 billion to build two new chip plants in Arizona by Kif Leswing (CNBC)

After losing huge ground to foreign competitors, Intel has decided to shift its strategy towards a more US-centric approach. The result is billions of capex on two Arizona factories. [Link]

Weird News

How Many Slaps Does it Take to Cook a Chicken? This YouTuber Built a Slapping Rig to Find Out by Alyse Stanley (Gizmodo)

Energy is fungible, so imparting kinetic force on a chicken should at least hypothetically be enough to raise its temperature to the point it is “cooked”. As it turns out, it’s not just a hypothetical possibility. [Link]

How to Kill a Zombie Fire by Matt Simon (Wired)

Peat fires can continue to burn long after they appear to be put out, and warming temperatures are making them more common. Luckily, new techniques are proving more effective in fighting these fires. [Link; soft paywall]

Gaming

RollerCoaster Tycoon: the best-optimised game of all time? by Matt Hrodey (PCGames)

Thanks to an expertise in a more fundamental language than the ones typically used to code graphics packages, RollerCoaster Tycoon’s original developer was able to pull off miraculous performance. [Link]

Infrastructure Week

Biden Team Prepares $3 Trillion in New Spending for the Economy by Jim Tankersley (NYT)

A two-part effort to revitalize physical infrastructure via investments in roads, bridges, telecommunications, housing, rail lines, ports, and green energy and human lives via job training, free community college, universal pre-kindergarten, subsidized childcare, and national paid leave is being floated by the Biden Administration. [Link; soft paywall]

Pandemic Spending

Pets and Pet Spending During the Pandemic: A Money Report by Paul Reynolds (Money)

Spending more time at home means spending more time with furry friends, leading to increases in value and affection of pets. Pandemic-enforced changes in behavior and increasing loneliness led to more purchases of pets, which were more commonly picked up from shelters or rescues than other sources. [Link]

Recast as ‘Stimmies,’ Federal Relief Checks Drive a Stock Buying Spree by Matt Phillips (NYT)

With $1400 economic impact payments rolling out the door, a legion of individual investors is looking to put their money to work in the stock market. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

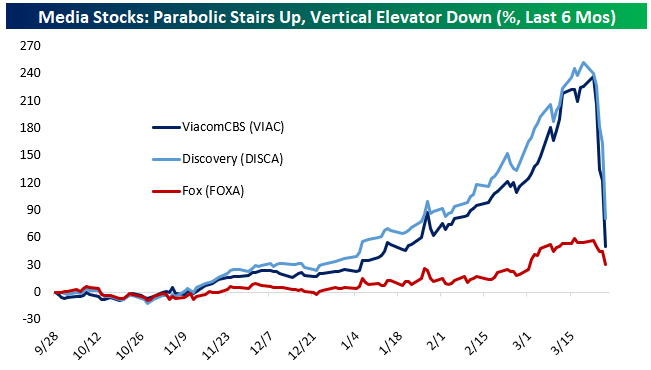

Media & Chinese Education Tech Carried Out On A Stretcher

This week we’ve seen a popular long blow up in a way that recalls the mess in GameStop (GME) earlier this year. As shown below, legacy media stocks like ViacomCBS (VIAC) and Discovery (DISCA) went parabolic since November. Fox (FOXA) also benefited, though to a much smaller degree. VIAC and DISCA both tripled in just a few months as hopes of a robust economic recovery boosting ad revenue and, more importantly, the potential for streaming riches similar to Disney (DIS) and its Disney+ platform helped fuel gains. But over the last four days, most of those gains have been incinerated. The catalyst appears to have been a secondary offering from VIAC a few days ago, with $1.7bn of shares sold into the $50bn market cap that existed at the time.

Since that secondary, the stock has been more than cut in half. There have also been rumors of a big, leveraged position by an unnamed fund having its portfolio seized and liquidated by its prime brokers. There have also been huge blocks of stock reported at dealers, with Goldman Sachs (GS) reportedly getting tapped to sell a block equivalent to more than 6% of VIAC’s free float and a second block equivalent to more than 12% of DISCA’s free float. In a reversal of the GME mess, VIAC has 18.5% of its float sold short, while DISCA’s short base is 29.7% of float. This particular blow-up is a win for shorts. Start a two-week free trial to Bespoke Institutional to access all of our analysis and market commentary.

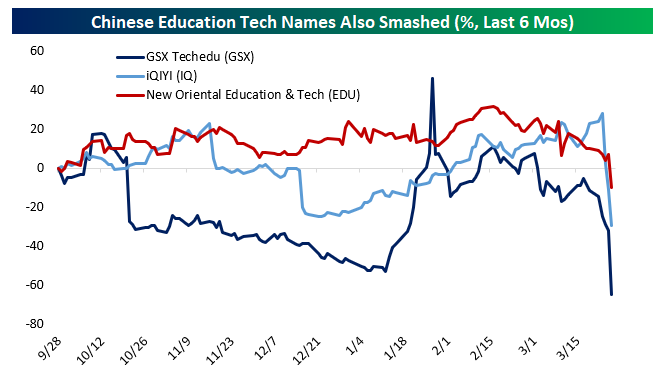

Another similar collapse has been playing out in Chinese education technology stocks listed in the US as ADRs. GSX Techedu (GSX) is down over 50% today, with a block offered by a dealer equivalent to almost 9% of the float. A similarly-sized block relative to float is also reportedly on offer in IQ. These names haven’t seen the same sort of parabolic gains as the media stocks above, but they’re a similar clustered theme that’s getting carried out to end the week.