Road and Rail Soar Above Air Freight

One major economic trend of the past several months has been supply chain constraints including logistics issues. Now in the throes of earnings season, earnings of companies related to supply chains and logistics (whether that be people or parcels) are beginning to roll in with four such names reporting in the past day alone: Kansas City Southern (KSU), United Airlines (UAL), Marten Transport (MRTN), and Knight-Swift Transportation (KNX). In the table below, we show all the S&P 1500 Transportation Industry stocks that have reported since late September. Most of these stocks have beaten estimates on the top and bottom line with a few exceptions. While it is the one furthest in the rearview now, FedEx (FDX) was perhaps the worst of these missing EPS estimates and lowering guidance. KNX, on the other hand, reported a triple play this morning; one of the first companies to do so thus far in earnings season.

Two more transportation names, CSX (CSX) and Landstar System (LSTR), are also set to report earnings after the closing bell today, and over a dozen other names will follow up in the next week alone. These names could potentially be interesting areas to look for anecdotes regarding broader supply chain issues pressuring the economy, but turning to the stock price reactions, Saia (SAIA) has averaged the largest single-day gain on earnings averaging a 2.5% move across its 60 past earnings reports. Old Dominion (ODFL), Echo Global Logistics (ECHO), Hub Group (HUBG), and XPO Logistics (XPO) are the only others that have averaged greater than 1% gains in reaction to earnings. C.H. Robinson (CHRW) and Avis Budget (CAR), on the other hand, have historically averaged the worst reactions to earnings of this industry.

While there are still plenty of companies within the industry left to report providing plenty of catalysts for moves, since the closing low on September 30th, the transports have seen solid performance with an 8.79% gain through today. That move has not only lifted the industry above its 50 and 200-DMAs but it has also broken the downtrend that has been in place since the spring. Currently, the group is still down 6.1% from its 52-week high. Click here to view Bespoke’s premium membership options.

Mortgage Activity Rollover

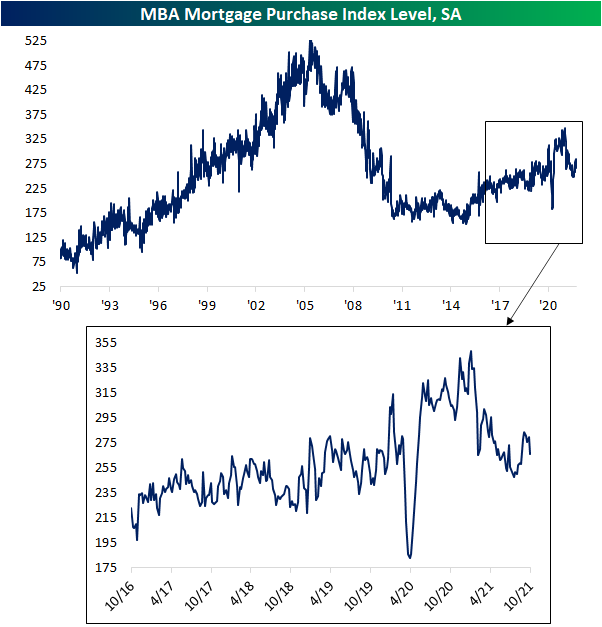

This morning the Mortgage Bankers Association (MBA) released their weekly read on mortgage activity. Whereas most of the past year has seen purchase applications trending lower, the reading bottomed out in late July indicating positive signs for other economic releases like new and existing home sales. Over the past month, though, as interest rates have been rising, the index has been erasing the late summer gains with this week’s 4.86% decline the largest for a single week since July 16th. With that said, the current level of purchase applications remains solid at the high end of the pre-COVID range.

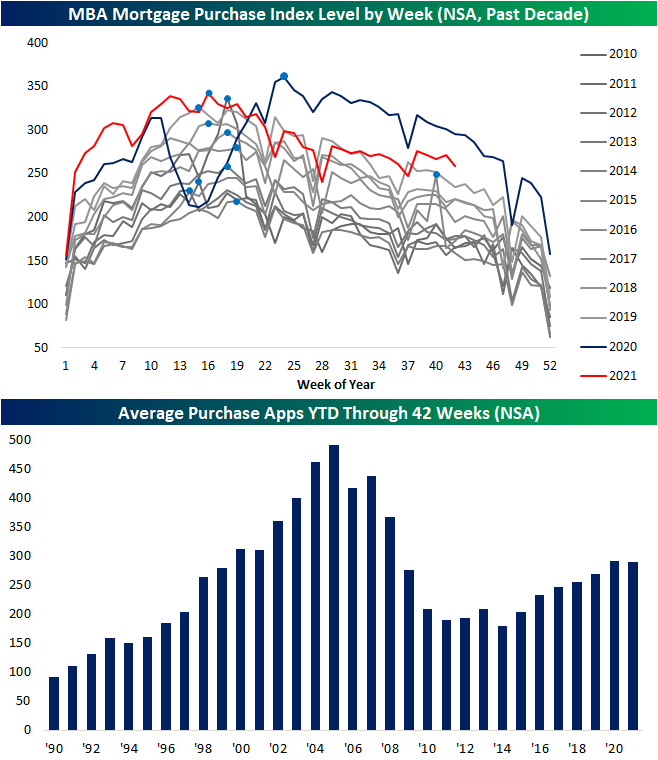

Purchase applications are generally following the normal seasonal pattern as well this year. Last year (dark blue line in the chart below) as the pandemic came about, purchase applications took a huge hit during what is normally the strongest point of the year for activity. That resulted in a later than normal seasonal peak (light blue dots). This year’s peak occurred in the spring as has been the norm over the past decade. While purchases have seen their usual seasonal decline since the spring, that does not mean purchases have been weak. Albeit not as strong as 2020 levels, purchase apps have been running at a clip similar to, if not stronger than, 2019 levels.

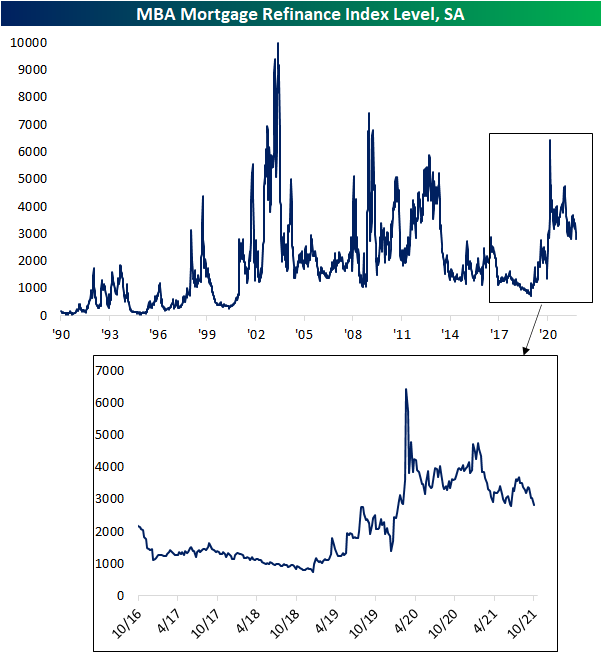

Refinance activity has also rolled over after moving higher in the summer. In fact, this week marked the fourth week in a row with a decline. In that span, this week and two weeks ago marked the largest declines of 7.12% and 9.58%, respectively. Those now leave the index just off recent post-pandemic lows set in early July.

Mortgage rates are certainly one factor contributing to the recent rollover in mortgage activity. As shown below, the national average for a 30-year fixed-rate mortgage is still at historic lows but is now off the lows. This rate bottomed in early August, and the end of last month saw a particularly significant leap higher. Currently, the rate stands at 3.18% versus 3.00% one month ago. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 10/20/21 – Futures Little Changed

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stone Age. Bronze Age. Iron Age. We define entire epics of humanity by the technology they use.” – Reed Hastings

There’s little movement in international equity markets and US equity futures currently, and the 10-year yield is flat at 1.63%. There’s no economic data to speak of today, but the Beige Book will be released at 2PM eastern. The S&P 500 has been up for five straight days now (its longest winning streak since late August) so a rest wouldn’t be too bad of a thing.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

While it initially rallied after the report was released, shares of Netflix (NFLX) quickly reversed in after-hours trading and are now looking at a loss of about 2% in the pre-market. While subscriber growth numbers came in better than expected, growth in North America looked a little more sluggish raising questions (again) that the streaming service has reached the saturation point in the United States.

Similar to the illustrations we provided of the large banks last week, the chart below shows the performance of NFLX since the start of 2020 with red dots indicating the closing price on the company’s earnings reaction day. What’s looking like a decline of around 2% for NFLX today would mark the seventh time in the last eight quarters where NFLX declined in reaction to earnings, and in each case, it has been a similar story; either sub growth was weaker than expected or investors anticipated that North American sub growth going forward would slow. Despite the short-term pessimism around each quarter’s report, since the start of 2020, NFLX has risen about 97% which is more than double the 44% gain of the S&P 500.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

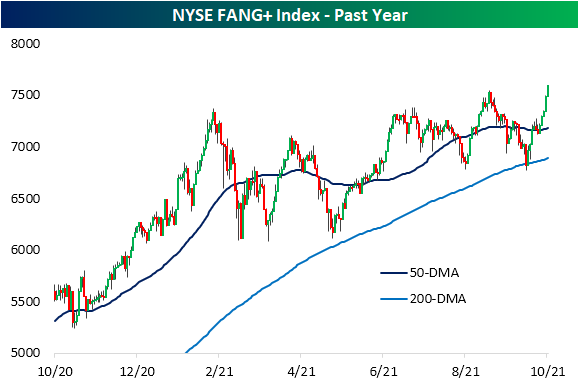

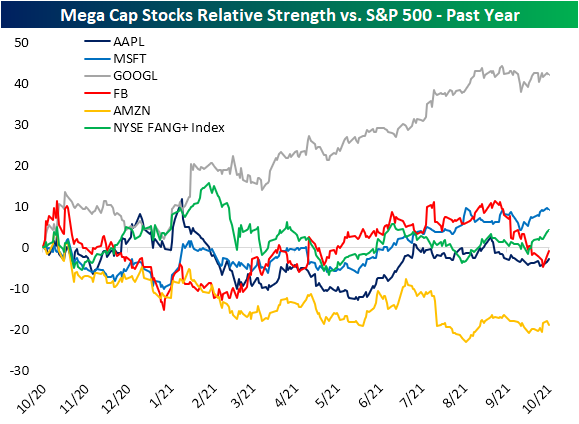

FANG+ Hits a New High With Mixed Relative Strength

One week ago, mega-cap Tech as measured by the NYSE FAANG+ index was trading right around its 50-DMA after successfully testing its 200-DMA not long before. After rallying 6.44% in the past five days, the index of FANG+ stocks is now back at a 52-week high.

In the chart below we show the relative strength lines of the five largest S&P 500 stocks as well as the FANG+ index versus the S&P 500. Microsoft (MSFT), Facebook (FB), and Apple (AAPL) have generally performed in line with the broader market over the past year. More recently, FB has given up any outperformance it had versus the S&P 500 as the stock has come under pressure over the past few weeks. Meanwhile, the broader FAANG+ space has seen its relative strength line turn higher. Two standout stocks on opposite ends of the spectrum for relative strength have been Alphabet (GOOGL) and Amazon (AMZN). Both have seen fairly flat moves in their relative strength lines since the late summer, but from their performance earlier in the year, GOOGL has distanced itself to the upside whereas AMZN has lagged behind other mega-caps.

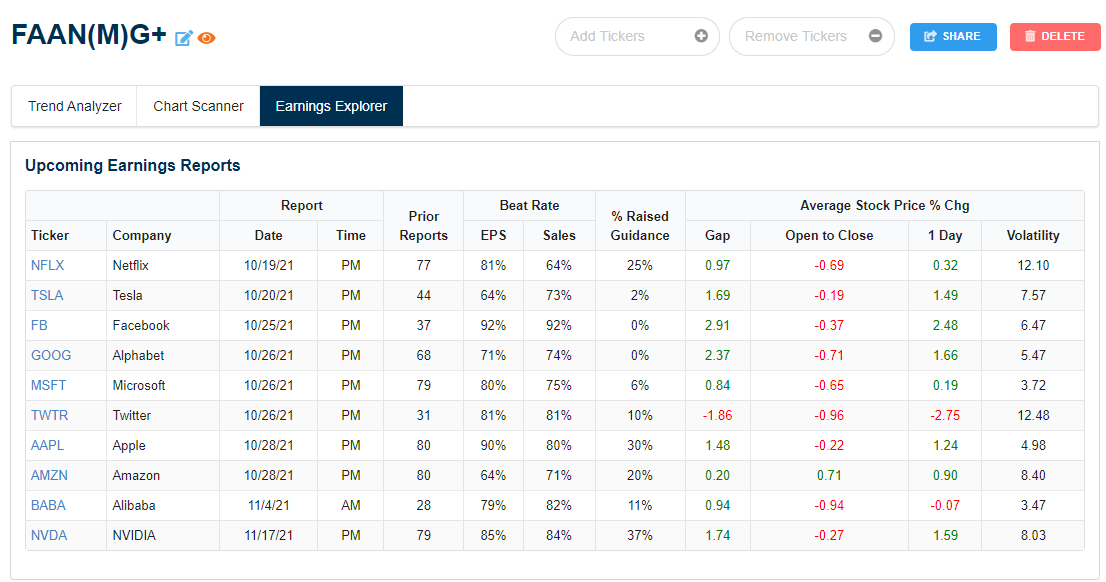

We would also note that a large portion of FAANG—or FAAN(M)G when including Microsoft—is scheduled to report earnings in the coming week. Of these, Twitter (TWTR) and Netflix (NFLX)—which reports tonight—have historically been the most volatile stocks on earnings with each one averaging a move of more than 12% (up or down). TWTR is also one of the only ones in the group to average a full-day decline on its earnings reaction days as shown in the snapshot of our Earnings Explorer below. Click here to view Bespoke’s premium membership options.

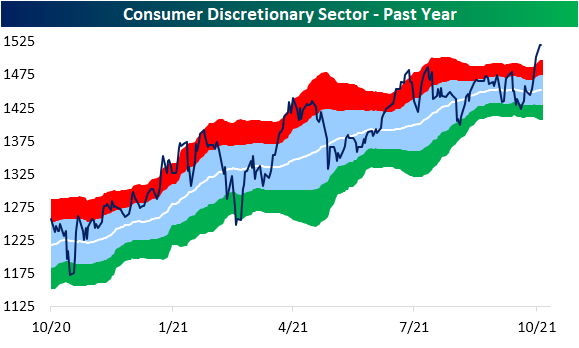

Consumer Discretionary Ripping

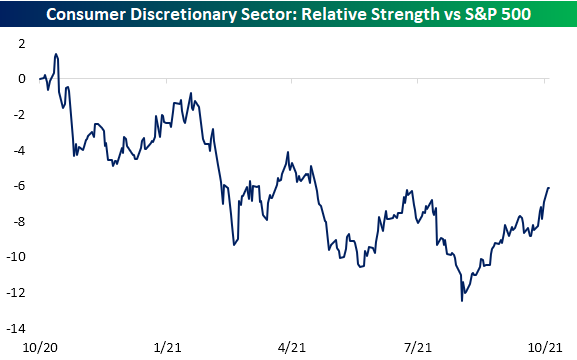

As we noted in last night’s Closer, some of the biggest members of the Consumer Discretionary sector by market cap like Amazon.com (AMZN) and Tesla (TSLA) have been pulling more than their fair share for the S&P 500’s gains recently. That also means the sector itself has been on a stellar run having risen over 5% in the past five days; the best five-day run since a 7.18% gain this past March. While currently elevated, this week’s move has marked a dramatic break out above the summer high. Additionally, its relative strength line versus the broader index has also made a significant breakout from the past year’s downtrend.

With that also comes a historic overbought reading. In the chart below, we show the distance in standard deviations that the Consumer Discretionary sector has traded from its 50-DMA. Finishing just shy of 3 standard deviations above its 50-DMA yesterday, the sector hit its most overbought level since the day after Christmas 2019. Going back to the start of our data in 1990, there have only been 20 times including that 2019 occurrence that the Consumer Discretionary sector was as overbought as it was yesterday.

Looking closer at some of the stocks that have driven the sector shows some interesting themes. As previously mentioned, online retail giant Amazon.com (AMZN) has been a key contributor to the S&P 500’s gains, and while the index has clearly broken out of its recent downtrend, AMZN is fighting to do the same. Meanwhile, Target (TGT) has posted double-digit gains in the past week bringing it quickly from oversold to overbought territory. Like AMZN, that move has smashed through a downtrend line.

Home improvement stores have also seen notable breakouts with Home Depot (HD) and Lowe’s (LOW) both breaking above their prior highs. Tractor Supply (TSCO), on the other hand, has maintained its uptrend but has yet to break out.

As consumers have likely had to put off car purchases due to constrained supply and instead repair the car they have, auto parts retailers have also been solid performers with notable breakouts of their own. Stocks like Advance Auto Parts (AAP), O’Reilly (ORLY), LKQ (LKQ), and AutoZone (AZO) have all made new highs in recent days. There are a couple of holdouts, though. Aptiv (APTV) continues to sit just short of a new high while Genuine Parts (GPC) has exited its downtrend but is much further below prior highs than its peers. Click here to view Bespoke’s premium membership options.

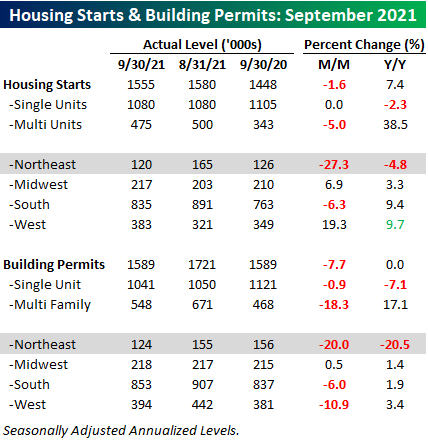

Residential Construction Activity Disappoints

This morning’s release from the Census Bureau on residential construction activity in September provided a double disappointment for investors. Not only did both Housing Starts and Building Permits come in weaker than expected, but the August reports were also revised modestly lower. The table below breaks down this month’s report by the size of unit and region. One positive about this month’s headline readings in both Housing Starts and Building Permits stems from the fact that all of the weakness was in multi-family units. Single-family units starts were actually unchanged relative to August and single-family permits were down less than 1%. Multi-family starts, meanwhile, were down 5.0% with permits even weaker, positing a decline of 18.3%.

On a regional basis, the Northeast was clearly an outlier with overall housing starts down 27.3% and permits down 20.0%. The remnants of Hurricane Ida and the massive flooding that encompassed many areas of the region may have been partly responsible for the slowdown in September’s activity.

Residential housing data barely even saw a downside blip in the aftermath of the pandemic, and levels of activity surged in the second half of 2021 and early this year. Signs are increasingly starting to emerge that things are cooling, though. Whether it’s lack of available supplies, labor shortages, affordability, or just a reversion to the mean after a strong pull-forward of demand, you can take your pick from one or all of the above. The slowdown is showing up in the 12-month moving averages of both starts and permits which both declined in September for the first time since May 2020, and unless monthly readings start to accelerate again next month, this trend will continue in the months ahead.

As for how Housing Starts interact with homebuilder stocks, the chart below compares the three-month average of starts to the performance of the iShares US Home Construction ETF (ITB) since 2007. The two series tend to track each other pretty well (correlation coefficient of +0.87), and you’ll notice that in recent months, the homebuilder stocks have run out of steam just as the level of starts began to stall out. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 10/19/21 – 8.47%

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The worst market I have ever seen in my lifetime or would hope to see again.” – John J. Phelan Jr.

Futures have been moving higher throughout the overnight session but have taken a slight hit following some weaker than expected residential housing data. In terms of both Building Permits and Housing Starts, the headline numbers came in significantly weaker than expected while August readings were revised modestly lower. Looking at the data, multi-family units look to have been the main driver of the weakness. Despite the weaker data, the 10-year yield is still above 1.6%. Commodities are higher as the dollar falls to its lowest levels of the month. All eyes will be on the crypto space this morning as the first US-based bitcoin ETF debuts today.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Thirty-four years ago today, the S&P 500 experienced what was at the time (and remains now) the largest ever single-day percentage decline losing just over a fifth of its value. The crash of 1987 has a lot of lessons for investors, but one important one is that time is on your side when it comes to investing. If you were a dip buyer and stepped in right at the close on 10/19/87 and held through now, your annualized return, not including dividends, would have been an impressive 9.2%. But what if you had the worst possible timing and decided to get long the market on the Friday before Black Monday? Surely, you would have felt pretty stupid on Monday afternoon. However, if you were able to lick your wounds and put the pain of those losses behind you, and hold through the present, the annualized return of your investment would have still been 8.5% (not including dividends). Sure it’s not as good as you would have done if you waited a couple of days and put that money to work after the crash, but it’s still nothing to turn your nose at. When making investment decisions, sitting on your hands sometimes is one of the better decisions you can make.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

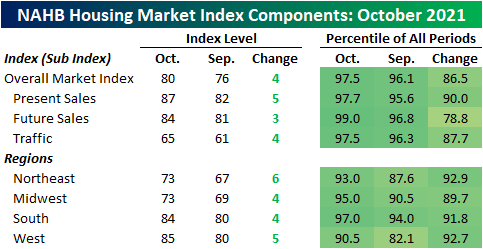

Homebuilder Sentiment Rebounds

Since peaking nearly a year ago, homebuilder sentiment has been in a steady decline, but the past two months have seen a rebound with the October report showing a particularly large jump. The NAHB’s Housing Market Index jumped four points in October to 80 which is the strongest reading since July. That was also a surprise compared to the forecasted one-point decline. While that reading is still well below higher levels of the past year, this month’s reading is back above pre-pandemic record highs.

There were increases in sentiment across all of the various sub-indices. Everything was higher with present sales increasing by the most. While it saw the smallest MoM increase of any part of the report, Future Sales are now the most elevated, coming in the top 1% of readings. Geographically, the South and West have higher homebuilder sentiment readings than the Northeast and Midwest, but all four regions saw big jumps in October.

As homebuilder sentiment has improved, so too have homebuilder stocks. As shown below, the SPDR S&P 500 Homebuilders ETF (XHB) has been rebounding from a near-test of its 200-DMA at the start of the month. Today, it is seeing an outside day reversal higher to fight to move above its 50-DMA. If it does manage to close above its 50-day, it would be the first time it has done so in a month. Even if it crosses that line in the sand, XHB would still only be in the middle of the past several months’ range.

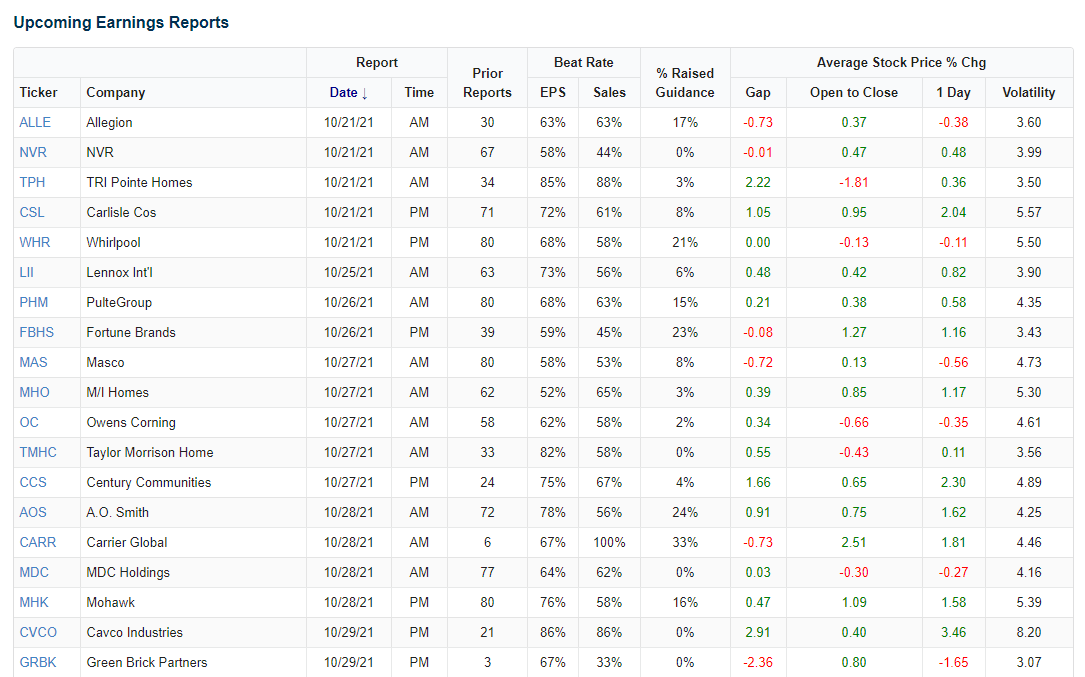

As earnings season ramps up, several XHB stocks are actually reporting in the next few days with many more to come in the following few weeks. We created a custom portfolio with XHB’s holdings, and below we show a snapshot of those holdings in our Earnings Explorer that are scheduled to report through the end of the month. Click here to view Bespoke’s premium membership options.

S&P 500 Market Cap Tops $40 Trillion

The S&P 500’s market cap has increased by more than $6 trillion this year, leaving the index’s total market cap above $40 trillion. As shown below, the Technology sector makes up more than a quarter of the index’s market cap at nearly $11 trillion. The next closest sectors are all right around the $5 trillion mark — Consumer Discretionary, Health Care, Communication Services, and Financials. There are also four sectors that barely add up to $4 trillion combined: Energy, Real Estate, Materials, and Utilities. The four largest stocks in the S&P 500 — Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN) — have a combined market cap that is $8.3 trillion, more than two times the size of the four smallest sectors.

While the Technology sector ranks in the middle of the pack in terms of year-to-date performance, on a market cap basis, it has easily increased the most of any sector this year. As shown below, Tech’s market cap has increased by nearly $1.7 trillion so far in 2021. The next closest sector is Financials with an increase of $1.1 trillion. So far this year, every sector has seen an increase in market cap, with the Utilities sector increasing by the smallest amount at roughly $48.5 billion.

Below is a quick snapshot of the 25 largest stocks in the S&P 500 at the moment. Apple (AAPL) and Microsoft (MSFT) are the two largest and the only members of the “$2 trillion club.” Alphabet (GOOGL) and Amazon (AMZN) rank 3rd and 4th with market caps of more than $1.7 trillion. There’s a big drop-off after the “big 4” of AAPL, MSFT, GOOGL, and AMZN. Facebook (FB) ranks 5th with a market cap of $916 billion, while Tesla (TSLA) has moved up to the #6 spot at $845 billion. With Facebook declining recently and Tesla rallying, the market cap spread between the two is now at just $71 billion. Berkshire (BRK/B), NVIDIA (NVDA), Visa (V), and JP Morgan (JPM) round out the top ten.

As you can see, all of the stocks on the top 25 list now have market caps of $250 billion or more.

In terms of the biggest market cap gainers so far this year, there’s Alphabet (GOOGL) and Microsoft (MSFT), and there’s everyone else. GOOGL has seen the biggest gain in market cap with an increase of $702 billion. There are only six stocks in the S&P 500 that currently have total market caps of more than that amount! The $702 billion gain for GOOGL is also larger than the total YTD gains in market cap for seven of the eleven S&P 500 sectors.

As shown, nine stocks in the S&P have seen their market caps increase by more than $100 billion so far in 2021. Of the 500 stocks in the S&P 500, 411 (more than 80%) of them have total market caps of less than $100 billion. Click here to learn more about Bespoke’s premium subscription services.

Bespoke’s Morning Lineup – 10/18/21 – China Growth Slows

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Uneasy lies the head that wears a crown.” – William Shakespeare

It’s looking like a weak start to trading for the week as futures are firmly lower ahead of the opening bell. We’ve seen a big jump in interest rates over the last two trading sessions as BoE Governor Bailey came out with some hawkish comments related to inflation. In economic data, Chinese GDP came in below forecasts with Q3 growth coming in at just 0.2 on a quarter/quarter basis.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Outside of Communication Services which fell nearly 1%, every other sector within the S&P 500 finished last week higher, and in some cases, a lot higher. Materials, Real Estate, and Consumer Discretionary all rallied more than 3% with the latter also hitting a new high. Every other sector besides Health Care (and Communication Services) were all up by over 1%. In terms of where each sector finished the week relative to its 50-day moving average, they are currently all over the map. Sectors like Consumer Discretionary, Energy, and Financials are all at ‘extreme’ overbought levels while Health Care and Communication Services are still below their 50-DMAs. Even Real Estate, which was the second-best performing sector, still finished the week below its 50-DMA.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.