Bespoke Brunch Reads: 3/7/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Mania

Leading Card Grader PSA Doubles Prices as Industry Booms by Darren Rovell (Action Network)

Two weeks after being sold for a bit less than $1bn, the leading grader of sports trading card quality, has doubled prices and raised minimum batch counts amidst an epic order backlog numbering millions of cards. [Link]

How a 10-second video clip sold for $6.6 million by Elizabeth Howcroft and Ritvik Carvalho (Reuters)

A non-fungible token purchased for $67,000 is telling for 100x that price less than six months after being sold for the first time last fall. [Link; auto-playing video]

First Trust Takes Aim At ARK; Launching Innovation ETF by David Dierking (The Street)

Following in the footsteps of ARK Invest’s extremely successful Innovation ETF (ARKK), ETF giant First Trust has filed for an ETF that takes a similar approach. [Link; auto-playing video]

Meme Stocks

Hertz, the Original Meme Stock, Is Turning Out to Be Worthless by Steven Church (Bloomberg)

The original retail-fueled short squeeze from 2020 saw Hertz declare Chapter 11; that process is now finishing up with equity owners getting nothing. [Link; soft paywall]

Bots hyped up GameStop on major social media platforms, analysis finds by Michelle Price (Business Insider/Reuters)

A Massachusetts-based cyber security company has identified a large number of social media bot accounts helped amplify the craze for GameStop (GME) stock. [Link]

Washington

The Evolution of the Oval Office Décor (American Home Shield)

Ever wonder what the President’s office looked like in the past? Décor changed little in the first half of the 20th century, but since Truman each President has redecorated to suit their personal styles and the fashions of the time. [Link]

Divided Senate Passes Biden’s Pandemic Aid Plan by Emily Cochrane (NYT)

Despite some confusion over specific unemployment provisions that delayed passage Friday, this weekend the Democratic-controlled Senate passed a $1.9trn aid bill that will result in thousands of dollars of aide for the middle class, expanded jobless claims benefits, and is estimated to cut poverty by an astounding one-third this year. [Link; soft paywall]

Whoops

Hey Citi, your bitcoin report is embarrassingly bad by Jemima Kelly (FT)

This week an effort to discuss crypto currency with clients led to some pretty spectacular whiffs from Citi’s research group, including a remarkable mix-up over basis points versus percentage points. [Link; paywall]

The Reemergent 1977 H1N1 Strain and the Gain-of-Function Debate by Michelle Rozo and Gigi Kwik Gronvall (NIH)

During the 1970s, a virulent flu strain that wrecked havoc likely represented a failure of containment at a bio research lab. The genetics of the virus were almost identical to strains first collected decades prior. [Link]

Shifting Gears

‘I’ve Never Seen Anything Like This’: Chaos Strikes Global Shipping by Peter S. Goodman, Alexandra Stevenson, Niraj Chokshi and Michael Corkery (NYT)

Shipping can be a volatile business, but the rapid swings in demand across goods and geographies have created unprecedented chaos across transportation markets around the world. [Link; soft paywall]

How Remote Work Is Reshaping America’s Urban Geography by Richard Florida and Adam Ozimek (WSJ)

Roughly half of Americans are working remotely, and while that share will decline as vaccine rollouts make normal offices safe again, some of the shift will persist amidst a longer-term trend towards the practice of working without going in to a physical desk. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

ARK Invest Still Sitting On Solid Gains, But They’re Sliding Away

The ARK Invest family of ETFs had a stellar 2020 that drew huge inflows. Across the five ETFs issued by Cathie Wood’s company, gains ranged from 105% to 178%, but 2021 has been much less friendly. The flagship ARK Innovation ETF (ARKK) is down 4.9% YTD (and getting worse), with a mixture of gains and losses across other themes. Flows haven’t yet had that kind of round trip: $20bn in 2020, with another $15bn this year (including $2bn of outflows since the peak in February). Looking at the total ARK Invest universe, we can calculate the amount of money investors have gained or lost in aggregate by subtracting flows from market cap. As shown below, back in December investors had a weighted average return of more than 60% across the five ETFs, weighted by the size of purchases. The selloff since has driven that down to just 19% through yesterday. With $15bn entering the funds this year, lots of investors are getting close to or further underwater, and declines could accelerate. So far this year, there’s only been $2bn of outflows, but the money that was quick to come in could just as quickly leave given the recent losses. This blog post is adapted from an analysis included in our nightly Closer report. Click here to start a free trial of Bespoke Institutional to get immediate access.

Bespoke’s Morning Lineup – 3/5/21 – Stronger Than Expected Jobs Report

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“You must not only learn to live with tension, you must seek it out. You must learn to thrive on stress.” – J. Paul Getty

Thankfully, it’s Friday. After another week of declines for equities, futures were modestly positive this morning, but that changed with the release of the February employment report. The bond market was already showing some signs of concern heading into the release, and those concerns look to have been warranted as the headline number came in well above forecasts (379K vs 200K). In reaction to the report, the 10-year yield has risen from a pre-release level of 1.58% to 1.62% now.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, movements in the Japanese bond market, German factory orders, an update on the latest national and international COVID trends, including our series of charts tracking vaccinations, and much more.

Normally, when the equity market comes under selling pressure bonds rally providing some level of cushion to a diversified portfolio. In the last few weeks, though, that still hasn’t been the case. The chart below is from the second page of the Morning Lineup and shows the relative strength of the S&P 500 versus the US Treasury Long Bond Future. In an environment like the last couple of weeks where stocks have been weak, you would expect the relative strength line of the S&P 500 to decline, but so far during this pullback that hasn’t been the case. Despite a 4.6% pullback in the S&P 500, its relative strength versus the Long bond Future remains near 52-week highs.

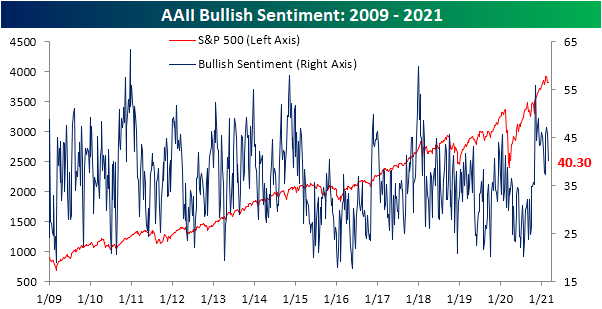

Declines Keep Sentiment in Check

The drift lower in equity prices over the past couple of weeks has resulted in bullish sentiment to similarly turn lower. The AAII’s weekly reading on bullish sentiment fell for the second week in a row this week as only 40.3% of respondents reported as optimistic. That is the lowest level since only the first week of February as sentiment remains above the historical average of 38%.

Just over a quarter of respondents reported a pessimistic outlook this week. That was up 1.5 percentage points from the previous week and the first increase in bearish sentiment in four weeks. Compared to the 5.6 percentage point decline in bullish sentiment (the largest since an 11.49 percentage point drop in November) the move in bearish sentiment was relatively small. In fact, even after the increase, outside of last week, every reading so far in 2021 has been higher than the current reading.

The decline in bullish sentiment drove the bull-bear spread to fall down to 15. That is only the lowest level since the first week of February as overall sentiment remains largely in favor of bulls, albeit less so than earlier this year.

Rather than the bearish camp, those losses to bullish sentiment went to neutral sentiment. 34.4% reported neutral sentiment this week, up 4.1 percentage points from last week. That is the biggest one-week increase and the highest level in neutral sentiment since the week of December 24th

As for the Investors Intelligence survey of newsletter writers, the same sort of moderation in optimism was evident. 53.9% of respondents to this survey reported as bullish this week while bearish sentiment saw a 0.1 point increase to 18.6%; those respectively made for the lowest and highest readings since the first half of November. While that means sentiment still favors bulls, a higher share of respondents are anticipating a correction. That reading rose to 27.5% this week, the highest level since the 29.1% reading for the week of September 23rd which was towards the tail end of a roughly 10% correction for the S&P 500. Click here to view Bespoke’s premium membership options for our best research available.

Claims Coming In After the Storm

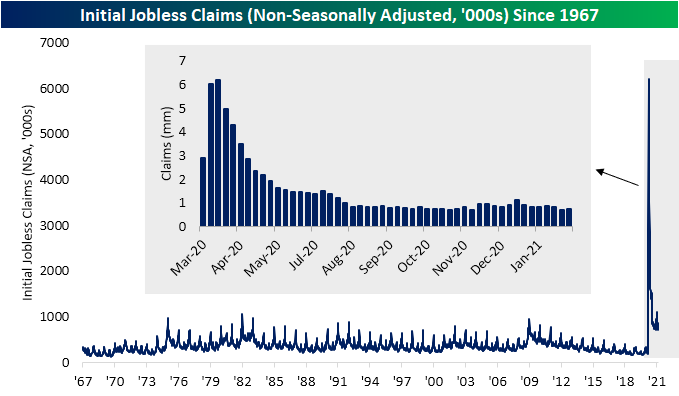

In addition to a higher revision of last week’s number (up 6K to 736K), initial jobless claims were higher this week moving up to 745K. While claims didn’t improve, they did come in 5K better than expectations and they remain around some of the lowest levels since November.

Unadjusted claims were also higher rising 31.5K to 748.1K. Again, in spite of that increase, claims are still at some of their best levels since the fall. Additionally, the current week of the year has normally experienced an uptick week over week. Going back through the history of the data, 72% of the time the current week of the year has seen a WoW uptick in claims.

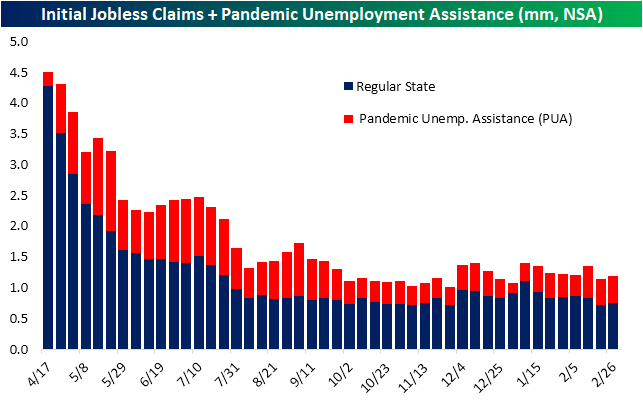

Claims from the Pandemic Unemployment Assistance (PUA) program also saw a slight uptick this week rising from 427.45K to 436.7K. The increases in regular state claims and PUA claims means total initial claims for the most recent week rose to 1.18 million from 1.14 million the prior week.

In the past few weeks, we have noted how state-level claims have seen some interesting quirks like very high readings out of Ohio. Again this week, Ohio was the single largest contributor to the level of national regular state claims followed by California, Illinois, New York, and Texas. Of these states, Texas also saw the largest week-over-week increase in regular state claims potentially as an after-effect of the winter storms in the region. That is after the state actually reported lower claims last week in the immediate aftermath of the storm. Although the Lone Star state saw a big increase in regular state claims, PUA claims saw a less significant uptick. Once again, Ohio saw a much more significant uptick by this measure.

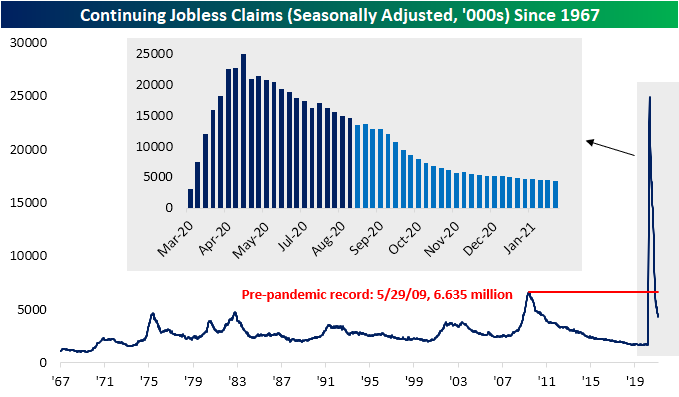

While initial claims have not seen much of an improvement, the decline keeps on coming for continuing claims. This reading for the week of February 19th fell to a new pandemic low of 4.295 million; down 124K from the previous week.

Tacking on all other assistance programs delays the data one more week. For the week of February 12th, continuing claims across all programs were lower at 18.061 million. That is the strongest reading since the week of January 15th when total claims had fallen to 17.873 million. The lower reading in total claims was a result of declines across almost all programs with the biggest decline coming from Pandemic Emergency Unemployment Compensation (PEUC) claims which fell by just over 600K. Click here to view Bespoke’s premium membership options for our best research available.

Treasuries Not Dancing To A Surging Inflation Tune

We’ve seen a lot of commentary suggesting that the recent increase in Treasury yields is being driven by a surge in fears over inflation. While it’s true that worries over inflation should drive bond prices down (higher yields), this recent episode isn’t consistent with that dynamic. In the chart below we show the change in the various segments of the UST curve since the end of October, in basis points. Higher readings indicate steepening, where a longer-term yield rises faster than a shorter-term bond yield. Generally speaking, Treasuries should steepen during inflationary episodes, with longer-term yields (more vulnerable to inflation) rising faster than shorter-term yields (more vulnerable to policy rate changes).

In the chart below we break the UST curve into 4 segments, each of which represents a certain kind of risk premium. Very short-term curvature is dictated by the Fed. As shown, the 3m2y curve has barely moved, because markets generally see the risk of near-term Fed hikes as little-changed over the last four months. The 2y5y curve is similarly tied to Fed policy action, but is much more speculative. As shown, this is where the biggest increase in yields has come. Effectively, the market sees the Fed as much more aggressive in its tightening once it lifts off. The next segment is the 5-10 year curve, which is a mixture of risk premium for Fed policy, growth, and inflation. The 5s10s curve has seen rapid steepening, but the long end of the curve (10s30s), which is most sensitive to inflation, hasn’t budged. If inflation concerns were surging, 10s30s would not be stable over the last few months.

We’ve also included on the chart market pricing for inflation over the five years starting five years from today. While we discourage investors reading too much into this metric as a forecast, it does represent a risk premium for inflation. As shown, this metric for inflation pricing has dropped considerably as yields have risen.

What to make of all this? In our view, the narrative that markets are worried about inflation is inconsistent with Treasury market movements in recent weeks. Instead, we see a market that is pricing in a much tighter Fed once interest rates do start to rise. Whether that will prove true or not is an open question, but what we can say is that inflation expectations are unlikely to be driving bond selling given where changes in yield are taking place on the curve and the performance of inflation pricing over the last few weeks. Interested in fixed income and macro analysis like this post? Click here to start a free trial of Bespoke Institutional to get immediate access to our nightly Closer and Fixed Income Weekly which focus on these markets.

Bespoke’s Morning Lineup – 3/4/21 – One Step Forward, Two Steps Back

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself.” – George Bernard Shaw

After a strong start to March, major US equity indices have given up all or most of those gains in the last two days. Based on where futures are trading now, today may mark a third step backward for the equity market, although not to the same degree as the last two days. Treasury yields, which have been the tail wagging the market lately, are lower this morning with the 10-year US Treasury yield trading right around 1.45%. The economic calendar is jammed packed with Non-Farm Productivity (weaker than expected), Unit Labor Costs (weaker than expected), and Jobless Claims (in line with forecasts) just crossing. Then at 10 AM, we’ll get Durable Goods and Factory Orders at 10 AM. Fed Chair Powell will also be speaking just after noon.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, some earnings reports from the US and around the world, an update on Eurozone labor markets, an update on the latest national and international COVID trends, including our series of charts tracking vaccinations, and much more.

The Technology sector closed below its 50-day moving average again yesterday, and while many tech stocks have been getting slammed of late, the sector is down less than 7% from its closing high in February. The chart of the sector lately looks a bit ominous though. If you squint enough, you can see what looks like a head and shoulders pattern forming over the last several weeks with the neckline also coinciding with the highs from early September. If that breaks, this March, which came in like a bull (briefly), would likely be filled with more bear.

The Energy sector has been a completely different story. The sector remains right near 52-week highs after recently breaking above resistance from its June post-COVID high.

Given the diverging paths of the two sectors, the performance spread between the two sectors over the last six months now stands at 35.3 percentage points, which is the widest margin of underperformance for the Technology sector relative to Energy in nearly 20 years!

Given the diverging paths of the two sectors, the performance spread between the two sectors over the last six months now stands at 35.3 percentage points, which is the widest margin of underperformance for the Technology sector relative to Energy in nearly 20 years!

Brazil (EWZ) Beaten and Battered

Looking across the country ETFs from the 23 countries tracked in our Global Macro Dashboard, most countries have pulled back in the past week though they remain up on the year. But one notable exception has been Brazil (EWZ). EWZ has gotten crushed falling 11.24% in the past five days alone and is now in a new bear market with a 20%+ drop from its 52-week high. Given these steep declines, the ETF is deeply oversold at nearly 3 standard deviations below its 50-DMA. There are only two other country ETFs that are currently oversold: Malaysia (EWM) and Switzerland (EWL). Granted, neither of these are nearly as oversold as EWZ. In fact, EWM is on the cusp of moving out of oversold territory. In addition to these countries, Mexico (EWW) is the only other one that is down year to date. While Brazil is down double digits this year, Taiwan (EWT) has risen over 11.5%. It is the only country ETF to have gained double digits so far this year while South Africa (EZA) and Sweden (EWD) are both closing in on doing the same. China (MCHI) is the next best-performing country this year, but it sits much further below its 52-week highs than the other top performers in 2021. Since the mid-February high, MCHI has fallen 9.6%. In recent days, that decline is resulting in a test of its 50-DMA. Click here to view Bespoke’s premium membership options for our best research available.

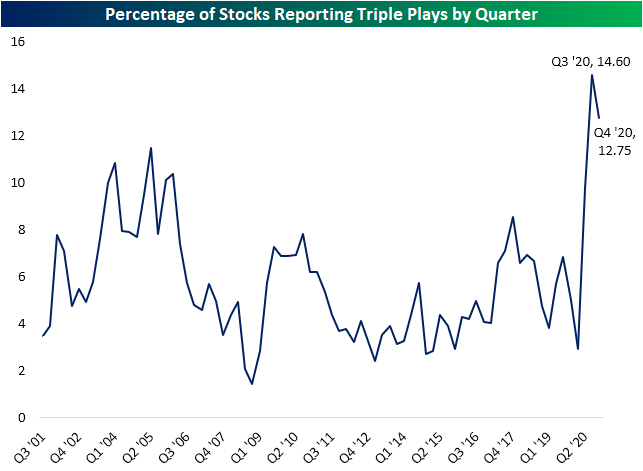

Mixed Results From Triple Plays

Earnings season unofficially came to a close a couple of weeks ago, and as such, the pace of earnings is slowing with the highest number of companies reporting for any day of the next month being March 12th with 47 reports due that day. Looking back on Q4 earnings results, a massive number of companies reported triple plays. A triple play is when a company exceeds analyst forecasts on the top and bottom line while also raising guidance. Using data from our Earnings Explorer tool, 12.75% of all earnings reports were a triple play in the just-completed earnings season. Although that is down from a rate of 14.6% the previous quarter, no other quarter in the history of our data has seen as strong of a number of triple plays.

On a day that the broader market is also trading lower, even triple plays of the past 24 hours are not seeing the best reactions to earnings despite solid results. Since the closing bell yesterday, there have been three triple plays from Hewlett Packard Enterprise (HPE), Veeva Systemes (VEEV), and Ambarella (AMBA). Of these, only AMBA is trading in the green today.

Enterprise software company HPE reported a third triple play in a row last night beating EPS estimates by 11 cents while sales came in at $6.83 billion versus estimates of $6.75 billion. The company also guided higher. While the stock was at a new 52-week high at the open, so far this morning HPE has shifted lower and is now down 1.24% for an outside day. Granted, headed into earnings the stock was and continues to be overbought at around 1.5 standard deviations above its 50-DMA after a substantial run over the past few months. From lows last October through today’s decline, the stock has risen 74%.

Veeva Systems (VEEV) is a cloud-based software solutions company specializing in the life sciences industry. The company has consistently reported triple plays in the past with half of its 30 reports having been triple plays. It is the other triple play that is trading lower today currently down over 4% as of this writing. In addition to raised guidance, the company reported revenues up 27.4% year over year which was around $16 million above forecasts. The company also beat on the bottom line with EPS topping estimates by 15 cents. Unlike the still extended HPE, VEEV has been fluctuating around its 50-DMA in recent days with the sell-off on earnings today bringing the stock to the low end of that range. If the stock continues to head lower, interesting support levels to watch will be the 200-DMA and the lows from the fall.

Not every triple play is trading lower though. Semiconductor design company Ambarella (AMBA) is up around 7.5% after reporting EPS of $0.14 versus $0.08 expected and revenues about $4.5 million above estimates. Shortly after the open, the stock broke out to new highs surpassing the previous highs from mid-February. Since then though, it has pulled back and is now back down around 5% below those highs. Click here to view Bespoke’s premium membership options for our best research available.

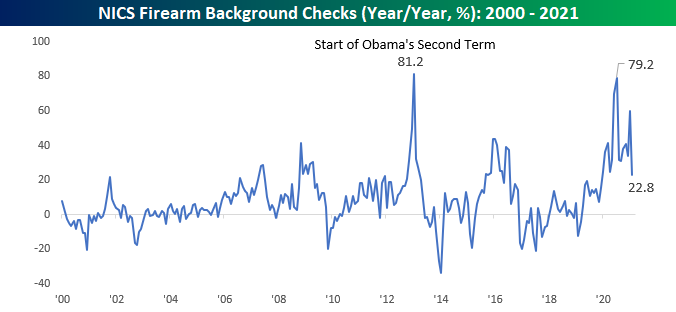

Guns Still Flying Off the Shelves

The latest data on firearm checks from the FBI for the month of February showed that while gun sales eased off from January’s record pace, by all accounts, the pace of gun sales is unlike anything seen prior to 2020. With a total of 3.44 million background checks during the month, February’s pace was down 20% versus January’s record pace. Even with the decline, though, February saw more background checks than all but six other months since 2000, and all of those six months were in the last twelve. For the month of February alone, background checks this year were higher than any other February on record by a margin of over 600K.

On a y/y basis, background checks were up over 22%, and while that’s a significant increase, it actually represents the lowest y/y increase since December 2019. Again, 2020 was a year unlike any other in the last twenty years in terms of Americans looking to buy guns.

With sales still near historically high levels but clearly slowing from the torrid pace of growth in 2020, the stocks of gun manufacturers (SWBI and RGR) have been in a bit of a holding pattern. Both stocks peaked in the middle of last year as protests and riots exploded around the country. They started to rally again after the election right up through early January. Interestingly, the closing high of the post-election rally in both stocks ended on the same day as the Capitol riots on 1/6, and since then both stocks have been drifting back into the ranges they traded in during the second half of 2020. For full access to our research and market commentary, start a two-week trial to our Bespoke Premium service.