Bespoke’s Morning Lineup – 11/18/21 – Philly Fed Jumps

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Trying to sell short in this market is like being run over by a train that’s going to derail a mile down the road.” – Julian Robertson

We may be at the tail end of earnings season, but it’s not going out quietly as we’re seeing some significant earnings-related moves this morning. On the downside, both Cisco (CSCO) and Alibaba (BABA) are down over 6% as they both missed sales estimates and lowered guidance. On the upside, even after the run it has had into earnings, Nvidia (NVDA) is up over 8%. In the retail space, a number of stocks including Victoria’s Secret (VSCO), Kohl’s (KSS), and Macy’s (M) are all up by at least 7%.

Today is also a fairly busy one for economic data as well with Jobless Claims and the Philly Fed at 8:30 and then Leading Indicators at 10 AM. Then, at 11 AM we’ll close out the week’s economic calendar (there are no reports scheduled for tomorrow) with the KC Fed r manufacturing report. Jobless Claims were pretty much right inline with expectations coming in at a post-COVID low of 268K while continuing claims were much lower than expected at 2.08 million. The Philly Fed report also came in better than expected coming in at a level of 39.0 which was the best reading since April.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Relative to last Wednesday’s close, major US equity averages have generally had a positive bias but have seen little in the way of moves in either direction. As shown in our Trend Analyzer snapshot of US index ETFs, the only one that has moved up or down 1% during this period is the Micro-Cap index (IWC) with a decline of 1.17%. Despite the decline, though, IWC remains at overbought levels and is still one of the top-performing ETFs YTD. Behind IWC, the next worst performing index ETF in our snapshot is IWM which is down 0.9% over the last week. Like IWC and every other index ETF listed below, IWM remains at overbought levels, so it’s not as though these moves have been significant.

With small caps and large caps at two different ends of the performance spectrum this week, we wanted to highlight each index’s price chart to show how the moves look from a longer-term perspective. IWM has seen a pretty swift reversal in the last week, but it also follows a short-term move that was much steeper to the upside. Large caps like SPY, on the other hand, saw more gradual (relatively) increases leading up to their recent highs and remain right near all-time highs with the S&P 500 actually coming up just short of a record closing high on Tuesday.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

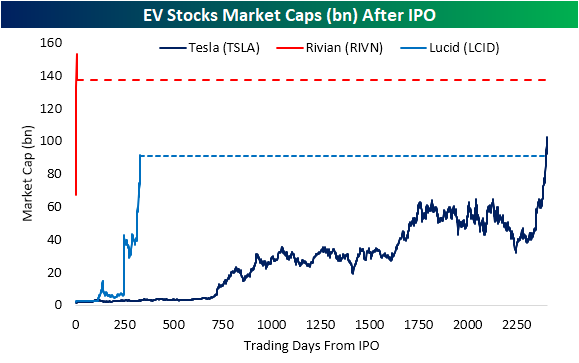

EV Market Caps Disregarding Sales

The newest EV IPO — Rivian (RIVN) — was down 15% today, but it still has a market cap of $125 billion, and it took only three trading days for the stock to close with a market cap of more than $100 billion.

Remember in the mid-2010s when Tesla (TSLA) bears complained about the company’s multi-billion dollar market cap even though it hardly had any revenues? Well, the action in the EV space lately makes those prior Tesla complaints look laughable.

With Rivian (RIVN) now worth over $100 billion after just a few trading days and Tesla competitor Lucid (LCID) worth more than $80 billion, we wanted to highlight how long it took Tesla (TSLA) to trade at a similar market cap. As shown below, it wasn’t until January 13, 2020 that TSLA’s market cap first crossed above Lucid’s current market cap, and TSLA didn’t cross above Rivian’s (RIVN) market cap until February 2nd, 2020. While it took Tesla 2,407 trading days from its IPO to hit $100 billion in market cap, it only took three trading days for RIVN to do the same.

When Tesla first reached $100 billion in market cap in January 2020, the company had reported revenues of $7.4 billion in the most recent quarter. RIVN and LCID, on the other hand, are still considered “pre-revenue” companies!

The rise of the electric vehicle is an overarching trend that consistently finds its way into the headlines. As shown below, Google Trends scores for terms like “Electric Car” and “EV” are approaching record highs and have more generally been grinding higher over the past few years with particular acceleration in 2020 and beyond.

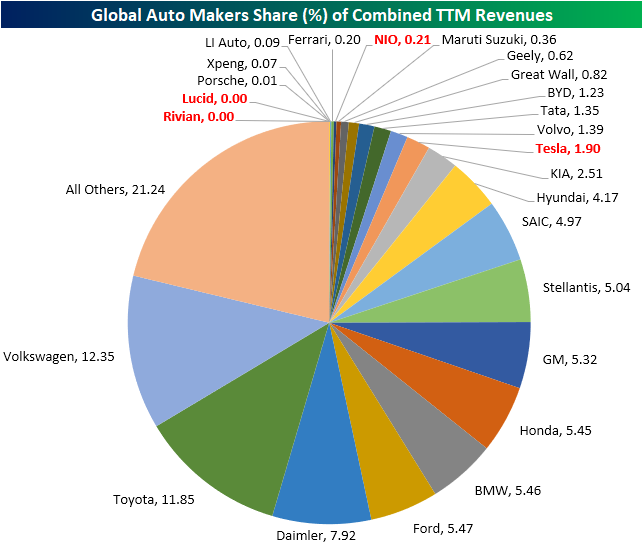

The past couple of months has seen plenty of EV stock headlines ranging from the surge in Tesla (TSLA) as it eclipsed a $1 trillion market cap and the strong IPO of Rivian (RIVN). As a result of the strong performance of these stocks, looking at the largest global automobile manufacturers by market cap, EV names now have a significant presence. In fact, of a universe of 118 global auto stocks with market caps of at least $100 million (USD adjusted), 42% of the combined market cap is made up of four EV names—Tesla (TSLA), NIO (NIO), Lucid (LICD), and Rivian (RIVN). TSLA is of course the bulk of this with nearly a third of that total share, but Rivian (RIVN) is also high up on the list ranking as the third-largest of any single auto stock, and that is only after trading for a few days!

With that said, those valuations are pretty extreme when compared to sales (again USD adjusted). In the chart below, we show the same stocks but as their share of the group’s trailing 12-month revenues. As shown, the most legacy company of the EVs, TSLA, only made up for 1.9% of the industry’s revenues. NIO is the only other one with any sales to speak of.

Obviously, there is a major disconnect between these stocks’ sales figures over the past year and their market caps. Traditional automakers are bringing in far higher revenues than EV’s which for whatever reasons (rational or not) are not being reflected in market caps. Click here to view Bespoke’s premium membership options.

Stocks Most Impacted by 7-10 Year Treasuries

Since the beginning of the pandemic, investors have consistently discussed the relationship between treasury yields and the performance of equities. Of course, every company is different, and there are some companies that benefit from higher Treasury yields while others outperform when rates decline.

The table below summarizes the S&P 500 members that perform best when the iShares 7-10 Year Treasury Bonds ETF (IEF) loses value. We measure this by calculating the correlation coefficient of individual stock prices against the price of IEF since the start of 2020. In other words, when rates increase (IEF price declines), these stocks experience positive price movement. M&T Bank (MTB), American Airlines (AAL), and Hewlett Packard (HPE) top this list, and all the names on this list have high correlation coefficients implying that they are closely tied to the performance of IEF on an inverse basis. Other notable names on this list include Ralph Lauren (RL), Citigroup (C), Fox Corp (FOX), and Tyson Foods (TSN). Of the 20 companies on this list, six come out of the Industrials sector and 5 are from the Financials sector. The average YTD performance of the names on this list through 11/15 was a gain of 31.1% (median: +25.2%).

To help you visualize exactly what we are looking at, take a look at the chart below. MTB is the stock most inversely correlated to IEF. Since 2020, it has routinely moved in the opposite direction as IEF. When IEF moves up, MTB tends to decline, and vice-versa. If you believe that treasury yields will rise, MTB and the other names on the list are ones that have historically benefitted in that environment.

The next table shows the S&P 500 stocks that have benefitted during periods of falling yields, which would be represented by an upward move in the price of IEF. The stocks on this list are generally less correlated to the movements of IEF, so the correlation coefficients are less statistically significant. The average returns for the stocks on this list on a YTD basis is a decline of 1.9% (median: -2.1%) through 11/15. Clorox (CLX), Vertex (VRTX), and Incyte (INCY) have the highest correlation coefficients to IEF, and other notable names include Regeneron (REGN), MarketAxess (MKTX), and General Mills (GIS). 7 of the 20 companies on this list are from the Consumer Staples sector, 4 are in the Health Care sector, and 3 are in the Real Estate sector.

As you can see, the price movements between CLX and IEF have been quite similar since the start of 2020. While prices of CLX and IEF have been well correlated since the start of 2020, we would note that outside of the first five stocks on the list, none of the other names listed have a correlation coefficient of more than 0.5 indicating that the relationships are not nearly as strong as the names on the first list above. In terms of both lists, the correlation coefficients are simply telling us how each stock has traded with respect to IEF since the start of 2020, but whether those relationships hold up going forward is uncertain, Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 11/17/21 – Soft Housing Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Trying to sell short in this market is like being run over by a train that’s going to derail a mile down the road.” – Julian Robertson

Futures have been weakening as we write this and are now pointing to a negative open ahead of some important housing data at 8:30 AM. Housing Starts came in at 1.52 million annualized which was weaker than expected and the second straight month that the headline reading missed expectations. Building Permits also missed forecasts for the second straight month coming in at a level of 1.630 million versus forecasts for a rate of 1.644 million.

In earnings news, both Lowes (LOW) and Target (TGT) reported earnings this morning, and while both reports were better than expected, concerns over margins at TGT have that stock trading down over 3%.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

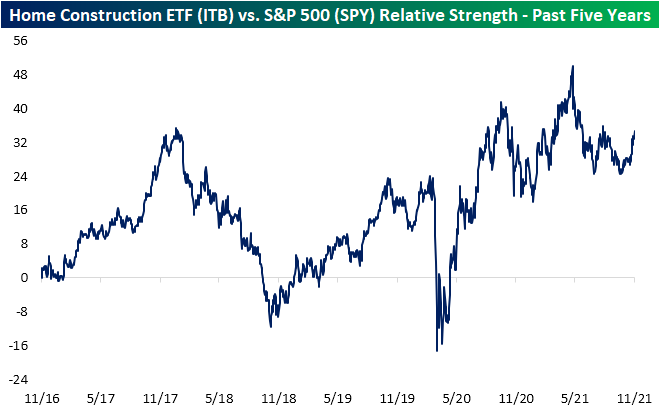

Ahead of today’s reports on Building Permits and Housing Starts for October, yesterday’s release of homebuilder sentiment for November came in significantly stronger than expected suggesting that the recent uptick in interest rates hasn’t deterred potential homebuyers. Rising rates also haven’t had a negative impact on homebuilder stocks recently either. In yesterday’s trading, the iShares Home Construction ETF (ITB) didn’t quite trade at a new intraday high, but it did manage to hit a new high on a closing basis. Meanwhile, the S&P Homebuilders ETF (XHB) not only hit a new intraday higher yesterday, but it has been trading at new highs on a pretty regular basis in recent days. Unlike ITB, which is more of a pure-play on homebuilders, XHB has more exposure to companies like Home Depot (HD) and Lowes (LOW) that supply homebuilders as well.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Homebuilder Sentiment Improves as Homebuilder Stocks Breakout

The NAHB released its November reading on homebuilder sentiment this morning. For the third month in a row, sentiment has improved with the index now at a six-month high of 83.

It has now been a full year since the index last hit a record high of 90. While off the peak, the current reading is still extremely strong from a historical perspective in the top 2% of readings. The same goes for the sub-indices. Present sales and traffic were both higher again this month while Future Sales went unchanged. That index has been notably flat over the past few months, stuck at 81 from July through September and now 84 in October and November.

Based on geography, most of the country saw an improvement this month. The only region where sentiment declined was the Northeast (-4). The Northeast is also the only region that is not in the top decile of its historical range after giving up most of the prior month’s gain. The South currently has the strongest reading in the top 1% of readings.

As for homebuilder stocks, the iShares US Home Construction ETF (ITB) is attempting to break out from a six-month period of consolidation. As shown below, ITB is rallying 1.74% today bringing it above the May 10th high closing high but still below the intraday high While near all-time highs, the group is extremely overbought trading 2.5 standard deviations above its 50-DMA following the 18% rally off the early October low when ITB briefly traded below its 200-DMA. With a strong run so far this quarter, only two of the ETF’s 50 holdings are in the red this quarter: Leggett & Platt (LEG) and Lumber Liquidators (LL). The former is down not even one percentage point though.

ITB has also bottomed out and been making a sharp move higher on a relative basis versus the S&P 500 (SPY). After several months of declines, in early October, the relative strength line held up around the same levels as the July lows. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 11/16/21 – Retail Detail

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If everybody is doing it one way, there’s a good chance you can find your niche by going exactly in the opposite direction.” – Sam Walton

Home Depot (HD) and Walmart (WMT) are on the tape this morning as earnings season winds down. Both companies reported better than expected results on both the top and bottom lines. WMT even raised guidance citing strong results in its eCommerce unit. In reaction to the reports, both stocks are modestly higher with gains of between 1.0% and 1.5%.

Retailers are dominating the earnings headlines this morning and Retail Sales will dominate the economic data as well. There are a number of other reports on the calendar for today (Import Prices, Capacity Utilization, Industrial Production, Business Inventories, and Homebuilder Sentiment), but Retail Sales will kick the day off and likely be the most important release for investors.

Ahead of all the data, US equity futures are flat to modestly higher on the morning, treasury yields are modestly lower, and crude oil is back above $81. The real action this morning has been in the crypto space as most major currencies are down at least 5%. Bitcoin briefly dropped below $59K and tested its 50-day moving average but has rebounded back above $60K since. Factors being cited for the move include the stronger dollar and another round of regulatory crackdowns in China as the government refers to crypto mining as ‘extremely harmful’.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

We reached the mid-point of Q4 yesterday, and it’s hard to find much to complain about if you are a bull. Besides the fact that SPY is already up nearly 9%, four sectors have rallied by double-digit percentages. Looking at these four sectors, though, they aren’t necessarily ones you would look at as typically rallying in unison with each other.

With inflation being the number one concern of investors these days, the fact that Materials and Energy are near the top of the list in terms of performance shouldn’t come as much of a surprise, but the fact that they are accompanied by Consumer Discretionary and Technology is a bit surprising. Consumer Discretionary is a sector that typically underperforms during inflationary periods, but it’s actually the top-performing sector so far this quarter. Similarly, Technology, which is usually associated with growth stocks that should come under pressure when inflation is a concern as future earnings are discounted at a higher rate, has rallied nearly 12%.

Given some of the enormous market caps of some of the largest stocks in the S&P 500, some of the sector performance figures are skewed a bit. Consumer Discretionary is a perfect example. With Tesla’s (TSLA) market cap topping a trillion dollars recently, the stock’s weight in the sector is above 15%, so the fact that it has rallied more than 30% already this quarter (even after dropping 18% in less than two weeks) is a big reason for the sector’s outperformance. Within the technology sector as well, some of the largest stocks in the index have much more reasonable valuations than many other smaller names within the sector and given their dominant positions, they also have attractive earnings profiles.

On the downside, there is none so far this quarter, but the only two sectors that are up less than 5% so far on the quarter are Communication Services (XLC) and Health Care (XLV).

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

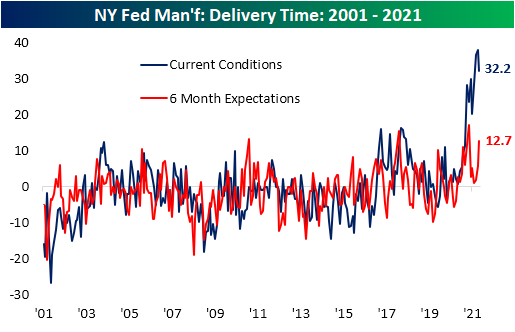

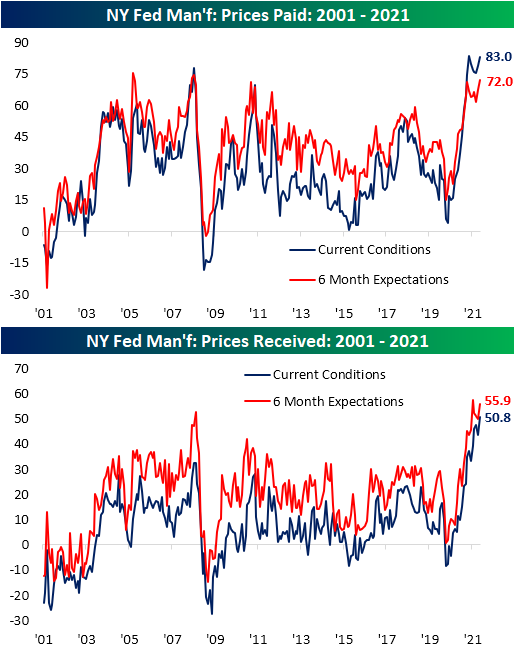

NY Fed Current Conditions and Expectations Split

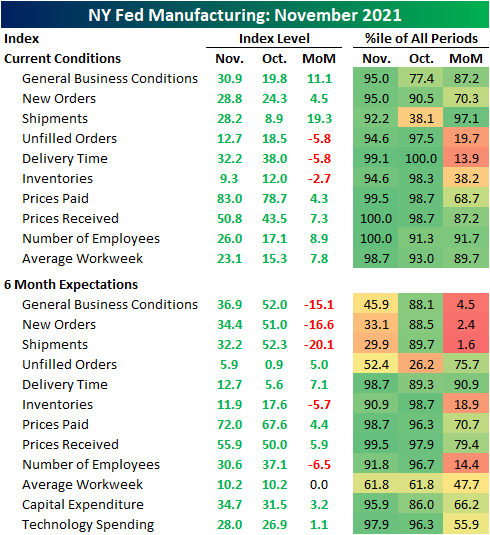

The New York Fed put out the first regional reading on manufacturing this morning with a big upside surprise. The Empire State Manufacturing Survey jumped from 19.8 to 30.9 in November versus a much smaller expected increase to only 22. As shown below, November’s level is indicative of a historically healthy growth rate for Northeast manufacturing and acceleration relative to October. While growth picked up in November, it remains in the middle of the range of readings from the past several months.

Although it was generally a strong report, one striking element was massive declines in optimism, specifically regarding the six-month expectation indices of General Business Conditions (red line above), New Orders, and Shipments. The month-over-month drop in each of those indices ranks in the bottom 5% of all monthly moves. While that may sound scary, the readings were pretty much outliers relative to the rest of the report. Current condition indices and most other expectations indices remain strong with the vast majority sitting in the upper decile of their historical range; a couple (Prices Received and Number of Employees) even hit record highs.

Current conditions for demand were historically strong and improving in November with New Orders rising 4.5 points to 28.8 while Shipments saw a huge 19.3 point leap to 28.2. That move brought the index from the 38th percentile all the way up to the 92nd. In spite of those improvements, responding firms took a sharply negative turn with regard to outlook. Like the headline index, expectations for new orders, and shipments took sharp turns lower in spite of the improvements in current conditions. The last time that all three of those indices experienced as large of declines simultaneously was back in March 2018. Back then, the catalyst for the big hit to sentiment was a rollercoaster of headlines regarding the trade war with China.

Supply chains remain strained as evident from the extremely elevated reading on Delivery Times. That being said, the index did pivot lower off of a record high in November. That improvement was likely a factor in the big increase in current conditions for shipments. Again though, the outlook is less optimistic with Delivery Time expectations surging back up to one of the highest readings on record. As with current conditions, that could be a part of the reason expectations for shipments coincidentally plummeted.

Given longer lead times, prices resumed their rise this month. Prices Paid came in only a half point below May’s record high while expectations rose to the fourth highest reading on record; the highest since July 2008. Prices Received, meanwhile, set a new record high for current conditions and expectations came in at the second-highest level on record behind July’s level.

Another part of the survey that saw big opposing moves in current conditions and expectations concerned employment. Six-month expectations for Number of Employees fell to a new short-term low of 30.6 as the current conditions index set a new record high. Average Workweek also increased and is now slightly below the September high.

While expectations for hiring people may have been on the decline, companies appear to be offsetting that with an increase to other spending. As shown below, both CapEx and Tech Spending were higher this month with the former notching the strongest reading since January 2018. Before that, it was over a decade ago that Capital Expenditures was as elevated as it was this month. Click here to view Bespoke’s premium membership options.

Small and Mid Caps Gain Ground

Equities broadly have been in rally mode so far this quarter, but in the month of November smaller market caps have generally outperformed. Month to date, the small-cap S&P 600 ETF (IJR) has gained 5.88% as of this morning while the mid-cap S&P 400 ETF (IJH) has risen 4.21%. Large caps as proxied by the S&P 500 (SPY), meanwhile, are up less than 2% MTD. While there is plenty of time left in the month for things to change, the spread between the month-to-date performance of small and mid-caps versus large caps is on pace to be on the wider side of all months of the past twenty years. As shown in the charts below, IJR is currently outperforming SPY MTD by 4.05 percentage points, and that reading is 2.37 percentage points for IJH versus SPY. Those rank in the 91st and 86th percentiles, respectively, of all months of the past twenty years. That also marks the first month with significant outperformance of smaller market caps relative to large caps since the stretch of large-cap underperformance that ran from the fall of last year through this past February. Prior to that, you would have to go back to March 2018 to find the last time that small and mid-caps both outperformed large caps by as much as they are this month. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 11/15/21 – Earnings Season: The Final Stretch

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The challenge of the retail business is the human condition.” – Howard Schultz

We’re heading into the final days of earnings season this week, and so far the results have been very positive. Whether earnings season ends on a positive note or not will depend on how the market reacts to a slew of high profile earnings reports from the retail sector – most notably Walmart (WMT) and Home Depot (HD) on Tuesday, Lowe’s (LOW) and Target (TGT) on Wednesday, and then Kohl’s (KSS) and Macy’s (M) on Thursday. Consumers still appear to be in a strong financial position but as last week’s sentiment report from the University of Michigan showed, they aren’t feeling particularly optimistic. And as the quote above implies, consumer sentiment is the key to retail sales.

Futures are higher to kick off the week, and it’s a slow day for economic data with Empire Manufacturing the only report on the calendar, and it came in better than expected. The 10-year yield is modestly lower this morning and WTI is down over $1 and back below $80 per barrel.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Speaking of oil, the recent pattern for WTI has been interesting. With the commodity having basically doubled over the last year, it’s hard to say anything negative about its performance, but we would note that the most recent peak in late October coincided right with its trendline of higher highs since the beginning of the year. Since that peak, though, the recent pullback has seen WTI break its short-term uptrend line from the most recent low in August. As it attempted to bounce back in mid-November, the rally stalled out right at that former uptrend line. The key level to watch going forward will be right around $78.50 which would represent a lower low. As long as that level holds in the short-term energy bulls probably don’t have a lot to worry about, but it’s a level that should be kept on the radar.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 11/14/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

The Future of Labor

Trapped in the Metaverse: Here’s What 24 Hours Feels Like by Joanna Stern (WSJ)

This video gives you an idea of what the world of working inside the offering of Meta (nee Facebook) might be like. [Link; paywall]

Six questions that could shape the future of the U.S. labor market by Jonnelle Marte (Reuters)

The COVID pandemic has driven a big shift in how the US labor market works. Here are some indicators and concepts to keep an eye on as the economy continues to evolve away from the pandemic recession. [Link]

DIY

How To Make A CPU – A Simple Picture Based Explanation (Robert Elder)

Ever curious where the chips which are fowling up so much of the global economy with their shortages come from? Here’s a step-by-step walk-through of how to make them from rock to final installation. Best of luck actually doing this yourself! [Link]

I Have Achieved a Glorious Victory Against the Music Industry and Twitter by Mark Joseph Stern (Slate)

While DMCA takedowns create all sorts of nuisance for social media users, there is a way to fight back; the author demonstrates the successful way to prove a point about fair use and copywrite laws. [Link]

Petty Crime

Scammer Convinced Instagram That Its Top Executive Was Dead by Joseph Cox (Vice)

In an illustration of how absurd the current management of social media networks has gotten, a scammer successfully managed to convince Instagram that their boss had died using a fake obituary. [Link]

‘It’s a great big mess’: Catalytic converter thefts rampant in the Bay Area by Michelle Roberson (SFGate)

An insurer reports thousands of catalytic converters (which prevent smog) are being stolen from California automobiles, with thefts more than doubling over the past year. [Link]

Conspicuous Consumption

The Mystery of the $2,000 Ikea Shopping Bag by Silvia Bellezza and Jonah Berger (Harvard Business Review)

Luxury brand Balenciaga offers a $2000 version of the ubiquitous reusable bags offered by Ikea, offering a fascinating insight into the psychology and branding of super high-priced goods. [Link]

The open secret to looking like a superhero by Alex Abad-Santos (Vox)

An investigation into the rampant use of steroids by men in Hollywood, which has become part of the cost of starring in shows or movies; the increase in steroid use also speaks to broader trends in mounting social pressures on men to conform to a specific body image. [Link]

Supply Chains

Bottlenecks: causes and macroeconomic implications by Daniel Rees and Phurichai Rungcharoenkitkul (BIS)

A helpful analysis about the macroeconomic effects of the pandemic and resulting bottlenecks in supply chains. [Link; 9 page PDF]

Thanksgiving Dinner Staples Are Low in Stock Thanks to Supply-Chain Issues by Stephanie Stamm (WSJ)

Turkeys, pies, and other Thanksgiving staples are hard to find on grocery store shelves this year as supply chain disruptions ripple through the economy. [Link; paywall]

Ancient Cooking

Culinary Detectives Try to Recover the Formula for a Deliciously Fishy Roman Condiment by Taras Grescoe (Smithsonian)

Romans were obsessed with a condiment called “garum”, which is similar to modern Asian fish sauces but involves a slightly different process. The umami-rich additive has finally been reproduced after falling out of favor over a thousand years ago. [Link]

Unintended Consequences

Investors Pushed Mining Giants to Quit Coal. Now It’s Backfiring by Thomas Biesheuvel (Bloomberg)

As larger, publicly-traded companies abandon coal under pressure from investors, smaller private companies willing to mine the carbon-heavy energy resource are stepping in to the fray. [Link; soft paywall]

YOLO

Rich Millennials to Financial Advisers: Thanks for the Golf Invite, but You Can’t Invest My Money by Rachel Louise Ensign and Peter Rudegeair (WSJ)

Aggressive, liquid young investors are forgoing traditional money managers in favor of running their investments themselves. As the old aphorism goes: everyone’s a genius in a bull market. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!