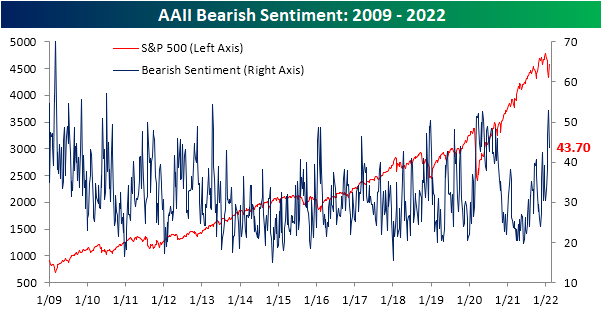

A Little Less Negative

While the S&P 500 and other major indices are being pulled lower today, the past week has generally seen them reverse some of January’s losses, and as a result, sentiment has become modestly more optimistic. The AAII sentiment survey showed bullish sentiment tip back above a quarter of respondents in the most recent week rising to 26.5%.

Bearish sentiment meanwhile fell back to 43.7% after hitting the highest level since April 2013 last week.

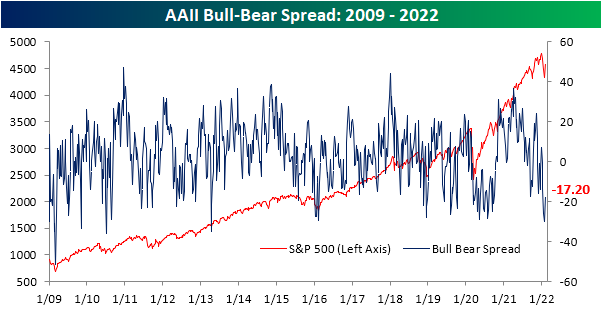

While bulls and bears both moderated in the most recent week’s survey, investor sentiment remains largely bearish. The bull-bear spread rose but remains deeply negative at -17.2. At that level, the bull-bear spread remains in the bottom 8% of all readings in the history of the survey.

While bulls did borrow from the decline in bearish sentiment, a larger share reported neutral sentiment this week. That reading rose six percentage points to 29.9% which is the biggest increase since the second week of December, but that level is still below the 30%+ readings that were common throughout the final quarter of 2021.

Other sentiment surveys like the Investor Intelligence survey of equity newsletter writers and the NAAIM Exposure Index, also saw a rebound in bullish sentiment this week which led our sentiment composite to regain some of the recent large declines. As with the AAII survey though, sentiment remains at a fairly bearish level in spite of this week’s improvements. Click here to view Bespoke’s premium membership options.

Berkshire (BRK/B) Unseats Meta (FB) For S&P 500’s Sixth Largest Stock

Yesterday, the news of the day was Alphabet’s (GOOG) massive gain on earnings that added $132 billion in market cap. The gain pushed Alphabet closer to the $2 trillion market cap club, which currently has two other members: Apple (AAPL) and Microsoft (MSFT).

Today, another mega cap Tech stock is in the spotlight for the opposite reason. After reporting weak quarterly results and forward guidance, Meta Platforms (FB) has shed over $225 billion in market cap. Given that is the stock’s worst single-day drop in its history as a public company, it is also the largest single-day drop in its history in terms of market cap. As a result of the decline, Berkshire Hathaway (BRK/B) has unseated FB for the S&P 500’s sixth-largest stock. At the moment, Berkshire’s market cap of ~$710 billion is more than $20 billion higher than Facebook’s (FB) $687 billion market cap.

Since the end of last year, BRK/B has actually now risen two spots in the rank of S&P 500’s largest stocks, eclipsing both Facebook (FB) and NVIDIA (NVDA). As for some other notables, Exxon Mobil (XOM) and Coca-Cola (KO) have made huge jumps in the rankings this year, rising 10 and 9 spots, respectively, to break back into the top 20 list. Looking at the change in rankings over the past couple of years, NVIDIA (NVDA) has also notably risen through the ranks at a very rapid pace, jumping 31 spots since the end of 2019. While Tesla (TSLA) was not a part of the S&P 500 at the end of 2019, taking where it would have ranked in the index back then, its 79-spot jump is even more impressive. Click here to view Bespoke’s premium membership options.

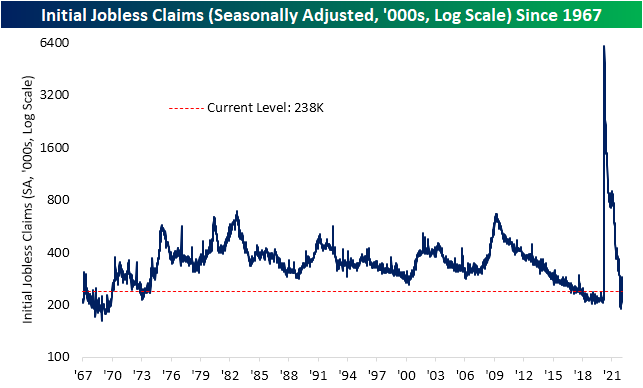

Claims Looking Healthier

Jobless claims spiked higher in early January, but the second half of the month saw some of that unwind with the most recent reading through the week of January 29th showing a drop to 238K from the previous week’s upward revised reading of 260K. That means claims have improved over the past couple of weeks and are still at a historically healthy level even if they remain off the pre and post-pandemic lows.

On a nonseasonally adjusted basis, after two weeks of smaller declines than what has historically been the norm, claims fell 11.7K WoW to 257K which was a larger drop than what could have been expected for the given week of the year (average decline of 4.89K since 1967). Heading into the next several weeks, NSA claims will continue to have seasonal tailwinds at their back while declining COVID caseloads will also likely help improve the claims situation.

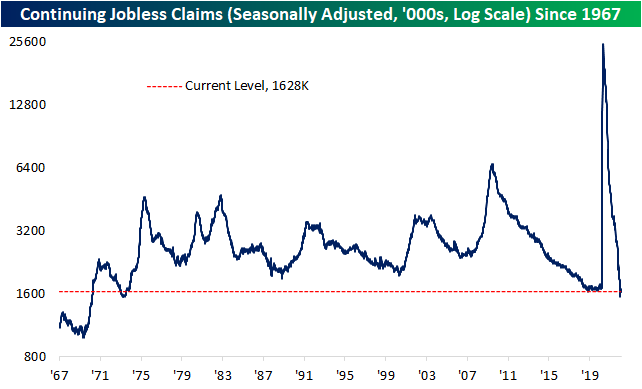

Delayed an extra week, continuing jobless claims continued to sit at the low end of the past several decades’ range. Seasonally adjusted continuing claims fell 44K this week down to 1.628 million. That is now slightly above the absolute low of 1.555 million set in the first week of January. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 2/3/22 – It Was Fun While it Lasted

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There are decades where nothing happens, and there are weeks where decades happen.” – Vlad Lenin

Good Morning Subscriber,

This earnings season, you could even say there are after-hours sessions where decades happen. Between earnings reports from Netflix (NFLX), PayPal (PYPL), and Meta Platforms (FB) last night, some very large market cap stocks have lost a fifth of their value overnight. These kinds of declines in reaction to one quarter’s worth of corporate performance are not exactly normal market events, and in the case of FB, today’s decline could be the largest single-day decline in market cap for a single stock in history! These are some unprecedented moves, and we’re not even halfway through earnings season!

We have a busy day of economic data ahead as well with Non-Farm Productivity, Unit Labor Costs, Jobless Claims, ISM Services, Durable Goods, and Factory Orders. Jobless Claims were already released and came in right around expectations while Non-Farm Productivity topped forecasts and Labor Costs were lower than expected. Following last month’s weaker than expected ISM Services report, the headline index is expected to show further deceleration this morning but still come in at a healthy reading of around 60.0. Durable Goods and Factory Orders, meanwhile, are both expected to show declines of less than 1%.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Yesterday looked like an encouraging day for the Nasdaq 100 as the index traded and closed back above its 200-DMA, but that’s unlikely to last long as the index is expected to gap down more than 2% at the open this morning putting it back below its 200-DMA.

Going back to 2000, today will likely be the Nasdaq 100 ETF’s (QQQ) 106th downside gap of more than 2%. In the charts below, we show its performance from the open to close on the day of prior downside 2%+ gaps broken out by weekday along with the frequency of positive returns for each day of the week. Overall, the best day for QQQ to gap down 2% has been Wednesday as it has averaged a gain of 1.52% from the open to close with positive returns 54.5% of the time. Average intraday gains on Tuesday haven’t been nearly as strong (0.42%), but QQQ has been more consistent to the upside with gains 60% of the time. Unfortunately, Thursdays haven’t been a very good day for QQQ to gap down 2%+. On those 17 prior occurrences, QQQ’s average performance from the open to close has been a decline of 0.02% with positive returns less than a third of the time.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

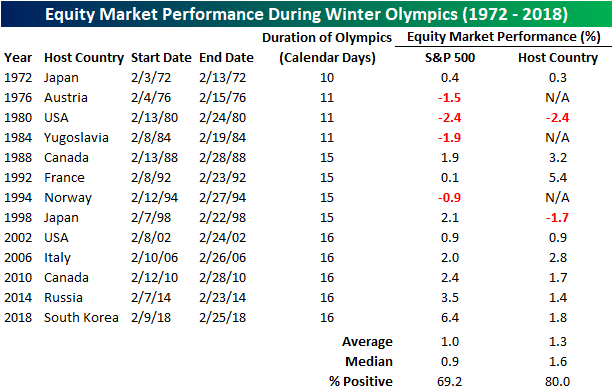

Performance During Winter Olympics

Are you ready for the Olympics? The 2022 Winter Olympics will kick off this Friday, and with that, we wanted to provide an update on how equities typically perform during the winter games. In the table below, we list the start and end dates of every Winter Olympics since 1972 and show the performance of the S&P 500 and the host country’s benchmark stock index during each one. For the S&P 500, performance has tended to be positive with an average gain of 1.0% (median: 0.9%) and positive returns just under 70% of the time. Compared to all two-week periods over that same period (average: +0.4%, median: +0.6%), these returns are better than average.

For the host country, stock market performance has also been strong. Since 1972, the host country of the Winter Olympics has had an average gain of 1.3% (median: 1.6%) with positive returns 80% of the time. The most notable outperformance came in 1992 when French equities rallied 5.4% during the Albertville games while the S&P 500 gained just 0.1%. On the other hand, the S&P 500 considerably outperformed South Korean equities in the 2018 Games in PyeongChang, resulting in a performance spread of 4.6%. In fact, in each of the three most recent Winter Olympic Games, US stocks outperformed stocks in the host country by an average of 2.5%. Countries often bid to host the Olympics in order to shed a positive light on their country, but it hasn’t always helped their stock markets outperform in the short run. To track the performance of China during the Olympic Games this year (starts on 2/4 and ends on 2/20), subscribe to Bespoke Premium today to gain access to our trend analyzer & chart scanner.

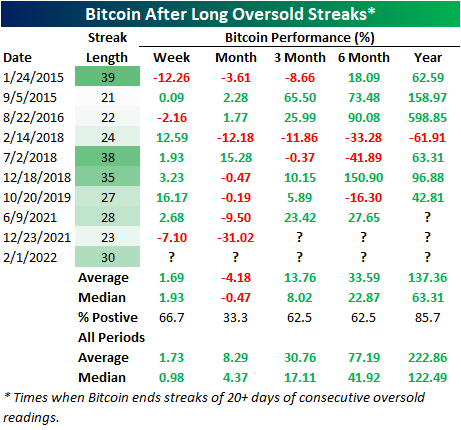

Bitcoin Oversold for a Month Straight

Bitcoin has rallied over 10% since the low a little over a week ago, but that still leaves the world’s largest cryptocurrency down over 40% below its all-time high set back in November. In fact, the past few months have seen Bitcoin trade in a steep well-defined downtrend which the rally over the past several days rally has now run up against.

While that downtrend line has the potential to act as resistance, the steep drop has resulted in Bitcoin consistently trading at oversold levels (measured in standard deviations from its 50-DMA). In fact, today marks the 30th consecutive day in which Bitcoin has traded at least one standard deviation below its 50-DMA.

As for the consistency of oversold readings, there have only been ten streaks including the most recent one in which Bitcoin has been oversold for at least 20 straight days. The current stretch is now the longest since December 2018. Other than that streak, only those ending in January 2015 and July 2018 also extended for at least 30 days.

While the current streak is not over, in the table below we show the performance of Bitcoin after the end of those past streaks of oversold readings that went on for at least 20 days. As shown, the end of those streaks have typically seen a bounce in the week after with positive returns two-thirds of the time and gains that are in line with the historical average. One month later has typically seen the crypto fall further, though, with positive performance only a third of the time. Three and six-month performance have been more consistent to the upside with positive returns nearly two-thirds of the time but average and median gains that are smaller than what Bitcoin has averaged across all other three and six-month periods since 2014. One year later has been a similar story with below average forward returns but a very high consistency of positive returns. Click here to view Bespoke’s premium membership options.

Bespoke Market Calendar — February 2022

Please click the image below to view our February 2022 market calendar. This calendar includes the S&P 500’s average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases. Start a two-week free trial to one of Bespoke’s three research levels.

Meme Stock Mania Anniversary

Last week was the most recent update of short interest data through mid-January, and that came on the one-year anniversary of the height of the meme stock mania when highly shorted stocks like GameStop (GME) experienced historic short squeezes. The year since then has not been kind to heavily shorted names. The Bloomberg High Short Interest index tracks the 100 US stocks with the highest short interest as a percent of float with monthly rebalancing. As shown below, since the height of meme stock mania on January 27th of last year, this basket has now been more than cut in half!

Although highly shorted stocks have performed terribly in the past year, the level of short interest across multiple industry groups is well below where it stood prior to last year’s short squeeze. As shown below, levels of aggregate short interest for each industry group were little changed in the first two weeks of the year, but are also a fraction of what they were at the end of 2020.

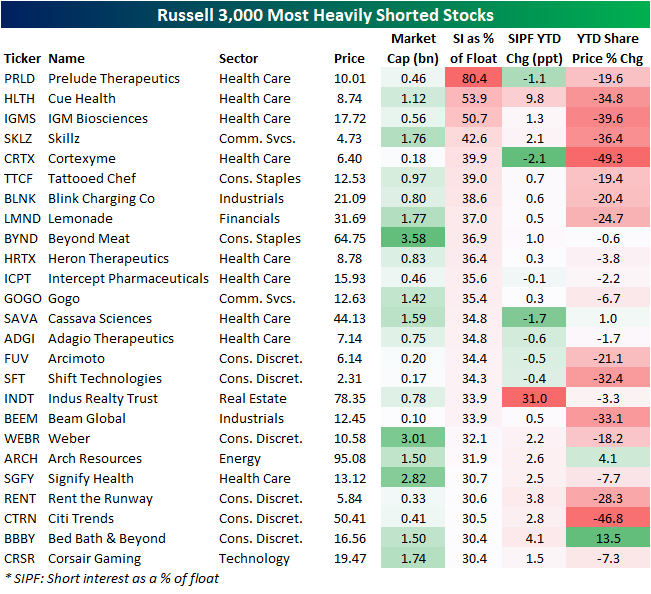

Below we show the stocks that currently have the highest levels of short interest of Russell 3,000 members. Prelude Therapeutics (PRLD) tops the list with more than 80% of float shorted. That is actually down slightly versus the last reading through the end of 2021. Cue Health (HLTH) and IGM Biosciences (IGMS) are the only other stocks with over half of their shares shorted. Those two, as well as several other highly shorted stocks, are down over 30% in January. The two worst decliners are Citi Trends (CTRN) with a 46.8% loss and Cortexyme (CRTX) which has nearly been cut in half. As for the meme stock mania posterchild GameStop (GME), it now ranks as the 209th most heavily shorted stock.

Indus Realty Trust (INDT) also finds itself high up on the list of highly shorted stocks, but that is a recent change. Its short interest has surged 31 percentage points in the first half of January on what has been a relatively small stock price decline in the same time. NETSTREIT (NTST), Codex DNA (DNAY), and Cresent Energy (CRGY) are the only other stocks to have seen double-digit percentage point jumps in short interest so far in 2022. Want more in-depth analysis from Bespoke? Click here to view Bespoke’s premium subscription options.

Massive Month-End Buying of Biggest Losers

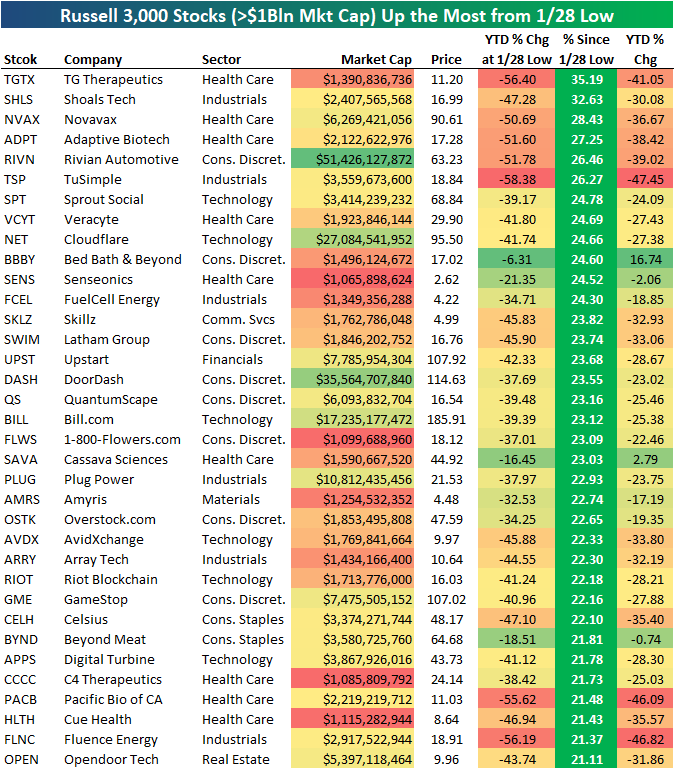

The average stock in the Russell 3,000 is now up 7% from the index’s low point last Friday (1/28) as we near the final close of January 2022. We have seen some massive rallies since Friday morning when US markets started the day in the red. Below is a look at the Russell 3,000 stocks with market caps >$1 billion that are up the most since their intraday lows last Friday. For each stock, we also show how it had performed on a year-to-date basis at its low point last Friday. What we see here is that the stocks that are up the most during this two-day month-end rally are generally the same ones that were down the most YTD heading into the rally. The six stocks that are up the most since their lows on Friday are up 26%+, but five of the six were down 50%+ YTD at their lows! A 50%+ YTD decline usually takes more than a month to play out, but not this year! And 25%+ rallies usually take more than two trading days to play out as well.

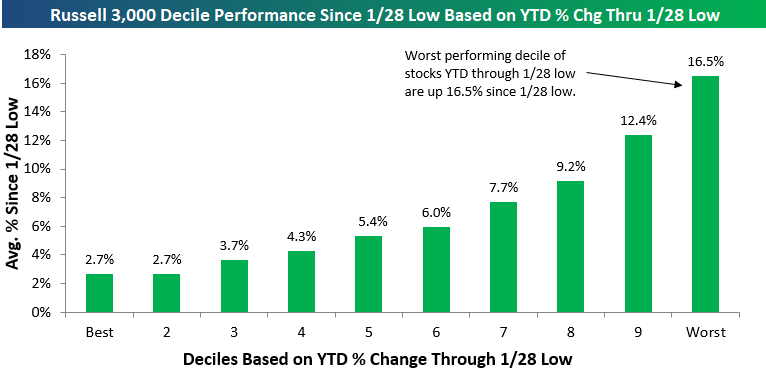

If we break the Russell 3,000 into deciles based on YTD performance through the low on Friday (1/28), we can clearly see that the stocks that were down the most YTD are the ones bouncing back the most. The 10% of stocks in the Russell 3,000 that were down the most YTD at the low on 1/28 are up an average of 16.5% since. Conversely, the 10% of stocks in the index that were doing the best YTD at their low point last Friday are only up 2.7% since then.

Below is a look at the rally off last Friday’s lows by sector. The average Health Care stock was down 25%+ YTD at last Friday’s low, but they’re now up more than 10% since then. Tech stocks were down nearly 20% YTD on average through last Friday’s lows, and they’re up 9.8% since.

We would note that the Energy sector is the only one that saw stocks up YTD through last Friday’s low, and they have tacked on a gain of 3.8% since then for a full-year average gain of 8.44%. Stay on top of market trends by becoming a Bespoke subscriber today. Click here to view Bespoke’s premium membership options.

The Rogan Rollercoaster

Any publicity is good publicity, right? When it comes to the world’s largest podcast and the company that hosts it, that seems to be holding true at least for today. As of this writing, Spotify (SPOT) is trading up double-digits versus Friday’s 52-week low for its fifth-best day on record since its IPO as the company has been in a whirlwind of headlines over the past week. Those headlines concern comedian Joe Rogan’s Spotify exclusive podcast, The Joe Rogan Experience, and the controversy it has caused due to artists like Neil Young pulling their music from the platform citing COVID misinformation on Rogan’s podcast. While there have been a slew of headlines in the past few days coinciding with huge moves in SPOT’s stock, it is not the first time this has happened.

In the chart below, we show Bloomberg and other major news agency headlines concerning Joe Rogan, his show, and Spotify over the past two years. Since Spotify and Joe Rogan first struck a deal to have the podcast exclusively on the platform in May 2020, headlines surrounding the show have at multiple points resulted in huge swings in the stock. When news of the deal first hit the tape, the stock soared and then soared again even more substantially roughly a month later as analysts upgraded the stock in response to the deal. In fact, that response to upgrades resulted in the stock’s third-best single-day gain on record. From May 2020 before the deal was announced to the highs later that summer in July, SPOT would rise from around $150 to a little under $300. After a few months of consolidation, including a sharp but short-term drop when Spotify staff gave pushback on Alex Jones’ appearance on Rogan’s show, the stock surged again on strong earnings partially accredited to the addition of the podcast. SPOT then erased much of those gains in early 2021, and more backlash over COVID “misinformation” again sent the stock lower last spring. While the last earnings report in the fall saw the stock spike higher, it quickly reversed lower and the recent onslaught of headlines resulted in a 52-week low on Thursday, leaving SPOT at similar levels to when the Joe Rogan deal first went through.

While there is some overlap with earnings, as previously mentioned, days in which Spotify and Joe Rogan find themselves in the news have coincided with some of the stock’s largest single-day moves or highest volumes. In fact, today is on pace to be the third-best day since the deal with Joe Rogan went through and volumes in the past several days have sat around the 90th percentile of all days since the stock’s IPO.

The most recent string of headlines have hit the tape with only a few days left before the company reports Q4 results. Using data from our Earnings Explorer tool, SPOT has historically traded weak in response to earnings. Since its IPO in 2018, there have only been four quarters in which the stock had a positive one-day reaction to its earnings report. One of those was last quarter when the stock rose 8.3%. When it comes to Q4 specifically, the stock has yet to react positively to earnings and the stock’s average decline has been the weakest of any quarter averaging a decline of 5.21%. Click here to view Bespoke’s premium membership options.