International Check-Up

The S&P 500 is down 20.8% on a YTD basis, which is worse than all of the international indices we looked at apart from the DAX (German stock market index) and ITLMS (Italy stock market index). Although the YTD performance is weak relative to other countries, performance relative to pre-COVID levels is still elevated, so long-term investors have been rewarded by investing in the US. Relative to mid February of 2020 just before COVID hit the West, the S&P 500 ranks third out of the 12 indices we looked at, falling short of just Argentina (Merval) and Chile (IGPA). Click here to learn more about Bespoke’s premium stock market research service.

Of the 12 international indices, eight are down relative to pre-COVID levels. The biggest decliners have been Hong Kong (Hang Seng), Spain (IBEX 35) and Italy (ITLMS). The charts below show the five year performance of each international index that we looked at (and the S&P 500). As you can see, five year returns are now negative for the DAX, the Hang Seng, the FTSE Italia, the IBEX 35 and the FTSE 100. So much for the benefits of international diversification!

The table below summarizes each index’s performance over the last five years, relative to pre-COVID levels, and on a YTD basis. Much of the differentiation in performance can be attributed to the means of each respective economy. For example, Argentina and Chile largely export materials, making the economies highly correlated to price moves in commodities. On the other hand, Western nations tend to have a healthy mix of industrial products, commodities and services. Click here to learn more about Bespoke’s premium stock market research service.

Firearm Background Checks

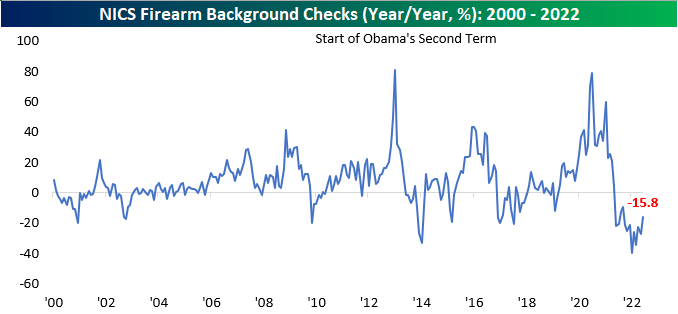

We track the number of NICS firearm background checks on a regular basis as it often provides interesting insights on the mood of Americans or the direction of political winds regarding gun control legislation. In times of higher volatility, uncertainty, or concerns that lawmakers in Washington will enact stricter legislation for firearms, purchases tend to rise. On the other hand, in periods of stability, background checks tend to fall. Ever since June of last year, background checks have been declining on a y/y basis, but the y/y decline moderated in June. Although still down 15.8% compared to last year, purchases moved higher sequentially for the first time in three months. Click here to learn more about Bespoke’s premium stock market research service.

Although checks moved higher month over month, they are likely to rise even further in July due to the Supreme Court’s recent ruling against the state of New York. This case expands the right to carry, and will likely increase firearm purchases in some of the most restrictive cities, such as New York and Los Angeles. In June, background checks rose by over 230K to reach 2.6 million. Although checks are in a near-term down-trend following the COVID spike, the longer-term uptrend is still very much intact.

On a YTD basis, background checks have declined at the fastest rate on record. This is largely due to elevated comps, as 2021 saw background checks near record levels due to a growing political divide, COVID lockdowns, and fears over legislation with Democrats in full control of Washington D.C.

Although background checks moved higher month over month, Sturm Ruger (RGR) and Smith and Wesson (SWBI) hit 52-week lows in June. All-in-all, RGR traded 6.3% lower in June, and SWBI declined 15.2%. The stocks have been weighed down by slowing sales over the last couple of quarters, increased legal risk associated with firearm manufacturer liability, and the pull of the overall market tide. Both these stocks are still in sustained downtrends, and even after initially moving higher following the Supreme Court decision, both stocks have essentially come full circle. Click here to learn more about Bespoke’s premium stock market research service.

Was It the Stock Price?

We’ve all seen the impact that falling stock prices have had on investor sentiment in the last few months. The weekly poll that the American Association of Individual Investors (AAII) takes of its members recently showed the lowest level of bullish sentiment since 1992. You read that right. Even during the depths of the Dot Com crash, the Financial Crisis, or the COVID crash, bullish sentiment bottomed out at higher levels than it has in the COVID unwind.

General consumer surveys have also cratered. Despite what we’re told is a strong labor market (for now) and the world moving on from COVID (even if parts of the world and some groups would prefer that people remain in lockdown indefinitely), we have raging inflation, rising crime, geopolitical uncertainty, gas prices at record highs, and a more politically divided populace than we’ve seen in decades. Consumers are among the most downbeat they’ve ever been. The monthly poll from the University of Michigan has even dropped to levels not seen in the entire 40+ year history of the survey.

The shift in sentiment extends beyond the sphere of investors and consumers and into the C-suite as well, most notably in the former high-flying tech/growth sector. Traditionally, these companies have looked like a utopian oasis with amenities, perks, and employee accommodations that the average American could only dream of. Just google the term “google headquarters inside” and you’ll see what we mean. From an outsider’s perspective, it seems like an employee can take a day off (or days off) simply for reasons like they aren’t feeling it or if their favorite team lost a game the night before.

It’s probably not that extreme. There’s a reason these companies became among the most valuable in the world, and it wasn’t because everybody just has fun and does nothing. But in terms of their ‘images’, they made it seem like working at their companies was like going to summer camp. When a company’s stock price shoots higher, showering perks on its employees and advertising them for the press to see is just a way of showing how much better the company is than all the ‘old’ economy stocks.

This year, we’ve started to see a shift in the attitude of companies towards their employees, and the two most notable were recent comments from Netflix’s Reed Hastings and Meta’s Mark Zuckerberg. Over the last year, there has been well-covered discontent among Netflix employees regarding some of the streamer’s programming and it not fitting in with their personal views. In early May, Hastings responded to these concerns with a long memo that included the suggestion “If you’d find it hard to support our content breadth, Netflix may not be the best place for you.”

Up north in Palo Alto, a similar shift has played out at Meta Platforms (META), formerly known as Facebook. In a Q&A session last week, Zuckerberg warned employees that the company was facing one of the steepest downturns in its history, and just after rebranding employees of the firm as his ‘metamates,’ he continued by saying “there are probably a bunch of people at the company who shouldn’t be here.” Ouch, mate!

So what explains the shift in tone among these CEOs from ‘kumbaya’ to ‘don’t let the door hit you on the way out’? Could it be the stock prices? As shown in the charts below, in the cases of both Netflix and Meta Platforms, the shift in tone has come after major declines in each company’s stock where prices have been more than cut in half. Just like many of us common folk, it looks as though stock prices can also have a big impact on the mood of CEOs. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Brunch Reads: 7/3/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Institutional Investors

Hedge funds braced for further stock market turmoil by Laurence Fletcher (FT)

Amidst high volatility and falling prices, fast leveraged money is slashing its exposure to the equity market, with the lowest net exposure since at least 2010 amidst reduced bets on higher stock prices. [Link; soft paywall]

Pension Funds Plunge Into Riskier Bets—Just as Markets Are Struggling by Dion Rabouin and Heather Gillers (WSJ)

Pension funds are starting to lever their portfolios in order to hit return targets that may prove unrealistic, just in time for a historic collapse in asset prices to hit in 2022. [Link; paywall]

Space

Inside SpinLaunch, the Space Industry’s Best Kept Secret by Daniel Oberhaus (Wired)

A new company is testing a frankly wild launch system: spinning a small payload on a centrifuge in a vacuum before releasing it in a massive parabolic arc that lofts the craft near to orbit. [Link; soft paywall]

‘No Aliens, No Spaceships, No Invasion of Earth’: An oral history of Contact, the sci-fi movie that defied Hollywood norms and made it big anyway. by Rachel Handler (NYMag)

A recollection of the unique vision that one of the largest-scale sci-fi movies ever attempted brought to Hollywood, and why it remains a breath of creative fresh air. [Link]

Sports

Thwack. Pop. Whack. Pickleball Noises Turn Neighbors Into Activists. by James Fanelli (WSJ)

Low-impact paddle ball sport pickleball may be easy on the knees and frankly quite a bit of fun, but it’s creating a major conflict for residents near courts: the perforated balls and wooden paddles make for low-speed volleys but make a huge and very annoying amount of noise. [Link]

Manny, Pedro and Papi’s kids are on the same team?! Meet ‘The Sons’ of the Brockton Rox by Joon Lee (ESPN)

The sons of some of Major League Baseball’s best players are sharing uniforms in a murderer’s row of genetic diamond talent about an hour from Fenway Park. [Link]

Energy

For the First Time, US Is Sending More Gas to Europe Than Russia by Anna Shiryaevskaya (Bloomberg)

Huge flows of liquid natural gas from the US to Europe amidst the fall-out of Russia’s invasion of Ukraine have led the United States to supplant Russia as the biggest source of natural gas for the continent. [Link; soft paywall]

The Supreme Court’s EPA Ruling Is Going to Be Very, Very Expensive by Robinson Meyer (The Atlantic)

Analysis of the SCOTUS ruling, which taken at face value means that preserved EPA authority to regulate greenhouse gas emissions could be much more expensive for industry than what the agency had sought to do. [Link; soft paywall]

Driving

Apple eyes fuel purchases from dashboard as it revs up car software by Stephen Nellis (Reuters)

Updates to Apple’s CarPlay software suite could mean consumers buy their gas through an app before they ever reach a gas station rather than paying at the pump. [Link; auto-playing video]

Uber, Lyft Drivers Switch to Teslas as High Gas Prices Squeeze Profit by Jackie Davalos (Bloomberg)

With fuel prices still near record levels, operating costs of relatively up-scale electric vehicles are so much lower than traditional ICE cars that they more than justify the upfront cost almost immediately. [Link; soft paywall]

Whoops

Japanese Man Lost a USB Drive With Entire City’s Personal Data After a Night Out by Hanako Montgomery (Vice)

The personal data of 465,177 residents of Amagasaki, Japan has been stolen after a contractor put the data on the flash drive then got so drunk he fell asleep on the street. [Link]

Social Media

TikTok Turns On the Money Machine by Zheping Huang (Yahoo!/Bloomberg)

Revenues at algorithmic video short network TikTok are exploding with top line likely to exceed Twitter (TWTR) and Snap (SNAP) combined by the end of the year. [Link]

Education

The Impact of School Facility Investments on Students and Homeowners: Evidence from Los Angeles by Julien Lafortune and David Schönholzer (American Economic Journal: Applied Economics)

Construction of school facilities in Los Angeles over the last few decades generated $1.62 for every $1 spent, with about a quarter of the benefit coming from higher test scores and the rest from other amenities. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 7/1/22 – Dazed and Confused

This week’s Bespoke Report newsletter is now available for members.

“Been dazed and confused for so long, it’s not true…Lotsa people talkin’, few of them know…Don’t know where you’re going, only know just where you’ve been…” – Dazed and Confused, Led Zeppelin

We can’t think of many songs that better encapsulate 2022, but if you can, let us know. Confusing has been an understatement as investors are faced with a barrage of back-and-forth moves and policy decisions that would make most fair-minded people scratch their heads. Despite the cross-currents, we hear a lot of confidence from both sides about what will go down in the second half, but even in normal times, let alone one of the trickiest economic backdrops any of us have ever experienced, few of them know.

There’s a lot to cover in this week’s Bespoke Report, including the horrible first half and what it might mean for the second half, the state of the economy and inflation, a preview of earnings season and the midterm elections, a look at consumer sentiment, and much more. To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to one of our three membership levels.

Bespoke Market Calendar — July 2022

Please click the image below to view our July 2022 market calendar. This calendar includes the S&P 500’s average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 7/1/22 – Fresh Start

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Remember too that your time is your one finite resource, and when you say “yes” to one thing you are inevitably saying “no” to another.” – Andrew S Grove

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures are picking up in Q3 right where they left off in Q2, but the declines have been contained to this point. Weak guidance from Micron (MU) as well as further concerns regarding the health of the consumer following profit warnings in the retail sector haven’t helped sentiment. Concerns are only more elevated that the economy is either already in or on the verge of a recession even as the Fed continues to press its case for more aggressive policy moving forward.

The only economic indicators of note today are the ISM Manufacturing for June and the May Construction Spending report. If global PMI data that has already been released today is any indication, don’t set your expectations all that high. Given the holiday weekend coming up, we would normally expect a Summer Friday like today to be on the quiet side, but given the way this year has played out, who knows.

In today’s Morning Lineup, we discuss moves in rates markets and what they’re pricing in regarding Fed policy, movements in Asian and European markets, a recap of global PMI data, and more.

As economic concerns have been ratcheted higher in recent weeks, we’ve seen a sharp pullback in US Treasury yields across the curve that followed the mid-June spike in reaction to the May CPI report and the preliminary UMich Confidence report. While yields remain elevated, the uptrend that had been in place since earlier this year appears to have been broken. Going forward, the path of interest rates, especially the yield on the 2-year, will go a long way in determining how stocks perform in the second half. If the pace of increases experienced in the first half continues in the second half, investors may be facing a long six months.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Consumer Pulse Report — July 2022

Strength Follows Weakness

Whether you’re looking at monthly, quarterly, or first-half performance, this year’s S&P 500 performance has been quite weak. As investors, we must avoid falling into the sunken-cost fallacy and are forced to be forward-looking.

Starting with weak months, there have been a total of 83 months in the post-WWII era in which the S&P 500 declined at least 5%. In fact, this has occurred three times in 2022 alone, and if the current pace continues will top the post-WWII high in 2008 when there were five months of 5%+ declines. Click here to learn more about Bespoke’s premium stock market research service.

In addition to 5%+ monthly declines, we also looked at periods where the S&P 500 declined 10%+, as well as six-month periods when the S&P 500 fell 20%+ (with no prior occurrences in the last three months). Over the following day, performance was inline with the historical average following 5%+ monthly declines and 10%+ quarterly declines, but the first trading day following a six-month decline of 20%+ was much better than the historical average. Over the following week and month, though, the picture looks different as performance after 10%+ quarterly declines has been much better than average while performance following 20%+ six-month declines has been well below average. In terms of the week and month after 5%+ monthly declines, returns have pretty much been in line with the historical average.

Taking a look at positivity rates (percent of the time the S&P 500 has posted gains in a respective period), the S&P 500 has boasted above average rates following a monthly decline of 5%+ in both the next day and month, but rates are lower over the following week. After quarterly declines of 10%+, positivity rates were lower in the following day, but above average for the following week and month, coming in at 61.9% and 71.4%, respectively. On the downside, positivity rates were much lower following the first rolling six month decline of 20%+ in the next week and month, coming in at 40.0% for both. Investors should note that the first occurrence of a 20%+ rolling six month decline occurred on June 16th. Click here to learn more about Bespoke’s premium stock market research service.

The Bespoke 50 Growth Stocks — 6/30/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.