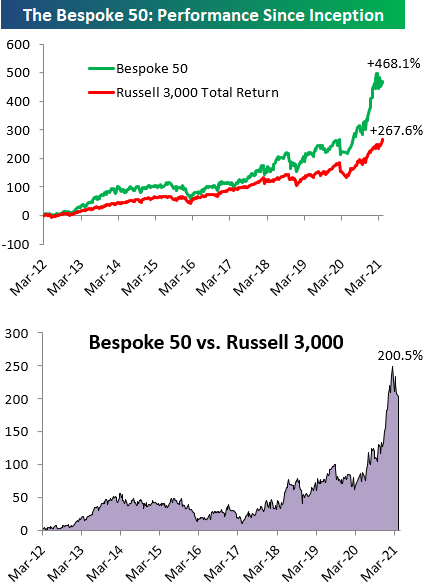

The Bespoke 50 Top Growth Stocks — 4/15/21

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” list is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” is up 468.1% excluding dividends, commissions, or fees. Over the same period, the Russell 3,000’s total return has been +267.6%. Always remember, though, that past performance is no guarantee of future returns. (Please read below for more info.) To view our “Bespoke 50” list of top growth stocks, please start a two-week trial to either Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, fees, or dividends are not included in the performance calculation. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities.

Explosive Empire

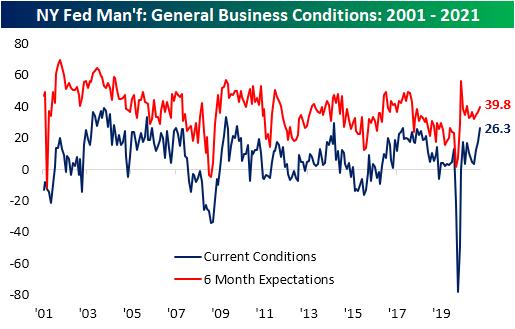

Manufacturing businesses in the New York area are roaring back to life this spring. After some readings showing only modest growth at the end of 2020 and at the start of this year, the New York Fed’s monthly manufacturing survey results released this morning showed the headline index rising to 26.3 which is the strongest level since October 2017. That indicates the region’s manufacturing sector is growing at a rapidly accelerated rate. In fact, only 12.2% of businesses reported worse overall business conditions in April which is the lowest level in nearly a decade (since May of 2011).

Given the strong reading in the index of General Business Conditions, every other area of the report also showed impressive readings. For the current conditions indices, every index is in expansionary territory with higher month-over-month moves. Some of these like those for Delivery Times, Prices Received, Prices Paid, and Unfilled Orders are also at or just off record highs after massive moves higher in the past month. Expectations generally remain positive although some indices are at less extreme places within their historical ranges while three of the indices were also lower versus March.

Beginning with a look at demand and production metrics, New and Unfilled Orders both surged in April rising 17.8 and 17.2 points, respectively. For New Orders, that month over month rise stands in the top 5% of all monthly moves and brings the index to its highest level since October 2009. That compares to last month when the index was essentially in the middle of its historical range. Meanwhile, Unfilled Orders had been elevated even before this report, but with the most recent surge in New Orders, Unfilled Orders are now at the second-highest level on record behind the reading of 36.5 from September 2001 when the fulfillment of existing orders was likely impacted by the September 11th attacks.

While demand has been very strong, firms have seen no lack of trying to fulfill those orders. Inventory levels were notably higher as that index rose to 11.6 which is in the top 2% of all readings and the highest since last February. The index for Shipments rose 3.9 points to 25 which is the highest level since August 2018. While that is a historically healthy reading, given the surge in unfilled orders and inventories it does indicate that the region’s manufacturers still have plenty of product to get out the door.

One likely reason for the weaker reading in shipments relative to orders and inventories is record length in delivery times. That index not only experienced the second-largest increase of any month on record (behind September 2001), but it also reached the highest level ever. At 28.1, the index surpassed the previous record by 11.9 points.

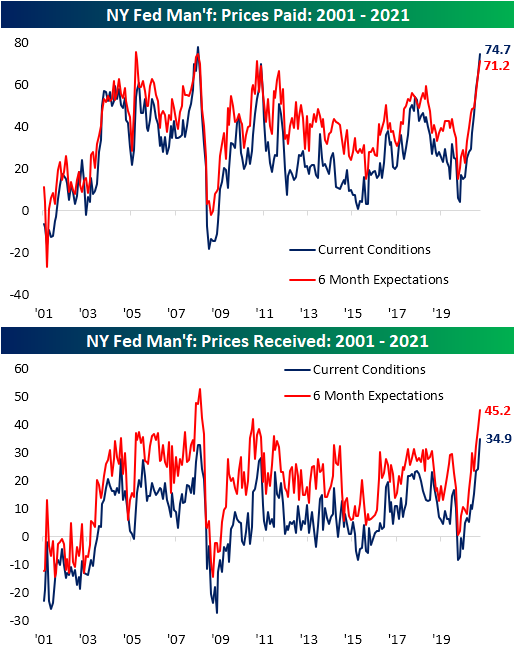

On top of—and likely because of—those supply chain disruptions, prices continue to rise at a record clip. Prices Paid came in at the second-highest level on record behind July 2008. Those price increases are also being passed onto customers as Prices Received rose to a record high. Additionally, businesses do not appear to see much of a chance for these trends to reverse as six-month expectations are also at very high levels.

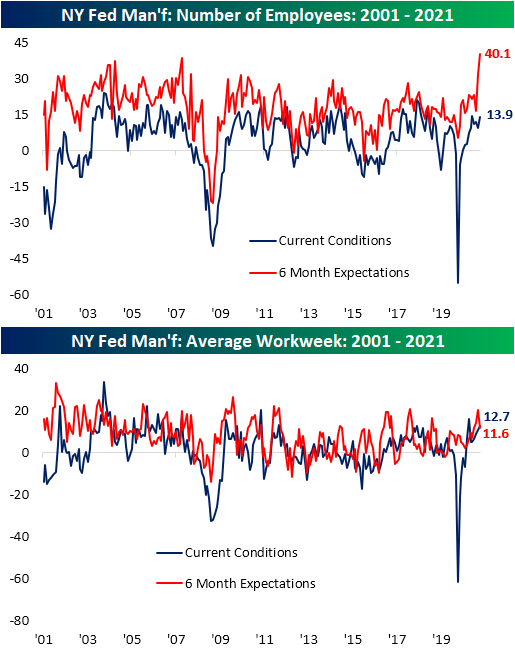

After a very strong nonfarm payrolls report at the start of the month and on the same day that initial jobless claims came in at a new low for the pandemic, this report also gave a rosy outlook for the labor market. The index for the Number of Employees was higher alongside Average Workweek meaning businesses took on more employees and increased hours for existing workers, but the real move was in expectations. Expectations for Number of Employees ripped higher to a new record of 40.1. That willingness to hire paints a very optimistic picture for the region’s labor market.

That sort of optimism extends beyond the workforce though. Six-month expectations for Capital Expenditures and Technology Spending were also higher, rising to the top 15% of all readings. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Hospitals Heaping It On (HCA)

B.I.G. Tips – Boom Goes the Retail Sales

After a lousy report for the month of February when freak weather across the south temporarily shut down several areas of the south, Retail Sales bounced back with a vengeance in March as vaccine rollouts accelerated and stimulus checks were spent.

The moves higher in Retail Sales over the last few months have been incredible. As shown below, while it took 40 months to make a new high following their pre-Financial Crisis peak, COVID only caused a five-month drought without a new high. From the low in April 2020, Retail Sales have bounced 50%!

Even more impressive, though, is not only are total Retail Sales above their pre-COVID peak, but they are more than 17% above that peak just 14 months ago. The second chart shows the 14-month rate of change in Retail Sales since 1992. While the post-COVID decline was the steepest on record, the 14-month gain is the highest on record. Ironically, had it not been for COVID and the stimulus it resulted in, there is no way Retail Sales levels would be where they are now.

In our just-released B.I.G. Tips report, we broke out the details of the March report including its bright and dark spots. For anyone with more than a passing interest in how the COVID outbreak and subsequent stimulus is impacting the economy, our monthly update on retail sales is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!

Hard to Hate This Week’s Claims

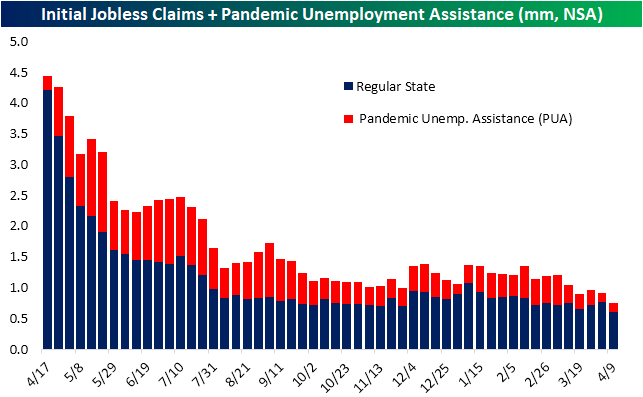

Among the many strong economic data points out this morning, jobless claims was one of the more impressive ones. Last week’s print was revised upwards to 769K from 744K. This week’s number was anticipated to fall back down to 700K, but the actual results were far better as seasonally adjusted initial claims fell by 193K to a pandemic low of 576K. That is the biggest one-week drop since a 219K decline at the end of July. Additionally, this week’s decline also brings claims back below the pre-COVID record high of 695K from October 1982.

On a non-seasonally adjusted basis, the picture was just as impressive. Regular state claims dropped 152.9K to 612.9K. Again this was the lowest level of the pandemic. The same can be said for Pandemic Unemployment Assistance (PUA) too. Although the 20K decline is on the smaller side for the past several weeks’ moves, claims from this program reached a new low of 131.98K. PUA claims are now down to around a quarter of where they stood just two months ago.

Over the past several months, continuing claims have consistently been making new lows for the pandemic. Since the high in claims last May, there have only been 8 weeks in which continuing claims did not fall with this week being one of them. Claims rose by a meager 4K from last week’s downwardly revised reading of 3.727 million. That snapped a streak of 12 consecutive weeks of declines. Additionally, outside of the week of September 11th when claims went unchanged, the 4K increase this week was tiny relative to other moves of the past year. Overall, while continuing claims increased, it came in the context of a long, albeit slowing, streak of declines.

Including all other programs creates another week’s lag for the data meaning the most recent reading is through the final week of March. Taking a look at continuing claims in this light, there were broad improvements with the only program to see an uptick being the very small State Additional Benefits which rose from 1.8K to 2.15K. As for the larger and more impactful programs, regular state claims fell by half of a million while PUA claims were not far behind dropping 474.7K. The third-largest program, Pandemic Emergency Unemployment Compensation (PEU), also saw a significant decline falling by 174.4K. That was the program’s fourth-largest week-over-week decline of the past year. Altogether, total continuing claims across all programs fell to 16.96 million. That is the second-lowest level of the past year.

In addition to the drop in the overall level of claims, another improvement comes from the composition of claims. Over the past several months we have noted how an increased share of claims are on account of programs that extend benefits past the expiration of various programs. In other words, a larger share of people on unemployment have been out of work for extended periods of time. For the time being, that trend has peaked. The most recent week showed further improvements with respect to those programs as they now account for a combined 34% of all claims. That is down for a third week in a row since the high of 36.9%. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 4/15/21 – Better Than Expected

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Money is made by sitting, not trading.” – Jesse Livermore

Futures have been higher all morning driven by solid earnings results from some of the largest banks. In addition to the earnings results, we just got a slug of economic data in the form of Jobless Claims, Retail Sales, Empire Manufacturing, and Philly Fed Manufacturing. As “Crazy Eddie” would say, the results were “Insane”. With the exception of Continuing Claims, which still came in right near their post-pandemic lows, every other report came in much stronger than expected. It’s still early, but what could be more impressive than the results themselves is the fact that the yield on the 10-year is actually lower now than it was before the releases.

Read today’s Morning Lineup for a recap of all the major market news and events including a recap of the biggest overnight events including some key earnings reports, international inflation data, as well as the latest US and international COVID trends including our vaccination trackers, and much more.

As shown on page two of our Morning Lineup, the S&P 500 has been consistently trading in ‘extreme’ overbought territory in recent days (2+ standard deviations above its 50-DMA). Yesterday marked the 9th straight trading day that the S&P 500 finished the day in this area marking the longest streak since January 2018 and just the 7th streak of nine or more trading days.

Daily Sector Snapshot — 4/14/21

Short Interest Through the End of March

On Monday, short interest data through the end of March was released. ln aggregate for Russell 3,000 stocks, short interest as a percent of equity float is little changed versus where it stood in mid-March. But on an industry basis, there have been some large moves. Compared to midway through last month (red dashes in the chart below), the Pharma, Biotech, and Life Sciences industry saw short interest build by the most rising 0.68 percentage points. Of the other industries, there were eight that also saw higher short interest than the prior report. Conversely, the Telecom Services industry saw short interest fall the most of any sector dropping 0.46 percentage points between reports. While the moves between the most recent and the prior report were not very large, across the board, just about every industry has significantly lower average short interest levels now than at the start of the year (green dashes). That is especially the case for Retailing which has seen average short interest fall by 4.89 percentage points.

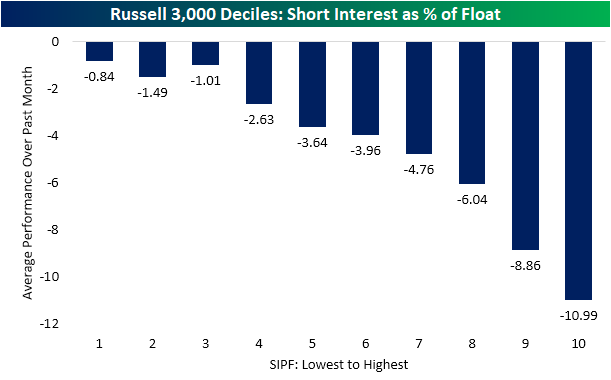

Earlier in the year, short interest appeared to be a key driver of performance. During the GameStop (GME) saga, the most heavily shorted stocks were some of the best performers. Fortunately for short-sellers, over the past month, the opposite has been the case. The stocks that had the highest short interest as a percent of float at the end of March have averaged a decline of 10.99% over the past month. Comparatively, stocks with low short interest have fared much better albeit still lower on average.

We would also note that while every decile based on short interest has averaged a decline over the past month, the Russell 3,000 has actually pushed to new highs. That is because the largest stocks by market cap have been driving the capitalization-weighted index higher.

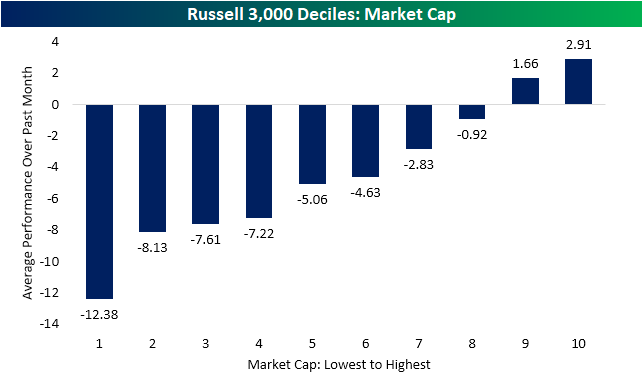

In fact, one other notable theme of performance recently has been market cap. The deciles of the largest stocks (deciles 9 and 10) are the only ones whose stocks have averaged a move higher over the past month. On the other hand, the other deciles have averaged declines with the severity of those declines getting worse with smaller market caps.

In the table below, we show the 30 most heavily shorted stocks in the Russell 3,000 at the end of March. Health Care stocks, namely those of the Pharma, Biotech, and Life Sciences industry, dominate this list. That includes IGM Biosciences (IGMS) which is the most heavily shorted stock with 44.8% of shares shorted. Of the other top 30 most shorted stocks, 25 have at least a quarter of their shares sold short. Some of these like Academy Sports & Outdoors (ASO) and Gogo (GOGO) have that high short interest in spite of big declines in short interest recently. Others like IGMS as well as Discovery (DISCA), Frequency Therapeutics (FREQ), and Rackspace Technology (RXT) have seen short interest rise considerably.

In fact, those names are the stocks in the Russell 3,000 that have seen short interest rise the most versus the last report. RXT, IGMS, FREQ, as well as SeaChange International (SEAC) and iTeos Therapeutics (ITOS) have all seen short interest rise by double-digit percentage points. There is an even larger number of stocks that have seen short interest fall double-digit percentage points, though, with Sumo Logic (SUMO) having seen the biggest decline falling 32.07 percentage points. Lastly, while the majority of stocks with high short interest or big increases/decreases in short interest are smaller in size, two standouts are Discovery (DISCA) and Rocket (RKT) with market caps of $26.57 billion and $45.6 billion, respectively. Click here to view Bespoke’s premium membership options for our best research available.

Gas Prices Hit the Breaks

While the surge in oil prices today will likely have some impact on gas prices in the days ahead, recent trends in prices at the pump have really done an about-face. After a record YTD surge that took prices as high as $2.88 per gallon as of March 19th, the national average price of a gallon of gas has dropped to $2.86 according to AAA. A two-cent decline in the price of a gallon of gas may not sound like much, but for this time of year, it’s extremely uncommon for prices to decline. Since 2005, prices have only declined in the period from 3/19 through 4/14 three times in 16 years.

To further illustrate, the chart below compares the change in average gas prices this year to a composite of every year since 2005. While it’s typical for gas prices to rise at this time of year, the surge we have seen in 2021 has been much larger than average. However, whereas prices typically continue to rise right up through late May, this year’s increase in prices stalled out nearly a month ago.

Even after this modest pullback, though, prices are still high relative to history for this time of year on both an absolute basis and in terms of their YTD change. At an average of $2.86 per gallon, prices haven’t been this high at this time of year since 2014 and are two cents above the historical average for 4/14. Similarly, the YTD increase of 27.0% in prices is more than twice the historical average at this time of year.

On a y/y basis, prices have also seen a major surge. At current levels, the national average price of a gallon of gas is up over 55% in the last year, and if prices simply stay at their current levels between now and the end of April, the y/y change would top out at 61.9%. While still slightly less than a record y/y change, it would still be pretty darn close. Start a two-week free trial to Bespoke Institutional to access all of our analysis and market commentary.

Health Care & Education Inflation Withering Away

Last night in The Closer we reviewed the BLS report on March CPI reported yesterday, including a couple of interesting long-term sources of inflation that have decelerated dramatically of late.

Two categories have long been a source of angst for consumers and policymakers for their persistent gains: medical care goods and tuition/child care. Prior to the last couple of years, it was extremely unusual for the prices of medical care goods to drop more than 1% or so below their prior record high. Instead, we saw slow and persistent price gains. Since COVID hit, though, prices have plunged by a record of more than 3% from their highs. The drivers are two-fold. First, after huge price gains relative to overall inflation for most of their history, prescription drug prices, which account for the largest weighting in the sector, have barely budged over the last couple of years.

The second factor behind the decline has been what is likely to be a temporary sharp drop in medical equipment and supply prices.

Turning to tuition, the steady above-headline growth of the cost of school has been a permanent feature of American life for decades, but that has started to shift. Tuition and childcare prices were actually negative year-over-year at one point in 2020, and demographics mean that the student cohorts are gradually getting smaller; college inflation may be starting to leave the picture after years of consistent pressure. Start a two-week free trial to Bespoke Institutional to access all of our analysis and market commentary.