Speculators Shorting USD

From its peak earlier this spring to its low earlier this month, the dollar had fallen over 7.5%. Around those recent lows there was a stretch of 12 straight days closing below its 200-DMA, as shown below. While the greenback managed to move back above its 200-DMA on Thursday and Friday of last week, it’s giving up the ghost this week falling around 0.5% yesterday and another 0.43% today as of this writing. Yesterday’s decline brought it back below its 200-DMA.

That decline comes on overall bearish sentiment for the dollar. In our Closer every Friday, we include the Commodity Futures Trading Commission’s data from the Commitments of Traders Report on speculator positioning. Last week’s report showed a massive shift in open interest getting short on the dollar. A net percentage of 26.9% are now short the dollar compared to +13.82% net long the prior week. That 40.71 percentage point shift was the largest move in favor of speculators getting short behind a 48.47 percentage point decline back in September 2005 as shown in the second chart below.

It is not just the dollar that speculators are short though. As for US equities, 31.13% of open interest are net short the Dow. That is the most pessimistic positioning speculators have taken on the index since August 2005. For other indices like the S&P 500, positioning is not as extreme but similarly holds a bearish bias. Click here to view Bespoke’s premium membership options for our best research available.

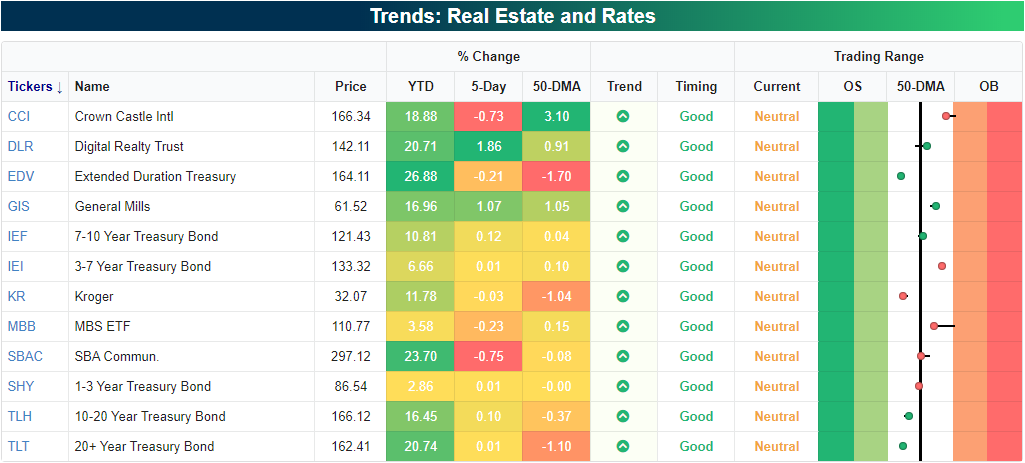

Real Estate and Rates Showing Good Timing

In our Trend Analyzer and Chart Scanner tools, we offer a number of different screens including ones for 52-week highs and lows and golden (rising 50-DMA moving above rising 200-DMA) and death crosses (falling 50-DMA moving below falling 200-DMA). Another screen we offer looks at the long term trends and timing scores from our algorithms. Typically, stocks that are overbought and in a downtrend will have poor timing while those in long term uptrends that are not overbought pose as better long ideas, and as a result, earn a good timing score. At the moment, due to the sharp declines and not everything having fully recovered from the bear market, there are still more stocks that are in downtrends and have poor timing (154) than those in uptrends and with good timing scores (21).

There is an interesting composition of stocks and ETFs that are currently in long term uptrends with good timing scores. The bulk of those 21 tickers are either Real Estate or Consumer Staples stocks or Treasury related ETFs as shown in the snapshot of our Trend Analyzer below. Typically seen as safe havens during market downturns, many of these held up during the bear market allowing them to not only maintain but also boost the picture for their long term uptrends. As risk appetite has improved over the past few months, the momentum of these names has slowed with each one now neutral rather than overbought which helps to earn their good timing scores.

As shown in the charts from our Chart Scanner below, all of these are in uptrends since the start of the year albeit with some volatility during the bear market. Broadly speaking for Treasury ETFs like EDV, IEI, IEF, TLH, and TLT in addition to a mortgage-backed security ETF (MBB), they have been in slight downtrends or trending sideways over the past few months after massive runs earlier this year. As a result, their 50-DMAs have caught up to price which now leaves them in neutral territory. Meanwhile, Real Estate names like Crown Castle (CCI) and SBA Communications (SBAC)—both in the business of cell towers—have pulled back to the bottom of their uptrends around their 50-DMAs.The same can be said for Consumer Staples names like General Mills (GIS) and Kroger (KR). These names have certainly sat out much of the rally in recent weeks, but any stress in the broader market from currently overbought levels will likely result in these stocks seeing increased interest. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Golden Crosses In Pandemic Proof Themes

Chart of the Day: Apple (AAPL) During the Worldwide Developers Conference (WWDC)

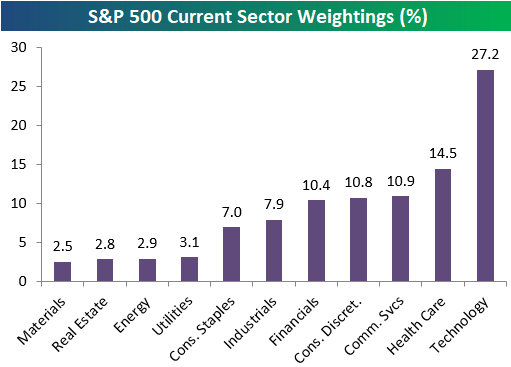

Nasdaq, Tech, Growth Keep Going

With Technology rallying and once again outperforming to start the new trading week, we wanted to note that the sector’s weighting in the S&P 500 has pushed above 27% recently up to 27.2%. That’s nearly twice as big as the next biggest sector in the S&P — Health Care — at 14.5%. Just three other sectors have weightings above 10%, and they’re all just only slightly above the 10% mark — Communication Services, Consumer Discretionary, and Financials. We’d note that Amazon (AMZN) makes up about a quarter of the Consumer Discretionary sector’s 10.8% weighting in the S&P, and while it is technically a retailer, between its web services division, and strong technology platform, you could argue that its just as much a Technology stock as it is Consumer Discretionary.

Industrials and Consumer Staples have seen their weightings dip below 8%, and the four smallest sectors each have weightings of just 2-3%.

At the moment, Tech’s 27.2% weighting in the S&P is larger than the weightings of the six smallest sectors combined.

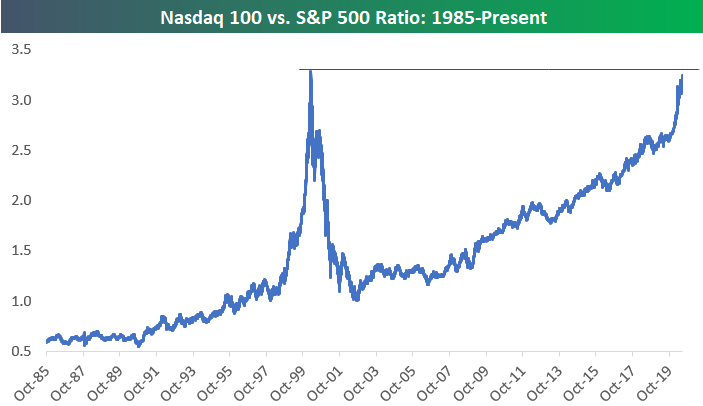

The tech-oriented Nasdaq 100 continues to outperform as well. Below is a chart of the ratio between the index levels of the Nasdaq 100 vs. the S&P 500. The ratio has been on a non-stop march higher since the end of the Dot Com bust in late 2002.

There have only been three trading days in history where the Nasdaq 100 to S&P 500 ratio was higher than the 3.25 level it’s at right now. Those three days came on March 8th, March 9th, and March 10th of the year 2000 — the very peak of the Dot Com Bubble.

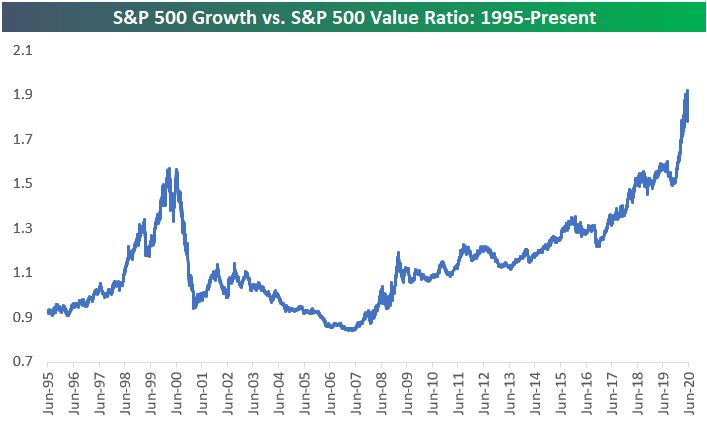

Finally, the Growth vs. Value trade remains lopsided towards growth. Below is a chart of the ratio between the S&P 500 Growth and S&P 500 Value index since 1995. This ratio actually took out its highs from the Dot Com Bubble in mid-2019, and it has exploded even higher over the last year. Value did outperform for a bit in May and early June, but over the last two weeks we’ve seen Growth soar and the ratio has once again made new highs. Click here to view Bespoke’s premium membership options for full access to all of our research.

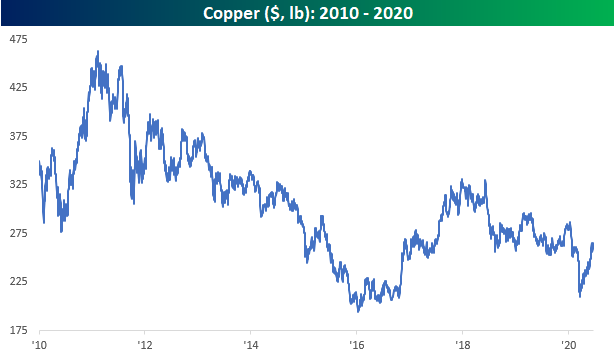

Metals Coming in Right in Medal Order

Going through the charts of gold, silver, and copper this morning, it’s ironic to see that in terms of both their performance over the last year, and over the longer term, their returns rank in the same order as their medal order in the Olympics. Starting with gold, it has been a strong year for the precious metal with a gain of about 25%. In recent weeks, though, we’ve seen a bit of a sideways pattern. Today, gold is trading up about 1%, and after two prior attempts at a breakout, it is once again testing resistance right below the $1,800 per ounce level.

Even if gold doesn’t break out above recent intraday highs, on a closing basis, it’s pretty much right at its highest levels since October 2012 but still below its closing peak of 1,889.70 back in August 2011.

Silver gets the silver medal with its 17% gain over the last year. Like gold, silver is also dealing with a good amount of resistance over the last year as the high $19/low $19 level has been a barrier to the upside on multiple occasions.

Unlike gold, which is near eight-year highs, silver is well off the extreme highs it saw early in the last decade. Back in 2012, silver was trading above $30 per ounce and traded just shy of $50 back in April 2011. Since 2014, silver has been in a relatively tight range with upside capped at around $20.

Trailing gold and silver for the bronze medal, copper prices are much further below their highs of the last year. At the current price of $265.2 per pound, copper is down nearly 2% over the last year.

Also, like silver, copper prices were a lot higher earlier in this decade than they are now. Back in 2010, the price per pound was closer to $450 but has been trending lower ever since then. Click here to view Bespoke’s premium membership options for full access to all of our research.

Bespoke Brunch Reads: 6/21/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2020 Annual Outlook special offer.

Remote Work

When Workers Can Live Anywhere, Many Ask: Why Do I Live Here? by Rachel Feintzeig and Ben Eisen (WSJ)

With COVID work-from-home responses untethering workers from their offices, they’re coming to the realization that they don’t actually need to be where they currently live. [Link; paywall]

Highest Salaries For Software Developer Remote Work (Metro Areas) by Wendell Cox (New Geography)

Adjusted for the cost of living, metros in North Carolina, Texas, Washington, and Colorado stand out as offering the best standard of living per dollar of pay for software developers. [Link]

China

China Is Collecting DNA From Tens of Millions of Men and Boys, Using U.S. Equipment by Sui-Lee Wee (NYT)

Chinese authorities are working to develop a national genetic database that will be used to augment surveillance and control capacity for the state. Massachusetts-based Thermo Fisher is helping in the effort. [Link; soft paywall]

China halts European salmon imports over suspected link to virus outbreak by Nerijus Adomaitis and Kate Kelland (Yahoo!/Reuters)

While salmon itself is unlikely to play host to the coronavirus, China is shutting down imports from northern Europe over concerns it drove an outbreak at a Beijing market. [Link; auto-playing video]

Food

America’s retreat to comfort food during the pandemic isn’t pure nostalgia — it’s a survival tactic by Kate Taylor (Business Insider)

“Junk” food isn’t just being purchased as a feel-good callback to more stable times but is also a strategy to reduce trips to the store and cut costs. [Link]

“One country’s joke is another country’s breakfast”: The story of Spam by Aimee Levitt (The Takeout)

An oral history of the canned meat that fed GIs in World War 2, became a critical lynchpin of a number of national cuisines, and is now being rediscovered as a rich and salty addition to avant-guard cuisine. [Link]

Why Is the McFlurry Machine Down Again? by Julie Jargon (WSJ)

Frustrating cleaning processes, frequent breakdowns, and social media frustration: why you can never get the ice cream cone or McFlurry you crave at McDonald’s. [Link; paywall]

Spending Patterns

Boats, Pools and Home Furnishings: How the Lockdown Transformed Our Spending Habits by Matthew Dalton and Suzanne Kapner (WSJ)

Stimulus payments and unemployment insurance are being pumped into home renovations and upgrades that provide a rare bright spot amidst broader economic decline. [Link; paywall]

The coronavirus pandemic can’t stop Americans from buying pickups by Nathan Bomey (USA Today)

Americans’ love affair with pickups is helping to keep the auto market afloat as the category remains much stronger than the sales of all light autos. [Link]

Parents are dropping $150K on luxury summer camps for their kids by Melkork Licea (New York Post)

Desperate to get their kids out of the house, parents are laying out six figure sums for summer sleepaway camps that will give parents a break from constant childminding. [Link]

COVID & The Elderly

Nobody Knows Exactly How Hard The Coronavirus Is Hitting America’s Assisted Living Facilities by Rosalind Adams and Ken Bensinger (BuzzFeed)

Assisted living facilities around the country have been hit hard by the virus, but New York state’s many care homes have been about as badly hit as it gets. [Link]

“Fire Through Dry Grass”: Andrew Cuomo Saw COVID-19’s Threat to Nursing Homes. Then He Risked Adding to It. by Joaquin Sapien and Joe Sexton (ProPublica)

Policy decisions by Governor Cuomo created a much worse outcome for New York nursing homes than those in other states, with roughly 6% of residents killed by the virus. [Link]

COVID Stories

Coronavirus: Dexamethasone proves first life-saving drug by Michelle Roberts (BBC)

While initial data from studies of dexamethasone is limited, it indicates a substantial positive impact on patients, reducing risk of death by one-third for patients on ventilators. [Link]

Rural Alabama County Fights Virus Outbreak With Just One Doctor by Margaret Newkirk and Danielle Bochove (Bloomberg)

Alabama’s Lowndes County has no hospital and just one doctor, relies on tightly packed mobile homes for housing, and an infection rate similar to New York City during the peak of its pandemic. [Link; soft paywall]

Fauci said US government held off promoting face masks because it knew shortages were so bad that even doctors couldn’t get enough by Mia Jankowicz (Business Insider)

CDC infectious disease head Dr. Anthony Fauci revealed that initial guidance for the public to wear masks was withheld because the government wanted to retain supplies of masks for health care workers, even though homemade masks and non-medical grade masks can still substantially reduce transmission with widespread use. [Link]

Oura

Covid-detecting ‘smart rings’ to be trialled by staff at Las Vegas resort by Patrick McGee (FT)

Casino staff will start using Oura smart rings to detect pre-symptomatic staff members that might be coming down with COVID but are not yet showing visible symptoms. [Link]

Inside the NBA’s plan to use smart technology and big data to keep players safe from coronavirus by Jessica Golden (CNBC)

The NBA will also use the Oura rings to help detect signs of infection among players who are living in Disney World in July as part of the NBA season’s restart. [Link]

Research

US dollar funding: an international perspective (BIS Committee on the Global Financial System)

A detailed review of why the dollar is such a critical piece of the global financial landscape, and how its movements and availability can have complicated effects on markets and economies around the world. [Link; 87 page PDF]

How Did COVID-19 and Stabilization Policies Affect Spending and Employment? A New Real-Time Economic Tracker Based on Private Sector Data by Raj Chetty, John N. Friedman, Nathaniel Hendren, Michael Stepner, and the Opportunity Insights Team (Opportunity Insights)

High frequency data suggests reopenings are not helpful for boosting local employment, while stimulus checks boost lower income household spending. Paycheck Protection Program loans had little effect on employment. The authors conclude that social insurance which protects incomes are more effective than other macroeconomic stabilization tools. [Link; 85 page PDF]

Structuring Federal Aid To States As An Automatic (and Autonomous) Stabilizer by Alex Williams (Employ America)

One social insurance policy option is the introduction of automatic block grants to states that insure lower levels of government against sudden revenue declines during a macroeconomic shock. [Link]

Social Media

TikTok Finally Explains How the ‘For You’ Algorithm Works by Louise Matsakis (Wired)

Algorithmically-driven Tik Tok serves up an endless feed of videos to each user, uniquely tailored to that user. This week the company published a blog post detailing the basics, which are weighted by everything from hashtags to the type of device being used. [Link; soft paywall]

Does Tweeting Improve Citations? One-Year Results From the TSSMN Prospective Randomized Trial by Jessica G Y Luc, Michael A Archer, Rakesh C Arora, Edward M Bender, Arie Blitz, David T Cooke, Tamara Ni Hlci, Biniam Kidane, Maral Ouzounian, Thomas K Varghese Jr, and Mara B Antonoff (PubMed)

Tweeting academic articles leads to a citation rate more than 4 times higher than un-tweeted articles, revealing the critical role Twitter plays in disseminating and highlighting new information. [Link]

Civil Liberties

After Barr Ordered FBI To “Identify Criminal Organizers,” Activists Were Intimidated At Home And At Work by Chris Brooks (The Intercept)

In response to massive protests over recent weeks, the FBI and DoJ more generally have singled out first-time activists for benign organizing activity. [Link]

Music

Top composers used to head to Hollywood. Now they’re into games by Will Bedingfield (Wired)

Hollywood blockbusters used to be a gravy train for composers, but in recent years the expansion of video games as their own category of prestige media have lured composing talent into their arena. [Link; soft paywall]

Investing

Investors Approaching Retirement Face Painful Decisions by Akane Otani (WSJ)

Large numbers of older investors were forced to sell at the worst possible time back in the first quarter as stocks plunged. Please note that this story features a correction at its end. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – Case Counts Rising

This week’s Bespoke Report newsletter is now available for members. Below is the opening excerpt.

The areas of the country where Covid case counts are currently rising the most are in Florida, Texas, Arizona, and California. So much for the heat keeping the virus at bay! On a day when Governor Cuomo thankfully ended his daily coronavirus press briefings, the stock market is once again focused on the daily case count numbers in other parts of the country. At least for most of the week, the market managed to shake off increased attention on case numbers. The S&P 500 was up 1.9% this week while the Nasdaq 100 rose 3.5%. Health Care, Materials, Tech, Consumer Staples, and Communication Services all rose more than 2%, while Energy was down 0.6% even though the oil ETF was up 6.8%. Outside of the US, China and India were up the most while Brazil, Spain, and Russia were in the red.

To read the full report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

100 Days

100 days ago today on March 11th, the WHO made it official and declared the COVID-19 outbreak a pandemic. Markets were already under a lot of pressure before the WHO declared the pandemic, but the 100 days since will probably go down as some of the craziest 100 days we’ll ever experience, not only in the market but in general society as well. More than enough ink and pixels have been spent discussing the societal impact at large, so we’ll spare you and just focus on the markets.

While much of the declines were already in the rearview mirror by the time the WHO made its announcement, equities still had a steep decline in the immediate aftermath. The large-cap Russell 1000, for example, fell another 19% to its March 23rd closing low, but after the rebound, the net change since the pandemic was officially declared has been a gain of 14.3%.

As impressive as the Russell 1000’s gain has been in the face of the global pandemic, many stocks have done a lot better than that. The table below lists the 25 stocks in the index that have seen the biggest gains so far during this pandemic. Topping the list is Wayfair (W) which has rallied more than 350%. If there is one thing Americans must have realized while they were stuck at home under lockdown it was that they needed some new furniture! Behind Wayfair, two other stocks have more than tripled and both were beaten down stocks from the Energy sector that were trading at less than $2 per share on March 11th. A number of familiar names standout including Moderna (MRNA), Twilio (TWLO), DocuSign (DOCU), Beyond Meat (BYND), and Etsy (ETSY), but looking through the list, there’s really a diverse group of names ranging from bombed-out stocks from the Energy sector (8 stocks), Consumer names (7 stocks), and the ever-popular software stocks from the Technology sector (6 stocks). It’s definitely been a rocky road for the markets over the last 100 days, but for anyone who had these names in their portfolio, they aren’t complaining. Click here to view Bespoke’s premium membership options for access to our weekly Bespoke Report which includes an update to our Stocks for the COVID economy portfolio that was released on March 11th.

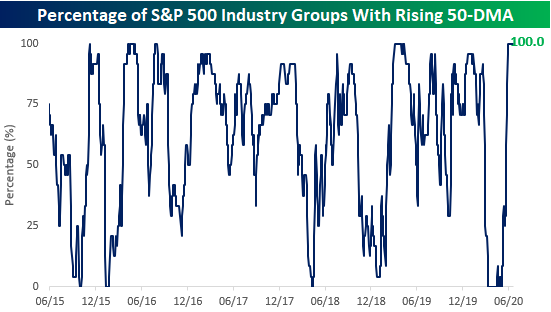

S&P 500 Industry Group Breadth Remains Positive

Equity markets have become a bit wobbly in the last week or so, but breadth, in terms of large-cap industry groups, still remains pretty robust. Relative to their 50-DMAs, all 24 S&P 500 industry groups still have rising 50-DMAs. When you consider the fact that the 50-day window spans the period going back to early April, a period encompassing most of what was one of the strongest 50-day rallies on record, the fact that every industry group has a rising 50-DMA isn’t all that surprising.

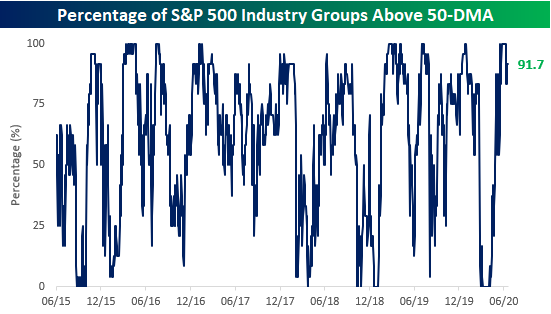

Even though all their 50-DMAs are rising, not every industry group is currently trading above its 50-DMA. While the reading briefly reached 100% in late May and early June, two industry groups have since pulled back below their 50-DMAs, putting the percentage at a still impressive 91.7%.

The table below summarizes industry group performance showing YTD performance, where each one is trading relative to its 50-DMA, as well as where the group is trading relative to its 52-week high.

As mentioned above, all but two groups (Drugs & Biotech and Food & Staples Retail) remain above their 50-DMAs, and another four are less than 2% above their 50-DMA. If Friday’s sell-off deepens into next week, the percentage of industry groups above their 50-DMAs has the potential to quickly sink as low as 75%. Of the 22 industry groups that are above their 50-DMAs, Autos and Tech Hardware are the only two greater than 10% above.

On a YTD basis, the S&P 500 is down less than 4%, but for the vast majority of industry groups, performance has been worse than that. Of the 24 groups shown, 16 are down more than 4% YTD, including eleven that are down over 10%. The worst performers of these losers include Energy, Banks, and Autos. While Energy gets most of the attention for being so weak, Banks are essentially down just as much! On the upside, just two industry groups are up over 10% (Retailers, which is basically Amazon, and Software & Services). Retailing is also the one industry group that is within 1% of a 52-week high and one of seven that is within 4% of a 52-week high. Click here to view Bespoke’s premium membership options for our best research available.