Commodity Performance in 2020

In the chart below, we show the year-to-date performance through last Friday of several different commodities. Fitting for a year with a pandemic ravaging the globe, vitamin C is in demand as orange juice is actually the top performing commodity year to date with a gain of 33.6%. Behind OJ, precious metals have been the next best performers. Gold is up the most of these with an 19.4% gain while silver is up about half that at +9.7%. The only other commodity shown that is in the green on the year is the industrial metal — copper.

On the down side, oil is the farthest in the red with a year-to-date decline of 34.2%. And conversely to OJ’s strong performance, another morning beverage that doesn’t provide a similar immune boost — coffee — is down 24%. Natural gas, corn, and platinum are all down more than 10% YTD, while wheat is down 6.7%. Click here to view Bespoke’s premium membership options for our best research available.

Communication Services and Consumer Staples Leading in 52-Week Highs

In Friday’s Bespoke Report, we broke down the rally off the bear market lows into three acts, noting a rotation out of “re-opening” stocks and back into the COVID economy stocks since early June. One metric where that is becoming evident is the sectors with the highest number of 52-week highs. As of Friday’s close, Communication Services had the highest net percentage of stocks at 52 week highs at just under a quarter of the sector’s stocks, 23.08%. While nearly 10 percentage points less, Consumer Staples has the second largest amount at new highs of the 11 sectors at 12.12%. For both sectors, these were the highest readings since the 2/19 high.

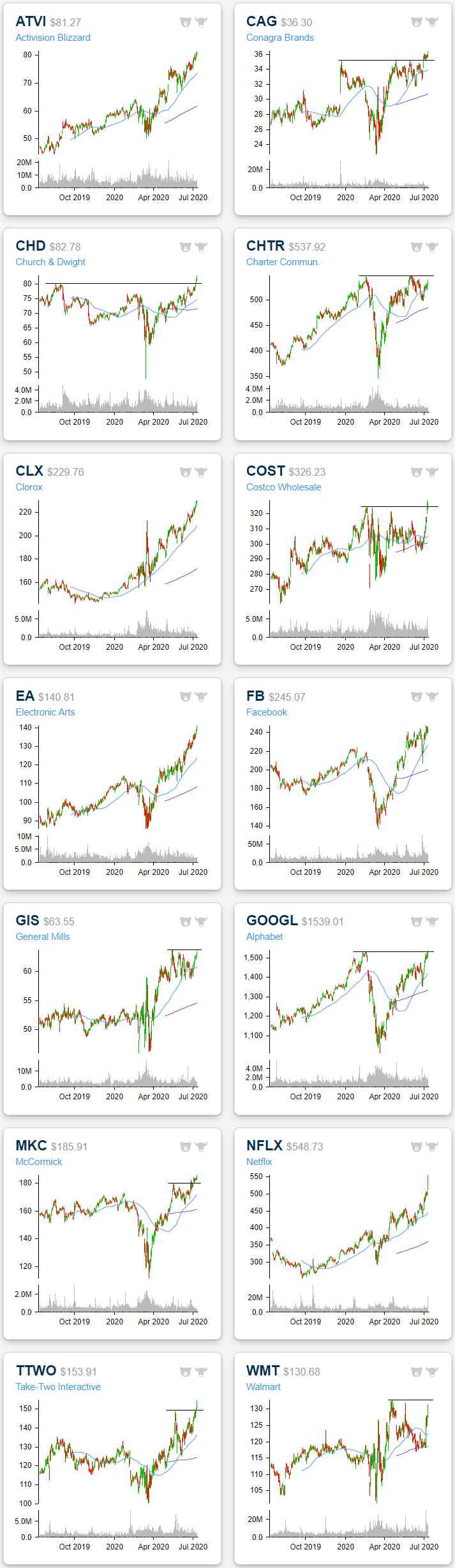

In the snapshot of our Chart Scanner below, we show the stocks in these sectors that reached new 52-week highs last Friday as well as a few others in sectors with interesting setups approaching or just off of 52 week highs. Of the Communication Services stocks, all of the major video game publishers—Activision-Blizzard (ATVI), Electronic Arts (EA), and Take-Two Interactive (TTWO)—made the list in addition to streaming giant Netflix (NFLX) and Google parent Alphabet (GOOGL). Each of the video game publishers has been in strong uptrends lately. Meanwhile, Netflix (NFLX) had an astounding end to the week, rallying 8.06% on Friday for its best single-day since March 23rd; the same day as the bear market low. Although all of these stocks have had strong uptrends, at the moment they are all extremely overbought meaning that now may not be the best entry point. Elsewhere in the sector, Charter Communications (CHTR) has been trending higher after a bounce off of its 50-DMA. If it continues to move higher it will be its second test (first one occurring in early June) of its February highs. Facebook (FB) is also right near a 52 week high after a sharp rally off of its 50-DMA in the past two weeks.

In the Consumer Staples sector, Conagra Brands (CAG), McCormick (MCK), Clorox (CLX), and Church & Dwight (CHD) also all reached new highs on Friday. For some like CAG and CHD, recent breakouts were above resistance from further back in 2019 while other highs for others like MKC were more recent. Other Consumer Staples stocks near 52-week highs include wholesale retailer Costco (COST) which broke out to a new high on Thursday but saw an inside day on Friday. General Mills (GIS) has broken its short term downtrend that has been in place since May over the past few weeks and has nearly returned to those prior highs. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke Brunch Reads: 7/12/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2020 Annual Outlook special offer.

COVID

US bets on untested company to deliver COVID-19 vaccine by Martha Mendoza and Juliet Linderman (AP)

In an effort to secure the material for rapid distribution of COVID vaccine doses, the government has invested more than half a billion dollars in a company that doesn’t have an approved device, doesn’t have a manufacturing facility, and is largely unproven. [Link]

Cause of Wuhan’s mysterious pneumonia cases still unknown, Chinese officials say by Helen Branswell (Stat News)

This article is a throwback to the very start of the COVID-19 outbreak Hubei, when a mysterious outbreak of pneumonia led to almost 60 hospitalizations by the first week of January. [Link]

Costs of COVID

The Toll That Isolation Takes on Kids During the Coronavirus Era by Andrea Patterson (WSJ)

While everyone feels the effects of isolation, they can have an especially extreme effect on children, adding concerns about childhood development to the public health calculation COVID is forcing governments to make. [Link; paywall]

Fearful and Frugal: Coronavirus Wreaks Havoc on America’s Psyche by Tiffany Kary (Bloomberg)

Survey data is suggesting a huge psychic toll on Americans as a result of the virus and the resulting economic impact. Austerity in the form of stockpiling, delayed purchases of durable goods, and less interest in public spaces are all warning signs for the viability of the economic recovery more generally. [Link; soft paywall]

Covid-19 Is Turning San Francisco’s Inequality Gap Into a Chasm by Olivia Rockeman and Gerrit De Vynck (Bloomberg)

COVID is hitting the more vulnerable workers in the service economy in a way that hasn’t had any salience for office workers in tech and other industries. [Link; soft paywall]

Carsyn Leigh Davis (Florida COVID Victims)

The horrifying story of an immunocomprised Florida teen who was exposed to COVID at a large youth event at her church. Her mother tried to treat her for the disease with totally ineffective anti-bacterials and hydroxychloroquine. Carsyn succumbed to the disease 12 days after the event at which she was exposed. [Link]

New York City

I’ve Seen a Future Without Cars, and It’s Amazing by Farhad Manjoo (NYT)

An argument and imagination of what a major city without cars looks like: less crowded, more vibrant, and faster-moving. [Link; soft paywall]

NYC Rental Market Pushed to Breaking Point by Tenant Debts by Prashant Gopal (Bloomberg)

With mass job loss in the hospitality industry, New York renters are completely incapable of covering their rent, and the result is a total inability for landlords to cover the cost of their debts, let alone property taxes and similar costs. [Link; soft paywall]

Heavier Reading

How to Fight Without Rules: On Civilized Violence in “De-Civilized” Spaces by Neil Gong (Social Problems)

This sociology paper is a bit off the wall, but is absolutely fascinating. The author sought to understand how “de-civilized” spaces without rules established new ways of ordering themselves. To do so, he participated in a no-holds-barred underground fight club that included weapons like sticks, chains, and dull knives as well as group battles. [Link; 18 page PDF]

The Dēmos In Dēmokratia by Daniela Cammack (The Classical Quarterly)

A novel reading of classical Greek sources which challenges our notion of democracy: not rule by all the people, but rule by the mass of people outside of the elite. The implications of that early political arrangement and our modern systems of representative government mediated by technocrats are profound: democracy in its original Greek forms was not a process of empowering elites (as it is today, via election of representatives) but was in fact a process of empowering everyone else over elites. [Link; 20 page PDF]

A tale of two wage subsidies: The American and Australian fiscal responses to COVID-19 by Steven Hamilton (National Tax Journal)

A comparative analysis of the different approaches to subsidizing wages taken by the US and Australia, arguing that a lack of infrastructure in the US led to a far less effective Paycheck Protection Program) that underperformed the Australian solution which relied on its tax payment systems instead of private lenders. [Link; 20 page PDF]

Eras Ending

Brooks Brothers files for bankruptcy by Jordan Valinsky (CNN)

The venerable American menswear brand survived the Civil War, two World Wars, and everything else since 1818, but COVID has ended its run. [Link]

Grim Day for Pipelines Shows They’re Almost Impossible to Build by Rachel Adams-Heard and Ellen M. Gilmer (Bloomberg)

Earlier this week a federal judge ordered the shutdown of the Dakota Access pipeline, followed by the cancellation of a planned pipeline by Dominion and Duke Energy. Well-funded and litigious environmental groups have proven incredibly effective at raising the costs of new pipeline projects beyond the point of viability. [Link; soft paywall]

Long Reads

The Hero of Goodall Park: Inside a true-crime drama 50 years in the making by Tom Junod (ESPN)

An incredible yarn focused on cars, baseball, the ephemerality of life, and history in a giant interconnected narrative. [Link; auto-playing video]

Markets

75 Years of American Finance: A Graphic Presentation 1861-1935 (St. Louis Fed FRASER)

A hand-drawn and annotated history of American financial markets and economic activity stretching from the start of the Civil War to the depths of the Great Depression. [Link]

Are Stock Investors ‘Irrationally Exuberant’ Again? by Mark Hulbert (WSJ)

An argument that basically unremarkable performance for IPOs, normal equity issuance, valuations of dividend-paying stocks versus those without a dividend, and closed-end fund discounts are all pointing to an unremarkable market relative to the late-1990s tech bubble. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — A Rally with Three Acts

This week’s Bespoke Report newsletter is now available for members.

The S&P 500 was up 3% on the week, while the Nasdaq 100 was up 6.6% (leaving it up 24.6% YTD). Chinese stocks also had a big week with a gain of 15.9%. Within the US, we continue to see huge performance divergence between the largest and smallest stocks. Within the large-cap S&P 500, the cap-weighted index was up 3% on the week, but the equal-weight index was up just 0.3%. YTD, the cap-weighted S&P is down just 0.28%, but the equal-weight index is still down more than 10%.

Here is a stat for you that highlights strength at the top: the five largest stocks in the S&P added $352 billion in market cap this week alone. That would rank as the 10th largest stock in the index. At the bottom of the index, if the 100 smallest stocks in the S&P 500 each doubled from here, it would only add 2.5% to the index. If only Apple (AAPL) were to double from here, it would add 6% to the index.

To read our full Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Bullish Sentiment Stops Sliding

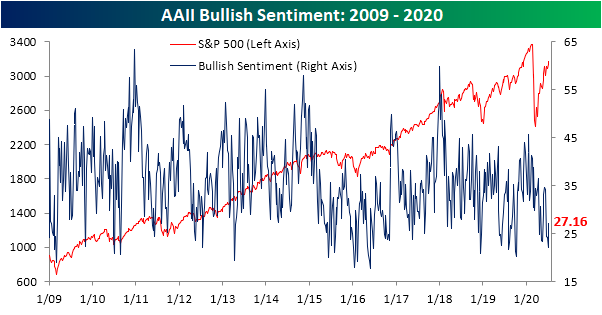

While the past week’s gains are mostly being erased today, for the most part, the S&P 500 has been trading firmly higher which has lifted sentiment. AAII’s weekly reading on bullish sentiment was lifted as a result, rising from 22.15% to 27.16%. That is the highest level of bullish sentiment since June 11th, and the 5 percentage point week over week increase was the biggest jump since the end of May. Not only was it the largest single-week increase in over a month, but this week snapped a four-week long streak in which bullish sentiment has declined. With the streak now over, it was the longest streak of consecutive declines in bullish sentiment since April of 2018 when sentiment also fell for four weeks. While higher this week, bullish sentiment is still below its historical average of 38% by at least one standard deviation as it has been for four straight weeks now. That is the first such streak since August of last year.

Meanwhile, bearish sentiment has come back down reaching 42.67%. Mirroring bullish sentiment, that is the lowest reading for bearish sentiment since June 11th, but it remains above its historical average by at least one standard deviation as has been the case for the past four weeks.

Bearish sentiment was not the only one to fall this week. Neutral sentiment also slightly pulled back falling to 30.17% from 31.96%. Although lower this week, neutral sentiment is still at a much more normal reading than the past few months’ extreme lows. In fact, this week marked the first time that neutral sentiment was above 30% for back to back weeks since February. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Off the Shelf Indicators – Google Search Trends Update

Internationals Benefit From Dollar’s Drop

During the market turmoil in February and March, the US dollar dropped 4.81% from its high on February 20th to its low on March 9th. That was followed up with a massive run up of 8.26% over the next ten days as the dollar index rose to its highest levels since the final days of 2016/first days of 2017. Since peaking on March 19th, however, the dollar has faced constant selling as it now sits at the lower end of the past couple of year’s range. A weaker dollar, all else equal, would make the price point of US products more attractive to foreign buyers and as a result, should theoretically bode well for companies that base a larger share of their revenues from outside the US.

In the chart below, we show the average performance of Russell 1000 stocks since the dollar’s high on March 19th based on deciles of international revenue exposure using data from our International Revenue Database. The 1st decile represents the stocks that have the highest share of total revenues derived from abroad while the 10th decile includes all stocks who’s revenues entirely come from within US borders. As shown, those with the most international exposure—which includes many semiconductors and some travel-related and Consumer Staples names— have generally outperformed most other deciles in that time. Granted, this was not the strongest decile. The 8th and 9th deciles were the strongest performers since March. These deciles are generally stocks with less than a fifth of revenues coming from abroad, and they actually saw even stronger returns on average since March 19th. Meanwhile, those with no international exposure are only up 34.5% on average since March 19th. Click here to view Bespoke’s premium membership options for our best research available.

Are Claims Rising or Falling?

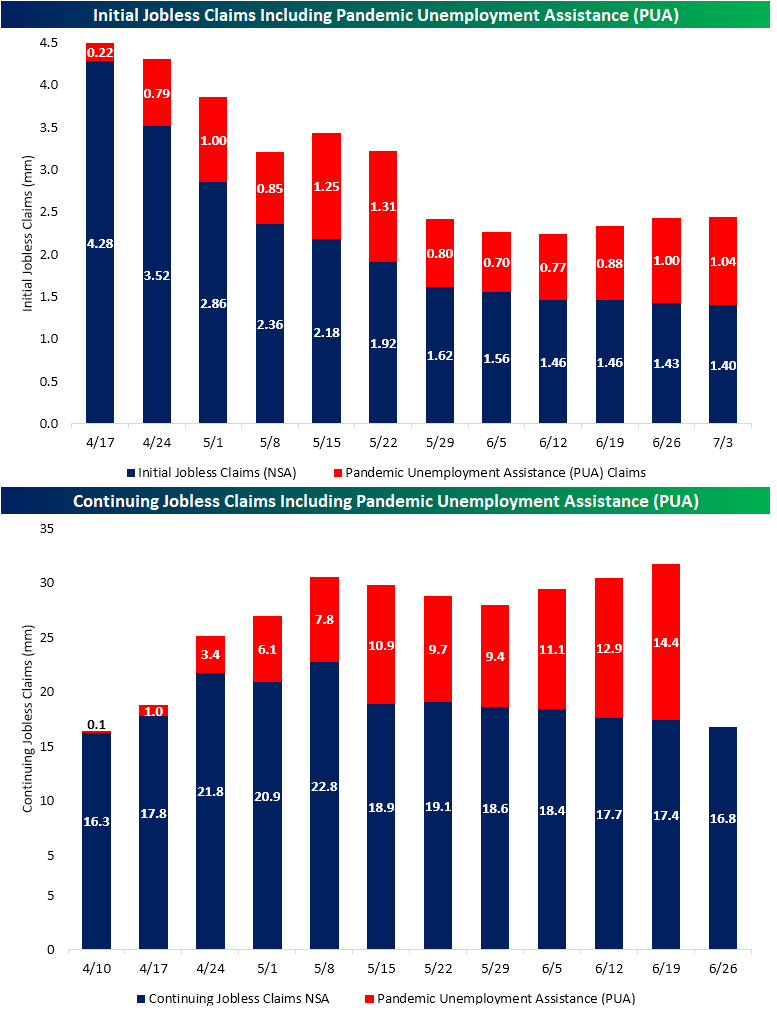

Jobless claims remain elevated on a seasonally adjusted basis though they did fall once again this week marking a 14th consecutive week with lower initial claims. The current streak of weekly declines now doubles what was the previous record streak of 7 weeks ending in November of 2013 and October of 1980. Claims came in at 1.3 million which was below estimates of 1.375 million but still were down 99K from last week. As we have frequently made note of recently, that is a smaller improvement than earlier in the pandemic, but this week’s decline was the largest since the first week of June’s 331K drop.

On a non-seasonally adjusted (NSA) basis, claims came in a hair below 1.4 million, down from 1.431 million last week. Compared to seasonally adjusted claims, the NSA print was less impressive at 31.6K but that too was the largest decline since June 12th. Again, the pace of improvement remains lackluster when compared to the first leg lower earlier in the spring. Whereas each week of May saw NSA claims average a decline of 379K, since the beginning of June claims have only averaged a 44K decline even with this week’s larger drop.

As for those that remain unemployed, continuing claims fell by 698K to 18.062 million. That is the lowest level of continuing claims since mid-April’s 18.011 million reading. Continuing claims have now fallen for five consecutive weeks; far from the longest streak on record, but that is the longest such streak since another five-week-long streak in April of last year.

While the trends have generally been positive for the past several weeks when factoring in other claims like Pandemic Unemployment Assistance (PUA) the picture is not as rosy. In addition to the roughly 1.4 million initial jobless claims filed (on a non-seasonally adjusted basis) this week, there were another 1.04 million PUA claims filed, totaling 2.439 million claims on the week. As shown in the chart below, that is actually up from 2.428 million last week. This week’s increase was actually a third consecutive week with higher overall claims and the highest level since the second half of May.

Continuing PUA claims are lagged and an extra week from the already one week lag in continuing claims meaning the most recent data for these claims that we have is for the week ending June 19th, however, these are showing the same dynamic. Unadjusted for seasonality, for the week ending June 19th regular continuing claims totaled 17.4 million which was lower for a fourth consecutive week. On top of those, PUA claims rose to 14.4 million. Adding in PUA claims, this was the third consecutive higher reading for PUA claims. Unadjusted continuing claims including PUA claims now sits at 31.8 million which is the highest level since they were first reported in April. In other words, regularly reported jobless claims have improved recently but the addition of other types of claims like PUA, paints a weaker picture of the labor market in which claims are rising rather than falling. Click here to view Bespoke’s premium membership options for our best research available.

Tesla (TSLA) Now the 16th Largest US Stock

Tesla’s (TSLA) meteoric rise in recent weeks has been widely followed especially as the company’s market cap eclipsed that of all other major auto manufacturers including the previous largest company: Toyota. While it is not a member of the S&P 500, in the table below we compare TSLA to the other 29 largest stocks (by market cap) in the index.

As we noted on Monday, TSLA has been one of the best-performing stocks year to date out of a broader range of stocks (the Russell 1000), but among the largest stocks in the S&P 500, its 226.51% YTD gain is even more impressive. That is triple the performance of the next best performer of these 30 stocks — NVIDIA (NVDA) — which has risen 73.86% in 2020.

Back at the start of the year before its 200%+ increase, TSLA was valued around $75 billion, which is around the size of the current market caps of stocks like American Express (AXP) and Altria (MO). After its massive run higher, it would now be the 16th largest stock in the S&P 500 just behind names like Home Depot (HD) and UnitedHealth (UNH). When it comes to the actual price of a share, TSLA would also be close to the top of the list for the S&P 500. If it was in the S&P, Tesla would be one of six other stocks in the index with prices above $1,000 per share. Click here to view Bespoke’s premium membership options for our best research available.

China Charges Higher

We’ve highlighted the run in Chinese equities quite a lot in the last several days, but it keeps getting more and more extreme. With a gain of over 1% overnight, China’s CSI 300 not only turned in its eighth straight day of gains but also its eighth straight day of rallying more than 0.5%. In the history of the CSI 300 dating back to 2002, there has only been one other time where the CSI 300 saw eight or more straight daily gains of 0.5%. That was back in April 2007.

If you don’t remember what was going on with Chinese equities back in April 2007, take a look at the chart below. The last time the CSI 300 had a streak of 8+ days of 0.5% daily gains, the CSI had already doubled in the prior six months. From there, though, it went on to nearly double again in the next six months. Eventually the bubble burst, and it wasn’t much more than a year later that the CSI 300 was back below where it was in April 2007. Like what you see? Click here to view Bespoke’s premium membership options for our best research available.