Payrolls Rolling Lower

A very weak jobs number from the Labor Department for the month of March just rolled in. Nonfarm payrolls fell 701K in March compared to 273K added jobs in February. That was also a much weaker number than the consensus forecast which was only predicting a drop of 100K. In fact, of all reports since 1998 in our Economic Indicator Database, this was the largest miss. This was also the first time since September 2010 that monthly payrolls have been negative.

Taking a longer-term look, this was also the eighth largest decline on record in the data going back to early 1939. The last time that a larger decline was observed was in March of 2009 (-800K). One important factor to note about this month’s report is the collection period. Since the reference week for the monthly report is in the first half of the month, the massive job losses recorded in the second half of March were not even fully picked up in this report. In other words, next month’s report is going to be a LOT worse. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Sector Relative Strength

Over the past year, the Technology sector has been the most notable sector in terms of outperformance relative to the S&P 500. As shown in the charts from our Sector Snapshot below, the relative strength chart for Technology has been in a steady uptrend for the past twelve months without much interruption even while the decade long bull market was coming to an end. In fact, last week it was the first sector to exit oversold territory after every sector was oversold for 13 days. The other sectors have not been as lucky. During the recent sell off, the relative performance of most sectors, especially cyclicals like Energy, Financials, and Industrials, fell sharply (indicating even worse declines than the S&P 500). Consumer Staples and Health Care, on the other hand, have seen much stronger performance than the rest of the market. Start a two-week free trial to Bespoke Institutional to access Sector Snapshot and much more.

The Closer – Crude Contango Collapse – 4/2/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin by reviewing crude oil’s record setting session. We then go into the Federal Reserve’s H.4.1 report on the Fed’s balance sheet. Turning to macroeconomic data, we review US trade data for February including US-China trade data. We close out tonight’s note with a look the geographic impact of COVID-19 on jobless claims and restaurant revenues.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke Consumer Pulse Report — April 2020

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Consumers Turn Bearish on Equities

Tuesday’s Consumer Confidence report managed to exceed expectations, but as we noted at the time, the survey for the March reports cuts off on the 18th, so as economic conditions turned south, sentiment levels also likely declined. One area of the report where sentiment already has seen a notable decline is in consumer sentiment towards stock prices. As shown in the top chart below, the percentage of consumers expecting stock prices to decline nearly doubled from 21.7% up to 39.2% while the percentage of consumers looking for higher prices dropped from 43.1% down to 32.3%. In the case of negative sentiment, the percentage of bearish consumers hasn’t been this high since late 2012.

Given the major shift in sentiment, the spread between bullish and bearish consumers has seen a major reversal falling from firmly positive (21.4) to firmly negative (-6.9). By this measure, the spread between bullish and bearish investors hasn’t been this negative since February 2016. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

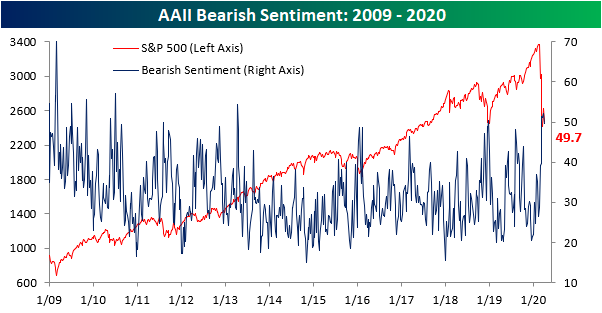

Sentiment Staying Home

Like the S&P 500 and many Americans practicing social distancing, investor sentiment hasn’t moved too far over the past week. Bullish sentiment rose from 32.9% to 34.24%. That is one of the smaller moves in recent weeks which leaves the indicator just about in line with the average for bullish sentiment (34.44%) since the bear market began on 2/19.

It may not have been by much, but bearish sentiment dropped below 49.7% for the first time since the first week of March. While lower, bearish sentiment remains very elevated compared to the past decade. The over 10% rally for the S&P 500 since last Monday’s low has not been enough to persuade a more optimistic outlook for the bulk of investors.

Not all the losses in bearish sentiment went to bulls. 16.03% of investors reported neutral sentiment this week which is a full percentage point higher than last week’s reading. While that is an improvement, this reading remains at the extreme end of the past several years’ range. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

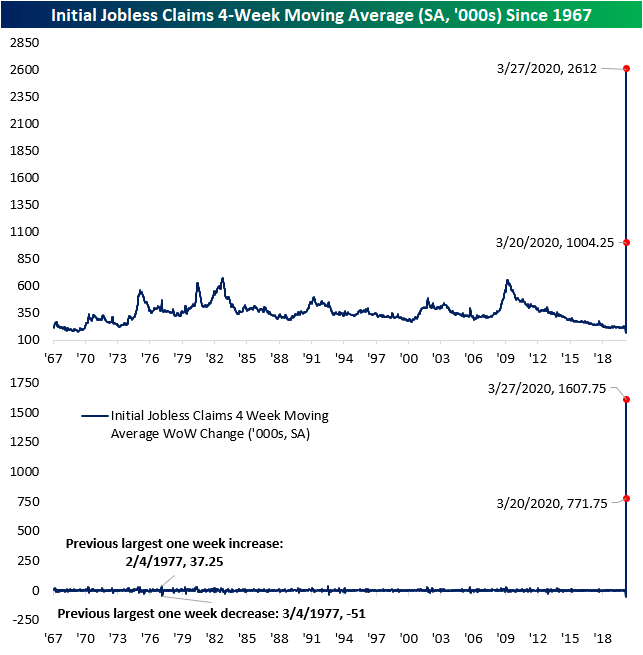

New Record Doubles The Old Record

Last week, a record number of Americans filed for unemployment as initial jobless claims surged to 3.283 million. That number was revised higher to 3.307 million this week setting an even higher bar for a new record. Despite that, this week’s print doubled last week’s record number as jobless claims came in at 6.648 million. Put another way, that is roughly 2% of the entire US population filing for unemployment this week alone! Not only did this week’s release double last week’s record print, but it was also above the most aggressive forecasts of 6.5 million. With claims having risen this much, any historical precedent has been utterly blown out of the water. The past few weeks are multiples larger than even past recessions’ peaks. Additionally, the size of the week over week changes have also been much larger than anything previously observed in the history of the data.

One silver lining of the report is due to seasonal factoring, the adjusted number is about 824K higher than the non-seasonally adjusted number which came in at 5.824 million this week. In other words, the actual number reported before seasonal adjustment is still very bad, but not quite as bad as the seasonally adjusted number lets on. As with the adjusted number, this did double what was already a record print last week on the largest week over week change ever.

Normally, the four-week moving average would help to smooth out any week to week fluctuations of this data. But seeing as the current situation is far from normal, there is not much smoothing happening. Even the moving average has ripped higher by more than any other period in history. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – 4/2/20 – 2% of the Population Files For Unemployment

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

All eyes were on jobless claims this morning, which were expected to rise by 3.7mm, though estimates were wide-ranging from 800,000 to 6.5mm. So, where did they come in? How about 6.648 million. That was above all economists forecasts!

Equity markets were pricing a gain of more than 1% but have given up half of those gains in the immediate aftermath of the report.

Read today’s Bespoke Morning Lineup for a discussion of the latest trends and statistics of the outbreak, overnight moves in the market, and some really weak employment-related data out of Spain.

Last week’s jobless claims reading reflected the fact that 1% of the US population filed for unemployment. With claims doubling this week, that means 2% of the US population filed for claims this week Not the labor force but the entire population. Given the moves in claims over the last two weeks, the historical chart of claims is essentially useless. That surge in claims we saw during the financial crisis? It looks like nothing more than a speed bump in relation to what we’re going through now.

The Closer – The Markets’ New Me, Same As The Old Me – 4/1/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we show how the past couple of day’s price action is similar to the start of the bear market. We then delve into the Fed’s repo operations before turning to over to today’s ISM release. We close out tonight’s report with a look at the shock to petroleum stockpiles and demand as well as weekly fund flows.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Fixed Income Weekly – 4/1/20

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we discuss the income opportunities in S&P 500 dividends.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!