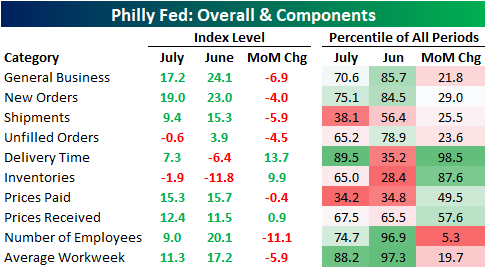

Philly Fed in a Funk

On the back on Monday’s weaker Empire Fed survey, today’s release of the Philadelphia Fed’s Business Outlook Survey similarly showed a slowdown in activity during August. The headline index fell 7 points to 17.2. While that is a third consecutive expansionary reading, it also marked back to back declines. That means that the region’s manufacturing sector has continued to grow, but at a decelerating pace in the past two months.

Like the headline number, many of the individual categories also remain in expansion territory but were lower than last month. The only readings to rise month over month were the indices for Delivery Times, Inventories, and Prices Received. Inventories as well as the index for Unfilled Orders were the only ones to be in contraction in August.

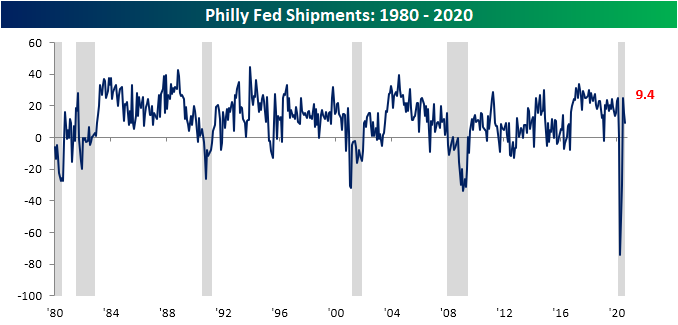

Demand continues to improve with both the indices for New Orders and Shipments showing another expansionary reading in August, but both were also lower indicating demand did slow somewhat. While the index for New Orders remains at a healthy level historically, in the upper quartile of all readings since 1980, Shipments are at a more muted level in just the 38th percentile.

As for employment metrics, there was a slowing in the Number of Employees hired in the region with that index falling from 20.1 to 9. That 11.1 drop was the biggest change of any sub-index this month and with respect to that index, this month’s decline was in the bottom 5% of all monthly changes. Not only did the index for Number of Employees fall, but so did the index for Average Workweek, although it still remains in the upper end of its historical range. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Leading Indicators Up Again

The Conference Board’s Index of Leading Indicators for July came in stronger than expected, rising 1.4% compared to expectations for a gain of 1.1%. From its high of 112.0 in January to its low in April, leading indicators saw the largest three-month decline in the history of the index. Since then, we’ve now seen the largest three-month increase on record. Unfortunately, the magnitude of the increase hasn’t been nearly as strong as the decline, but it’s an improvement nonetheless.

This month’s stronger than expected increase in leading indicators was also notable for what it suggests about the business cycle. As shown in the chart, the bounce of the last three months has now erased nearly half of the decline from January through April, but more importantly, the only other times the index has risen three times in a row during a recession was in the last three months of the 1981/1982 contraction from September through November and the last three months of the Financial Crisis from April to June 2009. If past history is any guide, that would suggest that the COVID-recession ended in July or earlier.

Looking at the ratio of leading to coincident indicators shows an even stronger picture. As we have mentioned numerous times in the past, this ratio always starts to roll over in advance of a recession. Interestingly enough, leading up to the most recent recession, this ratio started drifting lower beginning in late 2018, although not anywhere close to the typical weakness you would see heading into prior recessions. In other words, the economy was already on a relatively shaky footing in advance of COVID.

In the last three months, though, the ratio has seen a large rebound nearly erasing all of its declines from the last peak. At 22 months now since the last peak, the current streak has been a lengthy one, but looking just at the period since the end of the Financial Crisis, the current streak isn’t even the longest. That title belongs to the 27-month drought from mid-2011 through late 2013. Like what you see? Start a two-week free trial to Bespoke Institutional for full access to all of our research and interactive tools.

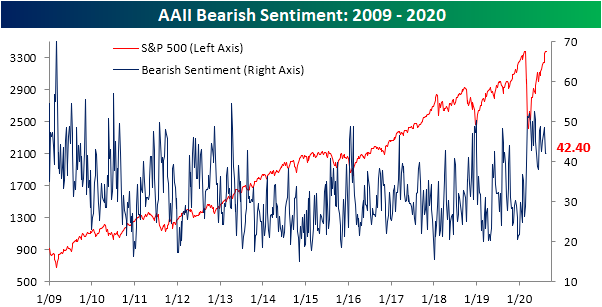

Sentiment Snoozefest

Weekly results from AAII’s investor sentiment survey was uneventful this week. All of the readings across bullish, bearish, and neutral sentiment saw a move of less than one percentage point. That is the first time this has happened since June 27th of last year and other than those two occurrences, it has only happened 15 other times throughout the survey’s history. Bullish sentiment held firm above 30%, rising 0.35 percentage points to 30.39%. That was bullish sentiment’s third consecutive week moving higher.

Bearish sentiment remains the predominant sentiment reported by investors as it rose slightly from 41.12% to 42.4% this week. In absolute terms, that is the smallest weekly change for bearish sentiment since a 0.03 percentage point move on March 19th.

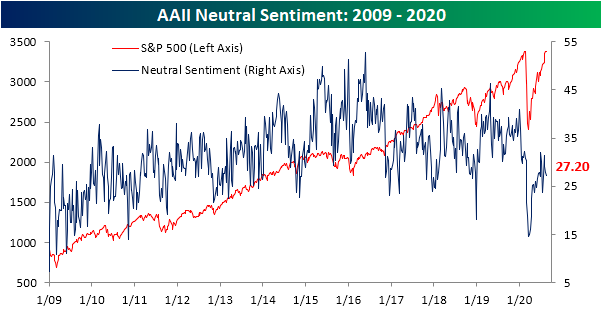

Those small gains to bullish and bearish sentiment took from neutral sentiment which fell 0.64 percentage points to 27.2%. Of the three readings, this was the largest move this week.

With bearish sentiment still outweighing bulls, the bull-bear spread remains negative as it has for a record streak of 26 weeks. Like what you see? Start a two-week free trial to Bespoke Institutional for full access to all of our research and interactive tools.

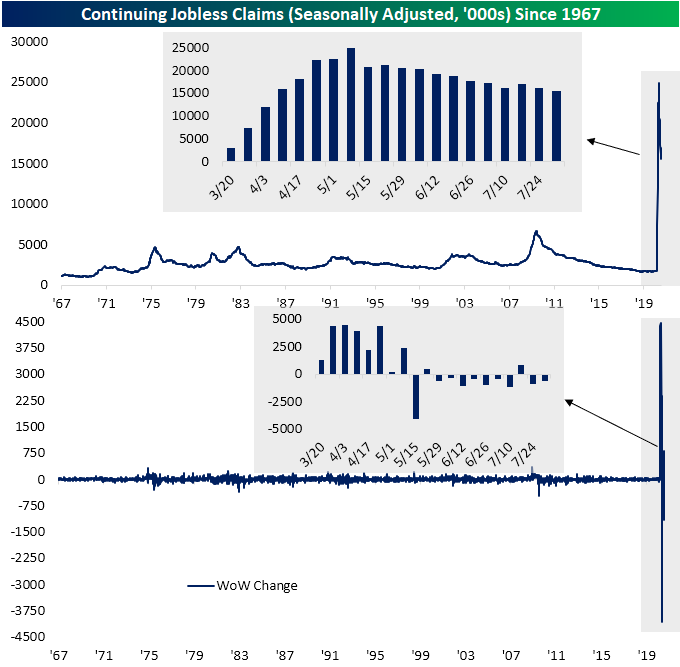

Jobless Claims Back Above 1 Million

Last week, initial jobless claims came in below one million for the first time in 21 weeks. Even though another sub-million print was expected, claims actually saw a dramatic increase rising to 1.106 million. The 135K increase week over week was the biggest single-week increase of the pandemic excluding the first two enormous jumps in the second half of March; both of which were increases of over 3 million. Even though that is a big jump from last week, the actual level of claims remains around some of the lowest levels since the pandemic began. In fact, despite the large increase this week, claims are still lower than they were two weeks ago.

On a non-seasonally, adjusted basis claims were 891.5K this week. That actually marks a third straight week with claims below a million as the level of this reading continues to offer a bit more of an optimistic view than the seasonally adjusted number. Although NSA claims remain around the lowest levels of the pandemic, there was not an improvement this week. The 52.8K increase week over week was the first rise in four weeks and was the third-largest increase since the first week of April.

As we have noted recently, the summer months through September have seasonally been a strong time for claims as the nonseasonally adjusted (NSA) number has tended to drift lower. The increase this week is out of the ordinary for this point in the year as it was the first time in the history of the data (since 1967) that NSA claims for the current week of the year (33rd week) were higher from the prior week. In other words, the rise in claims this week bucked a historically consistent trend of seasonal strength.

The big drop in claims last week benefitted the most recent reading for continuing claims (lagged an additional week to initial claims) which have continued to decline as they broke below 16 million for the first time since April 10th. The 604K WoW decline was slightly smaller than last week’s 861K decline

For Pandemic Unemployment Assistance (PUA), initial claims were also higher, rising over 50K from last week. In total, claims (the headline number plus PUA claims) rose to 1.43 million from 1.33 million last week. Again while that is an increase from last week’s lows, it is still around some of the strongest levels of the pandemic. Total NSA continuing claims for the last week of July (continuing PUA claims are lagged another additional week), on the other hand, fell slightly from 26.6 million to 26.4 million. That was entirely thanks to a drop in regular claims as PUA claims actually rose from 10.7 million to 11.2 million. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Industry Group Breadth Positive

While the S&P 500 moved to a new all-time high on a closing basis Tuesday, we wanted to check in on breadth with respect to S&P 500 industry groups and how they’re trading relative to their 50 and 200-day moving averages. While we hear a lot about the largest five stocks in the S&P 500 accounting for the lion’s share of the gains, it’s not as if everything else in the market is falling apart.

Looking first at S&P 500 industry groups versus their 200-day moving averages (DMA), while not extraordinary by any means, more than two-thirds are currently above their 200-DMAs, and the level continues to trend higher. A more worrying sign would have been if this reading was much higher and showing signs of rolling over. The seven industry groups that are currently below their 200-DMAs are Banks, Consumer Services, Energy, Insurance, Real Estate, Telecom Services, and Utilities.

On a shorter-term basis, the percentage of industry groups currently above their 50-DMAs is considerably higher at over 95%. In other words, the only industry group not above its 50-DMA is Energy. What else is new? Now that the S&P 500 has taken out its February highs, these breadth readings will be key indicators to watch for signs of participation (or lack thereof) in any rally. Click here to view Bespoke’s premium membership options for our best research available.

Fixed Income Weekly – 8/19/20

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review the implications of the euro’s large rally in recent weeks.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Bespoke CNBC Appearance (8/19)

Bespoke co-founder Paul Hickey appeared on CNBC’s Squawk Box on Wednesday to discuss markets after the S&P 500’s new high. To view the segment, please click on the image below. Click here to view Bespoke’s premium membership options for our best research available.

Tesla (TSLA) Now in Top 10

Tesla (TSLA) announced a 5 for 1 stock split one week ago after the close on August 11th. Shares are up 37% since then.

While Tesla (TSLA) is not yet in the S&P 500, if it were, it would now be the 10th largest stock in the index. TSLA’s $350 billion market cap puts it in between Walmart (WMT) at $380 billion and Procter & Gamble (PG) at $341 billion. Click here to view Bespoke’s premium membership options for our best research available.

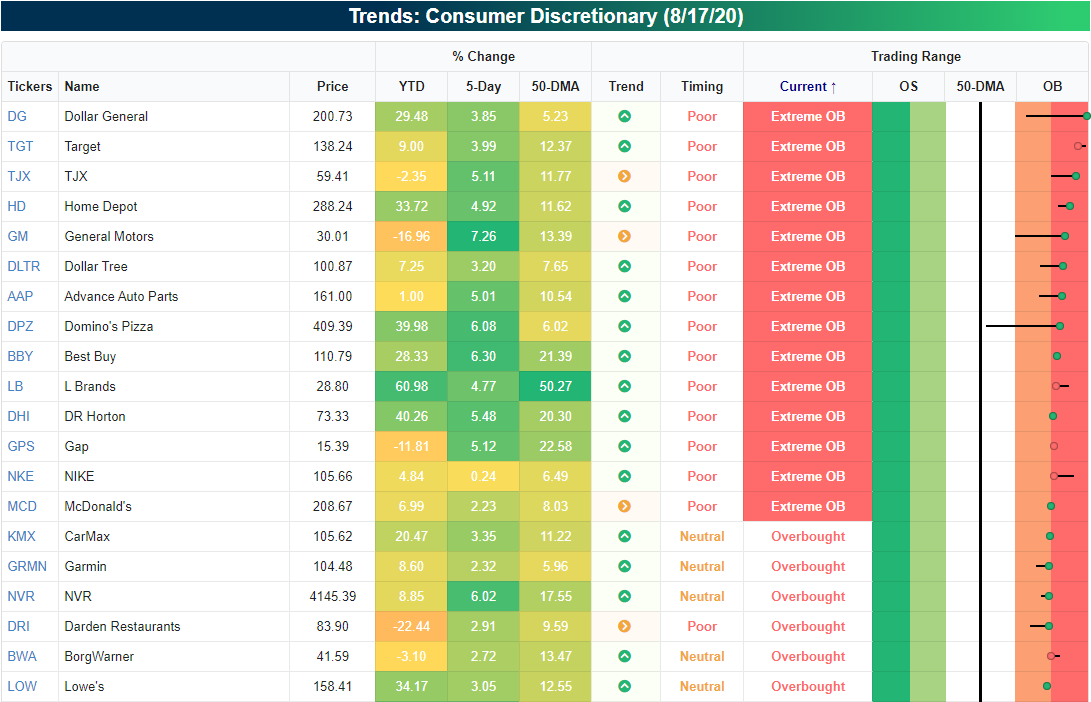

Retail Earnings On Deck

Earnings season came to its unofficial end today with the release of Q2 results for Walmart (WMT). As shown in the snapshot of our Earnings Explorer below, the earnings slate has slowed considerably but there are still several reports per day over the next month. The busiest day will be August 27th with 37 reports.

Similar to today, retail earnings dominate the upcoming calendar. While WMT and Home Depot (HD) blew the doors off their reports, upcoming earnings will give a better picture of how the consumer has been impacted by the pandemic. Over the next month there are 52 retailers scheduled to report second-quarter results. Of these retailers, less than half are expected to show positive EPS. Companies that have historically beaten EPS the most include Ollie’s Bargain Outlet (OLLI), Ulta Beauty (ULTA), and Restoration Hardware (RH). In terms of topline results, Vipshop (VIPS), OLLI, and Alibaba (BABA) have topped sales forecasts the most consistently.

In terms of stock price reactions, Land’s End (LE) has averaged the strongest performance on earnings days with an average full-day gain of just under 6% with positive returns a little better than half the time. Sportsman’s Warehouse (SPWH) is the only other stock on this list to have averaged a gain of more than 5% on earnings days. SPWH along with ULTA, and Burlington Stores (BURL) have also been the ones to most consistently experience a positive stock price reaction.

Given retailers tend to be fairly seasonal businesses, the table below looks only at these companies’ beat rates and average stock price reactions in just their reports for the Q2 earnings season. As shown, Sportsmans Warehouse (SPWH) has most consistently topped EPS and sales estimates. SPWH has averaged a 9.11% gain following its Q2 reports. On a side note, PDD has a 100% beat rate for its Q2 earnings season reports, but it has only had one prior report during the Q2 earnings season. While SPWH has seen positive returns, stocks like At Home Group (HOME), Duluth Trading (DLTH), and Vipshop (VIPS) have all averaged the worst performance fin reaction to their Q2 earnings reports.

As for where retail stands ahead of their earnings, the snapshot below from our Trend Analyzer shows the 20 most overbought stocks in the sector. Many of the stocks making the cut are retailers that are currently extremely overbought after sizeable runs. As of Monday’s close, the average S&P 500 retail stock is 1.7 standard deviations above its 50-DMA. Click here to view Bespoke’s premium membership options for our best research available.

One Streak Ends, A Longer One Continues

It was a big, albeit brief, moment for the market today when the S&P 500 notched a new intraday record high, fully erasing all of the declines from the COVID-crash in February and early March.

Today’s new high for the S&P 500 ended a streak of 125 trading days without a record intraday high. The chart below shows prior streaks of trading days without an intraday high since 1983 (when our intraday database begins). What’s amazing about the current period is that despite losing roughly a third of its value, the 125 trading day gap between record highs is barely even a blip on the chart, and doesn’t even rank in the top ten in terms of longest streaks without a new high. Even looking at more recent history, since the S&P 500 took out its pre-financial crisis high in early 2013, there have been three other streaks where the S&P 500 went longer without notching a new all-time high.

The S&P 500 may have notched a record high this morning, but it’s a much different picture for the small-cap Russell 2000. At the same time that confetti was streaming for the S&P 500, the Russell not only remains well below its February high, but it’s also nearly 10% below its record high from nearly two years ago at the end of August 2018.

While the S&P 500’s just-ended streak of 125 trading days without a record high wasn’t even one of the ten longest, the current streak of 493 trading days that the Russell 2000 has gone without a new high ranks as the 5th longest streak since 1983. Comparing the chart of Russell streaks below to the same chart for the S&P 500 shows that the Russell has been much more streaky. While the S&P 500 has only had three prior streaks of longer than 400 trading days without a new high, the current streak for the Russell ranks as its eighth such streak of more than 400 trading days. Start a two-week free trial to Bespoke Institutional for full access to our research and interactive tools.