Stocks Near Pre-COVID Highs

Yesterday, we outlined the percentage of stocks in each S&P 500 sector that were below their pre-COVID highs to show that many of the stocks that surged due to pandemic effects have significantly fallen off, netting long-term holders a negative return since the onslaught of the pandemic. Yesterday, the S&P 500 by 1.6% to a new 52-week low on a closing basis, but the index was still up over 15% relative to the pre-COVID highs. Along with this move from the broader index, three stocks broke below their pre-COVID highs for the first time. As things currently stand, 41.2% of S&P 500 members are now below their pre-COVID highs, and an additional 18 stocks (3.6% of members) are just 2% or less above their closing high prices between the start of 2019 and the end of February 2020.

Below we show the six-month price charts of the three stocks that traded below their pre-COVID highs for the first time yesterday. Click here to view Bespoke’s premium membership options.

As mentioned above, there are 18 stocks that were trading within 2% of their pre-COVID highs as of yesterday’s close, and charts of each one are highlighted below. Looking through them, some have already traded well below their pre-COVID highs but have since rebounded while a number of others haven’t traded at these levels in months. In fact, six of them closed at new six-month lows yesterday (AOS, BR, LEN, MGM, NVR, and SYK).

Sentiment Just Like Bear Markets

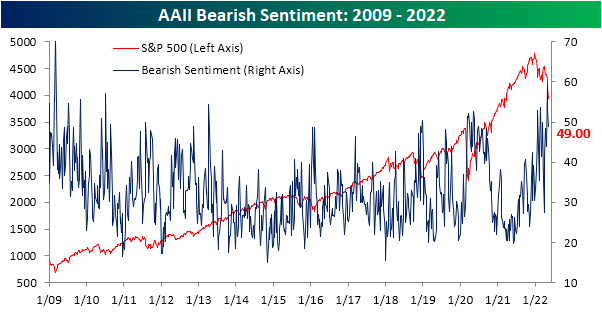

The past week may have seen the S&P 500 and other major US indices breach to fresh lows on steep declines that are nearing bear market territory, but the AAII sentiment survey has not fallen to its own lows as might have been expected. Bullish sentiment fell back below 25% this week but is still several percentage points above the lows in the teens from only a few weeks prior.

Historically, when the S&P 500 has hit 52-week lows as it has in the past week, bullish sentiment has usually been even higher with an average reading of 29.15%. The chart below shows the levels of bearish, bullish, and neutral sentiment in the AAII survey at the time the S&P 500 first traded into bear market territory (down 20% from a prior peak) for each bear market since the survey began in 1987. At 24.3% now, the current reading of bullish sentiment is on the low side compared to prior bear markets. The only two bear markets where bullish sentiment was lower were July 2008 and February 2009.

Although bullish sentiment declined, bearish sentiment also pulled back below 50% for the first time since the week of April 20th. Even with the decline, though, bearish sentiment remains at a historically high level.

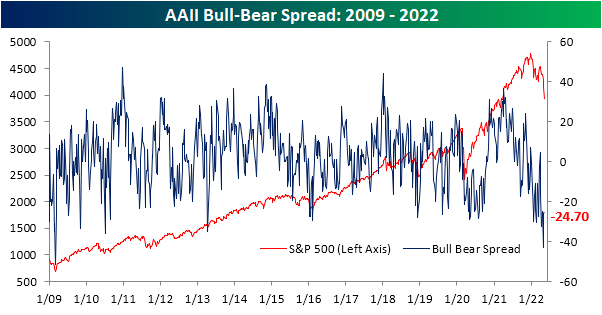

Given the moves, the bull-bear spread was higher for a second week in a row after it had reached the lowest level since March 2009 two weeks ago. Again, in spite of those improvements, the current level remains in the bottom 5% of all weeks on record.

The year is already a third over, and sentiment has found no respite after multiple months of declines in equity prices. In fact, bullish sentiment has not seen a single week with a reading above its historical average, and there has only been one such week for bearish sentiment. In the charts below, we show the average bullish and bearish sentiment reading by year since the start of the survey in 1987. While there’s still a lot of time left for things to change, with an average bullish sentiment reading of just 24.42% at this point in 2022, this year ranks as the worst year for bullish sentiment in the history of the survey (since 1987), although 1988 and 1990 have come close with average readings of around 27%. Meanwhile, the average reading on bearish sentiment has been 44.3% this year. 2008 is the only other year with a higher average reading at 45%. In other words, it is hard to find a comparable year since the late 1980s where optimism has been this low and pessimism this high. Click here to learn more about Bespoke’s premium stock market research service.

The Bespoke 50 Growth Stocks — 5/12/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Continuing Claims Reach More Multi-Decade Lows

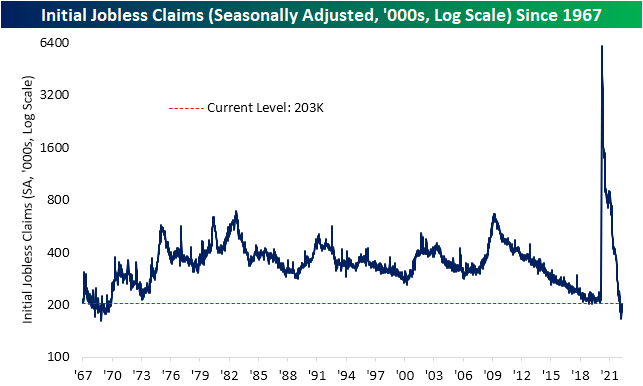

Initial jobless claims came in weaker than expected this week rising to 203K instead of the expected decline to 193K. Additionally, last week’s print was revised up to 202K. While that brings claims back above the 200K level for the first time since February, the current level remains historically impressive.

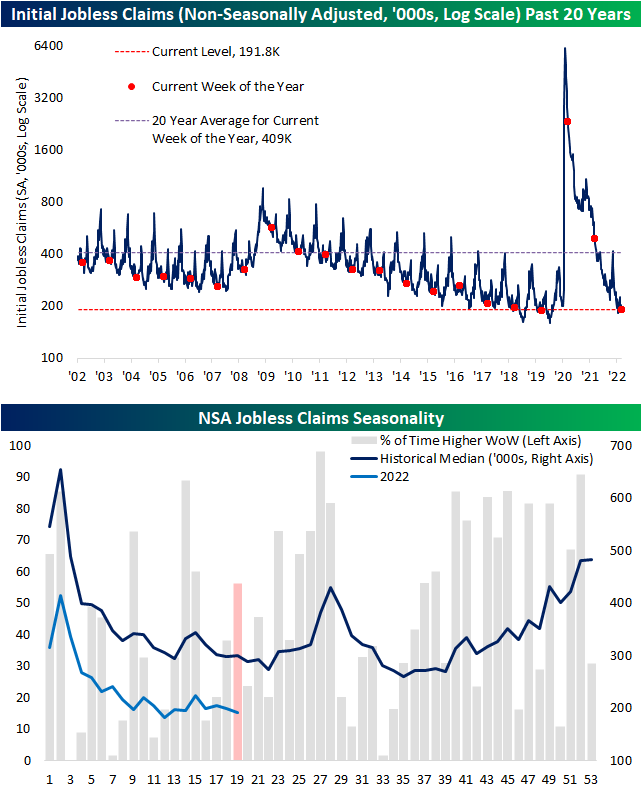

On a non-seasonally adjusted basis, claims still have seasonal tailwinds at their back, though, the winds will shift in the next few weeks. On an unadjusted basis, claims are still below 200K, dropping another 6.6K w/w to 191.8K. Behind the 182.3K reading from late March, that is the strongest reading on initial claims since 2019 and is in line with the readings for the comparable week of the year in the few years prior to the pandemic.

Unlike initial claims, continuing claims have continued to head lower unabated. Claims fell to 1.343 million in the most recent week marking the fifth consecutive weekly decline. Claims have not been at such a low level since late 1969/the first weeks of 1970. Click here to learn more about Bespoke’s premium stock market research service.

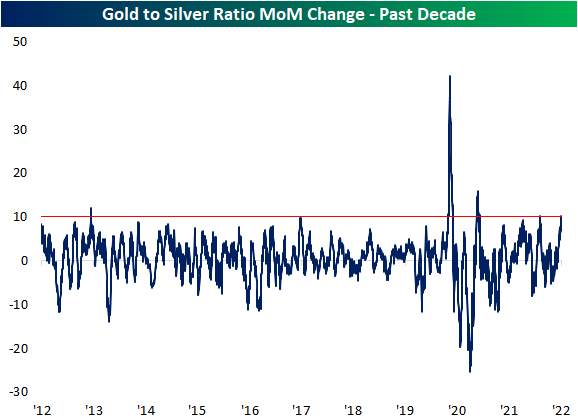

Precious Metals Harden Up

Little has been safe from heavy selling pressures recently including assets normally considered “safe havens” like precious metals. Gold is currently down over 9% from its March high while silver is down roughly 20% since its spring high. Today, both metals are bouncing from notable levels. For gold, it is finding support at its 200-DMA which also coincides with the rough uptrend line of higher lows of the past year. In addition to dramatic underperformance versus gold, silver’s test of support is perhaps a bit shakier. It is well below its moving averages, but today’s rebound is happening right around the lows from September and December. Granted, on an intraday basis, both yesterday and today’s lows breached those levels.

Given silver’s much larger decline, the ratio of gold to silver has ripped higher in the past month. In fact, the ratio has risen over 10% in the past month. The most recent 10% or larger surges were as recent as this past December with two even larger ones in the spring and fall of 2020. Prior to the pandemic, though, these sorts of rapid increases in the gold to silver ratio have been rarer. Before 2020, the only other instances of the past decade were in the springs of 2013 and 2017. Click here to learn more about Bespoke’s premium stock market research service.

Over 40% of S&P 500 Stocks Below Pre-COVID Highs

The world changed dramatically with the onslaught of the COVID pandemic in early 2020. Businesses were forced to digitize, consumers saved at historic rates, the Federal Government and Federal Reserve flooded the economy with cash, new hobbies were picked up faster than a dropped hundred dollar bill, and consumers emerged from the lockdowns financially stronger than ever. Long story short, COVID appeared to permanently alter the ways in which consumers and businesses interact, and companies that stood to benefit from the new way of life saw their stocks surge while the old-economy stalwarts were crushed. That was then.

This is now. As the economy has emerged from COVID, the cost of inputs has skyrocketed, real buying power has diminished, supply chains have become strained, and geopolitical tensions are hot. Not only that, but whereas the rate of fiscal and monetary stimulus was stronger than ever during the pandemic, the headwind from their removal is as intense as it gets.

Given the shifts, a number of stocks that originally surged in the COVID world have been hit hard in the post-Covid environment, and some of the biggest COVID losers during the lockdowns have turned into market leaders. As things currently stand, 40.6% of S&P 500 members are below their pre-COVID highs (closing high price from the start of 2019 through the end of February 2020), even as the index is up 18.0% from its pre-COVID closing high on 2/19/20. Besides the fact that four out of every ten S&P 500 stocks are below their pre-COVID highs, 8.1% of the index members are within 5% of their pre-COVID high and another 7.1% are within 10% of their pre-COVID highs.

At the sector level, three sectors – Communication Services, Real Estate, and Utilities- have more than half of their components trading below their pre-COVID highs. In addition to those three sectors, in both the Consumer Discretionary and Financials sectors, more than 40% of components are below their pre-COVID highs, and another 10% of each sector’s components are within 10% of those former highs. At the other end of the spectrum, the original ‘losers’ from COVID like Energy and Materials have fewer than a quarter of their components trading below their pre-COVID highs. While it seems some days like COVID will never go away, the rallies that a large number of stocks experienced are now nothing more than memories. Click here to view Bespoke’s premium membership options.

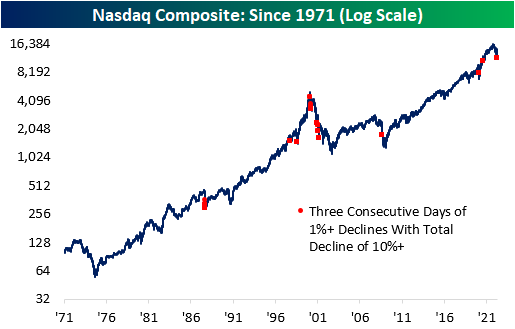

The Nasdaq’s Three Day 10% Drop

As of yesterday’s close, the Nasdaq declined more than 10% in the span of just three trading days. Selling pressure has been consistent as well as the Nasdaq notched declines of more than 1% on each of the three trading days. The last time the Nasdaq dropped 10%+ in the three days span with all three days experiencing drops of at least 1% was back in September 2020. Since the Nasdaq Composite started in 1971, there have only been eighteen other occurrences, and nine of those occurred during the bursting of the dot-com bubble.

Performance following these prior occurrences has not been very consistent. In the table below, we list each of the 9 occurrences in the chart below that took place without another occurrence in the prior month. One day and one week later, the Nasdaq’s median gain is better than the average and median returns for all periods since 1971. Moving further out though, median performance over the following one and three months has been weaker and less consistent to the upside than the average returns for all one and three-month periods. As has been the case with a lot of analyses lately, while short-term returns have been mixed, the one constant has been volatility. Click here to view Bespoke’s premium membership options.

Small Business Problems

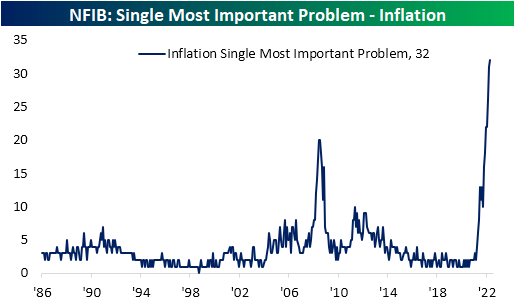

As we noted in an earlier post, inflation appears to be a major driver as to why small businesses are reporting historic pessimism for the US economy. Looking across the most important problems reported by small businesses in the NFIB’s monthly survey, inflation takes the cake as the biggest concern. Nearly a third of responding firms reported higher prices as their biggest problem; the highest level on record in data going back to 1986. That has now surpassed the prior series high of 20% in mid-2008.

Given inflation has stolen such a large share of small business worries, several other problems are now at or near record lows. For example, no firms reported competition from big businesses as the biggest issue. Government requirements and red tape are similarly at a record low after a one percentage point decline month over month. Taxes, poor sales, and financial and interest rates are also not a huge concern according to the survey.

With both government-related concerns dropping yet again, the combined reading between the percentage of respondents reporting taxes and government red tape as their biggest issues hit a new record low of 22%. The past few Presidential administrations have seen this reading more elevated and rising with Democrat presidents while Republican Presidents have coincided with lower readings. The current administration is now an exception with big declines as inflation concerns have come front and center.

The rise of inflation concerns have also resulted in a pullback in the share of respondents reporting cost or quality of labor as the biggest issue. While the combined reading rose one point in April thanks to the quality of labor, the combined reading is well off the peak of 40% from last September. Additionally, for the second month in a row and for the first time in roughly a decade, inflation continues to be the bigger concern. Click here to learn more about Bespoke’s premium stock market research service.

Inflation Slamming Small Business

Sentiment on the part of small businesses held firm in April instead of the further decline that was expected. The headline index came in unchanged at 93.2 versus estimates of a 0.3 point decline to 92.9. That remains some of the lowest readings since the early days of the pandemic.

Under the hood of this month’s report, individual categories were mixed. Like the optimism index, there were four categories that went unchanged month over month while another four were higher. The rest declined with some of those drops resulting in historic lows. Along with other global macro releases, in today’s Morning Lineup we noted the broad weakness in labor market indicators in this month’s report. Businesses reported negative net hiring (unchanged from last month) as there are also still elevated plans to take on new talent but positions are historically hard to fill.

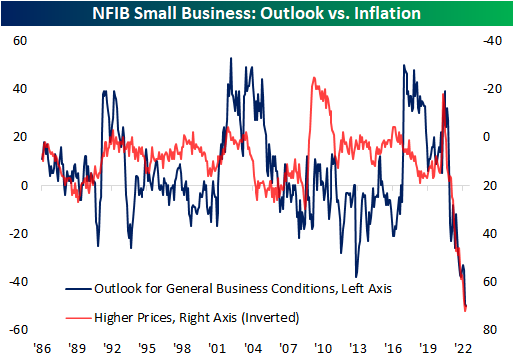

The most stand-out category is the outlook for general business conditions. This index points to record pessimism on behalf of small businesses. A net 50% of responding small businesses reported that they expect the economy to worsen versus improve in the next six months. Meanwhile, the percentage of respondents reporting now as a good time to expand dropped another 2 points and is in the bottom 1% of readings on record; only one point above the April 2020 low. Alongside those record/near record low readings, reported price increases pulled back slightly, though, the index remains at levels well above any precedence.

The NFIB also provided some more granular detail as to why businesses are reporting a lack of plans to expand. As we often note, the survey is often sensitive to politics and that is coming through here. 11% and 8% of responses blamed politics as the reason why now is either not a good time to expand or uncertain that now is a good time, respectively. With few respondents looking to expand on a net basis coinciding with a historic low for expectations for the economy to improve, of course, the dour economic outlook on the part of small businesses is the most widely reported reason to not expand. As shown below, 36% of responses blamed economic conditions as the reason they are not expanding and another 20% that reported uncertainty that now is a good time also blamed economic conditions. While insightful, “economic conditions” is a fairly vague term not providing much further insight into what exact economic conditions are holding businesses back (i.e. inflation or lack of labor).

That being said, we can extrapolate that inflation is likely the biggest reason. For starters, reported higher prices (inverted below) have surged during the pandemic right alongside the free fall in the outlook for general business conditions. Additionally, the percentage of respondents reporting inflation as their firms’ biggest problem hit another record high of 32% this month. Click here to learn more about Bespoke’s premium stock market research service.

Relative Strength in Dividend Stocks

In 2020 and most of 2021, dividend stocks underperformed the broader S&P 500 as investors put an emphasis on growth due largely to the low-rate environment. Since the Fed pivot to a tightening bias beginning in late 2021, though, there has been a sharp reversal in this trend.

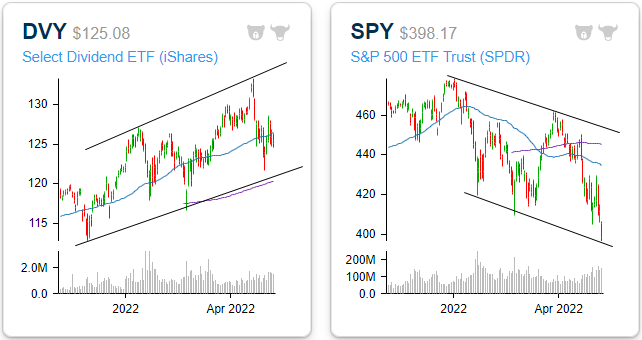

As it currently stands, the iShares Select Dividend ETF (DVY) has made up just about all of its pandemic-era underperformance versus the S&P 500 (SPY). Since the pre-pandemic highs, DVY has gained 16.9% versus a 17.9% advance for SPY, and that doesn’t even include the impact of dividends. After taking into account DVY’s higher yield (3.0 vs 1.6%), it is actually outperforming SPY during this span. Looking more closely at just 2021, DVY has outperformed SPY by 17.7 percentage points (+1.3% vs -16.3%) as investors have exited growth and into more value and income-oriented investments.

Whereas all of the major indices have entered downtrends, DVY is yet to break its uptrend. The ETF is trading well above its 200-DMA but slightly below the 50-DMA. Overall, the technical picture is relatively attractive, especially in comparison to the broader market. The following graphs are accessible through our Chart Scanner tool. Gain access to our proprietary tools by clicking here to view Bespoke’s premium membership options.

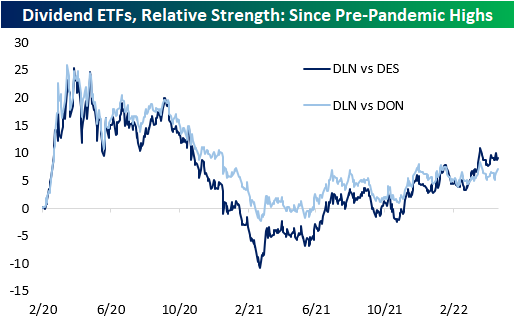

Within the high-dividend space, large caps have outperformed both mid and small caps. The WisdomTree US Large Cap Dividend ETF (DLN), the WisdomTree US Mid Cap Dividend ETF (DON), and the WisdomTree US Small Cap Dividend ETF (DES) were the funds used to compare performance across market caps. As you can see from the chart below, the larger companies that pay hefty dividends have outperformed mid-caps, and mid-caps have outperformed small caps. All three ETFs have similar yields, so the market cap discrepancies are likely more market-related.

While the average S&P 500 stock is down 11.8% on a year-to-date total return basis (median: -14.7%), the 25 highest dividend-paying stocks excluding energy (shown below) are down an average of 8.6% (median: -11.8%). Although this performance is not stellar, the average is still 320 basis points above that of the broader index. Given the recent surge in energy prices over the last year, a number of stocks in the Energy sector have seen their dividend payouts surge. Given the volatile nature of energy prices, the level of these yields may not be sustainable, so for that reason, we have left them out of this specific list.