Bespoke’s Morning Lineup – 2/9/23 – Claims Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I am a warrior, so that my son may be a merchant, so that his son may be a poet.” – John Quincy Adams

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After a weak showing yesterday, bulls are attempting to rebound this morning as S&P 500 futures are up over 0.50%, and the Nasdaq is priced to open up by 1%. It’s been an extremely quiet week for economic data, but we just got two reports this morning with initial and continuing jobless claims coming out at 8:30. Both reports came in slightly higher than expected with initial claims exceeding forecasts by 6K and continuing claims topping forecasts by 28K.

Not only are US futures rising this morning, but stocks in Europe have also been marching higher. In fact, Germany’s DAX is up over 1% and is actually trading at a 52-week high. Bear what?

Today’s 52-week high for the DAX broke a streak of 314 trading days that the index has gone without trading at a 52-week high. As shown in the chart below, the streak that just ended was hardly extreme as there have been nine other periods where the index went longer without a 52-week high, including an 883 trading day stretch that ended in September 2003.

The DAX may be trading at a 52-week high from the perspective of a German investor, but for US investors, there’s still some climbing out of the hole left to go. On a dollar-adjusted basis, the DAX remains just over 6% below its 52-week high. In order to reach a new high, the dollar-adjusted DAX can get there one of two ways. It can either rally from here, or it can merely trade sideways and as the 52-week window continues to drop higher prices from last February, the bar will get increasingly set lower.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

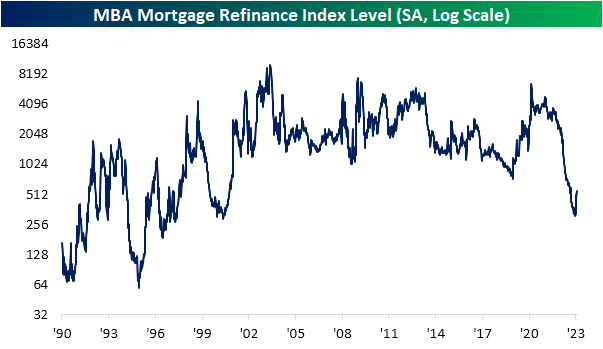

Refis Rise

Mortgage rates have come off of recent lows with the 30-year national average from Bankrate.com currently at 6.53%. While rates are not making new lows, those are much more attractive levels than last fall when they peaked well above 7%. On a rolling 3-month basis, the decline in mortgage rates continues to rank as some of the largest since the late 1990s (after the largest increase since the 1990s).

Given the alleviation on the rates front, purchase applications have been rebounding. The Mortgage Bankers Association’s weekly purchase application index is currently 19.2% above the post-pandemic low put in place in the first week of the year.

When rates were rising rapidly, massively stifling demand last year, refinance applications had taken a much larger hit than purchase applications. At the worst levels during the holidays, refinance applications reached the lowest level since May 2000. Since the start of the year, though, refinance applications have surged. Although there is still plenty of lost ground still to make up as applications continue to run below the past two decades’ range, the 68% month-over-month increase in applications has been the largest jump since March 2020 when applications doubled. Of all weekly readings since 1990, the current one-month increase ranks in the top 5% of all month-over-month moves on record. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 2/8/23 – All Quiet

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have civilized my own subjects; I have conquered other nations; yet I have not been able to civilize or to conquer myself” – Peter the Great

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

They say that you should never short a dull market, but that’s what seems to be the case this morning as futures are trading modestly lower despite a very quiet macro backdrop both here and abroad. Earnings season remains in full swing and a number of stocks are seeing big moves, but none of them are impacting much more than their respective shares let alone the broader market.

It’s hard to call the day-to-day performance of the equity market this year anything but impressive. Despite last Friday’s strong employment report and a continued hawkish (although no longer hawkish with a capital H) rhetoric from FOMC officials, the S&P 500 has managed to keep its rally intact. Just yesterday, it closed right near its YTD high from last Thursday. At the index level, every major US index ETF is currently at ‘overbought’ levels (greater than one standard deviation above its 50-day moving average) and all of them are in the green YTD with all but one (Dow Jones-DIA) up at least 8%.

Where things stand this year is a far cry from a year ago. At this point last year, all but one index ETF (DIA) was trading at oversold levels, they were all down YTD, and all but one (DIA) was down over 5% YTD.

Comparing the performance of these index ETFs this year versus last year provides an even clearer picture of the complete reversal. Indices that were down the most last year at this point like the Nasdaq 100 and the Russell 2000 are among this year’s biggest winners. Meanwhile, indices that experienced the least ‘damage’ at this point in 2022, like the Dow, have lagged so far this year. Another example? Of the 14 index ETFs we track in our Trend Analyzer, the seven ETFs that were down less than 7% YTD in 2022 are the only ones up less than 10% YTD in 2023.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

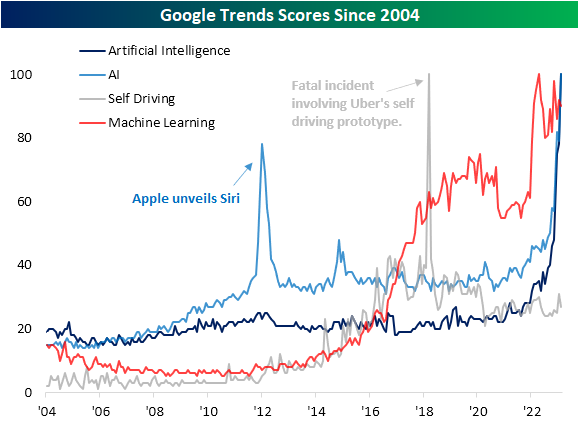

People All Over AI

In today’s Morning Lineup post, we compared Chat GPT’s rapid emergence into the mainstream to the rise of a number of other products. While Artificial Intelligence, or AI, has been a buzzword for some time now, this year it certainly has been in the spotlight more than in the past. Given the popularity of Chat GPT, some mega-caps like Alphabet (GOOGL) and Baidu (BIDU) have jumped in on the opportunity to announce their own versions. To quantify how in focus AI has become, below we show the Google Trends scores for a handful of related terms. Readings of 100 would indicate the peak in searches for a given topic globally.

Searches for “Artificial Intelligence” or its abbreviation have reached a new record while the field of “Machine Learning” has similarly seen searches rip higher and remain elevated in the past year. One interesting area which has not seen searches rise much is in regards to the automotive industry. Searches for “self-driving” have not picked up much within the range of the past few years. That is also well below the record from March 2018 when searches spiked due to a fatal incident involving Uber’s self-driving car. That being said, it is worth noting that even before the Chat GPT craze, these searches had been moving higher quite rapidly.

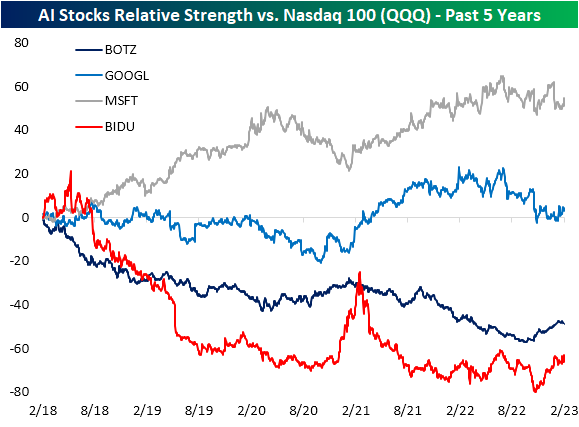

As we discussed earlier, although the broad topic of AI is in vogue, related stocks have not gotten much of a boost in reaction to this news. For those having made announcements regarding AI in recent days like Alphabet (GOOGL), Microsoft (MSFT), and Baidu (BIDU), relative strength versus tech more broadly (proxied by the Nasdaq 100 ETF (QQQ)) has not done anything too notable in terms of long term trends. For MSFT and GOOGL, relative strength has been sideways at best over the past year, and BIDU has been moving higher in recent months, but that follows a few rough years for the stock relative to US tech. The same can be said for a more encapsulating basket of AI-related stocks proxied by the Global X Robotics and Artificial Intelligence ETF (BOTZ). While the relative strength has been trending lower (meaning underperformance versus tech more broadly) the past few months have seen a rebound. Click here to learn more about Bespoke’s premium stock market research service.

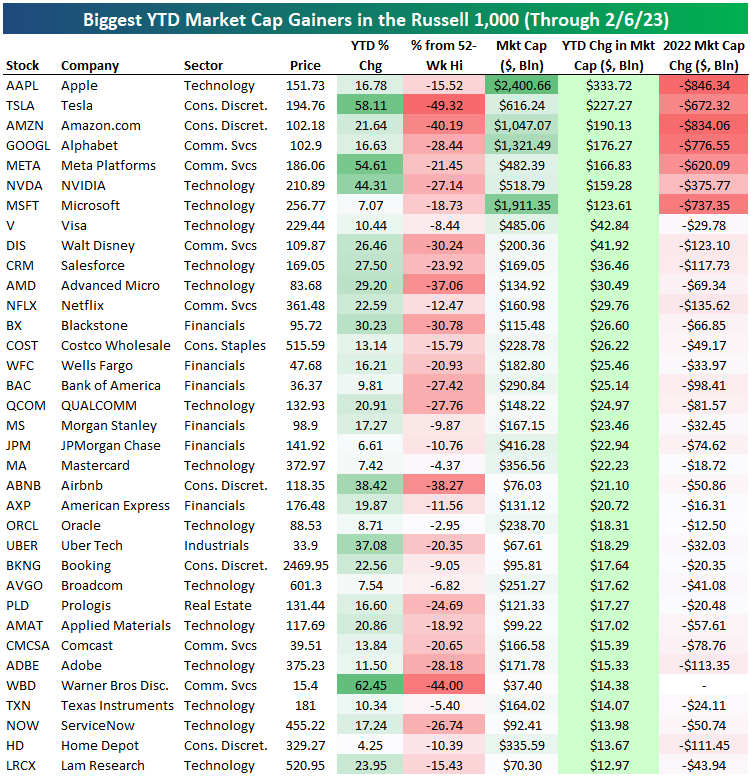

$2.9 Trillion in Market Cap Added

After seeing the total market cap for the Russell 1,000 fall by $10.9 trillion in 2022, we’ve seen a rebound of $2.9 trillion in market cap so far in 2023. Below is a look at the total change in market cap by sector across the Russell 1,000 so far in 2023 and for all of 2022. The Tech sector saw its market cap fall $4.35 trillion last year, and it has seen its market cap rise by $1.176 trillion to start 2023. Consumer Discretionary’s market cap has risen by $701 billion, followed by Communication Services at $516.9 billion and Financials at $373 billion.

Four sectors have actually seen their market caps fall this year. Health Care’s market cap has fallen the most at -$141 billion, while Energy has fallen $57 billion, Consumer Staples has declined $32.2 billion, and Utilities has fallen $29.9 billion.

Below is a look at the biggest gainers in market cap so far this year at the individual stock level. Seven stocks have already gained more than $100 billion in market cap this year. Apple (AAPL) has jumped the most at $333.7 billion, followed by Tesla (TSLA) at +$227 billion, Amazon (AMZN) at +$190 billion, Alphabet (GOOGL) at +$176 billion, and Meta (META) at +$166.8 billion.

While the seven biggest gainers to start 2023 have added a combined $1.377 trillion in market cap, they lost a combined $4.86 trillion in market cap in 2022. Click here to start a two-week trial to Bespoke Premium.

Bespoke’s Morning Lineup – 2/7/23 – The “Chat AI” Invasion

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“As long as we enjoy it, we’ll do it. ‘Cause we enjoyed it before we made any money.” – George Harrison, 2/7/1964

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Much like Chat GPT has rocked the way people gather and consume information, 59 years ago today, the music scene in the United States was changed forever as John, Paul, George, and Ringo touched down at Kennedy airport for the first time. The rest is history. When the Beatles appeared on the Ed Sullivan Show less than two weeks later, around 40% of the US population watched. Everywhere the band went they were swarmed by screaming (nearly all female teens) fans. For the imprint the Beatles made on both the music industry and pop culture, it’s hard to believe that within six years of first setting foot on US soil the band was no more. The Beatles’ candle may not have burned for long, but the movement they sparked still shines today.

A single event watched simultaneously on TV by 40% of the US population will never be duplicated again, but the stampede of Chat GPT into the mainstream is an event unrivaled by any other product in history. According to a study by UBS, Chat GPT reached 100 million monthly active users in the span of two months putting it years ahead of Google Translate (78 months), Uber (70 months), Spotify (55 months), and Instagram (30 months). Even TikTok took nine months to reach that milestone! Chat GPT is to consumer tech what the Beatles were to music. It will leave a permanent impact on society in terms of how people gather, produce, and consume information and who knows what else. The only question is whether it will be the AI tool we’re still talking about years from now, or will it burn out and allow others to fill the void? Just yesterday, Google launched its own AI technology called Bard to public testing, and according to Bloomberg, Baidu (BIDU) will launch its own service similar to Chat GPT by March.

These Chat tools may be the next big thing, but the stocks of the three companies launching them haven’t been particularly impressive. Shares of BIDU may be trading right near six-month highs, but the stock is still down over the last year and is trading for less than half of what it traded for at its peak in early 2021. Last week, it closed above its 200-day moving average for the first time in more than 200 trading days ending its second-longest streak of trading below that level in its history as a public company. Its time above the 200-DMA didn’t last long, though, as it closed back below that level the following day and is down over 15% in the last six months. Finally, Microsoft (MSFT) has the most direct exposure to OpenAI’s Chat GPT tool, but it too has been sucking wind. Like GOOGL, it only just recently traded above its 200-DMA and is still down more than 10% in the last six months.

Chat AI tools may be changing the world and there will be big winners, but the ones with the most immediate and direct exposure haven’t seen a big change in their fortunes. Maybe the fact that ‘everyone’ seems to be launching their own versions of these tools suggests that they don’t have a lot of scarcity value after all.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

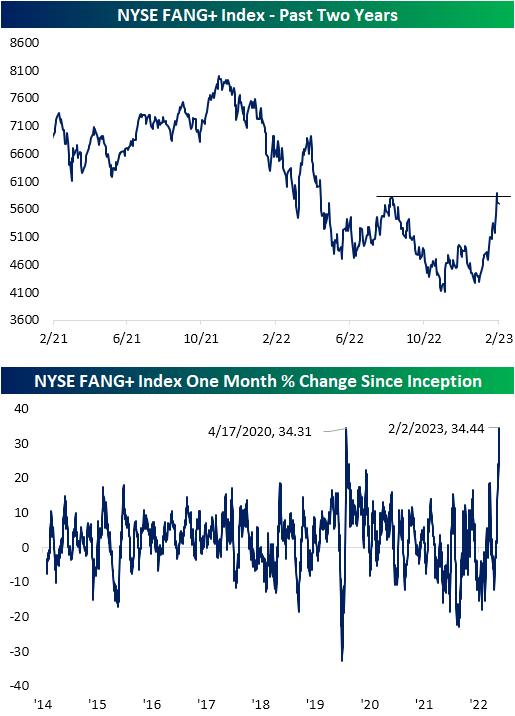

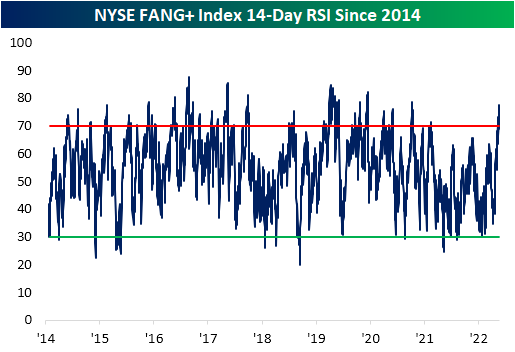

FANG Index Has Best One-Month Rally on Record

“Big Tech” stocks like Apple (AAPL), Amazon (AMZN), and Alphabet (GOOGL) have taken a breather over the past few days after reporting earnings last week. It’s important to note, however, just how much these stocks had rallied leading up to their near-term highs last week. Through last Thursday, the NYSE FANG+ had rallied 34.44% over the prior month. That was actually its biggest month-over-month rally in the index’s history dating back to 2014! As shown below, the index managed to make a “higher low” in early January just before it took off, and it just barely took out its highs from last August when it peaked last week before pulling back slightly.

While last week’s earnings results provided some negative fundamental catalysts (some of which we highlight in our most recent Conference Call Recaps), there is also the technical aspect that this group of stocks had gotten historically overbought. At last week’s highs, the 14-day RSI reached 77.4. Normally, any reading above 70 would be considered overbought. At 77.4, the RSI reading for the NYSE FANG+ index was the most elevated since June 2021 and ranked in the 97th percentile of all days since 2014. After further declines to start out this week, the RSI is still elevated, but back below 70. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 2/6/23 – Dispersion

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The greatest leader is not necessarily the one who does the greatest things. He is the one that gets the people to do the greatest things.” – Ronald Reagan

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

There’s very little data to speak of this morning, or for that matter, the entire week, so investors will have to focus primarily on earnings and Fed Chair Powell’s speech at noon tomorrow. Last week was the peak for earnings season in terms of the market cap of companies reporting, but in terms of quantity, it will be just as busy this week. Markets are starting off on a negative footing as US Treasury yields continue their climb following last Friday’s jobs report. After touching its 200-day moving average on Thursday at 3.29%, the 10-year yield is more than 30 bps higher this morning at 3.60%. Even after the volatility of the last year, that’s quite a big move in a short period of time. Crude oil and natural gas, meanwhile, are both trading up over 1%.

Last week’s market word of the week was dispersion. As shown in the snapshot from our Trend Analyzer, performance was all over the map with Communication Services leading the way higher with a gain of over 5% while Energy trailed falling nearly 6%. As a result of the moves, we finished off the week with two sectors at ‘extreme’ overbought levels (Communication Services and Technology) while Utilities, with its 1.4% decline, finished the week at ‘extreme’ oversold levels.

Energy and Utilities were the only two sectors down over 1% last week, and both of their price charts have been showing signs of deterioration. After stalling out at a lower high earlier this year, Energy stocks have been under pretty significant pressure as both crude oil and especially natural gas have been weak. If the declines continue this week, chart watchers will be focusing on support at the lows from late 2022 which also corresponds to highs from late in the Summer. The picture for Utilities has been even weaker. That sector is now in a well-defined downtrend and last week’s decline resulted in a potential breakdown below support.

It seems strange to say after a year like 2022 but a number of sectors have also been breaking out to six-month highs. Last week, Financials, Industrials, and Materials all managed to trade above multi-month resistance levels and trade to six-month highs.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 2/5/23

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Going Green

CTR reports on improved lithium extraction from brine (The Desert Review)

A new process for extracting lithium from the water inside geothermal power plant loops is starting to scale up in California’s Salton Sea. [Link]

Cities Would Literally Be Much Cooler With More Trees by Lara Williams (Bloomberg)

Sometimes big problems have remarkably simple solutions. For cities, high temperatures, pollution, and health crises could all be improved by planting a lot more trees. [Link; soft paywall]

Dysportsia

Get Used to Face Recognition in Stadiums by Khari Johnson (Wired)

The dystopian use of facial recognition systems at Madison Square Garden is only the tip of the iceberg as sports venues work to contain fans who get out of hand…and some they just don’t like. [Link]

Sports Illustrated Publisher Taps AI to Generate Articles, Story Ideas by Alexandra Bruell (WSJ)

Arena Group, which publishes a range of finance, sports, and general interest sites, is integrating AI to produce content using AI, sometimes by using inventories of content from the group’s previous articles. [Link; paywall]

ChatGPT

OpenAI launches ChatGPT Plus, a paid version of the popular AI chat by Christianna Silva (Mashable)

For $20 per month, paid users get more reliable uptime and faster access to the popular AI chatbot protocol which has spread widely across the internet in the last few months. [Link]

Are You Smarter Than ChatGPT? OpenAI Tool Aims to Detect AI-Generated Text by Michael Kan (PC Mag)

Amidst concerns that AI-generated text is being misused (especially by students), ChatGPT’s creators at OpenAI have created a tool that claims to be able to detect whether a piece of text was AI-generated or human in origin. [Link]

Chow

Wings and Guacamole Are Cheaper, Just in Time for Your Super Bowl Party by Kevin Simauchi (Yahoo!/Bloomberg)

After a huge surge alongside other commodities over the past couple of years, prices for chicken and avocados are collapsing just in time for the Super Bowl. [Link]

Wave of ‘sushi terrorism’ grips Japan’s restaurant world by Justin McCurry (The Guardian)

Conveyor belt sushi restaurants have become the focus of an unfortunate social media trend which has sent their stocks plunging as a breakdown in basic social decorum threatens to remake the industry in Japan. [Link]

Raising Chickens for Cheaper Eggs Gets Expensive Fast by Rachel Wolfe (WSJ)

If you’re trying to skip the high egg prices at the grocery store by raising your own chickens, watch out: you might be signing up for more than you bargained for. [Link; paywall]

Pandemic

Merck Covid Drug Linked to New Virus Mutations, Study Says by John Lauerman (Bloomberg)

A study has found that a Merck treatment for COVID-19 creates more mutations of the virus, which works by altering the virus’s genome to reduce replication. [Link; soft paywall]

US Offices Reach 50% Occupancy for First Time Since Pandemic Hit by Matthew Boyle (BNN Bloomberg)

For the first time since the pandemic hit, building occupancies across 10 major metro areas moved above 50%, marking a major milestone in the return to normal that has been slowly and steadily emerging. [Link]

Adani

The Adani affair: the fallout for Modi’s India by John Reed and Benjamin Parkin (FT)

A look at the macroeconomic and political milieu that surrounds Gautam Adani and his company in the wake of a catastrophic decline in shares following short seller allegations of stock manipulation and accounting fraud. [Link; paywall]

Balloon

US Downs Alleged Chinese Spy Balloon That Lingered for Days by Christian Hall and Riley Griffin (Bloomberg)

After a Chinese weather balloon (or, depending on who you’re listening too, spy platform) spent a week above the US, an American fighter jet shot it down over the South Carolina coast on Saturday. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 2/3/23

This week’s Bespoke Report newsletter is now available for members. (Log in here if you’re already a subscriber.)

In a blockbuster week for labor market data, the FOMC slowed the pace of rate hikes further but kept trying to talk tough about the outlook for rates. Equity, foreign exchange, and credit markets had different ideas both in the US and around the world. We dive deep into quarterly data on wages and productivity, monthly jobs numbers from the blockbuster Employment Situation Report today, PMI data from around the world economy, and other tidbits from the data this week. Earnings are also underway, and we provide qualitative and quantitative highlights from earnings results on both sides of the Atlantic this week.

View this week’s Bespoke Report newsletter by starting a one-month trial, or click the image below to view our membership options page.