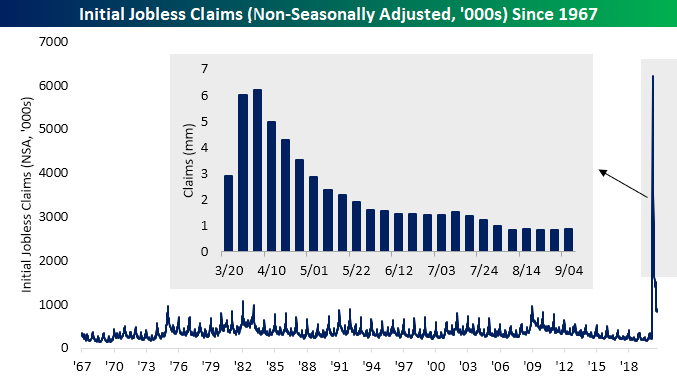

Jobless Claims Flat

Things were actually pretty calm this week for jobless claims. For the first time since August of last year, initial jobless claims were unchanged this week relative to last week’s 3K upwardly revised number of 884K. That was above forecasts of a reading 34K lower at 850K. With the caveat that comparisons of the past two weeks to prior readings are not exactly like for like on account of a change to the seasonal adjustment methodology (which we discussed in greater detail last week), that 884K reading is still a very high level of claims relative to history but is at the low end of readings since the pandemic began.

Non-seasonally adjusted claims were higher this week by 20.1K coming in at 857.1K. That is the second consecutive week with higher claims by this measure and which leaves claims at their highest level since August 20th. Granted, that is still at the low end of the range since the pandemic began.

Continuing claims (seasonally adjusted) saw similar results with a slightly higher reading of 13.385 million compared to 13.292 million last week. As with seasonally adjusted initial claims, the caveat with comparisons of pre-September readings still applies, but this was the first time seasonally adjusted continuing claims rose in five weeks.

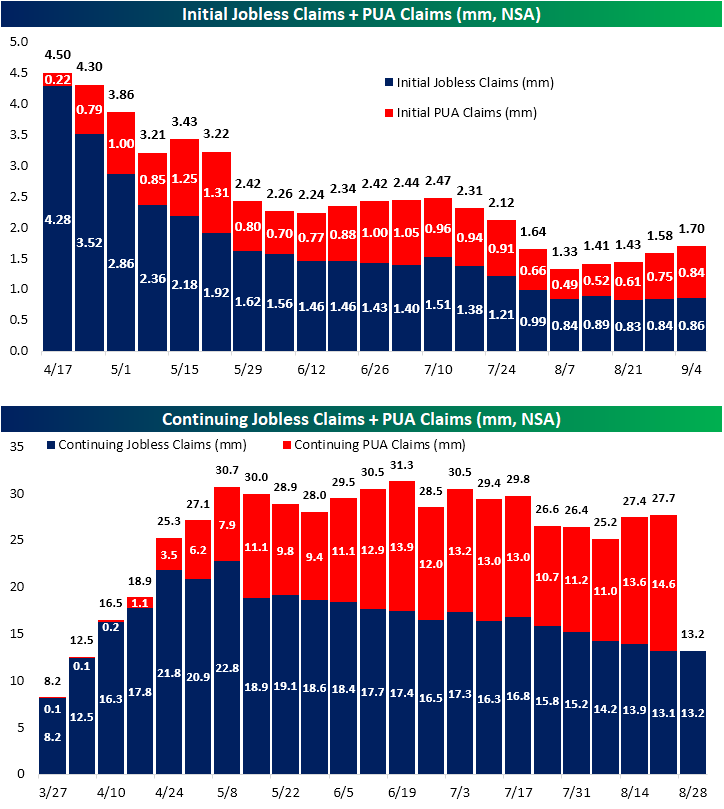

Taking into account Pandemic Unemployment Assistance (PUA), total initial claims have continued to worsen with the total count now at 1.7 million; up from 1.58 million last week and the highest since July 24th. The bulk of that increase comes from PUA claims which were up to 0.84 million from 0.75 million last week. This week marked a fourth consecutive week that both PUA claims and the total (PUA plus regular) claims have risen week over week. Continuing PUA claims for the week of August 21st which are lagged an additional week to regular continuing claims also rose with the most recent reading of 14.6 million marking a pandemic high. Even though regular claims are off their peak and have been trending lower, that leaves total continuing claims at the highest level since mid-July.

One interesting point of this data is that this weakness comes at a time of year in which claims have tended to turn around and head higher. As shown below, on a non-seasonally adjusted basis, this time of year on average has marked the annual bottom for NSA claims with the bottom for continuing claims typically coming a bit later before both rise into the end of the year. In other words, it is hard to say to what degree it is the case, but the recent uptick in both initial and continuing claims (especially taking into account PUA claims) could at least partially be a result of seasonality. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Material Moves

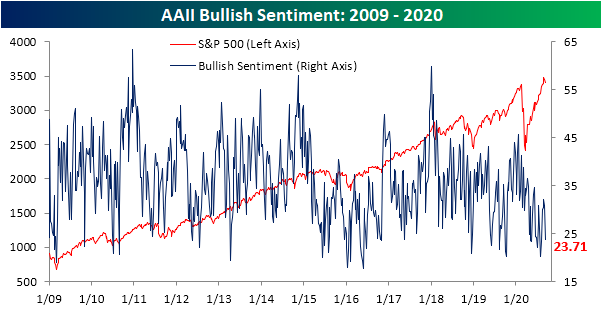

Correction Crushing Sentiment

With the Nasdaq entering a correction in under a week and the S&P 500 dropping just over 7% from last Wednesday’s closing high to Tuesday’s low, investor sentiment has understandably taken a hit. After a four-week stint in which the percentage of investors reporting as bullish in the American Association of Individual Investors (AAII) survey stayed above 30%, this week less than a quarter of respondents are bullish. At 23.71%, bullish sentiment is at its weakest level since the first week of August when it was 23.29%. Additionally, the 7.09 percentage point decline was the largest one week drop in bullish sentiment since mid-June when it fell 9.91 percentage points.

The decline in optimism was obviously met with a similar-sized increase in pessimism. The percentage of investors reporting as bearish rose 6.68 percentage points this week to 48.45%. That is the highest reading since the last week of July when bearish sentiment stood slightly higher at 48.47%. It was also the largest one week gain to bearish sentiment since June 18th. As shown in the chart below, that is at the high end of the past few months’ range but is still off the highest readings of the pandemic when more than half of respondents reported as bearish.

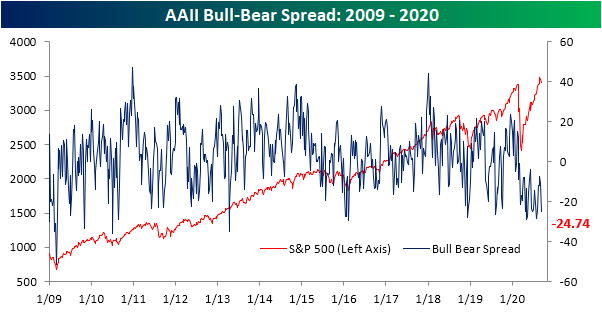

With the big moves in bullish and bearish sentiment, the bull-bear spread moved deeper into negative territory (which it has been in for a record 29 weeks now) falling from -10.97 to -24.74 this week. That brings the spread back to similar levels to the end of July. Since the pandemic began, there have only been five other weeks that the spread has been lower: the last week of July, June 25th, May 7th and 14th, and April 23rd. In other words, bearish sentiment continues to dominate.

Meanwhile, over a quarter of respondents are neutral on the market. 27.84% of respondents to the AAII survey reported as expecting no change in the S&P 500 over the next six months which was little changed from 27.43% last week and is basically right in line with the average of 25.77% since the bear market low in March. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 9/10/20 – Heads or Tails?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Seek advice on risk from the wealthy who still take risks, not friends who dare nothing more than a football bet.” – J. Paul Getty

It’s that time of year again as the NFL is set to kick off its season this evening as it typically does every year on the first Thursday after Labor Day. The season will go off as usual with a full season, playoffs, and the Super Bowl LV on February 7, 2021. Why are we even talking about this? Because after six months of abbreviated seasons and canceled events in the world of sports, the return to a normal season for a major league is a step in the right direction. Some degree of normality in just a small part of their lives is what just about everyone could use right now. The Chiefs even plan to allow fans to the stadium for tonight’s game against the Texans. While ticket sales were capped at 16,000, for some teams these days, that’s a perfectly normal crowd.

In economic data this morning, jobless claims were higher than expected on both an initial and continuing basis, while revisions to last week’s report were minimal. On the inflation front, PPI came in slightly higher than expected. Futures were modestly lower on the S&P 500 and higher for the Nasdaq heading into the release and basically remained there after the report as well.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, trends related to the COVID-19 outbreak, and much more.

Where the market goes from here in the short-term is basically a coin-flip, and the S&P 500 intraday chart from the last week has something for both the bulls and bears. On the bullish side, yesterday’s open broke what was starting to look like a downtrend from the high on 9/2. As the market rallied throughout the day yesterday, though, it ran out of steam right at Friday’s close. So until that level from Friday can be broken to the upside, the bears are on top.

Daily Sector Snapshot — 9/9/20

JOLTS Show Some Return To Normalcy

Today’s Job Openings and Labor Turnover Survey (JOLTS) report from the Bureau of Labor Statistics (BLS) on the flows in and out of jobs as well as the number of job openings was pretty encouraging. As shown in the first pair of charts below, the number of open jobs as a percentage of the labor force has surged back to pre-pandemic levels and is close to the very strong levels seen at the prior peak. This is a good sign that labor demand is holding up pretty well in aggregate.

Also encouraging is that while not at extreme lows, layoff and discharge rates are back to the levels they sat at in 2019. Instead of settling at a new higher level, the 1.4% private sector layoff and discharge rate is at the same level it was at numerous times during 2019 and the first two months of 2020. Hiring, which crashed and then surged as businesses started to reopen, was 4.1% the labor force in July. That was a stronger pace than any month in the history of the last expansion.

Finally, we think quit rates are about the best indicator of labor bargaining power available. As shown, they are bouncing and bouncing hard. They have not fully recovered from COVID’s hit, but the size and speed of the bounce is consistent with a very strong trajectory for labor markets relative to what other indicators (for instance, permanent job losses in the Employment Situation Report, or the level of unemployment claims) are saying. We will have more granular analysis of the JOLTS report tonight in The Closer. Click here to start a free trial and receive The Closer tonight with more analysis on the JOLTS report for July.

B.I.G. Tips — The Market? Or a Market of Stocks?

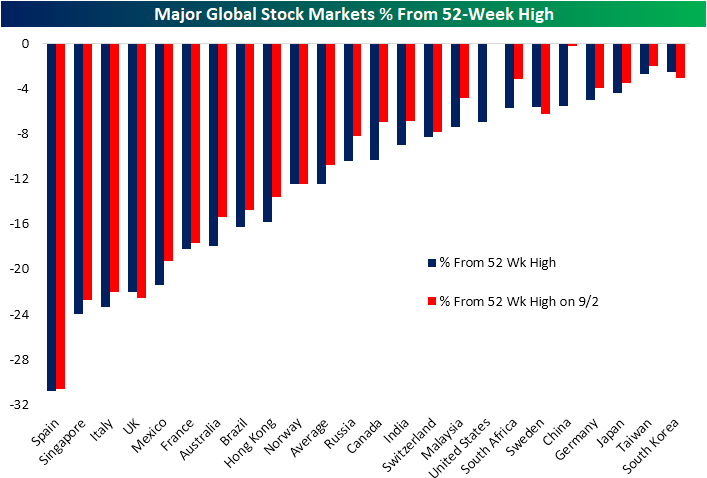

Pullback Seen Around the World

Through yesterday’s close, the S&P 500 has fallen just under 7% from its high on September 2nd. Compared to other major global stock markets that we track in our Global Macro Dashboard, only China has also fallen over 5% in the past week. The average global stock market of these 23 markets is down 1.8% since 9/2. Only three—South Korea, Sweden, and the UK—have risen in the past week. In other words, stocks have dropped around the globe but the US and China’s declines have far outpaced the rest of the world.

One interesting point of the past week is these declines have only brought US stocks off of their 52-week highs. As of last Wednesday, whereas US equities were at a record high, the average global stock market was over 10% below its 52-week high. As shown below, other than the US, the only other country that was within 1% of a 52 week high last week was China; the second-largest decliner in the past week. After those large declines in the past week, the US and China stand out far less than they did last week in terms of distance from 52 week highs.

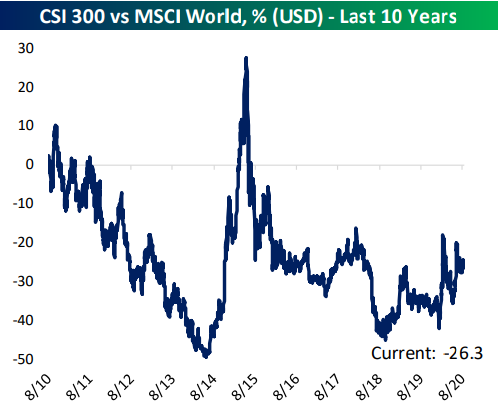

That dynamic of the US outpacing its global peers is nothing new though. As shown in the chart from our Global Macro Dashboard below, the US has consistently outperformed the rest of the world over the past ten years (a rising line indicates outperformance and vice versa). While its relative strength has been more mixed over the past ten years, China has similarly seen its equities outperforming recently. Click here to view Bespoke’s premium membership options for our best research available.

Housing Still Hot Headed Out of Summer

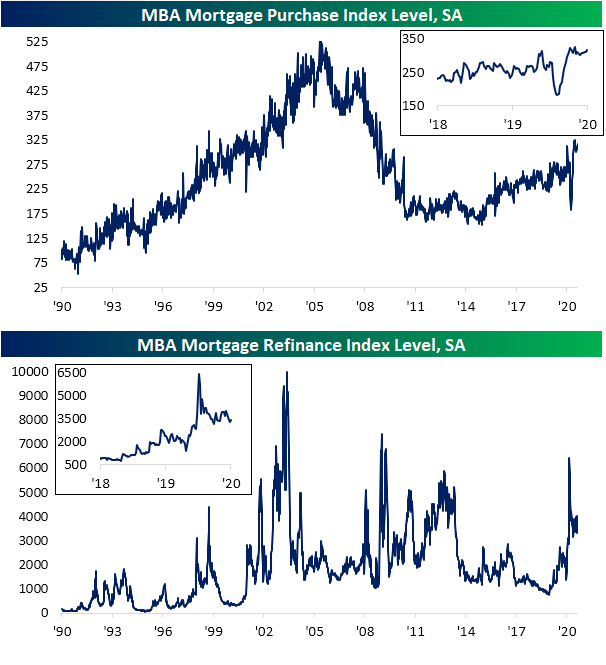

This morning, the Mortgage Bankers Association (MBA) released this week’s reading on mortgage applications. Seasonally adjusted purchases were up 2.6% from last week, rising to the highest level since the first week of July. In the past few months as housing activity has surged, other than that July reading, there was only one other time that purchases were stronger, and that was in the second week of June. In other words, purchase activity is once again on the rise after taking a bit of a breather in the summer months and is currently back to some of its strongest levels since early 2009. With rates staying low, refi activity similarly remains around some of its stronger levels of the past decade gaining nearly 3% this week. Granted, that is still in the range that the index for refinances has been in since the spring.

As shown in the charts below, on a non-seasonally adjusted basis, purchase applications continue to run well above trend. Even with the big decline that went against seasonal norms in the spring (first chart below), the index of YTD purchase applications has averaged 290.1 each week compared to 272.4 last year (second chart below); these are by far the strongest readings of the past decade. For every week since the mid-June 2020 peak (which was later in the year than usual due to pent up demand; denoted by the blue dot in the first chart below), purchase applications have been consistent with seasonal trends, but each week’s reading has been higher year over year by an average of over 24%. This week, thanks to the timing of the Labor Day holiday, the NSA purchase index rose by an even stronger 40% YoY which was by far the strongest reading of any week of this year.

Another housing indicator showing similarly strong demand that we touched on in last night’s Closer was the July version of Black Knight’s monthly Mortgage Monitor. Although it is at a greater lag than MBA’s readings, this was yet another data point pointing to strong housing demand as new originations in June (lagged an extra month to the rest of the report that covered the month of July) surged to over 1.3 million which was the highest reading since at least 2013; doubling year over year. The July Mortgage Monitor also indicated that delinquencies as a percentage of all loans have continued to improve, falling to 6.9% compared to its recent peak of 7.76% back in May. Albeit improved, the delinquency rate is still elevated at its highest levels since early 2013/late 2012. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke CNBC Appearance (9/9)

Bespoke co-founder Paul Hickey appeared on CNBC’s Squawk Box this morning to discuss the outlook for large-cap tech stocks and the broader market. To view the segment, please click on the image below. Click here to view Bespoke’s premium membership options for the best market analysis available.