Prices and Employment Surging in Philadelphia

While the results were not as impressive as the Empire Fed report earlier this week, this morning’s reading on the manufacturing sector from the neighboring Philly Fed did beat expectations. The headline number fell to 23.1 rather than the anticipated decline to 20. While it indicates some deceleration in the rate of growth, activity remains at the high end of the past several months’ readings indicating solid growth, In terms of expectations, though they remain positive, they took an even bigger hit with the index falling from 52.8 down to 39.5. That month-over-month decline stands in the bottom decile of monthly moves.

The decline in the headline number can be credited to broad declines in multiple categories. The only indices to move higher were those concerning employment as well as the indices for Inventories and Prices Paid. As for the indices for future expectations, the declines were even broader with only expectations of Prices Paid and Received moving higher.

Indices concerning demand were all consistent with a deceleration in February with the biggest declines coming from Unfilled Orders and Delivery Times. After record and near-record readings last month, the declines in the Unfilled Orders and Delivery Times indices stood in the bottom 6.8% and 1.7% of all monthly moves, respectively. Even after those declines, Unfilled Orders is still in the top 6% of all readings, and Delivery Times is still in the top 2% of all readings. In addition to the decline in the Delivery Times index, the corresponding index for expectations fell to a negative reading this month for the first time since Dember of 2019. In other words, manufacturers are still reporting historically long lead times, but they do foresee improvements on the horizon.

Inventories saw a big move higher in February. That index rose 7.4 points to a reading of 20, which is the seventh strongest reading on record. As for expectations, the Inventories index was one of the standout elevated readings. Whereas most indices for expectations are in the middle of their historical ranges, the Inventories index is in the 84th percentile.

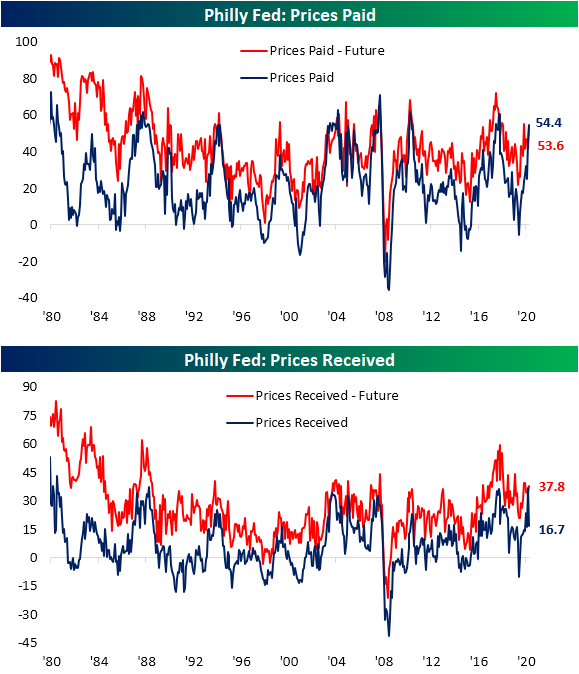

While the report showed prices continued to rise, there was a divergence between prices for final goods and inputs. Prices Paid have continued to accelerate with the index rising to 54.4 which is the highest reading since August of 2018. Conversely, Prices Received slammed on the brakes. The index collapsed from 36.6 last month to 16.7. While that is still above December’s levels, it was the sixth-largest MoM decline on record and the biggest decline since December of 2008.

Perhaps the strongest area of the report concerned labor. The index for Number of Employees rose once again reaching 25.3. That is the seventh-highest reading of all months since the survey data begins in 1968 and is the highest level for the index since July of 2019. Not only are the region’s businesses taking on more employees, but the average workweek has also risen at a historic rate. The index for Average Workweek gained 12 points in February to 30.6. There has only been one higher reading in the history of the data and that was a reading of 34.2 in May of 2018. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Small Changes in Sentiment

Even though the S&P 500 has essentially traded sideways over the past week, sentiment saw a slight improvement. AAII’s weekly survey of individual investors found 47.1% of respondents reported as bullish. That is up slightly from 45.5% last week and the highest level of bullish sentiment since the week of December 10th.

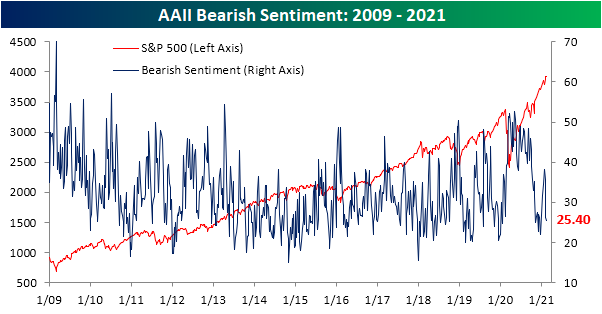

At the same time, bearish sentiment has continued to decline. Coming in at 25.4%, bearish sentiment has now declined for three straight weeks falling 12.9 percentage points in that span. That is the largest decline in a three-week span since October of 2019 when bearish sentiment fell 15.53 percentage points and leaves bearish sentiment at the lowest level since the week of December 24th when less than a quarter of respondents reported as bearish.

This week’s moves in sentiment resulted in the bull-bear spread rising for a third week in a row. With a spread of 21.7 percentage points, sentiment favors bulls by the widest margin since the first week of December.

Like bearish sentiment, neutral sentiment took a small move lower dropping 0.7 percentage points to 27.6%. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: Yeti (YETI) Yowling

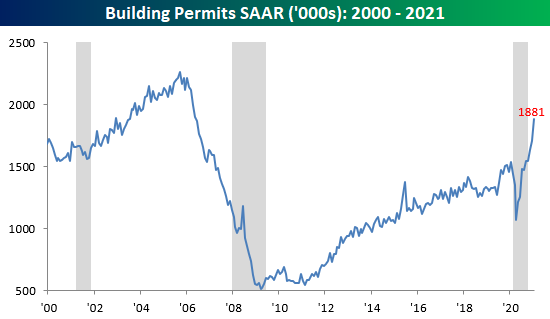

Starts Stuck, Permits Parabolic

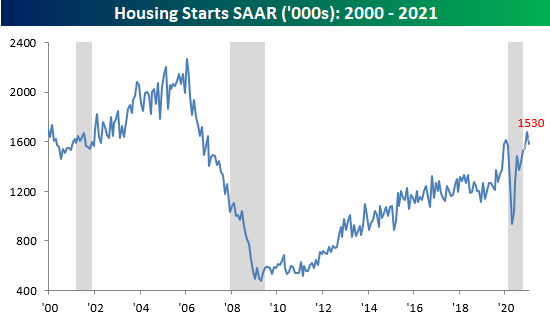

The January report on Housing Starts and Building Permits was mixed relative to expectations, but the overall backdrop remains very strong. Starting with Housing Starts, they posted a decline of 6.0% m/m falling to 1.58 mln versus expectations for a much smaller decline, but keep in mind that it comes after a 10+ year high in December.

Building Permits, which are less impacted by the weather, were much stronger in January. They surged to 1.881 million versus 1.704 mln in December and expectations for a much more modest level of 1.694 mln. Following January’s increase, Permits are now less than 17% from their bubble high in 2005.

Looking at the chart above, Permits have practically turned parabolic in the last few months. While it’s somewhat arbitrary to look at a nine-month rate of change, the fact that Permits have just experienced their second-largest increase in that span is worth highlighting. What’s also worth pointing out, too, is that while Permits are rebounding from a nine-month decline of just over 20%, the two prior spikes highlighted in the chart came following much larger declines.

In terms of the breakdown of this month’s report, the fact that multi-family starts and permits were key drivers of strength is a bit of a drawback. Single family-starts actually dropped more than 12% m/m while permits were up less than 4%. Multi-family units, meanwhile, were up over 15% for both starts and permits. On a regional basis, every region of the country saw declines in starts relative to December, while the Northeast was just barely higher. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Ohio Drives Claims Nationally

Jobless claims disappointed this week as both initial and continuing claims came in above expectations. In addition to an upward revision of 55K to 848K last week, initial jobless claims were higher at 861K this week. That brought claims to the highest level since the week of January 15th when they were 14K higher at 875K. This week also marked the third week in a row without an improvement in jobless claims.

Although the seasonally adjusted number was higher, on an unadjusted basis claims were a bit better. Only 862.4K claims were filed this week compared to 868.1K the prior week. We would note that seasonality is very much on the side of claims for the current week of the year though. In the history of the data going back to 1967, there has only been one year, 1978, that the seventh week of the year has seen the unadjusted number move higher week over week.

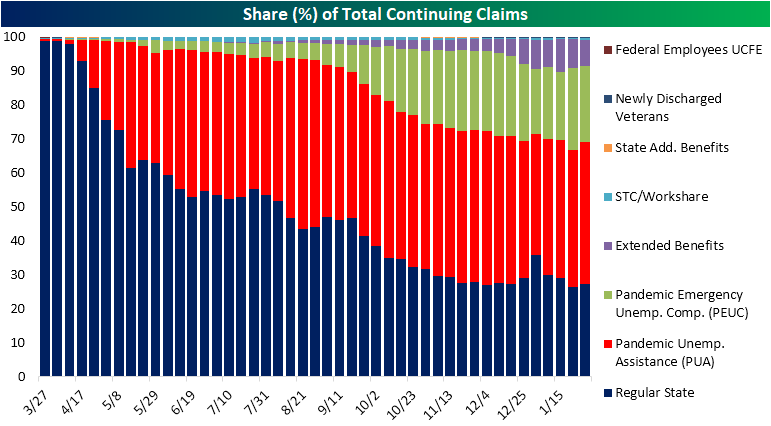

While unadjusted regular state claims were slightly better, factoring in Pandemic Unemployment Assistance (PUA) claims, the picture once again worsens. PUA claims saw a significant increase of 174.43K from last week rising to 516.3K. That is the highest level of PUA claims since the week of September 18th and the biggest one-week increase since mid-May.

On a state level, though, there are some added quirks. Ohio was the single biggest contributor to that increase in PUA claims as the state reported 232,016 claims (or 44.9% of all national claims) compared to only 10,156 in the prior week. That’s 2% of the state’s entire population The next biggest contributor to PUA claims was California with only 38,052 claims. Even for just regular state claims, Ohio has led the pack with the highest level of claims of any state second to only California. Over the past two weeks, Ohio has reported regular state claims above 140K. That compares to an average for the state of 49.7K from March through the last week of January. When looking at these numbers, we would urge some caution taking them purely at face value given news of large-scale fraudulent claims.

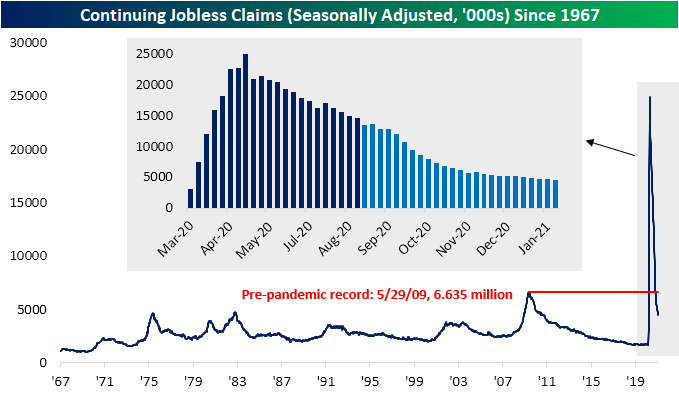

As for continuing claims, the same trends are still very much in place. Seasonally adjusted continuing claims which are lagged one week to initial claims fell for a fifth consecutive week and made another low for the pandemic period. At 4.494 million in the first week of February, regular state continuing claims were at the lowest levels since March 20th.

Factoring in other programs adds an additional weeks’ lag to continuing claims, and here too continuing claims improved. Total claims across all programs fell from 19.7 million for the week of January 22nd to 18.376 million in the last week of January. While sequentially better, total continuing claims have still hit a bit of a plateau for the time being. Additionally, extension programs like Extended Benefits and Pandemic Emergency Unemployment Compensation (PEUC) saw some of their most significant declines since the start of the pandemic; to a degree reversing what has been a trend of a growing prevalence of these types of claims. PEUC continuing claims fell by 718K on a week over week basis which was the second-largest drop behind the drop of over 1 million at the end of 2020 due to the expiration of benefits before being renewed shortly after. For the Extended Benefits program, the 196.9K decline was the biggest single-week decline of the pandemic.Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

B.I.G. Tips — Charts We’re Watching — 2/18/21

Bespoke’s Morning Lineup – 2/18/21 – Earnings Season Ends on a Down Note

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“High expectations are the key to everything.” – Sam Walton

With Walmart’s (WMT) earnings crossing the tape this morning, we have finally reached the unofficial end to earnings season. Despite high investor expectations, it was generally a positive period for the equity market, although initial stock reactions to earnings reports haven’t been particularly positive. The key to the tepid initial reactions of stocks reporting, as Sam Walton once said, is high expectations. When investors and analysts are expecting good news, it sets the bar high. The key to the market’s ability to post positive returns during earnings season was the fact that the economy has been hanging in just fine, COVID trends are moving in a more favorable direction, and the FOMC continues to prime the pump.

WMT’s reported weaker than expected headline EPS this morning, and the stock is trading down over 4% on the news. While 4% may not sound like much for the typical stock reporting earnings, for WMT, it represents a pretty significant move. Historically, the stock has only moved up or down 2.6% on the day it reports earnings, and going back to 2001 there have only been two other times where the stock saw a larger downside gap – 2/20/18 (-7.4%) and 8/17/07 (-4.6%).

Futures are indicating a lower open today as the trend has been lower all night. A ton of economic data was just released, though, so we’ll see how the market digests them. Below, we provide a summary of how these reports came out relative to expectations. Overall, it was a mixed bag, and the initial reaction from futures has been muted.

Housing Starts – 1,580K vs 1,660K estimate

Building Permits – 1,851K vs 1,679K estimate

Initial Claims – 861K vs 770K estimate

Continuing Claims – 4,494K vs 4,450K estimate

Import Prices – 1.4% vs 1.0% estimate

Philly Fed – 23.1 vs 20.0 estimate

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports from around the world, economic data out Asia and Europe, an update on the latest national and international COVID trends, and much more.

Concerns over rising interest rates crept into the market yesterday as the 10-year yield briefly topped 1.30% hitting its highest level since last March. Heading into the opening bell, the 10-year yield is currently sitting right at 1.30%, but that is still well below levels seen a year ago right before the pre-COVID peak in rates and also 20 basis points below the dividend yield on the S&P 500. Which would you rather have? All else equal, higher rates are worse for equity prices than lower rates, but when you’re coming from record low levels of rates due to a complete shutdown of the US economy, some increase in rates can certainly be tolerated.

Daily Sector Snapshot — 2/17/21

Tech Leading in New Highs

The S&P 500 has been reversing from its record highs over the past couple of sessions, but on an individual stock basis there are still a large number of names that have reached new 52-week highs. As shown in the charts from our Daily Sector Snapshot below, through yesterday’s close, a net percentage of just over 15% of the S&P 500 reached new 52-week highs. That is the strongest reading in new highs since January 12th. Outside of several days at the start of 2021, the only other days of the pandemic era with as high if not higher readings were September 2nd, October 9th, and November 9th. Most of the sectors are also seeing their number of new highs rise to strong levels. In addition to the S&P 500, yesterday’s reading for Communication Services, Financials, Materials, and Tech all were in the top decile of all days since at least 1990. In the case of Materials, while new highs have been trending higher and yesterday’s reading was historically strong, it was still well off the record highs from earlier this year.

On the other hand, perhaps the most impressive sector in terms of net new highs has been Technology. Yesterday, 35.53% of the sector’s stocks reached a new 52-week high. Not only is that the highest reading with respect to the other sectors, but that high reading also stands in the top 0.5% of all days for the sector since at least 1990. In other words, there have only been 38 other days since 1990 that the Tech sector saw as strong of a reading in net new highs as yesterday. The most recent of those was November 9th when 43.84% of the sector touched a new 52-week high. Overall, in the context of more broadly positive breadth with strong readings in new highs for other sectors, Tech’s large number of new highs is an added plus for the broader market given the massive 28.08% weight of the sector. Try Bespoke Premium to receive these charts on a daily basis in our Sector Snapshot report.

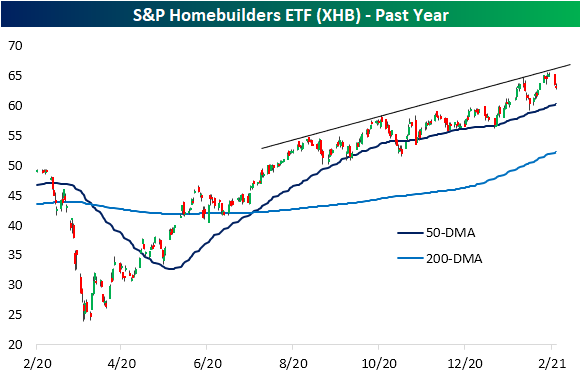

Homebuilders Hot While Purchases Decline

The housing sector remains on fire and as such, homebuilder sentiment remains historically elevated. After falling for the past two months, the NAHB’s Housing Market Index experienced a small bounce in February. The index rose from 83 to 84 compared to expectations of no change. At 84, it is still 6 points below the November record high of 90, but that is also above any other reading in the history of the data prior to October.

The improvement in the headline number this month was driven entirely by higher traffic. That index was up 4 points month over month and now sits 5 points below November’s record high of 77. Meanwhile, of the other components, Present Sales went unchanged at 90 while optimism for the future was dented with that index dropping to a six-month low of 80. Again, although those readings have not improved, they remain historically strong.

As with the different categories of the report, the readings across the various regions’ indices were mixed. The West was the only region where homebuilder sentiment declined. Granted, that drop was only 1 point and at 91, the index still ties the pre-pandemic record high. Meanwhile, the South went unchanged and the Midwest experienced a small rebound.

One of the more notable changes of the whole report was sentiment in the Northeast. Even though it too has been at some of the strongest levels on record, over the past few months the region’s reading on homebuilder sentiment has been a significant laggard compared to the rest of the nation. From its high of 87 in October, the index for the Northeast fell 19 points through January. For comparison, in that same span, the Midwest index fell only 4 points while the South and West were up 1 and 3 points, respectively. In February, though, whereas other regions remain several points off their highs, the Northeast put in a new record high after lurching 21 points higher. The only times that this index has risen by more in a single month was in June (31 points) and July (22 points) of last year.

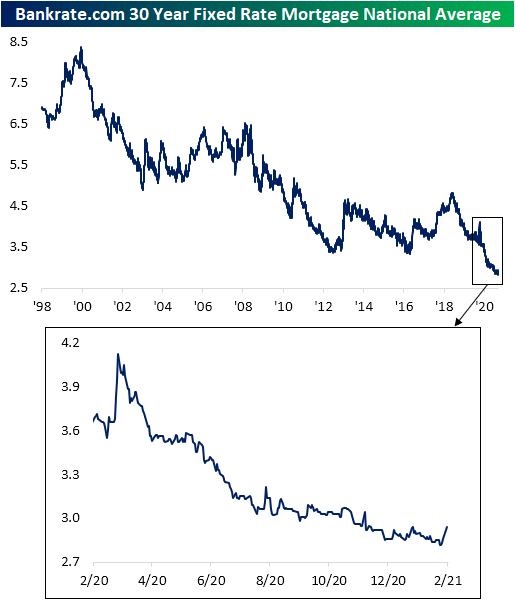

As for other housing data released this morning, the MBA’s weekly reading on mortgage purchase applications has continued to fall. Since the peak in mid-January, mortgage purchase applications have fallen nearly 14%, and the index now sits at the lowest level since the first week of November. Granted, that is still well above pre-pandemic levels, so it’s hardly a weak reading.

Higher mortgage rates likely in part played a role in that lower reading in mortgage applications. As shown below, with a broader rise in rates recently, the national average for a 30 year fixed rate mortgage has gone from a low of 2.82% just over a week ago to 2.94% yesterday; tied with January 12th for the highest rate since the end of November. That has also been the biggest one-week rise in the average mortgage rate since August.

Like the macro data released today, homebuilder stocks are in turn off their highs. After reaching extreme overbought levels last week at the top of its uptrend channel that has been in place over the past few months, the S&P Homebuilders ETF (XHB) has been mean-reverting over the past couple of days. With the downward move, the 50-DMA will be a support area to watch as it consistently has been since the summer. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.