The Bespoke 50 Top Growth Stocks — 8/26/21

Chart of the Day: SPAC Update

Bulls Head In Separate Directions

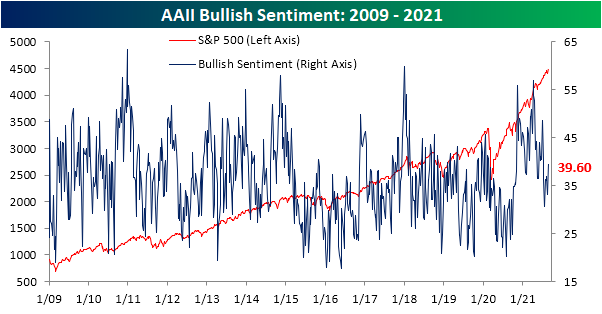

As the major indices have set more record highs in the past week, bullish sentiment has rebounded. The American Association of Individual Investors’ (AAII) weekly reading on bullish sentiment rose 6.4 percentage points to 39.4% this week. That is the highest reading of optimism since the week of July 8th when bullish sentiment was a hair above 40%. While recovered, that reading is still muted versus the past year’s range and is only 1.5 percentage points above their historical average. In other words, bullish sentiment has rebounded but is far from elevated.

While the AAII survey showed an increase in bullish sentiment, another survey of newsletter writers from Investors Intelligence saw the opposite result. This survey’s reading on bullish sentiment dropped to just 50% this week which is the lowest level since May of last year. Although this reading has now fallen out of the past year’s range, it is still slightly elevated versus the historical average of 45%.

Given the uptick in bullish sentiment, the AAII survey saw only a third of respondents report as bearish versus 35.1% last week. Like bullish sentiment, this reading remains outside of the range it has occupied for most of the past year although that current reading is also not far away from the historical average of 30.5%.

As we noted in last Thursday’s Chart of the Day, the bull-bear spread dipped into negative territory last week for the first time since late January and it was at the lowest level since October 2020. With the inverse moves in bullish and bearish sentiment this week, the spread has moved back into positive territory to its highest level since the last week of July.

Not all of the gains to bullish sentiment came from the bearish camp. Neutral sentiment saw an even larger decline of 4.2 percentage points. That brings the reading down to 27.5% which is the lowest reading since April 15th when it stood at just 21.6%. Click here to view Bespoke’s premium membership options.

NSA Claims Break Below 300K

For the first time in four weeks, seasonally adjusted jobless claims came in higher with claims ticking up to 353K. Additionally, last week’s reading was also revised 1K higher to 349K. Albeit higher, this week’s print does remain at the low end of the range since the pandemic began and is less than 100K away from the March 13, 2020 level of 256K (the last print before claims rose into the millions).

It continues to be a point in the year that regular state claims have the benefit of seasonal tailwinds. The current week of the year has historically only seen claims rise week over week 16.7% of the time on a non-seasonally adjusted basis. This week, claims fell by 11.7K resulting in the first sub-300K print of the pandemic. While regular state claims were lower, PUA claims rose for a fourth week in a row even with the program’s expiration (September 5th) rapidly approaching. This week’s 9.63K increase was the largest of the past few weeks bringing PUA claims up to 117.71K. That is the highest level since the week of April 23rd.

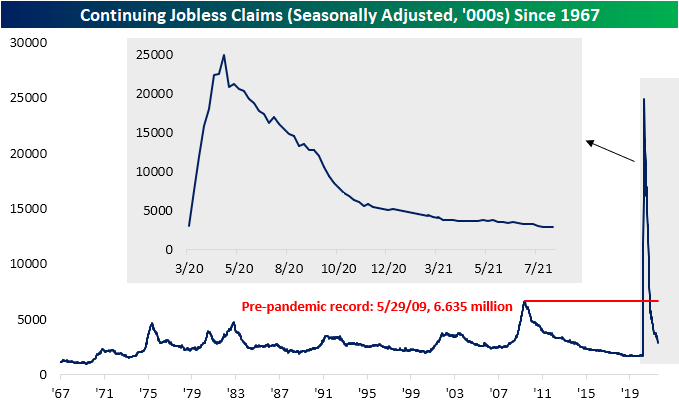

Seasonally adjusted continuing claims were also disappointing this week. Last week’s print was revised higher by 45K to 2.865 million, and while this week’s number was lower at 2.862 million, it was worse than expectations for a decline to 2.72 million. Thanks to that higher revision, claims have now fallen for three weeks in a row and are once again at pandemic lows.

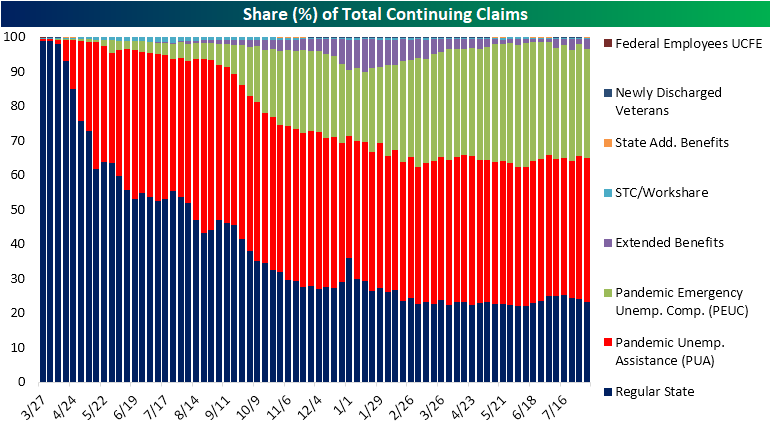

Including all other programs adds another week of delay so the most recent read on continuing claims across all programs is through the week of August 6th. Total claims rose to 12.02 million that week versus 11.84 million in the final week of July. Two of the largest programs, regular state and Pandemic Emergency Unemployment Compensation (PEUC), saw significantly lower claim counts that were offset by increases in PUA and extended benefit claims. PUA claims rose back above 5 million due to a 104.71K increase erasing most of the decline from the second half of July. Extended benefits remain particularly volatile, and this week saw another big move with claims rising 173.5K. At 351.4K, this program is at one of the highest levels since April. While there are still several weeks until the data would catch up, through those most recent readings there are 8.8 million slated to lose benefits with the September 5th expiration for pandemic programs. Click here to view Bespoke’s premium membership options.

Subway Traffic Holding Up

Earlier this week, we took a look at the decline in airline passenger traffic in recent weeks and noted that while some of the declines may be related to the Delta-variant, seasonality was likely a decent contributor to the slowdown. With summer winding down and schools getting back into session, vacation season is winding down and diminishing the need for air travel. At the same time, business travel remains depressed and therefore isn’t there to pick up the slack.

It’s only one data point, but along these lines, we were surprised to see that subway ridership in New York City has seen little in the way of a negative impact on ridership in recent weeks. On a good day, the last place most people want to be is on the subway, and if you’re worried about catching COVID, it’s one of the first places you would avoid. The chart below shows weekly turnstile traffic on NYC subways going back to 2015 with red dots marking comparable weeks to the most recent data.

The first thing that stands out on this chart is that subway traffic still has a long way to go before getting back anywhere close to normal levels. From 2015 through 2019, subway traffic was gently drifting lower but was still pretty consistently above 30 million riders per week. At the depths of the shutdowns, ridership plummeted down to 2.6 million riders and has slowly climbed higher ever since. In the week ending 8/14, ridership totaled just under 12 million riders. While that is up over 50% from the same week last year, it is still well below the average of 30 million for the same week of the year from 2015 through 2019. At this point, ridership would have to increase by 150% just to get back to pre-pandemic levels.

Looking a little closer at the ridership numbers, we found it interesting to see that while ridership usually declines in August (look at the line before the red dots in each of the years before 2020), this year we haven’t seen nearly as large of a drop. To put it in percentage terms, from 2015 through 2019, weekly ridership in the current week of the year dropped an average of 5.6% relative to its level from four weeks earlier. This year, though, the decline has been close to half that at 3.3%. In the grand scheme of things, this isn’t an enormous difference, but if the surge in COVID cases was causing more cautious behavior, we would have expected to see an even larger decline. An alternative explanation for a smaller than normal decline in ridership levels could be due to the fact that many of the people riding the subway now have little in the way of alternative options for commuting and are in fields where summer vacations aren’t as typical as those in other occupations. Ultimately, it’s probably a little of both, but seeing subway ridership levels hold up even as COVID cases surge is a trend we didn’t expect to see. Click here to start a Bespoke Premium trial and receive access to all of our market analysis and commentary.

Travel & Leisure Bounces

After trending lower for the last few months in what now looks like an anticipatory move in advance of the current COVID wave, travel & leisure stocks have bounced back in a big way over the last week. Every one of the travel & leisure stocks in the snapshot below is up 5%+ over the last week, with MGM Resorts (MGM) up the most at +9%. The three cruise stocks — Norwegian (NCLH), Royal Caribbean (RCL), and Carnival (CCL) — have bounced 7-8% over the last week, while the airlines are up between 5-6%.

A week ago, most of these travel & leisure stocks were trading in oversold territory, but they are all back in “neutral” territory now, meaning they’re between one standard deviation above and below their 50-DMAs. The hotels and cruise stocks have largely crossed back above their 50-DMAs, while the airlines are still sitting below them.

As you can see, even though they’ve had a rough time over the last few months, all of these travel & leisure stocks are still in the green on a year-to-date basis, with MGM and American Airlines (AAL) up the most at 33.7% and 27.77%, respectively.

The underperformance of these names well ahead of the current COVID wave and their recent bounces in the midst of the wave serves as an important reminder that it’s often the case that the markets knew the headlines you’re reading today months ago. Click here to start a Bespoke Premium trial and start building your own custom portfolios.

Mega-Cap Tech Snapshot

Bespoke members have the ability to build “custom portfolios” that allows them to easily track the stocks and ETFs they care about most. One simple custom portfolio that we’ve created tracks the eight mega-cap Tech stocks. Below is a snapshot of these eight stocks as they appear in our “Custom Portfolios” tool. If you wanted to track your own stocks and ETFs in a similar fashion, simply start a Bespoke Premium trial and click on the “Custom Portfolios” page once you’re logged in.

As shown below, all eight of the “mega-caps” are up over the last five trading days, but NVIDIA (NVDA) is the clear standout with a massive gain of 16.66%. The recent move higher for NVDA leaves it up 70% on the year and 12.4% above its 50-day moving average! It also puts the stock in extreme overbought territory, which means it’s more than two standard deviations above its 50-DMA.

While Amazon (AMZN) is up 3% over the last week, it’s still 4.8% below its 50-DMA and in oversold territory. Apple (AAPL) is the only mega-cap that’s not overbought or oversold but rather neutral, meaning it’s trading within one standard deviation above or below its 50-DMA. Facebook (FB), Alphabet (GOOG), Microsoft (MSFT), Netflix (NFLX), and Tesla (TSLA) are all overbought, but unlike NVDA, they’re not in extreme territory.

On a YTD basis, none of the mega-caps are in the red, but three are just barely positive. Amazon (AMZN) is up 1.3% YTD, Netflix (NFLX) is up 1.27% YTD, and Tesla (TSLA) is up 0.78% YTD. That’s about as close to flat as it gets, and we’re already nearly eight full months into the year already. Behind NVDA’s 70% gain, Alphabet (GOOG) is up the second most in 2021 at +63.2%, followed by Microsoft (MSFT) at +36.67% and Facebook (FB) at +34.86%. Apple (AAPL) is sitting on a YTD gain of just over 12.33%. That’s a solid move, but it’s well behind the S&P 500’s YTD gain of 19%.

Bespoke members can also easily see price charts of all the stocks or ETFs in the custom portfolios that they create. This is a helpful way to monitor technicals across baskets in an efficient manner. Instead of having to look through price charts one by one, you can quickly see them all on the same page. Looking at the price charts of the eight mega-caps, you can see that Apple (AAPL), Facebook (FB), Alphabet (GOOG), Microsoft (MSFT), and NVIDIA (NVDA) are all in long-term uptrend channels, while things have been much more choppy for Amazon (AMZN), Netflix (NFLX), and Tesla (TSLA). Click here to start a Bespoke Premium trial and start building your own custom portfolios.

Bespoke’s Morning Lineup – 8/26/21 – A More Equal Rally

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing great was ever achieved without enthusiasm – Ralph Waldo Emerson

Futures are mixed heading into the second to last trading session of the week, and there has been little change even after initial claims and the revision to GDP. Generally speaking, the reports came in close to expectations with little in the way of surprises. For the rest of today, markets will be watching for commentary from Fed officials ahead of tomorrow’s Jackson Hole speech from Fed Chair Powell. This morning, KC Fed President Esther George, who is a non-voter, suggested that it’s time for the Fed to start removing stimulus, and right now St. Louis Fed President Jim Bullard (another non-voter this year) is striking the same tone, although he has had these views for some time now. All week long, the market has been betting that Powell would take a dovish tone in tomorrow’s speech, but after the rally of the last five days, maybe that has become too priced in at this point.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

After underperforming the market-cap-weighted index for months, the equal-weighted S&P 500 has recently started to get back on track and has been reaching new highs itself as well. After bumping up against resistance multiple times in the spring and early summer, the equal-weighted index briefly broke out to new highs in late July and early August before pulling back last week on concerns over Afghanistan and a Fed taper. The index pulled back to its 50-DMA, but like the market-cap-weighted index, it has bounced back nicely and finally hit a new high again in yesterday’s trading.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.