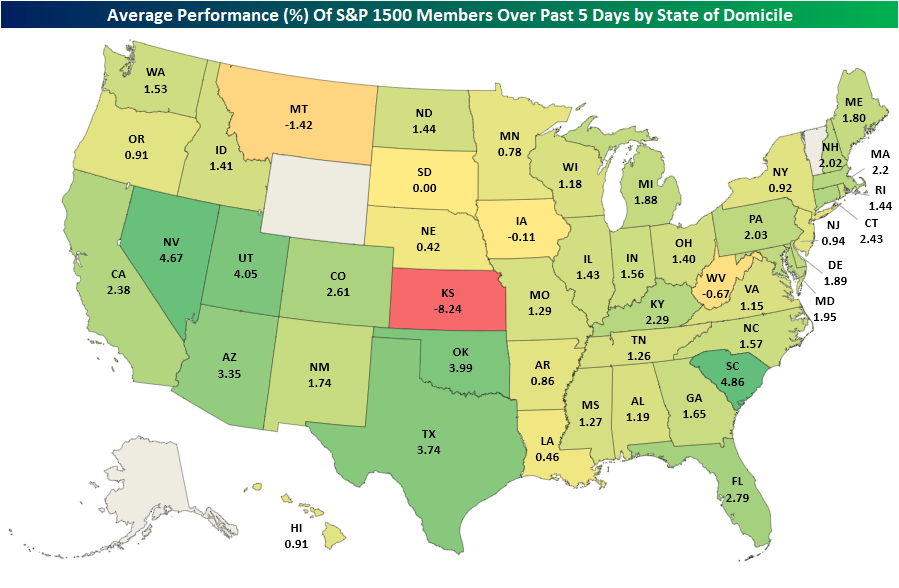

S&P 1500 States of Domicile

It’s hurricane season and leading the news to start the week has been the landfall of Hurricane Ida on the 16-year anniversary of Hurricane Katrina. In today’s Morning Lineup, we detailed the initial impact of the storm on what will likely be the most impacted sector: energy. As could be expected with a regionally focused event, equities are largely shrugging things off with the S&P 500 and Nasdaq both solidly higher and reaching new records today. As for a more particular look, in the heatmap below, we show the average five-day performance of S&P 1500 stocks based on their state of domicile.

Obviously, this is not an exact read-through of a stock’s geographic exposure—for example, a company may be headquartered in one state, but the bulk of its business is based in others—but Louisiana based equities have, on average, actually seen worse performance than neighboring states or the country more broadly. Of the average performance of stocks domiciled in the 48 applicable states plus DC (no S&P 1500 companies are domiciled in Alaska, Wyoming, or Vermont), Louisiana-based stocks rank as the eighth-worst performers over the past five days. The absolute worst state, though, has been Kansas, but that is primarily due to an over 36% decline in SelectQuote (SLQT). Admittedly, this is an imperfect measure of a company’s geographic exposure, and individual stories related to each specific business are of greater importance than where each company is domiciled. it is interesting to note that S&P 1500 companies domiciled in Louisiana have underperformed the broader market in the past week.

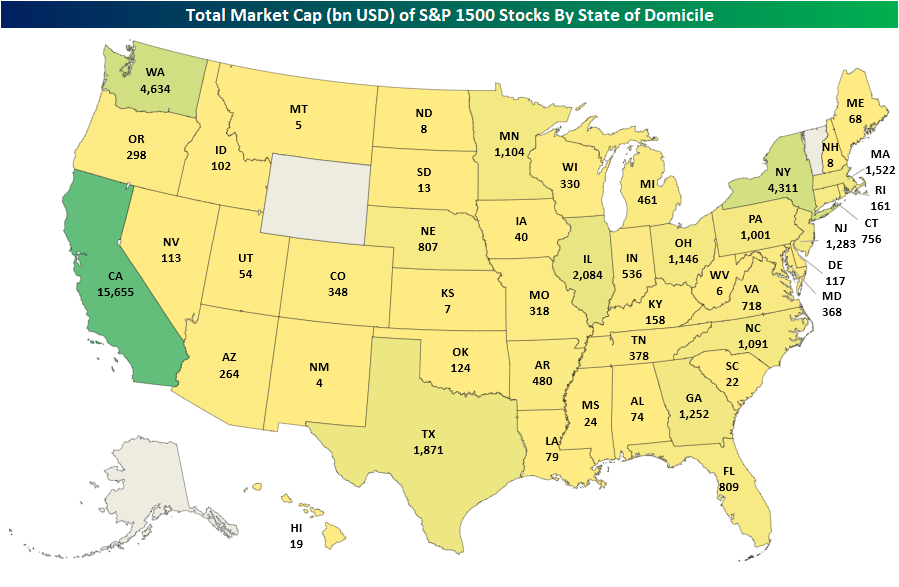

When looking at average performance, we would also caution that various states have dramatic differences in the actual number of stocks domiciled within each state. For example, there are just seven S&P 1500 companies domiciled in Louisiana, and their combined market cap is only $79 billion. That compares to neighboring Texas with 130 stocks that have a total market cap of $1.8 trillion. It also pales in comparison to California’s 223 stocks with a combined market cap above $15.5 trillion. So again, holding constant any more systemic or lasting effects of the storm, looking purely at where stocks are domiciled does not imply Hurricane Ida would necessarily have a massive impact on broad swathes of the market. Click here to view Bespoke’s premium membership options.

Dallas Fed Flops

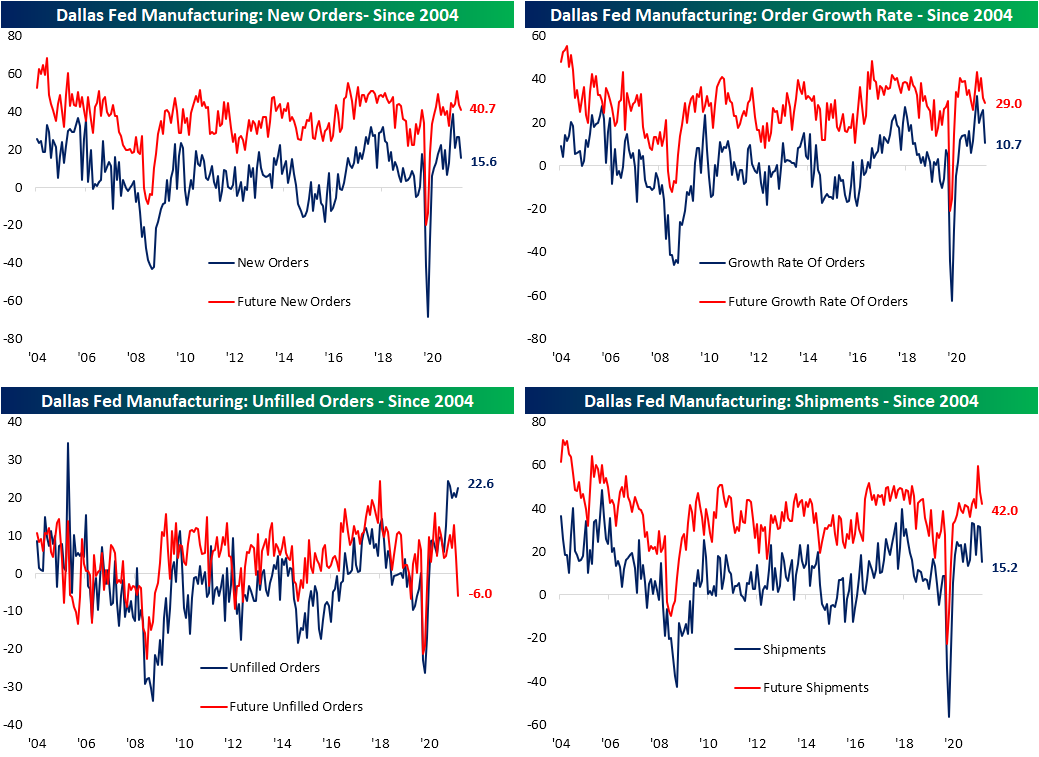

Leading into today, the four already released results from regional Fed banks’ monthly manufacturing reports broadly showed a material slowdown in activity in August which we showcased in the most recent update of our Five Fed Manufacturing Composite in last week’s Bespoke Report. The fifth and final report out of the Eleventh District added more confirmation to that slowdown with its release this morning. The Dallas Fed’s headline index peaked back in April at 37.3 and has declined each consecutive month since then including in August. In fact, this month’s decline was by far the most severe as the indicator dropped 18.3 points versus only 3.8 point declines the prior two months and a 2.4 point decline in May. The 18.3 point decline month over month also ranks as the eighth largest MoM decline on record and the largest since last March when it fell by a record 70.4 points. Another decline had been penciled in this month with the index forecasted to fall from 27.3 to 23, but the drop to 9 made for the eleventh biggest miss versus expectations since at least 2009.

Looking across the various categories of the report, declines were broad across categories with only unfilled orders, inventories, hours worked, and prices paid higher relative to July. Those declines are largely coming off of historically strong readings, though, with many in the top decile of their historical range last month. Even after falling, every category is still above their historical median readings with many still in the upper deciles. In other words, manufacturing activity slowed but remains at solid levels.

Order growth and shipments are the areas to have seen the greatest moderation over the past few months. In August, these indices all saw some of the largest declines in point terms and are now much less elevated than other readings. For example, new orders are only in the 72nd percentile and Shipments are only in the 65th. Those declines leave the indices at similar levels to the start of this year. Again, the declines in these indices do not mean activity is contracting, but rather is decelerating meaning orders are still growing at a healthy level. One example of this is unfilled orders. With order growth at a solid clip, unfilled orders actually ticked higher, remaining at unprecedentedly high levels. We would also note, while businesses reported order backlogs are continuing to grow at historic rates, they do not foresee that to remain the case. Expectations for the category dropped into negative territory this month (the only reading across current conditions and expectations to do so).

Prices and supply chains also appeared to have gotten some relief in August and could be playing a role as to why businesses appear optimistic to work off order backlogs. While still right around record highs, prices received and delivery times were both lower. Unfortunately, while customers saw some price relief, prices paid were slightly higher. Meanwhile, Inventories are starting to grow again as the index rose 12.9 points to go back into positive territory for the first time since March 2019.

Employment-focused categories were a somewhat dour point of the survey. Readings on Employment and Wages & Benefits were both lower in August which was met with a decline in capital expenditures. On the bright side, current readings are still at healthy levels and the expectations index for wages and benefits actually hit a record.

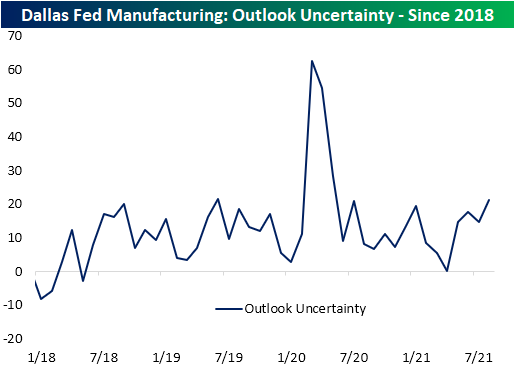

One other point to watch is uncertainty. The Dallas Fed’s reading on uncertainty does not have much in the way of an extensive history, only dating back to the start of 2018, but the index did rise to 21.1 as COVID cases rose through the summer. Those levels are well below the highs reached earlier in the pandemic, but are once again at the upper end of the past few years’ range. Click here to view Bespoke’s premium membership options.

Bespoke Matrix of Economic Indicators – 8/30/21

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Bespoke’s Morning Lineup – 8/30/21 – Slow Start to the End of August

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The roots of education are bitter, but the fruit is sweet.” – Aristotle

It’s hard to get closer to unchanged in the futures markets this morning than we are now. The S&P 500 is indicated to open up by 3 points, the Nasdaq by 12, and the Dow higher by 10 points. While Hurricane Ida continues to slam Louisiana and the deadline for the US withdrawal from Afghanistan approaches, market-moving news is scarce this morning. In terms of economic data, Pending Home Sales will be released at 10 AM, and the Dallas Fed Manufacturing report comes out a half-hour later.

Last week was a good one for the US equity market with the S&P 500 rallying about 1.5% and the Russell 2000 surging more than 5%. Across individual sectors, though, returns for the week were mixed. For sectors like Energy, Financials, and Materials, it was a great week with all three rallying more than 2.5% and Energy surging by triple that rate. Despite the surge in Energy stocks, though, it is still the only sector that heads into the week below its 50-day moving average.

On the other end of the spectrum, Utilities, Consumer Staples, and Health Care all actually fell more than 1% while Real Estate was also lower. Given its weighting in the overall market, the sector that really matters is Technology, and with a gain of 1.45% that was actually up pretty much right in line with the broader market.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Bespoke Brunch Reads: 8/29/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Collectibles

Al Capone’s Last Haul: The Gangster’s Family Auctions His Mementos by Richard Morgan (WSJ)

A huge batch of pistols, pocket watches, and other curios like a silver-plated cocktail shaker owned by the gangster are set to hit the auction block. [Link; paywall]

Labor Markets

Driver recruitment wars: Cowan to pay $20,000 sign-on bonus by Todd Maiden (Freight Waves)

With huge demand for freight services, drivers are an extremely scare commodity and are driving a bidding war for CDL holders; sign-on bonuses are going as high as $20k. [Link]

Bad Reviews

Yelp Reviews Fuel Fights Over Covid-19 Vaccine Requirements by Charity L. Scott (WSJ)

Small businesses which opt to require vaccination for clients or customers are being mobbed by hordes of anti-vaccine trolls, which seek to drive down their ratings. [Link; paywall]

Supply Chains

Why Is the Supply Chain Still So Snarled? We Explain, With a Hot Tub by Austen Hufford, Kyle Kim and Andrew Levinson (WSJ)

A step-by-step walk-through of the thousands of parts and intricate assembly that goes into a hot tub, all of which has been snarled by delays and shortages across the entire global supply chain. [Link; paywall]

Exclusive-Ford doubles Lightning production target on strong pre-launch demand -sources by Ben Klayman and Joseph White (Street Insider)

Ford’s electric F-150 model is due for launch next year, and the company has seen reservations top more than 120,000. As a result, it’s targeting production of more than 80,000 by 2024 but only 15,000 next year. The contrast between total demand and what the company is planning to build is striking. [Link]

Investors

Yale Taps Matthew Mendelsohn to Succeed Endowment Chief David Swensen by Juliet Chung and Dawn Lim (WSJ)

Yale’s massive $31bn endowment will have new leadership to replace legendary investor David Swensen, who passed last May. [Link; paywall]

God, Money, YOLO: How Cathie Wood Found Her Flock by Matt Phillips (NYT)

A profile of the manager who has built a massive active ETF empire out of relentless optimism and business analysis that presses that optimism for all it’s worth. [Link; soft paywall]

COVID

Those Anti-Covid Plastic Barriers Probably Don’t Help and May Make Things Worse by Tara Parker-Pope (NYT)

Aerosolized COVID virus is best fought with air flow, not plastic barriers which prevent the turnover of air in a given space by blocking movement. [Link; soft paywall]

Weird News

Baby on cover of ‘Nevermind’ sues Nirvana alleging child pornography by Nadine El-Bawab (CNBC)

The infant baby who was used in the iconic cover of Nirvana’s album is suing on the grounds that the use of his image constitutes child pornography. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Daily Sector Snapshot — 8/27/21

The Bespoke Report – He Came, We Saw, Bulls Conquered

This week’s Bespoke Report newsletter is now available for members.

For several days, all the market could do was focus on the upcoming Jackson Hole speech from Fed Chair Jerome Powell. Will he signal in September or won’t he? Well the day finally came, and because the conference was changed from in-person to virtual, we all got to see the speech live on Friday morning. Powell didn’t say anything new, and since that followed a number of hawkish comments from other members of the committee, that was all bulls needed to conquer the day and push the S&P 500 to more record highs.

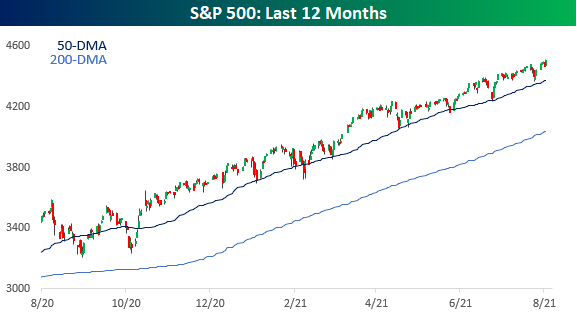

With the exception of last September and October, the S&P 500 has been in one of the steadiest uptrends ever. Tests of the 50-day moving average (DMA) are few, far between, and extremely short. Meanwhile, the S&P 500 is still maintaining ample social distance with the 200-DMA as that trend line shouts, “Remember me?”

In this week’s Bespoke Report, we cover a lot of different topics. Among them:

- A record number of records and Nasdaq 1,000 point milestones.

- A loot at some high-frequency COVID statistics,

- This week’s surge in crude oil and what it means for energy stocks going forward.

- A review of prior market responses to the GOMC Jackson Hole conferences.

- Bitcoin sentiment.

- Low volume rallies. Do they matter?

- The “Montana Curve”.

- Seasonality. And much more.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

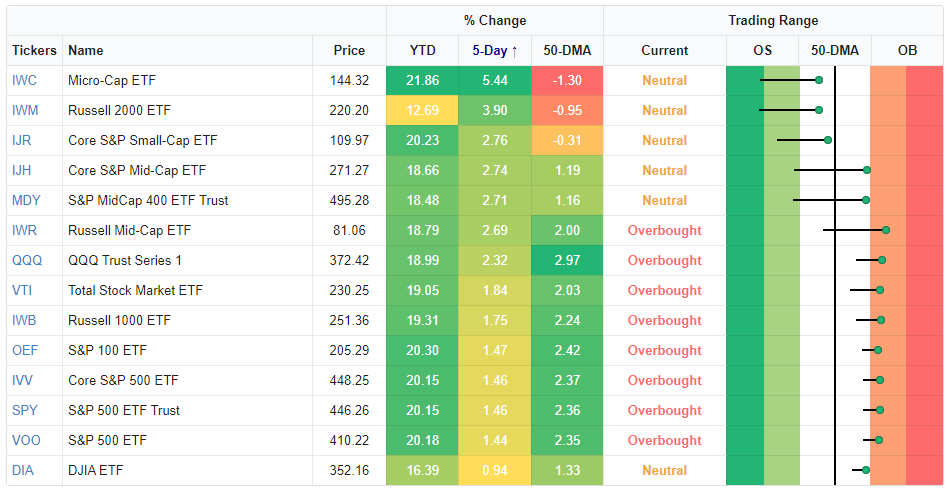

Small-Caps Bounce

ln today’s Morning Lineup, we noted the inverse correlation between performance this week and market caps. As shown in the major US Indices screen of our Trend Analyzer tool, the two best performers over the past five days have been Micro-Caps (IWC) followed by small caps like the Russell 2000 (IWM) and the Core S&P Small-Cap ETF (IJR). Mid-cap ETFs are the next best performers with high 2% gains then most large cap indices have only risen around 1.5% this week with the exception of the Dow (DIA) which has not even gained 1%. As for where these indices are trading relative to each one’s trading range, it is partially a mean reversion story. Small caps were deeply oversold one week ago and are now sitting just below their 50-DMAs. While not to as extreme of a degree, mid-caps were similarly trading a full standard deviation below their 50-DMAs last week. Today, they are on the opposite side of their 50-DMAs and on the verge of overbought readings.

As previously mentioned, small caps like the Micro-Cap ETF (IWC) and Russell 2000 ETF (IWM) were oversold last week. From a charting perspective, each of these indices’ rallies this week are not only bounces from extreme oversold levels, but they also follow brief dips below their 200-DMAs. But whereas the past five days have seen solid gains, yesterday saw IWC and IWM reject their 50-DMAs and the high end of their ranges that have been in place since late July. In other words, even though small caps have led the market this week, they are not out of the woods yet.

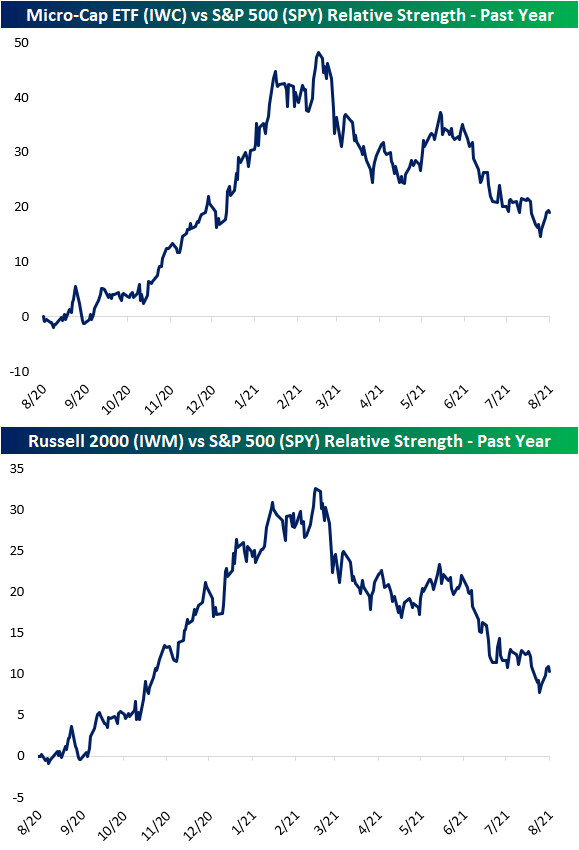

Looking at the relative strength lines of small caps like IWC and IWM versus the large cap S&P 500 (SPY) over the past year, the past week’s outperformance again is a blip on the radar and has only put a small dent in the longer term trend of underperformance.

Where that is not necessarily the case is small market caps versus the smallest market caps. As shown below, the relative strength line of the Micro-Cap ETF (IWC) versus the Russell 2000 (IWM) broke out of the past few months’ downtrend over the past few days. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 8/27/21 – Here Today, Gone Tomorrow

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Every time we can force our opponents into a bad decision, we win.” – Annie Duke

The moment investors have been waiting for all month is finally here. Will Fed Chair Jerome Powell hint at a taper or won’t he? That’s the question everyone is waiting for. While the market will no doubt react to the Fed Chair’s words, it’s likely only a matter of time before his comments are in the rearview mirror and the market shifts its focus to other things. Leading into the release of this morning’s speech, a number of Fed governors have been on the tape in the last 24 hours suggesting the need for the Fed to start the process of tapering, so while they could be greasing the skids for a start of the taper, the only opinion that really matters at this point is the opinion of the Chair.

A number of economic indicators just crossed the taps and while most were more or less inline with expectations, the biggest outliers were Wholesale Inventories which rose less than expected (0.6% vs 1.0%) and Personal Income which saw a big beat rising 1.1% compared to forecasts for an increase of 0.3%.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

It’s been a very strong five days for US equity markets even after yesterday’s decline. Since the close last Thursday, every one of the major index ETFs we track in our Trend Analyzer is up, and the only one that’s up less than 1% is the Dow Jones (DIA). Looking at the performance of the various ETFs, performance has been inversely correlated to market cap with the indices covering the smallest market caps up the most (Micro-Cap and Russell 2000) while the large-cap ETFs have seen more muted, albeit still impressive, returns. In terms of where each ETF stands relative to its trading range, the most overbought ETFs have generally been the laggards this week while the top performers are actually still below their 50-DMAs.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.