Jobless Claims Finally Below 1 Million

This morning’s release of initial jobless claims marked the first time that claims were below 1 million since the week ending March 13th (21 weeks). Jobless claims fell 228K to 963K compared to expectations of a much smaller drop to only 1.1 million from 1.19 million last week. This week’s 228K decline was a slightly smaller drop than the prior week’s 244K decline but remains a much larger improvement than what was observed through most of June and July. Overall, claims are certainly on the right track with the first sub-1 million milestone now in the bag, but the 963K initial claims filed in the past week is still a historically elevated level higher than anything observed prior to the pandemic.

On a non-seasonally adjusted basis, this was actually the second week that claims were below 1 million with last week’s reading of 988.3K and this week’s 831.9K. This decline comes with the seasonal tailwind that claims typically decline from early July through September.

Continuing claims are echoing the continued improvements in labor data with another decline of 604K this week bringing the seasonally adjusted number to 15.486 million. That leaves continuing claims at the lowest level since the first week of April. Again, as is the case with initial claims, continuing claims remain historically high but are headed in the right direction.

Not only is the headline number of claims improving but so are claims for Pandemic Unemployment Assistance (PUA). Initial claims by this measure fell from 0.66 million to 0.49 million this week. These are some of the lowest readings since the program began in mid-April. That brings the total between NSA claims and PUA claims to 1.32 million. While lagged an additional week, continuing claims for the week ending July 24 (26.6 million) were the lowest since April 24th, and for PUA claims in particular, it was the lowest reading since the end of May. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – 8/13/20 – Jobs in the Spotlight

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Time is the friend of the wonderful company, the enemy of the mediocre.” – Warren Buffett

For the first time in 21 weeks, jobless claims dropped below a million (963K), which was below consensus forecasts for 1.1 million. Continuing claims also came in lower than expected but by a narrower margin. 963K is still high by all historical comparisons outside of the last several months, but it indicates a continuation of a move in the right direction. Regarding stimulus talks, if it was going to take a sense of urgency to get Democrats and Republicans to come to an agreement, the stock market trading right near record highs and jobless claims back below a million aren’t providing any ammunition.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, new FHFA fees on mortgage refinancings, trends related to the COVID-19 outbreak, and much more.

Small caps have been outperforming large gaps in recent weeks off the March lows after the Russell 2000 was decimated during the COVID crash. Over just the last week, the Russell 2000 has outperformed the S&P 500 by nearly a full percentage point, but as shown in the chart below, the index still has some catching up to do. Besides the fact that small caps saw their peak relative to large caps earlier in the last decade, they have only erased barely more than half of the underperformance they saw from the S&P 500’s February peak to March trough.

100 Days of Gains

Today marked 100 trading days since the Nasdaq 100’s March 20th COVID Crash closing low. Below is a chart showing the rolling 100-trading day percentage change of the Nasdaq 100 since 1985. The 59.8% gain over the last 100 trading days ranks as the 3rd strongest run on record. The only two stronger 100-day rallies ended in January 1999 and March 2000.

While the Nasdaq 100 bottomed on Friday, March 20th, the S&P 500 bottomed the following Monday (3/23). This means tomorrow will mark 100 trading days since the S&P 500’s COVID Crash closing low. Right now the rolling 100-day percentage change for the S&P 500 sits at +46.7%. But if the S&P manages to trade at current levels tomorrow, the 100-day gain will jump above 50%. It has been 87 years (1933) since we’ve seen a 100-day gain of more than 50%! Click here to view Bespoke’s premium membership options for our best research available.

TGIW

Friday is just about everyone’s favorite day of the week, but for both the entire year and since March 23rd, the best days for the S&P 500 have been Monday and Wednesday. On a YTD basis, the S&P 500’s median gain on Mondays has been 0.70% while Wednesday’s median gain has been 0.50%. Outside of those two days, Tuesdays and Thursdays have been modestly positive, while Friday is the only day of the week that has seen declines on a median basis.

Looking just at the period since 3/23, Mondays and Wednesdays have still been the strongest with median gains of 0.73% and 0.71%, respectively. Behind those two weekdays, Fridays have seen improved performance with a median gain of 0.34% followed by Tuesday (0.17%) and Thursday (0.00%). What’s notable about the nearly five months since the 3/23 low is that every day of the week has seen gains on a median basis.

In terms of consistency, Mondays have been the most positive day of the week both on a YTD basis and since the March lows. Since the March low, Wednesday and Friday have both seen gains two-thirds of the time, and while Monday through Thursday have seen similar levels of consistency whether you look on a YTD basis or since the March lows, Friday has had a pretty wide disparity. In the period from late January through late March, investors did little in the way of buying on ‘Corona Fridays’ ahead of the weekend, but once the initial panic of the outbreak began to subside in April, that sentiment started to fade. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Rotation Underway

Bespoke’s Morning Lineup – 8/12/20 – Summer Reruns

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“From neither the White House nor any other senior administration post would there come any leadership, any attempt to set priorities, any attempt to coordinate activities, any attempt to deliver resources.” – John M. Barry, The Great Influenza

In reading the quote above, critics of the President would think that it’s a description of the current attitude in the White House towards the Covid-19 outbreak. It’s actually from the book, The Great Influenza: The Story of the Deadliest Plague in History. Back in 1918. Amazingly, President Wilson never made a single public statement related to the flu pandemic and acted like it never happened and instead had a singular focus on mobilizing the country for WWI.

In looking at today’s “Overnight Trading” chart from the Morning Lineup, it looks the exact same as yesterday’s chart. For the sake of the bulls, let’s hope that today’s intraday trading for US stocks isn’t a re-run of Tuesday as well.

Joe Biden’s selection of Kamala Harris wasn’t particularly surprising to the market as she was already considered one of the leading contenders along with Susan Rice, and the pick makes sense for Biden as Harris will likely be solid on the campaign trail and go after Trump in the way that a VP candidate is expected to. While the selection isn’t likely to provide much of a boost for Biden, at this point it likely won’t hurt him either. Harris wasn’t exactly successful as a Presidential candidate in her own right, but back in 2008 neither was Biden and that didn’t hurt Obama.

On the inflation front, after yesterday’s PPI doubled expectations (+0.6% vs 0.3% forecast), today’s CPI for July saw the exact same print on a headline basis relative to the same consensus expectation for an increase of 0.3%.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, trends related to the COVID-19 outbreak, and much more.

Since last Thursday’s close, the S&P 500 is down 0.46%, but the decline has been far from broad-based. As shown to the right, four sectors are up over 1% during that period with Industrials and Financials both rallying more than 4%. On the downside, Technology has been the main drag with a drop of over 3.6% while Communication Services has dropped 1.8%. Of the 500 stocks in the index, nearly two-thirds are actually up during that span, so the vast majority of stocks in the index and the US for that matter have risen during this period.

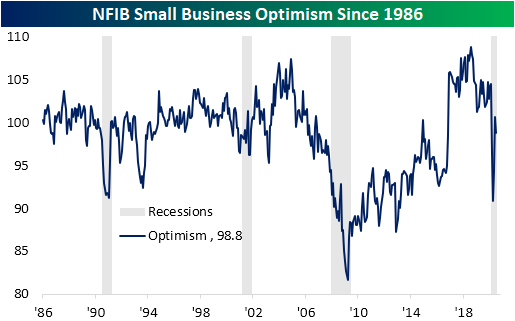

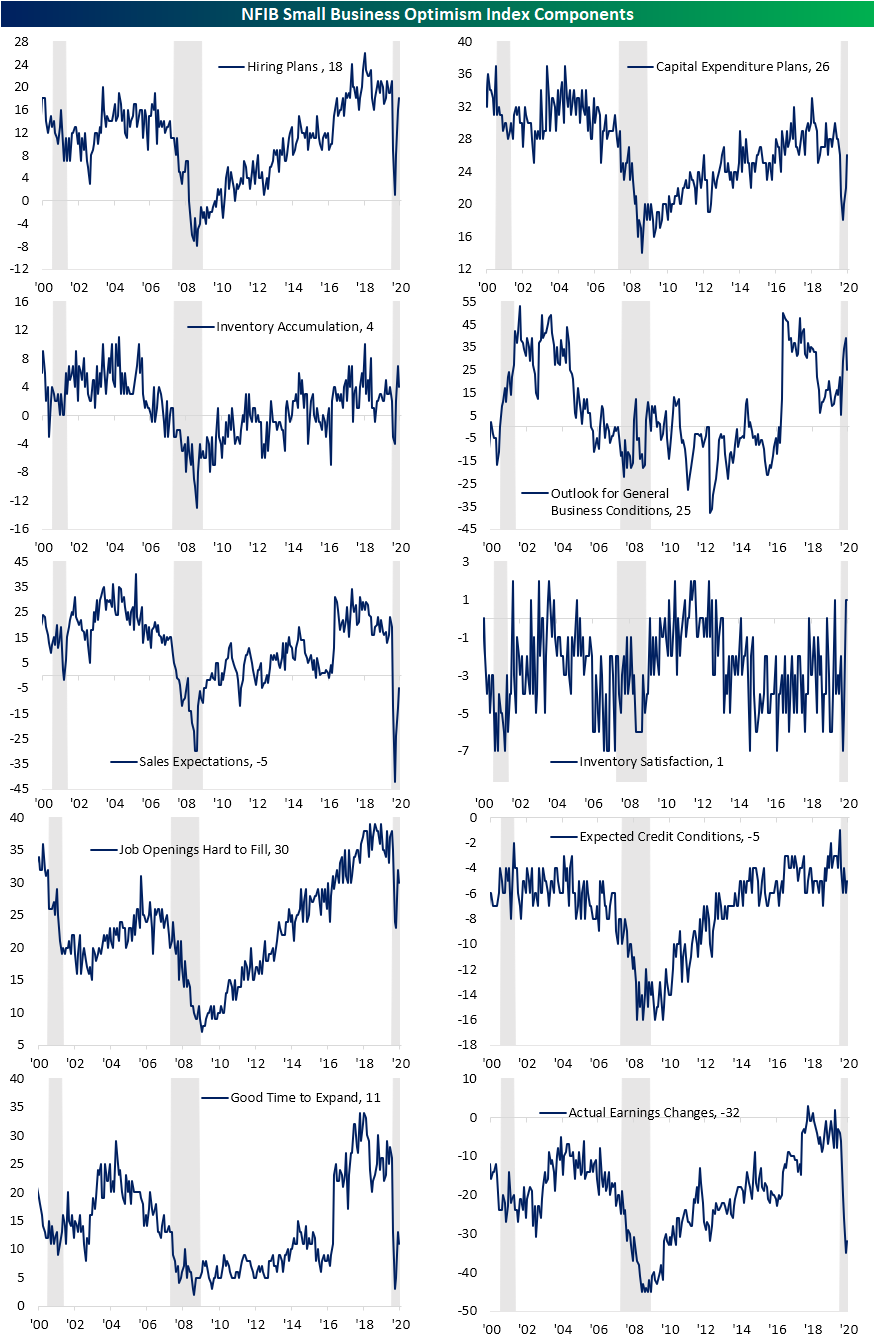

Small Business Split

After two months of some of the largest gains to small business confidence on record, NFIB’s Small Business Optimism index pulled back slightly in July. The index fell 1.8 points to 98.8 which was also below expectations of a reading of 100.5. While lower sequentially and still well off the highs from prior to the pandemic, July’s level of 98.8 was less than half a point from the historic average for small business optimism of 98.4.

Overall, breadth was very mixed in the July report. Of the ten components of the headline index, four fell, one was unchanged and the other five rose. As the pandemic drags on, the most glaring decline weighing on the headline number was for expectations of improvements in the economy. Fewer companies reported now as a good time to expand (that index fell to 11 from 13 in June) and a net percentage of 25% expect the economy to improve compared to 39% in June. The 14 point decline is tied with an identical decline in August of 2011 for the seventh-largest MoM decline on record for that index, but it only leaves that component in the 81st percentile of all readings. In other words, small businesses are less optimistic for the future than they were in June, but on net are still expecting the economy to improve. That can be seen through hiring plans as a higher share plan to increase employment and increase capital expenditures with those indices rising 2 points and 4 points, respectively. On the other hand, fewer businesses plan to increase inventories as those expecting higher sales remains muted albeit improving. That can also be seen through the 3 point rise in the index for actual earnings changes. Fewer businesses were also reporting weak sales as the most pressing issue for business.

Additionally, although they are not inputs to the headline index, a record low of 26 percent reported borrowing on a regular basis, though, the cause of that does not appear to be due to credit availability. The index for credit availability was slightly higher in July and remains in the top 5% of all readings. The most important issues echo this as only 1% reported financials and interest rates to be the biggest issue; unchanged from last month. The biggest issue for businesses remains the quality of labor. That index rose from 19 in June to 21 in July. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Gold (GLD) Gaps Down

Bespoke’s Morning Lineup – 8/11/20 – New Highs Back in View

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Can we make it eight in a row? Based on this morning’s move in the futures, the DJIA and S&P 500 are both on pace to extend their current seven-day winning streaks to eight. The Nasdaq, meanwhile, is working on its own streak as it is on pace to underperform the S&P 500 for the third straight day.

In economic news, the NFIB Small Business Optimism report missed expectations, and PPI came in much higher than expected. That hotter than expected inflation data hasn’t had any impact on futures as of yet, though.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, trends related to the COVID-19 outbreak, and much more.

As the S&P 500 sets its sights on new record highs, its cumulative A/D line has already set the path. With a number of positive readings in the last few days, the cumulative A/D line has broken out of its short consolidation range from the last couple of weeks. That’s an encouraging sign for the direction of the market going forward, even as tech starts to take a back seat.