Chart of the Day: EM En Fuego

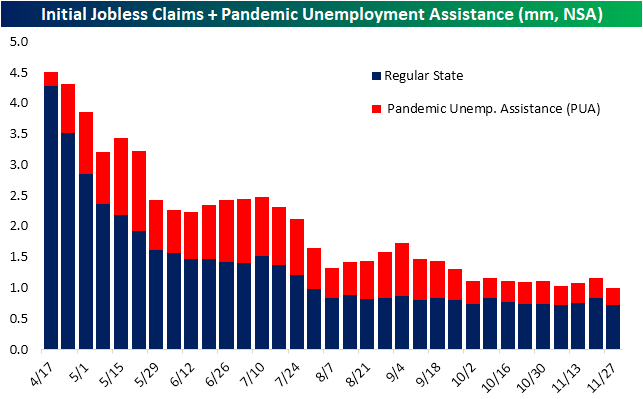

Claims Back to the Lows

After two weeks of upticks, initial jobless claims saw some good news this week ahead of the Nonfarm Payrolls number on Friday. Claims experienced a sizeable decline falling 75K from last week’s upwardly revised reading of 787K. A decline had been expected with forecasts calling for a drop to 775K. Instead, the decline was much larger as claims came in at 712K. That is just 1K above the pandemic low from the first week of November. Although it is still a historically high reading, claims have continued to get closer to moving below the pre-pandemic record high of 695K from October of 1982.

The picture was even better for unadjusted claims. Although the current time of the year has historically marked a seasonal upswing in claims, the 48th week of the year has typically marked a decline week over week. Given the seasonal tailwind for the current week of the year, claims fell to a new low for the pandemic. Unadjusted claims came in at 713.8K, 122.5K below last week’s reading of 836.3. That was the largest weekly decline in the unadjusted number since the last major leg lower in the first week of August when claims fell by nearly 150K.

As we note every week, while the decline in regular state initial claims is a welcome sign no matter what, it does not show the entire picture. In the chart below, we show initial claims and claims through the Pandemic Unemployment Assistance program (PUA). This week, total claims between regular state and PUA also reached a new low for the pandemic coming in just above 1 million this week and below the previous low of 1.021 million from the first week of November. That was a result of not only the drop in regular state claims, but PUA claims also falling 30K to a new low.

While lagged an additional week to initial jobless claims, adjusted continuing claims likewise painted a pretty optimistic picture as well. Continuing claims fell 569K this week, down to 5.52 million, exceeding expectations for a decline to 5.8 million. That is the first reading below 6 million since March 20th, and it is also now well below what had been the pre-pandemic record high of 6.635 million from the global financial crisis.

Including the data for all programs of the weekly report adds yet another week of lag, but it does give a more complete picture. For the week of November 13th, total continuing claims fell to 20.2 million from 20.56 million the previous week. That is slightly below the level from the last week of October, which brings total claims to the lowest level since April. Taking a look across the programs, the overall decline was driven by drops in regular state claims and an even larger decline in PUA claims.

Given the length of time that many claims have been in place though, counts for programs that extended insurance once expiration is reached (which varies in length from state to state) like the Extended Benefits program and Pandemic Emergency Unemployment Compensation (PEUC) program have continued to rise. With regards to the Extended Benefits program, claims have now risen for 22 straight weeks through November 13th, albeit the most recent week’s 59.7K rise was the smallest week over week increase since August 21st. Similarly, PEUC claims have continued to rise with the most recent week adding another 79.7K. That leaves the total number of claims between these two programs at over 5.25 million for the first time of the pandemic. That means that despite some light at the end of the tunnel of the COVID front given positive vaccine news, with the pandemic continuing to drag on, nearly a quarter (26%) of all people receiving jobless benefits have been unemployed for an extended period of time. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 12/3/20 – Less Terrible Claims

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Confidence is not ‘I will profit on this trade.’ Confidence is ‘I will be fine if I don’t profit from this trade.’” – Yvan Byeajee

It’s a busy day for economic data, and it’s starting off on the right foot with both initial and continuing jobless claims coming in better than expected, albeit at still terrible levels. As bad as the numbers are, though, it’s encouraging that claims are moving in the right direction. With claims behind us, the next report of focus is the ISM Services report at 10 AM Eastern. Expectations for this report are also low as activity levels have started to decline in recent weeks as case counts rise.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, Markit PMI data for the services sector, an update on the latest national and international COVID trends, and much more.

The latest COVID wave has clearly been the most severe in terms of the number of confirmed cases, geographic reach, hospitalizations, and soon to be deaths. The chart below compares the 7-day average number of US confirmed COVID cases (red line) versus the relative strength of our basket of “Stocks for the COVID Economy” that we first published in early March versus the S&P 500 (blue line).

In the early stages of this wave, right before and up to the announcement of the vaccine from Pfizer (PFE) on 11/9, COVID stocks underperformed the S&P 500 rather sharply, but since 11/9, COVID stocks have once again started to outperform the S&P 500. They still remain well off their highs on a relative basis, but the initial reaction to vaccine news appears to have been overdone.

Salesforce Big Buys

The past couple of weeks had seen some rumblings that one of the newest additions to the Dow, Salesforce.com (CRM), was in talks to buy Slack (WORK). On Tuesday, the deal was officially announced to the public with the transaction valued at approximately just over $25 billion. The deal is set to be CRM’s largest acquisition to date, surpassing last year’s $14 billion acquisition of Tableau Software. While that would nearly double the previous record-sized acquisition for the company, there have been several other acquisitions valued at more than $1 billion at the time of the announcement.

The announcement concerning Slack is CRM’s seventh acquisition with a value of at least $1 billion, and it is the second such deal of 2020 after software company Vlocity was taken on back in February. Additionally, while the announced deal with Slack is the largest in terms of dollars, as a percentage of CRM’s market cap it is actually roughly in line with the Tableau acquisition and will be slightly larger than the deal with Exact Target in 2013.

As for these past deals, a negative reaction in the stock price of CRM has very much been the norm one week after the deal was announced. As CRM has fallen over 9% in today’s session, it is already on pace to see the worst stock price reaction since the announcement of a deal with MuleSoft in 2018. While positive returns have come down to a coinflip one to three months later, in the times the stock has rallied, the gains have been double digits. Additionally, six months out has consistently seen Salesforce higher with an average gain of over 20%. Click here to view Bespoke’s premium membership options for our best research available.

Market Caps and YTD Performance Drivers in November

In yesterday’s B.I.G. Tip report, we showed a decile analysis of performance in the month of November based upon a range of metrics. One of the most notable themes was performance based on market cap. Whereas for most of this year the stocks with the largest market caps have outperformed, the opposite was true in November. If the small-cap Russell 2000’s return to new all-time highs wasn’t indication enough, the decile of Russell 1000 stocks with the smallest market caps rose an average of 28.5% in November. That is head and shoulders better than the next decile (the 9th) in which the average stock rose 17.09%. As you move up the ladder in terms of market cap, performance worsened with the largest stocks seeing some of the worst performance on the month. The first decile saw an average gain of 12.39%. That group includes stocks with market caps above $100 billion including the trillion-dollar club: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), and Google (GOOG).

Again, some of the stocks with the largest market caps have also been the ones that have risen the most this year. Given this, the stocks that were up the most on a year-to-date basis through the end of October were also the ones that underperformed the most in November and vice versa. As shown below, the decile of stocks that have been the top performers from the start of the year through October averaged a gain of 12% in November. The second decile averaged an even smaller 9.35% rally. On the other end of the spectrum, November saw heavy rotation into the stocks that had been most beaten up this year. The decile of the worst performers averaged a substantial 38.08% rally in November. Deciles 8 and 9 similarly saw big rallies of 16.05% and 21.45%, respectively. These deciles included a lot of reopening stocks like airlines, energy, travel, regional banks, and brick and mortar heavy retail. Click here to view Bespoke’s premium membership options for our best research available.

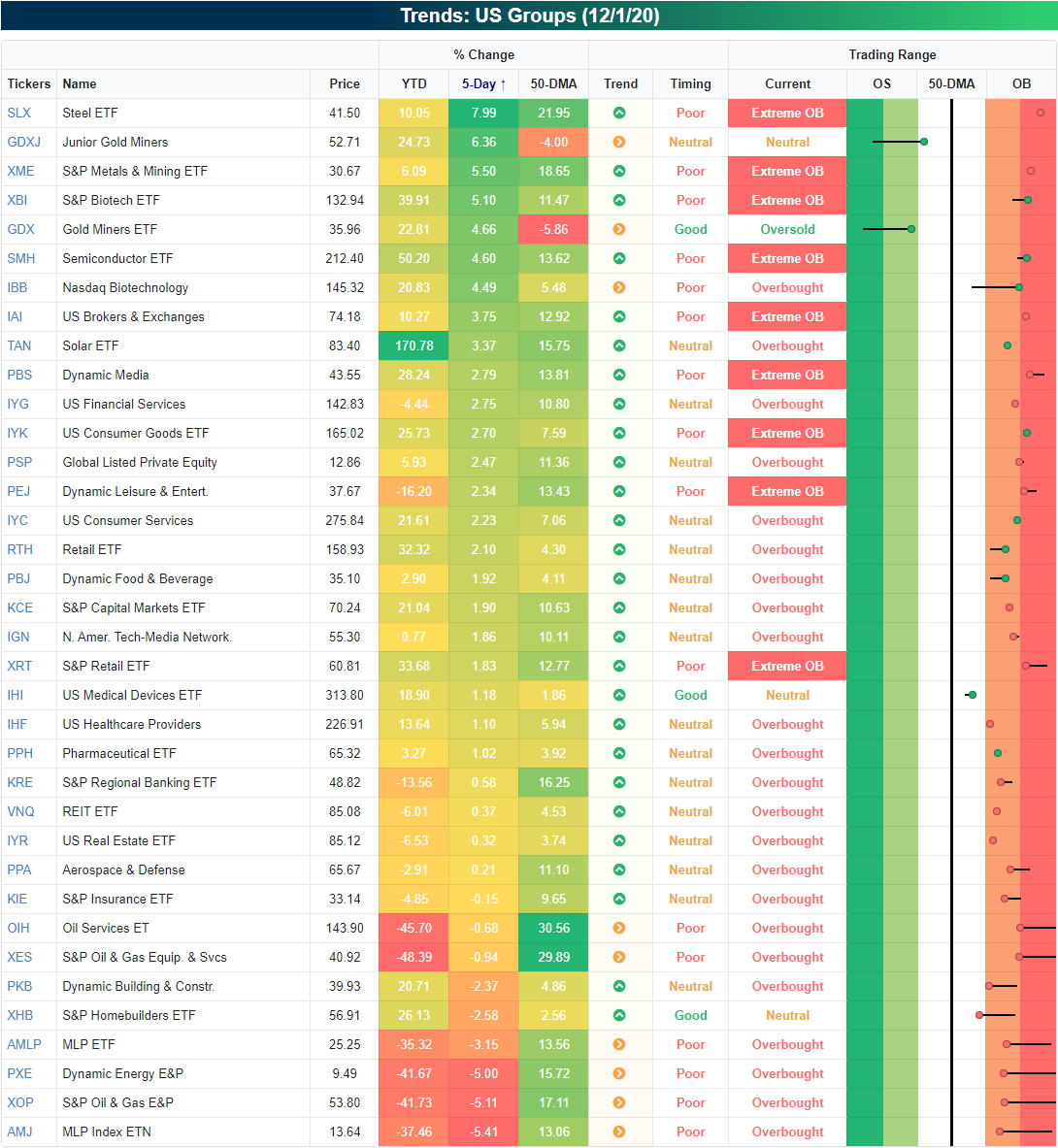

Hard to Beat Steel

In Monday’s Chart of the Day and Closer, we noted the recent outperformance of industrial metals relative to other commodities, namely precious metals like gold. Given the strength of industrial metals, in the equities space, stocks related to the steel industry have been surging in recent days. Over the five days through yesterday’s close, the Steel ETF (SLX) which tracks these types of stocks has been the top-performing ETF of the US groups screen in our Trend Analyzer with a nearly 8% rally as shown below. That massive rally has left SLX as the most overbought ETF of this screen. Other metal related groups like the Junior Gold Miners (GDXJ) and S&P Metals and Mining ETF (XME) have also been top performers.

While there are plenty of reasons for steel’s rally including bets on a recovery in global growth, seasonality also appears to play a role. As shown in the snapshot of our Seasonality Tool below, for the current week of the year over the past 10 years, SLX has been the top-performing ETF with a median rally of 2.26%.

With SLX’s massive rally over the past several months which has accelerated in part thanks to seasonal tailwinds more recently, the ETF’s long-term downtrend that has been in place since not long after its inception has now been broken. As shown below, SLX is now around its highest levels since April of last year. While that is a positive from a long-term perspective, on a shorter-term basis SLX is running very hot. As shown in the second chart below, the ETF currently trades over 2.5 standard deviations above its 50-DMA. That is a historically elevated overbought reading as it is in the 98th percentile of the historical range. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 12/2/20 – Wednesday Hangover

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Well, I don’t have any greater insight than anybody else.” – Jensen Huang

Hangover on a Wednesday? Well, there is football today, so anything is possible! After a great start to the month yesterday, futures are indicated lower this morning as concerns over a stalemate on any agreement related to a stimulus/spending bill weigh on sentiment. ADP Private Payrolls for November was just released and came in weaker than expected. While economists were forecasting an increase of 440K jobs, the actual reading came in more than 100K weaker at 307K. That’s a pretty big miss, but there has been little reaction in the futures market on the premise that ADP has been consistently weaker than expected over the last few months.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, Eurozone auto sales, an update on the latest national and international COVID trends, and much more.

Equities have continued to do well lately, but semis have been an area of notable strength. While the S&P 500 has rallied nearly 1% in the last three trading days, the Philadelphia Semiconductor Index (SOX) has rallied over 1% on each of the last three trading days for a total gain of over 4%. Semis are considered one of the more cyclical sectors of the market, so their recent strength is a good sign.

Chart of the Day – December: The Worst of Times for Retailers

November 2020 Asset Class Performance

The S&P 500 had its best November since 1928 with a gain of 10.75%. Below is a snapshot of our asset class performance matrix showing total returns across US-listed ETFs. Of the major US index ETFs, SPY was actually up the least in November with a gain of 10.88%. The S&P Smallcap 600 (IJR) and the Russell 2,000 (IWM) were up nearly twice that with gains of more than 18%.

Of the major sectors, Energy (XLE) was up by far the most in November but you’ll notice that it’s still down 35% year-to-date. The Financial sector (XLF) was up the second most in November with a gain of 16.85%, but like Energy, it too is still in the red on the year. Utilities (XLU) had the worst month with a gain of just 0.74%.

Outside of the US, four countries gained more than 20% — Brazil (EWZ), France (EWQ), Italy (EWI), and Spain (EWP). All four of these countries still finished November in the red for the year. India (PIN) and China (ASHR) were up the least of the countries listed with gains of 8% and 6.95%, respectively.

Looking at commodity ETFs, oil (USO) had a banner month with a gain of 22.65% while natural gas (UNG), gold (GLD), and silver (SLV) were all solidly in the red. For the year, though, USO remains down 69.8%. Finally, the various fixed income ETFs in our matrix were all up slightly on the month. The long-term Treasury ETF — TLT — remains up nearly 20% on the year, which easily beats the S&P 500 by more than five percentage points. Click here to see Bespoke’s premium membership options and start a free trial for instant access to our research and interactive tools.

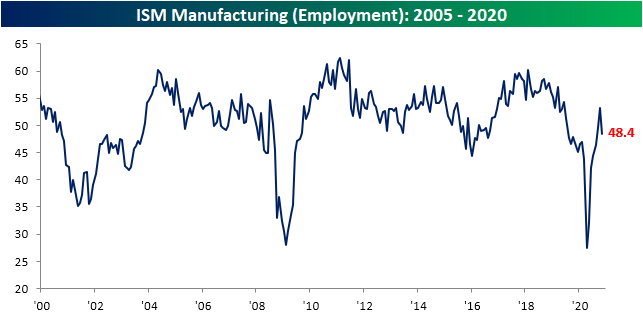

Headcounts Hurting

Today’s ISM report pointed to broad improvements in the manufacturing sector in November, albeit there were some slowdowns in areas like New Orders, Production, and worst of all Employment. The index for Employment saw the sharpest decline falling 4.8 points from an expansionary reading of 53.2 in October to a contractionary 48.4 in November. That decline was in the bottom 5% of all month over month changes. Taking a more granular look, 18.9% of companies reported a lower number of workers (compared to 17.7% last month) whereas 14.8% reported a higher number (23.1% in October). 66.4% reported no change in the number of employees, up from 59.3% last month.

That reading at face value may be a bit of a worrying sign as it points to more companies reporting lower rather than higher headcounts. That also goes counter to other parts of the ISM report which pointed to further growth in demand and production. Some explanation can be found at least anecdotally through the comments section though. As shown below, rather than firms mentioning that they are laying off workers, the verbiage more often points to troubles in hiring. For example, there are mentions of “labor shortages” as “finding new people is an issue”. Put differently, there is anecdotal evidence that the manufacturing labor market is facing a supply instead of a demand issue. As a result of these shortages, firms report that there have been production constraints while demand has been strong. Click here to view Bespoke’s premium membership options for our best research available.