Heavily Shorted Stocks Stand Tall in 2021

By far one of the biggest movers of the past few days has been video game retailer GameStop (GME). Since last Friday, GME has risen over 96% with a 57.4% rally in Wednesday’s session alone. Today, the stock is up another 30.61% as of this writing and has reached one of the highest levels since November 2015. One likely factor behind the stock’s move has been a short squeeze of the company’s massive short base. For more than a year now, short interest as a percent of equity float has been around or well above 100%. The most recent reading as of the end of 2020 was 144.33%. In other words, there have been far more shares sold short than are available to trade. In a screen of all active stocks trading on US exchanges, we found only 18 that have more than 100% of their freely floating shares sold short, and they are all penny stocks with very small market caps.

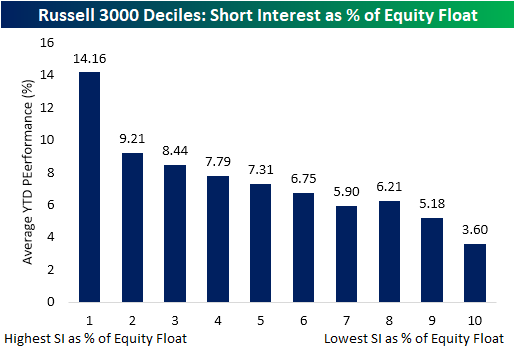

While you would be hard-pressed to find a stock with as high of short interest as a percentage of the float as GameStop, generally speaking, stocks with high short interest have been some of the top performers this year. In the chart below, we show the average YTD performance of Russell 3000 stocks broken into deciles based on their short interest. The decile of stocks with the highest short interest as a percentage of float have by far been the best performers YTD, up for an average of 14.16%. Even excluding GME, the decile’s average YTD performance is a 13.93% gain. As you move across the deciles with lower short interest levels, performance gets worse. The tenth decile of stocks which consists of stocks with average short interest levels below 1% of float has only risen 3.6% on average.

In the table below, we show the 30 Russell 3000 stocks with the highest short interest as a percentage of equity float. Across these names, they are up for an average of 15.76% in 2021, with only three not in the green: National Beverage (FIZZ), Acutus Medical (AFIB), and B&G Foods (BGS). Including GME, the largest number (7) of these most heavily shorted stocks are retailers. In fact, Dillards (DDS) and Bed, Bath, & Beyond (BBBY) both find themselves in the top 5 alongside GME. The former has over 90% of its float shorted while nearly two-thirds of BBBY’s float is sold short. Click here to view Bespoke’s premium membership options for our best research available.

Chart of The Day: This Is Ludicrous

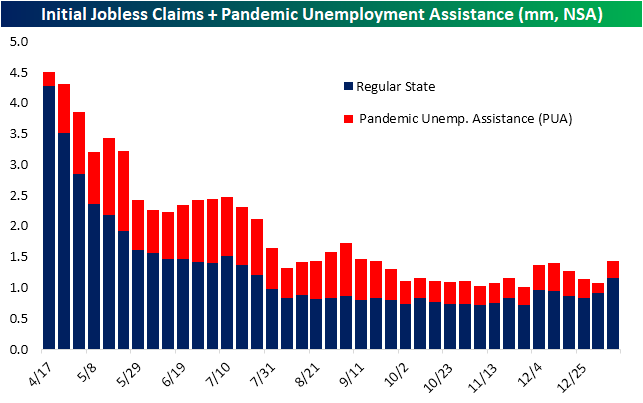

Claims Make A Big Swing Higher

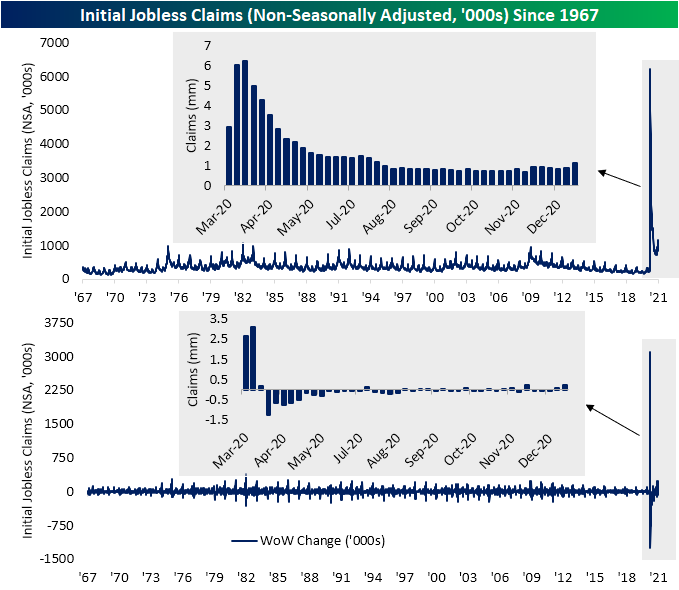

Overall, it was a bad week for jobless claims with both initial and continuing claims missing expectations. Initial jobless claims came in at the worst level since the week of August 21st rising to 965K versus forecasts for a jump to just 789K. That 183K increase versus last week was the largest move higher since April when claims were rising in the millions per week. Additionally, of the states that offered comments on the changes in jobless claims, many noted layoffs in industries like retail, accommodations and food services, and transportation. Despite the acceleration in the vaccine rollout, due to the fact that case counts remain near record highs and COVID restrictions remain in place, businesses and workers in the customer-facing services sectors are still feeling the pain.

While the seasonally adjusted number managed to stay below a million, before seasonal adjustments that wasn’t the case. Initial claims by this measure came in at 1.151 million this week, the highest reading and first time above 1 million since July 30th.

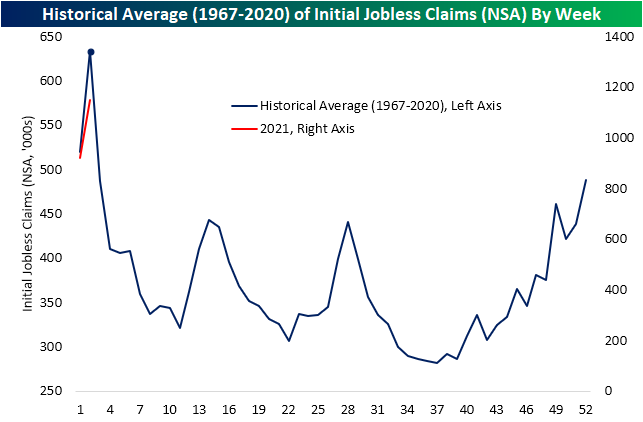

While the most recent week’s uptick is likely not all due to seasonality, as shown in the second chart below, the second week of the year usually does see a fairly large uptick in claims.

Last week we noted how PUA claims experienced a significant drop potentially due to the timing of the signing of the spending bill and the holidays. While there were yet again a handful of states unusually reporting zero PUA claims this week, total PUA claims across the nation were higher by 123.3K up to 284.47K this week. In other words, both regular state claims and auxiliary programs contributed to this week’s uptick.

Continuing claims are lagged one week to initial claims meaning this week’s increase in the initial number was not factored into the continuing claims number, but nonetheless, it was also higher rising to 5.271 million from 5.072 million. That brings claims back to around where they were in mid-December.

Adding in all other programs to regular state claims adds another week’s lag. As of the last week of 2020, total continuing claims across all programs fell to 18.422 million from 19.183 million the prior week. That number is likely to move higher given the significant uptick in initial claims this week, but another problematic aspect of total claims is the growing number of unemployed who have been out of work for a long period of time. The share of claims from extension programs like PEUC and Extended Benefits accounted for nearly 30% of the most recent week’s total claims. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 1/14/21 – Earnings Season Begins

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The ability to recognize that the winds have shifted and to take appropriate action before you wreck your boat is crucial to the future of an enterprise” – Andrew Grove

The President was impeached by the House for the second time in just over a year yesterday, and like the first time, financial markets were unfazed. While the President’s first impeachment in the House in December 2019 was completely on a partisan basis and dead on arrival in the Senate, this time around, the fate of the impeachment in the Senate is more uncertain. What seems certain at this point, though, is that the completion (or maybe even the start of a trial) would not take place until after the inauguration, so from a market perspective, it really doesn’t matter much.

The only economic data of note today was Jobless Claims, and both initial and continuing claims came in much higher than expected. Initial Claims spiked up to 965K versus forecasts of 786K, and Continuing Claims rose to 5.271 million compared to forecasts for 5.0 million. In terms of the market reaction to these much weaker than expected reports, there really hasn’t been any.

In terms of individual companies, although earnings season kicks off today with reports from BlackRock (BLK) and Delta (DAL), the pace of reports will remain slow today and tomorrow. Regarding today’s reports, both BLK and DAL are trading modestly higher in reaction to their reports. Also notable, although not a US company, Taiwan Semi (TSM) also reported strong results and is trading up over 2.5%.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, a discussion of the latest import and export orders from China, an update on the latest national and international COVID trends, and much more.

With yesterday’s big move in Intel (INTC), the stock is now over three standard deviations above its 50-DMA. In the last nearly 40 years, there have only been 22 other days in which the stock was as overbought or more overbought than it is today.

Chart of the Day: Bitcoin Sentiment

Swan Song Bodes Well for Intel (INTC) But for How Long?

After two years at the helm, news broke this morning that Bob Swan will be stepping down from his position of CEO of Intel (INTC). He will be replaced by VMware (VMW) CEO Pat Gelsinger on February 15th. While INTC has been a significant underperformer over the past year—it is the only semiconductor stock in the S&P 500 that is lower than it was one year ago—the immediate response from the market to today’s news has been overwhelmingly positive. As of this writing, the stock is up 8.55% which would be its best day since March of last year around the time of the bear market lows.

Though there is plenty of time left in the day for those gains to be built upon or eaten into, the opening gap was substantial. Opening at $59.50, the gap up of 11.76% was one of the largest for INTC on record. The only times since 2000 that there were larger gaps to the upside were in April of 2001 when the stock gapped up 12.64% on the 11th and 12.21% on the 18th. Going back before 2000, the only upside gap that was even larger was a 29.92% move in October of 1987, not long after Black Monday and when Intel’s stock was trading under $1 on a split-adjusted basis.

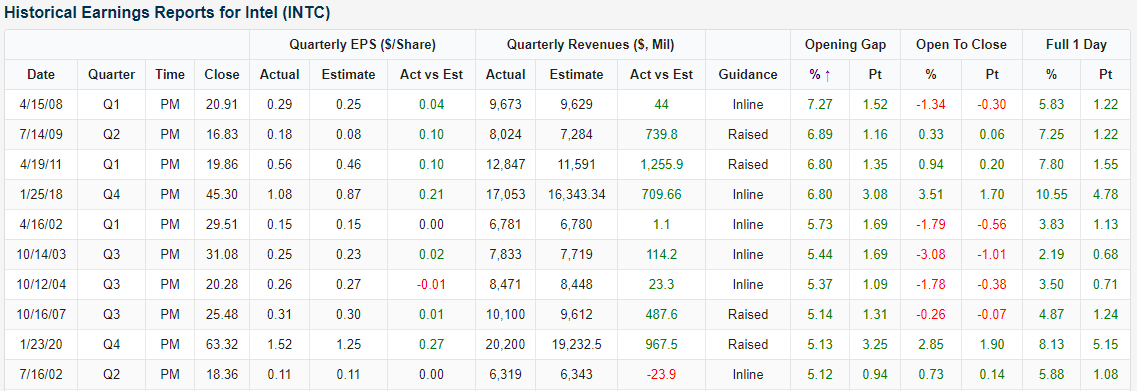

Today’s gap up on the news of a CEO change was also even larger than any move on earnings of the past nearly two decades. As shown in the snapshot from our Earnings Explorer below, the best gap up on earnings news that INTC has experienced since late 2001 was a 7.27% gap following the Q1 results of 2008.

As previously mentioned, there is not much historical precedent for INTC from gaps up as large as today, but of the past four times that INTC gapped up at least 10%, performance in the weeks and months after have generally been pretty negative. The next week has usually seen some further moves higher with the only decline being the second gap up over 10% in April 2001. As for returns throughout the next year, the stock has consistently declined. Like what you see? Click here for a trial to any of Bespoke’s premium membership options.

Impeachment Indicators

The President’s first impeachment proved to be a non-event from both a political perspective and for markets. The possibility of a second impeachment is likely irrelevant to the equity market but could have significant political implications into 2024 and beyond as the Republican Party manages the post-Trump landscape.

Last night, the House passed a request for the Vice President to activate the 25th Amendment and remove the President from office. The Vice President officially declined to do so, which makes impeachment by the House likely either today or tomorrow. The House vote will largely be on party lines, but not entirely. Third-ranking Republican in the House Liz Cheney of Wyoming (daughter of former Vice President Dick Cheney) said yesterday she will vote “yes” on impeachment, and at least four others have joined her as-of this writing. We don’t have a firm estimate on the number of Republicans who will vote “yes” in the House, but we also note that Trump ally and Minority Leader McCarthy (CA) has said he will not formally whip votes against impeachment, raising the possibility that a material chunk of the Republican caucus could side with Democrats.

Of course, the real action will be in the Senate, where the state of play is quite different. While Democrat Joe Manchin of West Virginia has waffled, we think it’s reasonable to expect Democrats to vote as a bloc, delivering 50 of the 67 votes required for conviction should all Senators participate in the final vote.

A number of Republicans have expressed views that support impeachment. Romney (UT), Toomey (PA), and Murkowski (AK) are firm “yes” votes, with Romney already supporting the prior effort and the other two publicly on the record saying they would his time. Other senators including Blunt (MO), Collins (ME), Portman (OH), and Sasse (NE) have expressed openness to the idea of impeachment. Based on assessments of their public stances, we see 24 GOP Senators as “no” votes, and 18 as insufficiently committed either way.

The 7 potential “yes” votes listed above do not include Mitch McConnell, the Republican Senate’s leader. Reports yesterday from a variety of sources reported that he is ‘pleased’ with impeachment efforts, and supports the removal of the President, but at this point, McConnell hasn’t said anything publicly to support this. McConnell is a superlative parliamentary strategist and extremely effective politician. If he does in fact support removal and is willing to whip votes for it, then the 7 other potential “yes” votes will increase given the sheer number of uncommitted Senators and the potential for flips among the 24 “no” Senators. In other words, Mitch McConnell will likely decide the President’s fate, and if yesterday’s reporting is accurate, he is leaning towards impeachment. Below we summarize all 50 GOP Senators into three categories: likely yes, likely no, and no way to tell on the question of conviction.

Conviction of the President in the Senate would functionally remove him from the political scene because he would no longer be able to run for office; if convicted, only a simple majority vote would be required to prevent him from ever again seeking federal office. Therefore for 2024 hopefuls, a “yes” vote could be a simple political calculation that the damage to their primary chances is outweighed by the benefit of not being forced to face the President on the ballot. Regardless of motivations, there are enough potential “yes” votes (especially McConnell and those he would bring with him) that a conviction can’t be ruled out at this stage Also, keep in mind that If a material number of the GOP caucus members abstain from the vote in protest or for other reasons, the number of required votes for conviction drops.

As mentioned above, the possibility of a second impeachment is likely irrelevant to the equity market, especially in the short-term. Regardless of what happens in the House this week, McConnell has already noted that the earliest the Senate would start a trial would be after the inauguration when President Trump will be out of office already and raises questions of whether it is even possible to hold a trial for a President who is out of office. All these are no doubt questions that will be debated in the following days, weeks, and months. Like what you see? Click here for a trial to any of Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 1/13/21 – Easy Going

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” – Benjamin Graham

We’ve had a flurry of central bank officials on both sides of the Atlantic reiterate their stances that they are in no rush to start removing accommodation from the system. In Europe, ECB President Lagarde and council member Villeroy de Galhau both doubled down on their commitment to a 2% inflation target and that they will keep monetary policy loose for as long as needed in order to get the economy back into gear. These comments today follow comments from Fed Presidents Bullard and Rosengren who both also reiterated their commitments to get the economy back to its full potential.

Despite the dovish commentary, futures are modestly lower this morning ahead of the December CPI report. Outside of that report, though, the only other report of note is the monthly Budget Statement later this afternoon. On the political front, the House is expected to vote on impeachment again and at least some Republican members are expected to vote in favor.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, a discussion of the latest report on Machinery Tool Orders in Japan, an update on the latest national and international COVID trends, and much more.

Small-cap stocks have been on roll so far in 2021, but the real action now has been in micro-cap stocks. Through the first seven trading days of 2021, the Russell Micro Cap Index is up 9.4% which is the best start for the index since its inception in 2007. The only other year that was even close was in 2019 when the Micro Cap index was up 8.1% in the first seven trading days of 2021.

The chart below shows the performance of the Russell Micro Cap Index from the close on the seventh trading day of the year through year-end. For all years since 2007, the Russell Micro Cap index has seen a median gain of 11.62% for the remainder of the year with gains 64% of the time. While it’s a very small sample size, in the three prior years where the Micro Cap Index was up over 3% to start the year, the index continued higher for the remainder of the year with gains all three times ranging from 11.9% up to 38.5%.

November JOLTS: Questions & Answers

Today the Bureau of Labor Statistics updated its monthly Job Openings & Labor Turnover Survey (JOLTS). November’s data showed an uptick in layoffs and firings from a record low rate earlier in the fall. While that was some bad news, hiring has been accelerating. Private sector gross hiring was 4.5% of the labor force in August, and it’s now up to 4.7% in November. That’s a record pace of new hires for any period in the history of the series other than the immediate bounce-back from the initial COVID shock this spring. As for job openings, openings have stabilized a ways below their peak from the last cycle. So while there are lots of layoffs, the story is less negative than it might sound. Like what you see? Click here for a free trial to any of Bespoke’s premium membership options, including our nightly Closer note that regularly features economic analysis of this kind.

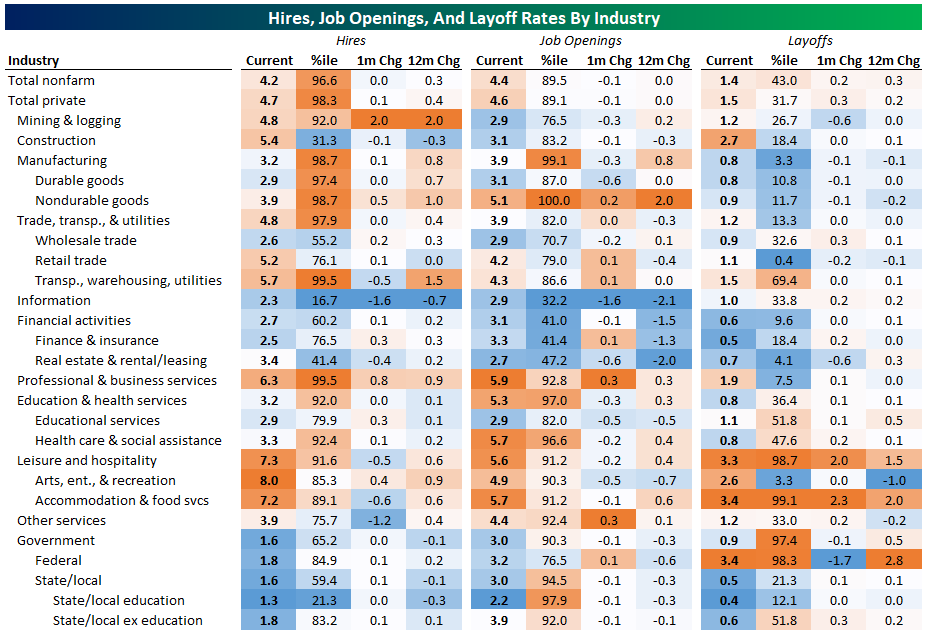

Another interesting dynamic in the JOLTS data is the industry-level results. Hires are strongest versus history in areas that you might expect given the impact of COVID: manufacturing, transportation/warehousing/utilities. Some surprising areas are very weak though: construction and information stand out. As for COVID impacts, you wouldn’t expect strong hires in accommodation and food services, but there they are. Job openings are the highest relative to history in manufacturing but are also extremely high in accommodation & food services as well as state and local education. Finally, we note that layoffs are basically consistent with COVID-driven weakness, plus the effects of Census hiring rolling off for the Federal government.