Facebook (FB) and Tesla (TSLA) Set for 5%+ Gaps Higher on Earnings

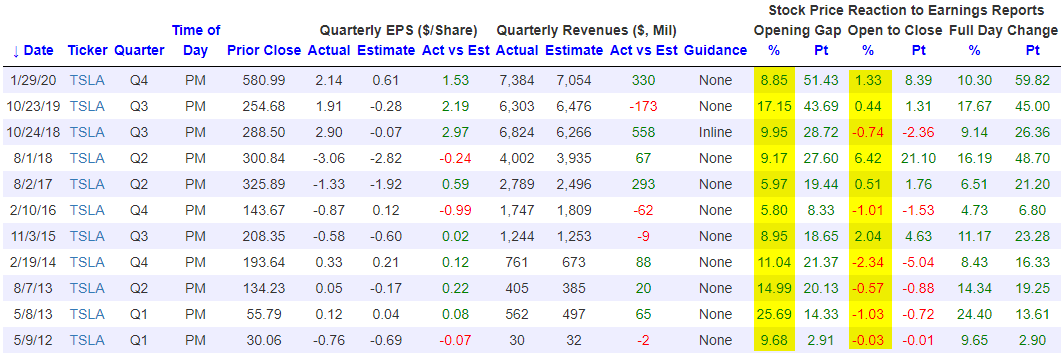

Our popular Earnings Explorer tool has quarterly earnings results and share price reactions to those earnings reports for nearly every US stock going back to 2001. The database is online, massive, and it’s interactive so that users can quickly look up historical results for individual companies. One way to use the database is to see how stocks that are set to experience huge opens higher on earnings typically trade from the open to the close of trading after their initial moves higher. Two stocks that are set to gap up sharply on earnings this morning are Facebook (FB) and Tesla (TSLA). At the moment, both are set to open higher by more than 5%.

Below we have pulled all historical instances in which both Facebook and Tesla have gapped higher by at least 5% at the open of trading following quarterly earnings reports. Coincidentally, each stock has had 11 prior gaps up of 5%+ on earnings in their history as public companies. For Facebook (FB), when it has gapped up 5%+ in the past, it has actually traded lower from the open to the close 7 of 11 times for an average open to close change of -0.91%. This tells us that at least in the past, investors have more often than not used these opportunities to lighten up on shares during the regular trading day.

For Tesla (TSLA), when it has gapped up 5%+ on earnings, the stock has also traded down from the open to the close more often than it has traded up from the open to the close, but its average open to close change on these 11 prior gaps higher has been positive at +0.46%. We’d note that this will be the third quarter in a row that TSLA has opened higher by 5%+ on earnings, and the prior two quarters saw a slight positive move from the open to the close for the stock. If you’d like to test out our Earnings Explorer tool to see how your stocks typically trade on earnings, start a two-week free trial to Bespoke Institutional. You’ll also gain access to our entire platform that includes our most actionable research reports and our full suite of investor tools.

50-DMAs in the Rearview

Stocks have continued to rally this week and for many individual names, these gains have lifted them above their 50-DMAs. As shown in the chart below, over three quarters of stocks in the S&P 500 have now moved back above their 50-DMAs. Three sectors—Technology, Communication Services, and Health Care—have more than 90% of their stocks above their 50-DMAs with Health Care leading the way at 96.7%. Readings above 90% are very rare — just as rare as the sub-10% readings we saw in March. As for the other sectors, similar to the S&P 500, Consumer Staples, Consumer Discretionary, and Materials all have over three-quarters of their stocks above their 50-DMAs. Meanwhile, Financials, Industrials, and Energy are lagging somewhat but still have more than half of their stocks above. The only two sectors that are truly lagging with just 32.1% and 38.7% above, respectively, are Utilities and Real Estate — two defensives.

Health Care and to a lesser degree Consumer Staples were the first sectors to see a large number of stocks trade above their 50-DMAs. This reading for both sectors saw a more gradual build throughout April. As for the rest, the percentage of stocks trading above their 50-DMAs has exploded higher and in a much more rapid fashion, especially within the past week. In fact, as recently as last Thursday, excluding Health Care and Consumer Staples, the highest reading across sectors was only 40.85% (Technology). The big pickup in the number of stocks moving above their 50-DMAs means two things. For starters, many stocks are clearing resistance at their averages which is a positive technical development. Second, many stocks are roughly around the same areas of their trading ranges and are moving higher together (strong breadth). Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

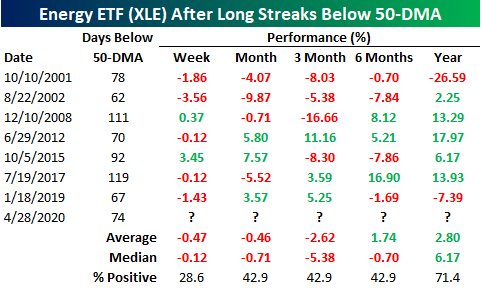

Energy (XLE) Finally Above Its 50-DMA

As we noted yesterday, more and more sectors have begun to cross back above their 50-DMAs in the last couple of weeks. With the outperformance of recent underperformers in yesterday’s session, the most beaten-down sector, Energy (XLE), finally managed to move back above its 50-DMA. Yesterday marked the first time that XLE had closed above its 50-DMA since January 10th. As for today, XLE is poised to gap up over 3% at the open bringing it further above its 50-DMA.

With XLE being under its 50-DMA for nearly four full months, that streak ending at 74 trading days was the fifth-longest in the ETF’s history. The last time XLE experienced a similar streak was in 2017 which was actually the longest streak on record ending at 119 days. The other longer streaks came in 2015, 2008, and in 2001.

As for performance after these long streaks below the 50-DMA come to an end, XLE has typically been pretty weak. In the table below, we look at all prior streaks below the 50-DMA that lasted for at least 60 trading days (roughly three months). One week after such streaks come to an end has only seen XLE higher around a quarter of the time with an average decline of 0.47%. Returns have also been positive less than half of the time one, three, and six months later. Fortunately, one year later XLE has been higher 71.4% of the time with an average gain of 2.8% (median 6.17%), although even here, those returns are nothing to get overly excited about. Start a two-week free trial to Bespoke Institutional to access our full range of research and interactive tools.

Historically Bad GDP For Q1 As Services Suffer

This morning the BEA released one of the worst GDP numbers in the modern history of the US economy. Total output fell 4.79% at annual rates, worse than the 4.0% decline (again, at annual rates) that economists had forecasted. That’s not as bad as the worst numbers from the financial crisis, but the details under the hood were qualitatively different. Instead of being led down by falling capital expenditures and gradually decelerating consumption, Q1 saw an outright collapse in services and durable goods spending with large but historically less remarkable declines in business spending. Services spending has been the steady Eddie of US growth for the better part of a century now: it’s never contributed more than an 82 bps headwind to total QoQ SAAR growth since World War 2. But in Q1 it was a 5% headwind, almost an order of magnitude more than its worst quarter in the global financial crisis. We outline the sobering numbers in more detail below. Start a two-week free trial to Bespoke Institutional to access our Chart Scanner, custom screens, and much more.

Outperformers Underperform

This morning, we highlighted the recent performance of sector ETFs noting how Health Care has led the way higher rising the furthest above its 50-DMA. Consumer Discretionary (XLY), Technology (XLK), Materials (XLB), Communication Services (XLC), and Consumer Staples (XLP) each had also risen above their 50-DMAs. Given their outperformance, as shown in the table below, headed into today these were the sectors closest to their levels on the S&P 500’s last all time high on February 19th. The Health Care ETF (XLV) actually headed into today less than 2% away from its 2/19 levels and XLP was also under 10% away.

Today, that performance was turned on its head as some of the sectors that have been playing catch up outperformed while those that have been the outperformers recently underperformed. Whereas it has typically been the strongest sector, Health Care (XLV) actually fell the most dropping ~2%. On the other hand, Energy (XLE) rose over 2.1% and it even finally rose above its 50-DMA. Other areas of strength today included Financials, Industrials, and Materials which all finished up over 1%. Recent winners were the losers today while the recent laggards were today’s winners. Start a two-week free trial to Bespoke Institutional to access our full range or research and interactive tools.

Who Is Now Overbought?

Over the past couple of weeks, as equities have mean reverted, the vast majority of S&P 500 stocks have moved out of oversold territory. In fact, today there are just two stocks that are oversold: Everest (RE) and Southwest Airlines (LUV). Meanwhile, more and more stocks have gotten extended above their 50-DMAs. At the moment, there are around 16% of stocks in the S&P 500 that are overbought. That is certainly not a large amount of the index, but it is the most we have seen in some time now.

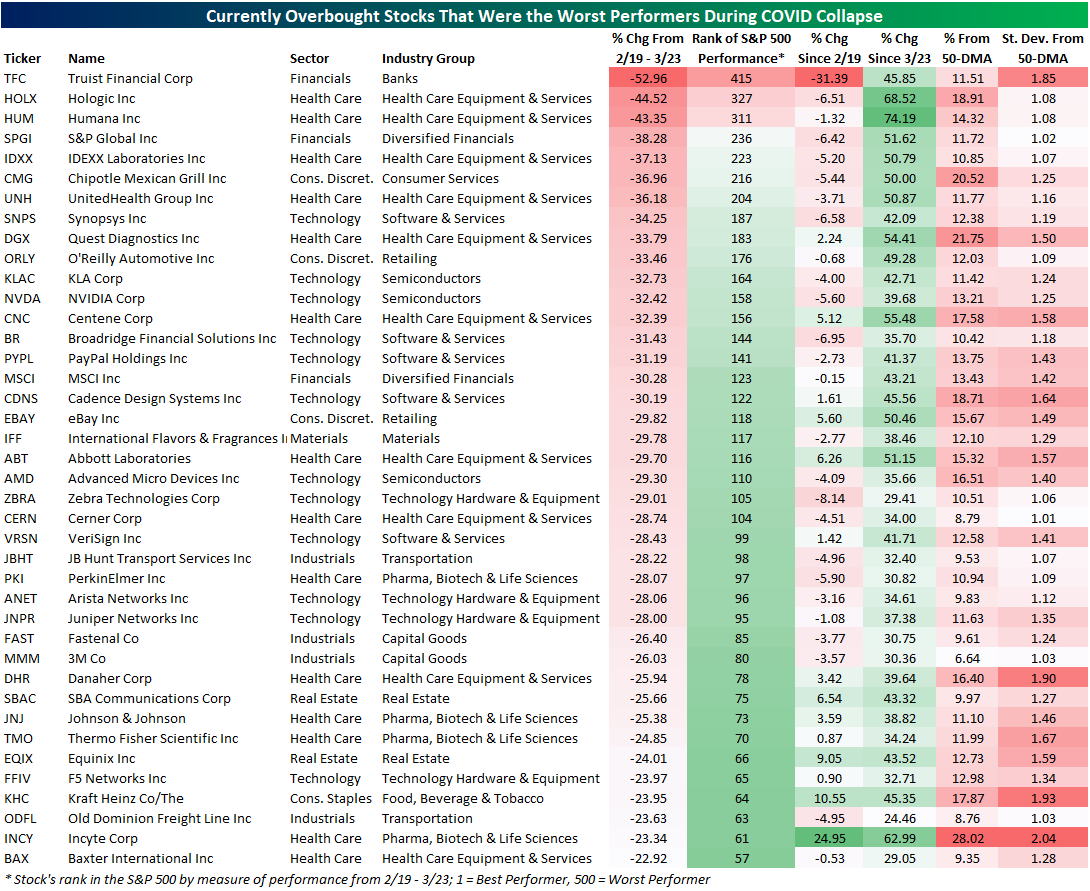

Taking a look across the stocks that are currently overbought, very few of them were those that had gotten hit the hardest from the February 19th peak to the March 23rd low. In fact, of the 100 worst performing S&P 500 stocks in that period, there is only one that is overbought, Truist Financial (TFC), and there are only twelve (including TFC) that have retaken their 50-DMAs. Currently, the median distance from the 50-DMA of those 100 worst performers from 2/19 through 3/23 is 9.31% below their 50-DMA. In other words, the hardest hit stocks during the worst of the sell off have still yet to completely mean revert (more specifically, move back to their 50-day average).

As for the stocks that have mean reverted and are now looking a bit extended (at least 1 standard deviation above their 50-DMAs), most were of the better performing half of the S&P 500. In the table below, we show the 40 names that were hit the hardest during the sell off from 2/19 through 3/23 out of the 77 S&P 500 stocks that are currently overbought. While these are the worst hit of the currently overbought stocks, most of these were actually some of the strongest performers of the broader S&P 500 during the sell off though that does not mean they were totally immune from massive declines. For example, 17 of these stocks were in the top 100 best performers during the sell off. On the other hand, only three stocks, Truist Financial (TFC), Hologic (HOLX), and Humana (HUM) were in the bottom performing half of the index during the sell off. The massive rebounds that these names have staged has led them to their current overbought levels. Overall, due to the size of the massive declines in February and March, the hardest hit stocks in the S&P 500 have rallied considerably but have not yet reached overbought territory so much as even retaken their 50-DMAs. That means that many of the least hard hit stocks are the ones that have first reached and are currently sitting in overbought territory. Start a two-week free trial to Bespoke Institutional to access our full range of research and much more.

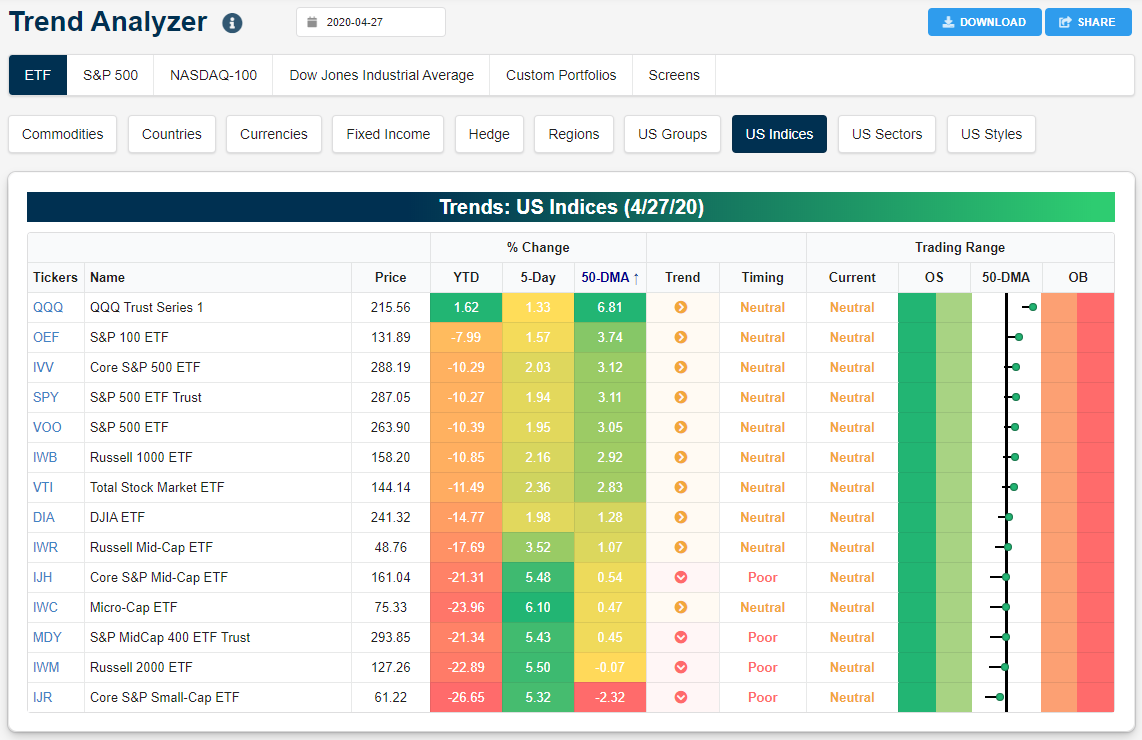

More and More Equity Market ETFs Back Above Their 50-DMAs

It hasn’t been talked about much but the Nasdaq 100 (QQQ) remains up on a year-to-date basis with a 2020 gain so far of 1.62%. Below is a snapshot of QQQ and other major US index ETFs run through our Trend Analyzer tool that’s available to Bespoke Premium and Bespoke Institutional members. Note that all but two of these index ETFs have now moved back above their 50-day moving averages, which often acts as a key support/resistance level. The Nasdaq 100 (QQQ) is the farthest above its 50-DMA at +6.81%, followed by the S&P 100 (OEF) and the three main S&P 500 ETFs (IVV, SPY, VOO). The Total Stock Market ETF (VTI) is 2.8% above its 50-DMA, while the mid-cap ETFs like IWR, IJH, and MDY are all just slightly above their 50-DMAs. While the Micro-Cap ETF (IWC) is above its 50-DMA, the two main small-cap ETFs (IWM, IJR) are the ones that remain slightly below. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

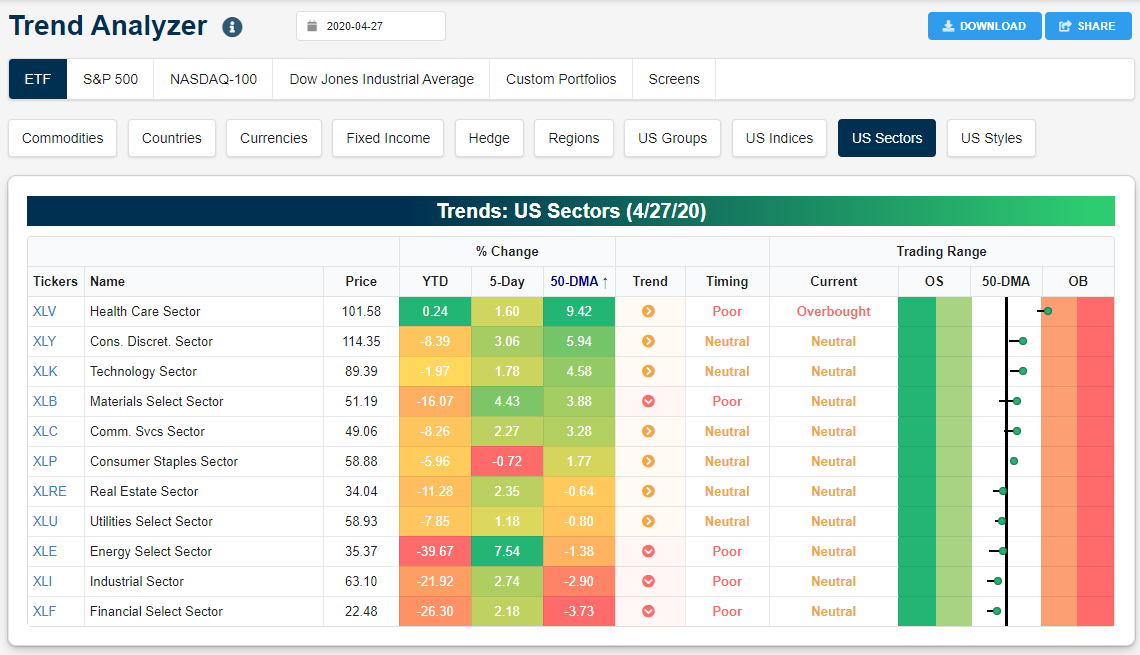

Below is a snapshot of the main S&P 500 sector ETFs from our Trend Analyzer tool. While almost all of the broad US index ETFs are back above their 50-DMAs, only six of eleven of the sector ETFs have re-taken them. The Health Care sector (XLV) is the farthest above its 50-DMA at +9.42%, and Health Care is the only sector that is now trading in overbought territory. It’s also the only sector that’s up year-to-date, similar to QQQ. Consumer Discretionary (XLY), Technology (XLK), Materials (XLB), Communication Services (XLC), and Consumer Staples (XLP) are the other five sectors above their 50-DMAs.

On the downside, the Energy sector (XLE) is no longer the farthest below its 50-DMA; that title now belongs to Financials (XLF) which is 3.73% below. The Industrials sector (XLI) is 2.9% below its 50-DMA, followed by Energy (XLE) at -1.38% and Utilities (XLU) at -0.80%.

While Health Care is up on the year, three sectors — Energy, Industrials, and Financials — are still down more than 20% year-to-date. Gain access to our Trend Analyzer tool and our daily investment research with a two-week free trial to Bespoke Premium.

Five Largest Market Caps Report This Week — AAPL, AMZN, FB, GOOG, MSFT

The earnings slate ramps up in a big way this week. Included in the 784 total companies reporting this week are the five largest stocks in the S&P 500. As shown below, Alphabet (GOOG) will kick things off tomorrow followed by Facebook (FB) and Microsoft (MSFT) on Wednesday and Amazon (AMZN) and Apple (AAPL) Thursday evening.

Our Earnings Explorer tool lets users conduct in-depth analysis of individual companies and how their share prices typically react to quarterly results. Below we highlight the ins and outs of quarterly earnings for the five largest stocks in the S&P 500 — all of which report Q1 results this week.

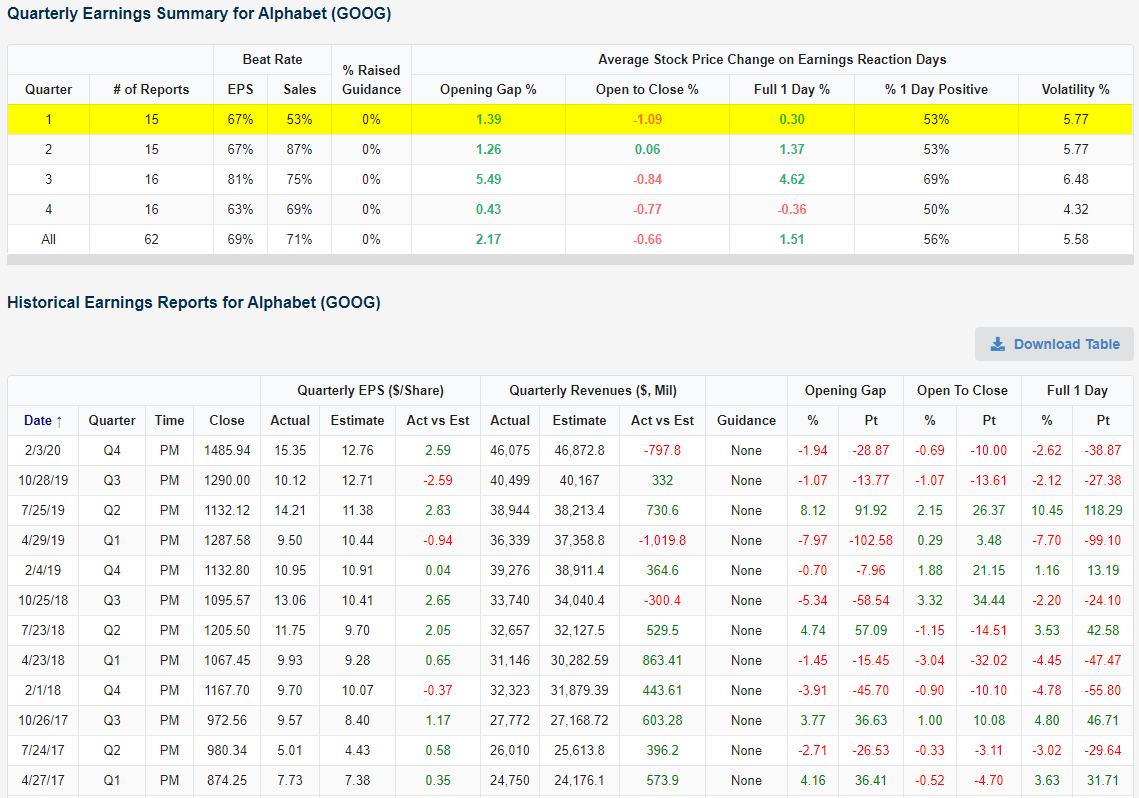

Below is a snapshot from our Earnings Explorer that shows how Alphabet’s (GOOG) share price has historically performed on its earnings reaction day. For GOOG’s Q1 earnings report specifically, the stock has historically averaged a small one-day gain of 0.30% in reaction to the news with positive returns just 53% of the time. Conversely, GOOG’s best earnings reports have come on its Q3 release where the stock has averaged a one-day gain of 4.62% in reaction to the news. For GOOG, the first quarter has also been the one that the company most often misses sales estimates.

As for Facebook (FB), which reports on Wednesday, historically the stock has beaten EPS estimates 94% of the time and sales estimates 90% of the time. In terms of share price reaction, FB has been a big winner on earnings with an average one-day gain of 2.7%. Looking at Q1 specifically, FB shares have averaged a gain of 3.38% on earnings reaction days with positive returns 57% of the time.

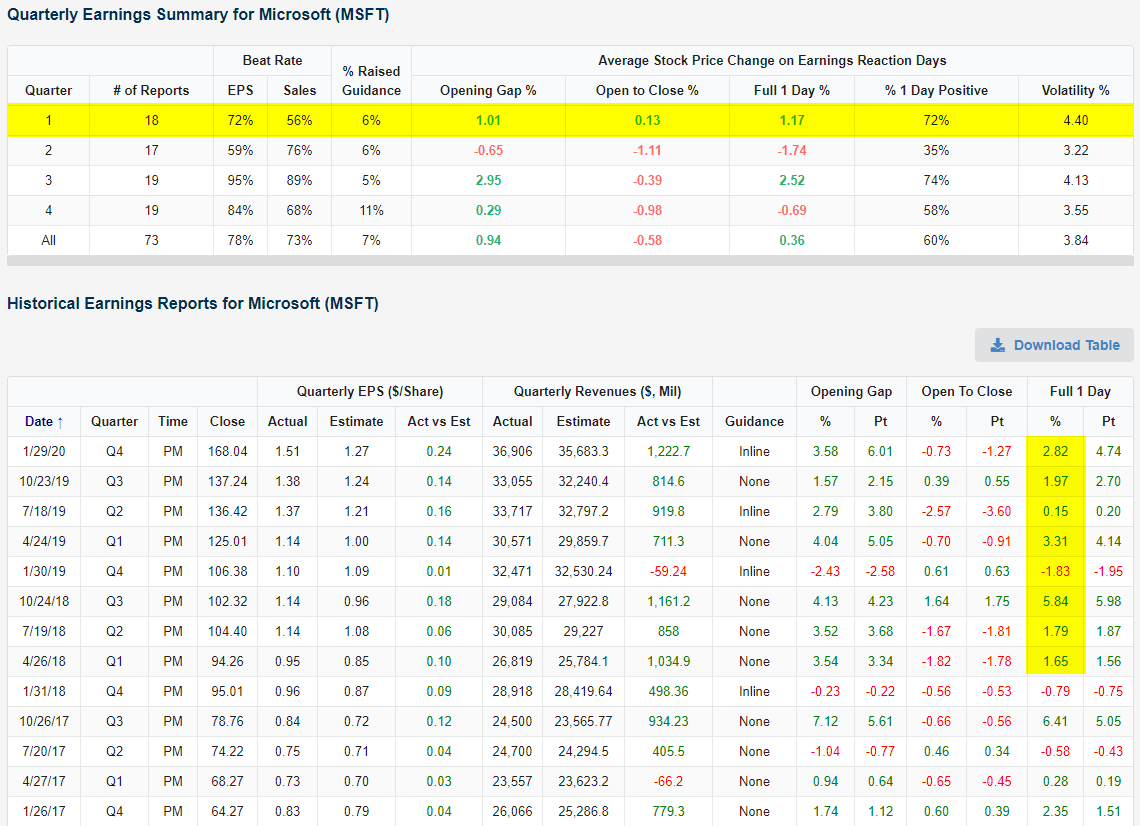

Microsoft (MSFT) heads into Q1 earnings as the largest stock (by market cap) in the S&P 500 and on a bit of a hot streak. As shown in the snapshot below, MSFT has seen gains on seven of its last eight earnings reaction days dating back to April 2018. On Q1 earnings days, MSFT has averaged a full day gain of 1.17% and has closed higher 72% of the time. Q3 is the only other quarter that has seen MSFT average gains on earnings reaction days. The worst quarter for MSFT earnings has historically been Q2 (reported in July). MSFT has averaged a decline of 1.74% on its Q2 earnings reaction days with positive returns only 35% of the time.

Amazon (AMZN) has been notable recently in that it managed to break out to fresh all time highs. With that strength at its back, AMZN heads into what is typically its strongest quarter in terms of share price reaction. Amazon has the highest sales and beat rates in the first quarter, and as a result, the strongest stock price reaction of any quarter. As shown below, AMZN has averaged a full day gain of 4.86% on Q1 earnings days compared to a 1.23% gain for all quarters. It has also been in the green around two-thirds of the time.

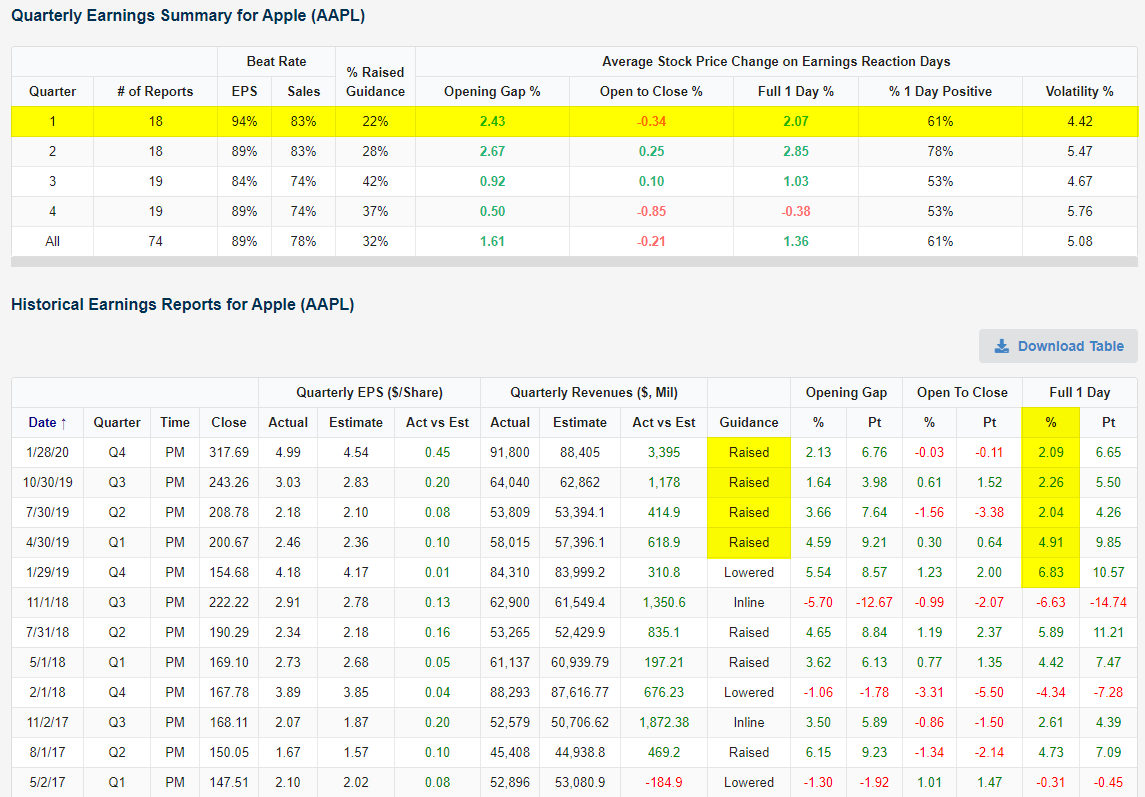

Like AMZN, Apple (AAPL) also heads into what has historically been one of its strongest quarters for earnings on a hot streak. The stock has risen on every earnings day of the past five quarters and Q1 earnings has been the second strongest for the stock with an average one-day gain of 2.07%. Additionally, every quarter of the past year has seen Apple report a triple play (EPS beat, sales beat, raised guidance). While nothing is out of the realm of possibilities, given the current environment’s impact on business, it is questionable if the company will keep up that streak of triple plays. For example, today it was reported that there will be delays in the new iPhone’s production. Regardless of whether or not the triple plays streak stays alive, AAPL has been seasonally strong in Q1, consistently beating EPS and sales estimates with the stock price reacting accordingly. Start a two-week free trial to Bespoke Institutional to access our interactive Earnings Explorer and much more.

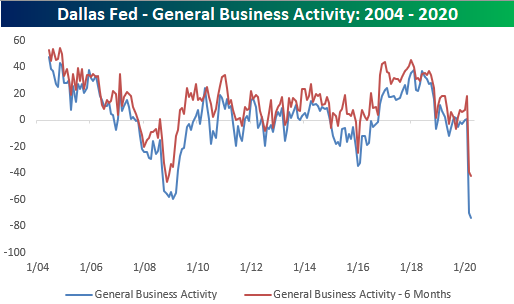

Another Regional Fed Record Low

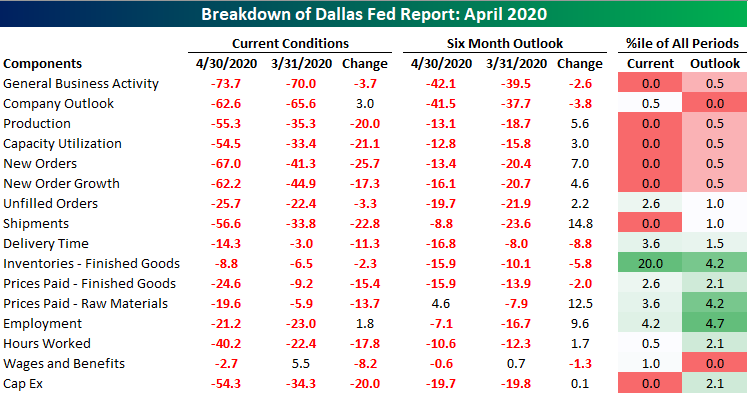

What an encore. Following the largest decline ever and a record low reading in the Dallas Fed’s Manufacturing index for March, April’s fared even worse as the headline index fell even further, dropping from -70 to -73. Although that is a new record low and far from a sign of good conditions in that region, it wasn’t as bad as the consensus reading of -75.

That thin silver lining aside, this month’s report was broadly weak. In addition to the headline number, the indices for current conditions on Production, Capacity Utilization, New Orders and New Order growth, and Shipments were all at their lowest levels ever (since 2004), and the six-month outlook indices for Company Outlook and Wages and Benefits were also both at record lows. As for the rest of the categories, if they were not at a record low they were close with most coming in at the 5th percentile or lower of all readings.

As we have frequently highlighted over the past month for other regional Fed indices, demand has been absolutely crushed. Each of the categories for demand like those for new and unfilled orders and shipments have completely collapsed. On the bright side, although they still remain low and the increases were small, there was a slight pickup in the outlook indices across these indicators in April.

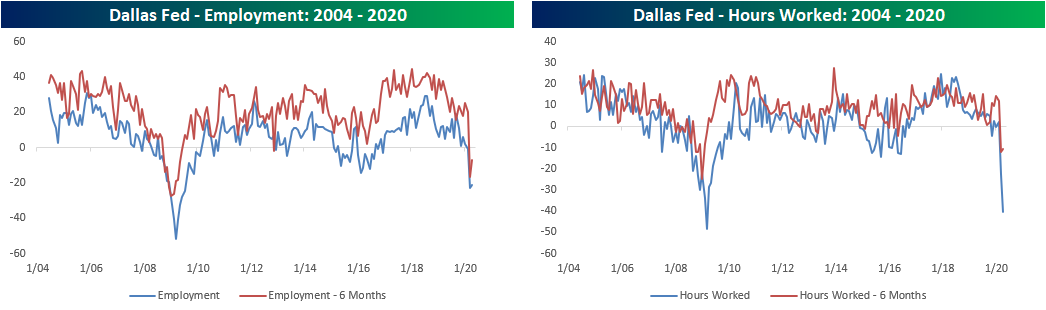

The same can also be said for the categories covering employment. Outlook six months ahead for Employment and Hours Worked both picked up in April. Albeit, these are still around some of their lowest levels since the global financial crisis, and the index for current hours worked continued to fall in April as shutdowns remain in place. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

The Smaller The Better

While lately it seems as though all anyone is talking about is the concentration of market cap in the largest stocks in the S&P 500, you may be surprised to hear that small caps have actually been leading the charge higher from the market lows. It’s been neck and neck, but while the S&P 500 is up just over 31% from its intraday March low, the Russell 2000 is up over 32%.

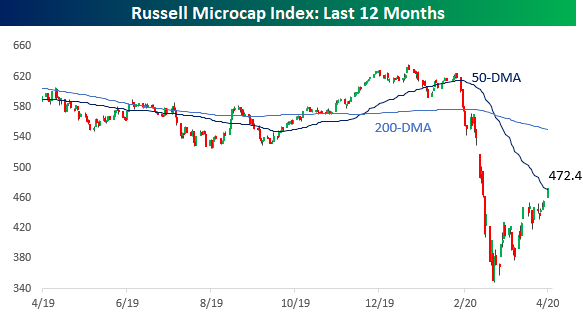

Granted, the Russell 2000 is only outperforming the S&P 500 by a slim margin, but it’s micro-cap stocks that have stolen the show. Since its low in March, the Russell Micro Cap Index is up 36% and actually back above its 50-day moving average for the first time since late February. The index is still down much more from its highs than either the Russell 2000 or the S&P 500 and the index’s entire market cap is only $365 billion (less than the market cap of Walmart WMT), but from the lows at least, micro-cap stocks have been on fire.

The last four days have been especially strong for the smallest of the small stocks as the Russell Micro Cap index has risen at least 1% on each of the last four trading days, including a 3.8% gain today. The Russell Micro Cap Index has only been around since 2006, but during that time there have only been two other periods where the index saw four straight days of 1%+ gains. The first was in late October 2008 while the second was in August 2009. Back in October 2008, if you chased micro-cap stocks after their four-day rally, the next few months were pretty painful, but the occurrence in August 2009 came in the early stages of the bull market. Receive full access to our research and commentary with a free two-week trial to Bespoke Premium.