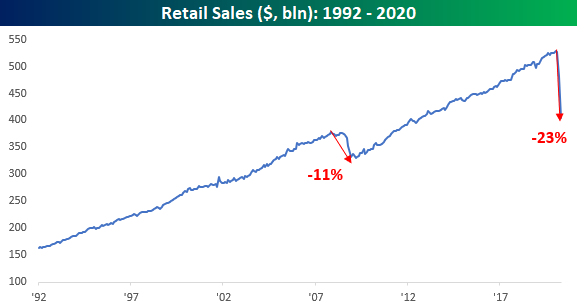

Retail Sales – R.I.P.

We were expecting the worst monthly report on record in today’s Retail Sales report for April, and the bar wasn’t set nearly low enough. While economists were forecasting a 12.% m/m decline in sales, the actual decline was much larger at 16.4%. Ex Autos and Ex Autos and Gas, the declines were even weaker. Not bad enough for you yet? Well, March’s report was also revised lower. To put the last two months in perspective, total retail sales have declined by more than 23%. That’s nearly a quarter of total sales!

Among individual sectors, the sharpest decline in sales has come from the Clothing sector. From its recent peak, the monthly rate of sales in this sector has declined by nearly 90%. Apparently, we’re becoming a nation of nudists!

For anyone with more than a passing interest in how the economic shutdown is impacting economic data, our monthly update on retail sales is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!

Breadth Picking Up But Still Low

With the S&P 500 range bound over the past couple of weeks, short term breadth has left something to be desired. So far in May less than half of trading days have seen a positive net number of advancing stocks in the S&P 500 . As such, and as we noted earlier this week, the 10-day advance/decline lines across sectors had broadly entered oversold territory this week. Some of the more beaten down sectors like Consumer Discretionary and Financials did so to a more extreme degree than other sectors. But yesterday’s intraday reversal higher marked the first day this week with positive breadth for the index which allowed the 10-day A/D lines of Communication Services, Energy, Utilities and the S&P 500 to exit oversold territory. Meanwhile breadth for Consumer Discretionary, Financials, Industrials, Materials, and Real Estate all remain pretty weak. Start a two-week free trial to Bespoke Institutional to access our Daily Sector Snapshot and much more.

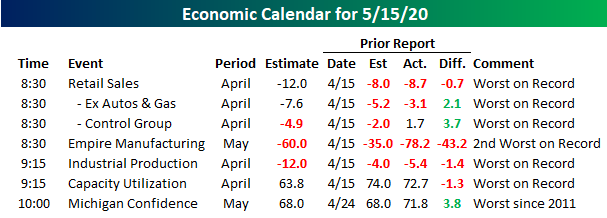

Ugliest Economic Data Day of All Time?

It has been a pretty quiet week of economic data so far, but the week closes out on a busy and what will ultimately be an ugly note. Reports on the calendar for tomorrow include Retail Sales, Industrial Production, and Capacity Utilization, which all cover the month of April. In addition to those reports, data for May includes Empire Manufacturing and preliminary Michigan Confidence. April was the peak period of the economic shutdowns, and the data will highlight that. Retail sales is expected to show its largest m/m declines on record (dating back to 1990), building on already weak readings from March. The history for Industrial Production goes all the way back to 1920, and even with 100 years of data (including the Great Depression), there has never been another month where it saw a larger m/m decline at least based on current estimates. Likewise, data for Capacity Utilization goes back to WWII, and that too will likely be the weakest on record. With all the weak hard data, it’s somewhat surprising to see that Michigan Confidence is only expected to fall to its lowest level since 2011. In any other time, a nine-year low reading in an economic indicator would be notable enough, but in the midst of a global pandemic, it’s peanuts. Start a free trial to Bespoke’s premium platform for full access to our stock market analysis and interactive tools.

Investors Remain On Guard

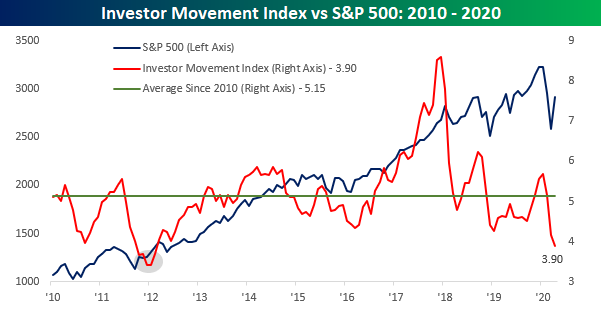

In a post earlier today, we noted that individual investors still remain overwhelmingly bearish despite the equity market’s rally off the March lows. Another sentiment indicator released by TD Ameritrade supports this view that investors aren’t particularly bullish right now. The TD Ameritrade Investor Movement Index is a proprietary, behavior-based index created by TD Ameritrade designed to indicate the sentiment of individual investors’ portfolios. It measures what investors are actually doing, and how they are actually positioned in the markets.

The TD Ameritrade Investor Movement Index has been in existence since 2010, and in that entire history there have only been five months where the index was weaker than it is now, and that was from October 2011 through February 2012. That was also a period that marked a major low in the equity market and was followed by a nearly uninterrupted three-year rally in the S&P 500.

While the Investor Movement Index is near record lows right now, it has been weak for some time, and that weakness came even as the S&P 500 was climbing to record highs over the last 12-18 months. In other words, while investors are just about as cautious as they have been at any time in the last ten years, this conservatism is nothing new. Start a two-week free trial to Bespoke Institutional for full access to our analysis and interactive tools.

Sentiment Still Sits Bearish

In last Thursday’s Chart of the Day, we noted that for the first time in a decade less than a quarter of respondents were bullish or neutral while over half were bearish. Although that isn’t exactly the case again this week, sentiment still leans heavily bearish. Bullish sentiment dropped down further to 23.31% from 23.67% last week. That is the lowest level of bullish sentiment since the COVID-19 pandemic began and the lowest number since last October when the percentage of investors reporting as bullish bottomed out at 20.31%.

The move out of the bullish camp didn’t exactly flow into the bearish camp, though. Bearish sentiment likewise fell slightly this week from 52.66% to 50.61%. Although that is slightly lower, the majority of those surveyed are still bearish.

Simply put, bearish sentiment has been high for a long time. Of the previously mentioned past ten weeks, even if bearish sentiment was not above 50% it was at least one standard deviation above its historical average. That now ranks as the longest streak since 2008 (14 weeks) and the fourth-longest in the history of the survey daying back to 1987.

With such a large divergence between bulls and bears, the bull-bear spread now stands at -27.3 which is slightly better than the -28.99 reading last week but still clearly at the low end of the past decade’s readings. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Sixth Straight Decline In Claims

This week was another ugly one for jobless claims, although the weekly trend is moving in the right direction. While the 2.981 million print was significantly higher than estimates of 2.5 million, this week marked the sixth in a row that claims were down week-over-week. This week also marked the first sub-3 million print and the lowest number since claims first spiked in the week ending March 20th. While the slowed pace of claims is an improvement, this was a smaller WoW decline compared to the past several weeks. Additionally, with another 2.981 million added this week, the grand total of jobless claims since that March 20th print now sits at nearly 36.5 million, or roughly 11% of the entire US population.

As shown in the chart below, the streak of WoW declines over the past six weeks is now tied for the second longest such streak on record. Back in 2016, 2009, 1994, and 1993 were the last times that claims had fallen for six straight weeks, and there have only been two other periods where claims fell for longer: 2013 and another in 1980. Both of those streaks ended at seven weeks.

As for non-seasonally adjusted claims the same story holds true. The drop to 2.614 million this week was the fifth consecutive weekly decline and the lowest print since the initial spike in claims in late March.

With another lower print, the four-week moving average has also continued to decline. That measure has now declined for three straight weeks to its current level of 3.617 million. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

The Trump-Tepper One-Two Punch

What started out as a weak open for equities today started to show improvement early on. Just an hour after the open the S&P 500 was even up for a few minutes, but then the President sent out a tweet where he argued that “dealing with China is a very expensive thing to do.” He then went on to say that “100 Trade Deals wouldn’t make up the difference” for the “Plague from China.” The timing of this tweet was especially concerning as it comes just two days before the expiration of a 90-day enforcement provision of the trade deal on Friday. With that tweet, the equity market’s rally was stopped dead in its tracks as the S&P 500 sold-off for the rest of the morning.

By noon, the market was attempting to bounce, but then David Tepper came on CNBC to say that the current market was one of the most overvalued he has ever seen. That stopped any chance of a rebound and within minutes, the S&P 500 was at its lows of the day. Ever since then, the market has been trading sideways all afternoon, but with 45 minutes left in the trading day, we’ll see if those lunchtime lows can hold. Between Druckenmiller after the close yesterday, Trump this morning, and then Tepper at lunch, you can’t fault the market for acting a little punch drunk. Start a two-week free trial to Bespoke Institutional for full access to our research and interactive tools.

Bull Flag For Gold (GLD)

Over the past year and a half, gold has been on the up and up though it was interrupted by the string of volatility from the recent Covid crash across asset classes. In the past few months, the SPDR Gold Trust ETF (GLD) fell 12.5% from its March 9th high to March 19th low, which was followed by an 18.33% rally off that low to its last closing high on April 23rd.

Since its April high, GLD has been consolidating with a set of higher lows and lower highs between roughly $158 and $163. This is a flag pattern that suggests a breakout is coming either to the upside or the downside. For now it’s closer to breaking out to the upside as it tests the top end of the flag’s range. Start a two-week free trial to Bespoke’s premium research platform to access a full range of equity analysis and interactive tools.

Reversal to Neutral

Currently, the only two sectors that are trading in overbought territory (1+ standard deviations above its 50-DMA) in our Trend Analyzer are Technology and Communication Services. Meanwhile, Financials, Industrials, Utilities and Real Estate are all closer to oversold territory than overbought without any of those sectors yet to have even moved above their 50-DMAs.

As for short-term breadth levels as measured by the 10-day advance/decline line, as shown in the charts from our Daily Sector Snapshot below, those same sectors in addition to Consumer Discretionary and Materials have actually begun to touch oversold levels after the late day reversal lower yesterday and a lack of a push higher with lackluster breadth over the prior few days.

Even the sectors that have been market leaders like Health Care, Communication Services, and Tech have more neutral 10-day A/D line readings at the moment even with prices at or near overbought levels. Start a two-week free trial to Bespoke Institutional to access our Daily and Weekly Sector Snapshots and much more.

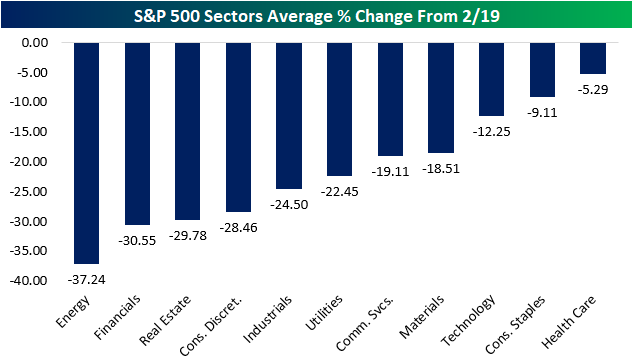

Some Stocks Moving Above February Highs

In last night’s Closer, we noted that as of yesterday’s close, the S&P 500 (SPY) sat over 15% away from its 2/19 all time high. But as for the index’s individual stocks, about 12.4% have retaken their 2/19 levels. As shown in the chart below, Health Care sector stocks on average are the closest at 5.29% below their levels on 2/19. Consumer Staples are the only other stocks that are less than 10% away from those levels on an average basis. Conversely, Energy, Financials, and Real Estate have the furthest to go, all down around 30% or more.

Meanwhile taking a look across industries, there is only one group of stocks that’s currently above its 2/19 levels on an average basis: Pharmaceuticals, Biotechnology, & Life Sciences. While stocks of that industry have pushed above by 1.2% on average, the other groups are not even close with the next closest to doing so being Food & Staples Retailing at 7.6% below 2/19 levels. In addition to Food & Staples Retailing, Food, Beverage, & Tobacco, and Health Care Equipment & Services are the only others that are even within 10% away. On the other end of the spectrum, Banks, Energy, and Consumer Durables & Apparel are down the most.

Those same dynamics can be seen in the table below of the stocks furthest above and below their 2/19 levels. While Health Care stocks like Dexcom (DXCM) and Regeneron (REGN) have surged over 40% since 2/19, some of the biggest losers during the sell off remain beaten down. Of the 20 stocks that are furthest below their 2/19 levels, most have something to do with oil, planes, cruises, or retail stores. Start a two-week free trial to Bespoke Institutional to access our Closer and much more.