Bespoke’s Morning Lineup – 9/21/20 – No Joy in Marketville

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“I want to put a ding in the universe.” – Steve Jobs

2020 has put more than a ding into the universe, and just when you thought things can’t get any more complicated, the world received news Friday night regarding the death of the iconic Supreme Court Justice Ruth Bader Ginsburg. From a purely political perspective, what already promised to be one of if not the craziest, and most politically charged election cycles of our lifetimes only heated up more. Add to that a resurgence of the COVID outbreak in Europe, and it’s looking like another typical September week of declines.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, discussion of the political ramifications of the upcoming SCOTUS fight, trends related to the COVID-19 outbreak, and much more.

The S&P 500 is poised to open down about 1.5% this morning, and below we have summarized the typical performance of SPY from the open to close following downside gaps of 1% or more. On the 64 days since 1994, that these downside gaps have occurred on a Monday, SPY’s median performance from the opening to closing bell has been a gain of 0.02% with positive returns half of the time. In other words, it’s basically a coinflip.

Bespoke Brunch Reads: 9/20/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

California

CME Group to Launch First-Ever Water Futures Based on Nasdaq Veles California Water Index (Nasdaq)

This week the CME Group announced a new futures contract based on the price of water based on the prices traded in California’s five most-active spot water markets. [Link; soft paywall]

California’s wildfires are producing more CO2 than its power plants by Tim McDonnell (Quartz)

In a grim example of the positive feedback loops climate change can create, wildfires on the West Coast have created a larger release of carbon this year than electricity generation in the state for the year. [Link; paywall]

Wacky Wall Street

Citigroup Employee Who Operated QAnon Website on Leave by William Turton and Jennifer Surane (Bloomberg)

A senior IT group manager at Citi was suspended this week when his operation of major sites dedicated to spreading the QAnon conspiracy emerged. [Link; soft paywall]

Reddit’s Stock Threads Become a Must-Read on Wall Street by Sarah Ponczek (Bloomberg)

As frenetic retail trading has become increasingly important on Wall Street, professional investors are increasingly noting what happens on message boards and social media. [Link; soft paywall]

Eating Out

As Demand For Travis Scott Burgers Soars, Some McDonald’s Locations Run Out Of Beef (Restaurant Business)

A punched-up quarter-pounder, fries with barbecue sauce, and a Sprite…not much, but slap some internet celebrity on it and the whole thing has wrecked the MCD supply chain. [Link]

National Restaurant Association report: Pandemic has forced 100,000 restaurant closures in six months by Nancy Luna (Nation’s Restaurant News)

A new survey shows that more than 100,000 restaurants have closed in the last six months, with one in six establishments across the country shuttering; another 40% of operators report they cannot stay open without further relief. [Link]

COVID Leisure

Demand for ‘certified used’ bikes is so strong, some sell above new sticker price by Ethan Wolff-Mann (Yahoo! Finance)

With surging enthusiasm for bikes that can provide safe leisure time amidst the pandemic, second-hand providers are incentivizing new supply…and some customers may be over-paying. [Link; auto-playing video]

Golf and the virus by Myles Udland (I’m Late to This)

Golf’s popularity amidst the pandemic is forcing some very difficult questions about who exactly the golf industry is selling to and why that’s probably not most people. [Link]

Amazon

Amazon Plans to Put 1,000 Warehouses in Neighborhoods by Spencer Soper (Bloomberg/MSN)

With the Everything Store trying to shrink delivery times ever-narrower, expect a lot more logistics close to where customers are, including thousands of new warehouses on the front lines of American consumerism. [Link]

Give It Away

Exclusive: The Billionaire Who Wanted To Die Broke . . . Is Now Officially Broke by Steven Bertoni (Forbes)

The cofounder of Duty Free Shoppers never led an extravagant life, but his effort to give away his fortune is most certainly impressive, painting a stark contrast to other members of the 10 figure club. [Link]

Public Policy

Racial Disparities in the Massachusetts Criminal System by Elizabeth Tsai Bishop, Brook Hopkins, Chijindu Obiofuma, Felix Owusu (Harvard Law School Criminal Justice Policy Program)

A data-first approach to identifying racial inequality in the Massachusetts court system, concluding that differences in the severity of initial charges explains why Black and Latinx defendants have longer sentences; the effect is especially large for drug and weapons charges. [Link; 103 page PDF]

A Bizarre Argument About the COVID Economic Response by Matt Bruenig (People’s Policy Project)

Bespoke’s work has argued in the past that the CARES Act was broadly generous to households and to a lesser extent small businesses, giving out grants to those groups while larger businesses got loans which had to be repaid. But misunderstanding of basic mechanics is leading to a strange argument that loans requiring repayment are somehow more valuable than cash transfers. [Link]

Silver Linings

The southern hemisphere skipped flu season in 2020 (The Economist)

In the Southern Hemisphere, flu season peaks between May and August, but this year there have been barely any cases as efforts to prevent COVID transmission also break flu virus transmission chains. [Link]

Frauds

Nikola (NKLA) admits to faking video of driving prototype in weak response to allegations by Fred Lambert (Electrek)

After a short-seller claimed last week that electric truck company Nikola had engaged in fraudulent behavior, the company delivered a lackluster response that seemed to confirm a number of the allegations. [Link]

Tattooed by Bill Gross (William H Gross)

Without any endorsement, we can’t resist passing on this screed of complaint about a son’s tattoo not-so-well-disguised as an investment letter. [Link; 3 page PDF]

I Want To Believe

Potential sign of alien life detected on inhospitable Venus by Will Dunham (Reuters)

Phosphine gas is only produced by biological life on our planet, which makes its discovery on Venus fascinating; it could signal microbial life even though the planet is widely assume to be unlivable. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

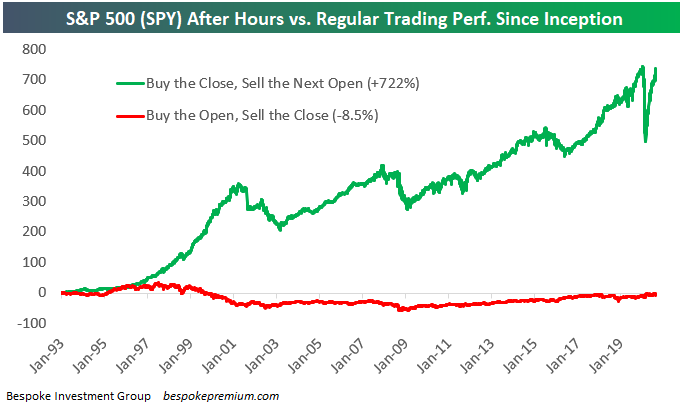

Intraday Selling

One of the more remarkable stats you’ll ever see is the breakdown of long-term performance between after-hours and intraday trading. Using the S&P 500 tracking ETF (SPY) that began trading in 1993, we can see how much of the S&P’s gains over the years have come outside of regular trading hours versus during regular trading hours. As any investor that follows the market closely knows, the S&P doesn’t open the next day at the same level that it closed the prior day. That’s because the futures market that trades outside of the regular 9:30 AM ET to 4 PM ET drives index levels. Positive news that occurs any time after the 4 PM close or before the 9:30 AM open gets priced into S&P futures as do ETF prices that trade after hours. When SPY officially opens for trading at 9:30 AM ET, it will “gap higher” to levels it was trading at in the pre-market. If bad news has S&P futures trading lower after hours, SPY will “gap down” and open lower at 9:30 AM.

The “After Hours” trade represents the initial “gap” that occurs between the prior day’s official closing price and the current day’s official opening price. Conversely, the move during “Regular Trading” — or intraday — represents the change from that day’s official opening price at 9:30 AM and that day’s official closing price at 4 PM. By combining the moves during After Hours and Regular Trading, you get the full-day’s change from the prior day’s close to that day’s close. The full-day change is the normal daily percentage move that you see quoted when you’re looking at price changes on whichever financial media tools you use.

Now that we’ve explained the difference between After Hours and Regular Trading, let’s take a look at how the two strategies have performed since SPY began trading back in 1993. To calculate the two performance numbers, we run two strategies — one that buys SPY at the close every day and then sells it at the next day’s open (After Hours), and another that buys SPY at the open every day and then sells it at that day’s close (Regular Trading). Had you only invested in the After Hours strategy by buying the close and selling the next open, you’d be sitting on a solid gain of 722%. Had you done the opposite, however, and only invested in the Regular Trading strategy by buying at the open and selling at the close, you’d actually be down 8.5%. That’s right — if you only owned the US stock market during regular trading hours going back to 1993, you’d be sitting on a decline right now in September 2020. This stat shows that more than 100% of the S&P’s gains since 1993 have actually come outside of regular trading hours. For anyone trying to make a living doing intraday trading, it’s certainly a tough game!

The reason we’re bringing up the After Hours versus Regular Trading strategies now is because we’ve seen some big moves in the two so far this year.

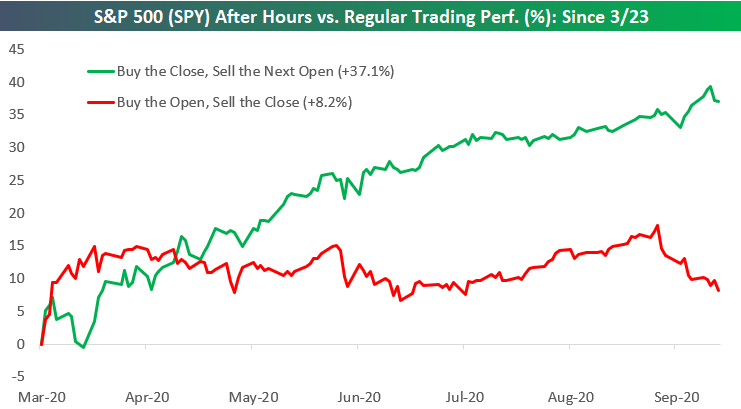

When COVID first hit, the After Hours strategy — which has historically been the winner — plummeted as futures markets seemingly tanked every day resulting in SPY “gapping down” sharply each morning. At the same time, the Regular Trading strategy was holding up remarkably well. Once the initial negative reaction occurred at the open back in February and March, investors stepped in to buy the market throughout the trading day. As shown below, at one point in late March when the S&P was down more than 30% year-to-date, had you only owned during Regular Trading hours, you would have actually been up on the year.

The two strategies have been converging lately, however. Since late August, the After Hours strategy has actually been performing well, meaning SPY has been gapping up in the morning most of the time. But during regular trading hours, investors have been selling. This new trend of gaps up at the open followed by intraday selling began on August 27th. Since then, had you bought SPY at the close every day and sold at the next open, you’d be up 2.3%. Had you done the opposite and bought at the open every morning and sold at that day’s close, you’d be down 7.1%.

After the recent action, the difference in 2020 between the After Hours strategy and the Regular Trading strategy is minimal. The After Hours strategy is only down 1.1% on the year while the Regular Trading strategy is up 3.9%. We know that the After Hours strategy has won out over the long term, and after dipping way in the hole earlier in the year, it’s getting closer and closer to taking the lead in 2020 as well.

Generally speaking, we don’t like to see gaps higher at the open that are sold off intraday, but that’s what has been happening during the month of September. We know that September has historically been the worst month of the year, and it’s a month that is usually volatile as well. Given the recent action, it’s not the most positive backdrop for the weeks ahead. Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.

Seasonal Volatility Just Getting Started

The market’s day-to-day volatility has picked up in September after experiencing more stable trading action during the summer months. This is not out of the ordinary. Historically, the most volatile time of the year for stocks has been between September and early November. You can see this in the chart below that shows the average absolute daily percentage change for each trading day of the year beginning on the first trading day of January through the last trading day of December. As shown, daily volatility is very consistent around the +/-0.70% level over the first eight months of the year, but then it starts to pick up beginning in September until it reaches a peak during the first week or two of November. From there, the holiday season takes over and daily volatility plummets right through the end of the year. As shown in the chart, unfortunately we’ve still got a ways to go to get to the top of the volatility mountain, so make sure you’ve got your climbing gear ready for the next six to eight weeks! Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.

No Love for Triple Plays

Long-term readers of Bespoke know that we follow closely stocks that report earnings triple plays. An earnings triple play occurs when a company releases quarterly numbers that 1) beat consensus EPS estimates, 2) beat consensus sales estimates, and 3) raise forward guidance. Go check out the definition of a “triple play” on Investopedia.com (which they’ve given us credit for) if you’d like to read more.

An earnings triple play is usually met with significant buying from investors. Our Earnings Explorer tool contains the quarterly results of nearly every US stock that has reported earnings over the last twenty years. At the tool — which is available to Bespoke Institutional members — users can filter the entire database to find all historical earnings triple plays that have occurred since 2000. We used the tool to find all triple plays over the last ten years, and the summary results from the tool are provided in the snapshot below.

As shown, there have been 4,914 earnings triple plays in the US over the last ten years. On average, these triple plays have seen their share prices rise by 5.63% on their earnings reaction days (the first trading day following the triple play). That’s a significant one-day gain, but it’s also commensurate with the strong earnings report that accompanied it.

The reason we’re bringing up earnings triple plays and their normal upside price reaction is because the ones we’ve seen so far in September have come up woefully short. So far this month, there have been twelve earnings triple plays, and these stocks have averaged a one-day decline of 3.26% on their earnings reaction days. Remember, usually triple plays see a gain of more than 5% on their earnings reaction days. This month, not only are triple plays not averaging gains…they’re actually selling off sharply.

Below is a snapshot of the twelve earnings triple plays we’ve seen this month. You’ll notice that quite a few are some of the most well-known high-fliers of 2020 like DocuSign (DOCU), Peloton (PTON), Chewy (CHWY), and CrowdStrike (CRWD). None of these four managed to post gains in reaction to their earnings triple plays.

From the looks of it, it appears that a lot of the upside earnings strength that companies are showing is already priced into shares before the actual news hits the tape. Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.

Keeping Tabs On High Frequency Growth

The week ended September 11th showed a sharp decline in our index of weekly GDP versus the year before. As shown, our index can be quite volatile, but it does do a decent job tracking the general trajectory of GDP. Since peaking at an implied growth rate of +0.9% YoY on July 10th, our index has slid to -2% YoY, the lowest reading since mid-June.

Taking a look at another tracker of short-term economic growth, below we show Weekly Economic Index data updated by the New York Fed each week. After decelerating sequentially YoY for the week ended September 4th, the WEI reported sequential YoY growth slower once again in the week ended September 11th. We also show what each high frequency tracker implies about quarterly growth. As shown, our tracker has consistently implied a higher quarterly growth rate than the Weekly Economic Index, and official data for the last two quarters. That said, Q3 is tracking at least 20%, with upside to the high-20s as the US continues to rebound from COVID. This post was originally published in our post-market macro report — The Closer — last night. Click here to start a free trial to Bespoke Institutional and receive our nightly Closer for the next two weeks, featuring more commentary and data on macro markets.

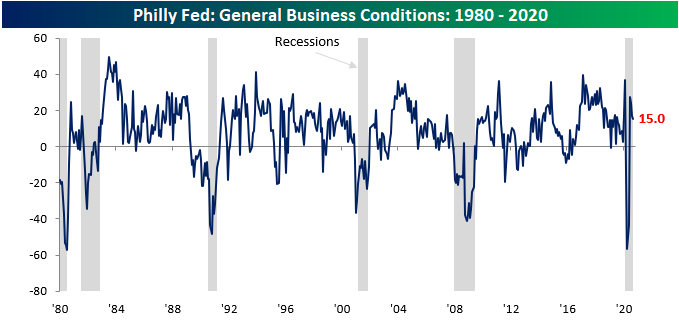

Philly Fed Flat

Unlike its neighbor to the north, the Philadelphia Fed Manufacturing Report lost a bit of steam in September. Economists were expecting the headline index of General Business conditions to remain unchanged at 17.5, but the actual level showed a modest decline to 15.0. Nothing to get alarmed about, but still weaker than expected. Even at current levels, though, it’s worth pointing out that September’s reading was still above the predominant levels we were seeing in the year leading up to the COVID outbreak.

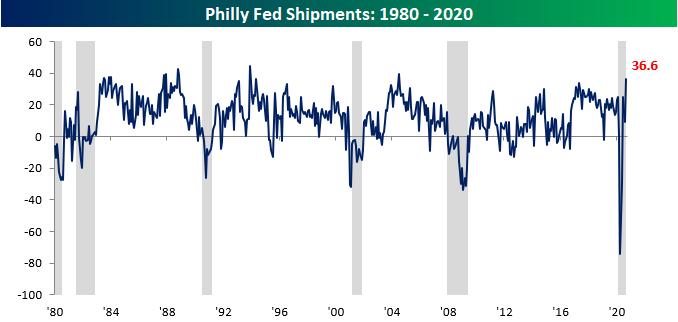

Breadth in this month’s report was also positive. Besides the index of General Business Conditions, the only other indices that declined on a m/m basis were Inventories and Average Workweek. On the upside, the biggest gains were seen in Shipments and Prices Paid. In the case of Shipments, its current level now ranks in the 98th percentile of all prior readings while Delivery Times are also elevated in the 96th percentile of all other periods.

This month’s surge in shipments also ranks as the highest level in over 16 years (July 2004), and that comes just six months after the lowest reading on record.

Finally, in the report’s special questions this month, respondents were asked how Q3 production will compare to Q2, and the responses were positive. 22.2% of those surveyed expect production to increase by more than 10% while just 11.1% expect business to contract by more than 10%. While these results bode well for Q3, the outlook for Q4 doesn’t look as great. Only 6.7% of respondents expect Q4 production to increase significantly while 11.1% expect activity to decline by a ‘significant’ margin. In a trend that doesn’t bode well for the current high levels of unemployment, of those expecting activity to increase, only 17% plan to accomplish this by hiring additional staff. The rest plan to either increase productivity, the hours of current staff, or other measures. Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.

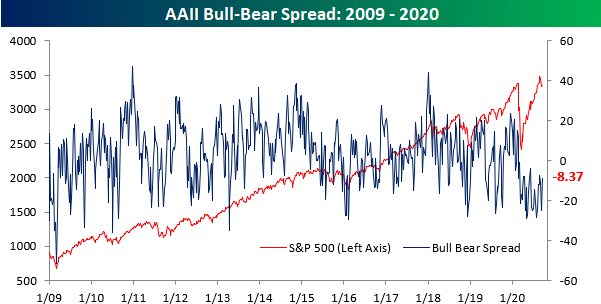

Bullish Sentiment Bounces

With the S&P 500 rallying in the first two days of the week and early on Wednesday, bullish sentiment on the part of individual investors saw a sizable uptick over the last week. According to the latest weekly survey from the American Association of Individual Investors (AAII), bullish sentiment increased from 23.71% last week to 32.02%. That 8.31 percentage point increase was tied for the largest weekly increase since January 16th but only marks a three-week high in optimism.

With the big move into the bullish camp, there was an exodus of equal magnitude from the bears as negative sentiment fell from 48.45% down to 40.39%. The last time bearish sentiment dropped that much in a week was on February 13th just before the Q1 stock market peak. Similar to bullish sentiment but in the opposite direction, though, bearish sentiment was actually lower four weeks ago.

Even after the shifts in sentiment this week, though, the bull-bear spread remains negative at 8.34 percentage points.

This week’s bull-bear spread now takes the current record streak of negative sentiment readings to 30 which is eight weeks longer than the prior record reading of 22 weeks back in late 1990. It’s been well-documented that the sample of this survey tends to skew bearish, but 30 weeks is a long streak! Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.

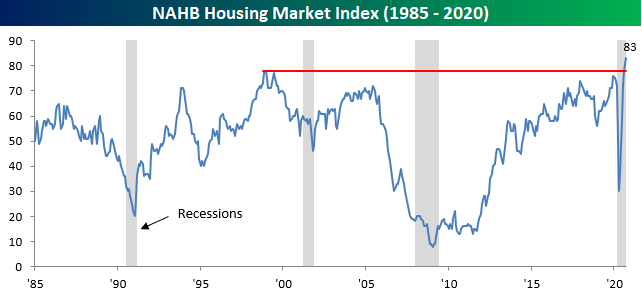

Homebuilder Sentiment Soars

Homebuilders had nothing to complain about in recent months, as the National Association of Homebuilders (NAHB) sentiment index was already tied for its best levels on record. Today’s release of the September update surpassed all expectations. While economists were forecasting the headline index to come in at a level of 78, the actual reading was five points higher at 83. Never before has the homebuilder sentiment index topped 80, let alone moved as high as 83. If this sentiment survey was a stock chart, technicians would consider it a textbook breakout.

The internals of this month’s report were also very strong. Both Present and Future sales as well as Traffic all surged to record highs, and on a regional basis, every region except the West increased. The decline in the West likely stems from the fires in California, but even with that decline, all four regions are now comfortably back above their pre-COVID levels. Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.

The Lights are on North of Broadway

New York City may still be closed for the most part, and the lights are still out on Broadway, but factories across the state are open for business. In the latest release of the Empire Manufacturing report for the New York region, the headline index of general business conditions rose from 3.7 up to 17.0 which was a full ten points above consensus forecasts. What’s very encouraging about these readings is that in the case of both current conditions and expectations, the levels for September are higher now than they were pre-COVID. Despite concerns that the running off of Federal relief programs was going to cause a sharp slowdown in activity, that hasn’t shown up in the Empire Manufacturing report as of yet.

In the early days of the COVID pandemic, manufacturers’ sentiment for present conditions dropped much more than their expectations for the future. In April, the spread between Expectations and Current Conditions was as wide as it has ever been. As businesses have come back online, though, things have moved back into a more normal range. In fact, the current spread of 30.60 is pretty much right in line with its historical average (30.1). That’s a great indication of how quickly certain parts of the economy have been able to adjust and adapt to the new reality.

Breadth in this month’s report was also fantastic. Every component of the Current Conditions part of the report improved relative to August, and just two of the components in the Expectations part (Delivery Times and Prices Received) declined. The biggest improvement came in the Average Workweek, while Number of Employees saw the smallest increase. That suggests that rather than hiring new workers, employers are getting more out of their current workforces. Not necessarily great for the jobs outlook.

Plans for Capital Expenditures and Technology Spending also increased in September. After dropping to their lowest levels since the Financial Crisis earlier this year, the rebound in both indices has been nearly as swift as the pullback. While current levels are still below where they were pre-COVID, the pace of recovery has never been sharper. The economy may still be far from normal, but things have bounced back a lot faster than many were thinking a few months ago. Click here to start a free trial to Bespoke to unlock full access to all of our research and interactive tools.