“Quitters”

Like an old pair of “quitters” that keep falling down because their elasticity is shot, the market has had its own trouble staying up over the last few trading days. Today isn’t over yet, but if the S&P 500 finishes around current levels it will mark the fourth straight day of finishing down at least half of one percent from its intraday high. Compared to the three days before, today’s pullback from an intraday high has actually been pretty mild up to this point. Following Monday’s 2%+ decline from the intraday high shortly after the open, yesterday, the S&P 500 traded down close to 1% from its afternoon high. These two reversals followed Friday’s late-day sell-off when the S&P 500 finished the day down 0.75% from its intraday high.

While it’s disheartening to see the market erasing early gains as the day goes on, it’s helpful to put the last four trading days into perspective. Over the last 25 years, it hasn’t been uncommon for the S&P 500 to finish the day down at least 0.5% from an intraday high for four days in a row. The current streak, if it holds, would be the 158th such streak of four or more days. That works out to more than six a year. There have also been a number of streaks that were much longer than the current one. In fact, it was only a month ago that the S&P 500 went 11 straight days of finishing the day down at least 0.5% from its intraday high, and besides that streak, there have been five other streaks that spanned ten or more trading days. Start a two-week free trial to Bespoke Premium for instant access to our premium research and interactive tools!

Off Season Roadtripping

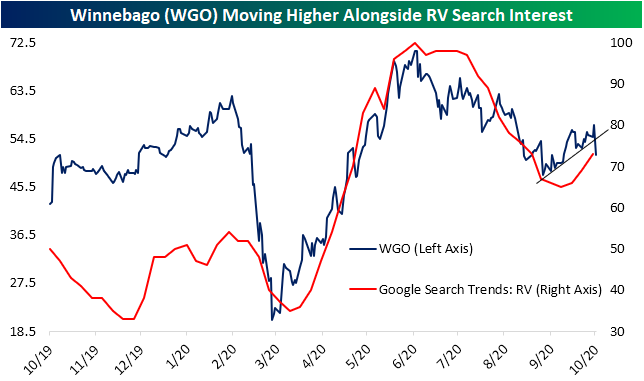

A staple of the recreational vehicle industry, Winnebago (WGO) reported third-quarter results this morning with strong results as the company beat on both the top and bottom lines. EPS came in at $1.45 versus estimates of $0.93. Not only was this the highest reported quarterly EPS for the company in our Earnings Explorer database, but it was also the biggest beat relative to expectations on record. Additionally, the company reported record sales in the quarter at $737.8 million; handily above estimates of $722.9 million and up 39% YoY. Despite the strong results, like most other stocks so far this earnings season, today’s report has been met with selling as the stock is down over 9% as of this writing. As shown in the snapshot of our Earnings Explorer below, all of this is somewhat in line with what could be expected for WGO’s third-quarter results. Even as the stock has boasted the highest beat rate of any quarter in Q3, its stock has only risen in response to its report half of the time. Even though Q3 is typically weak, today’s decline is on pace to be the worst reaction to earnings for WGO since December 2015 and the tenth worst on record.

Back in the spring, interest (proxied by Google Trends data) in outdoor activities like camping, water activites, and recreational vehicles (RV) rocketed higher as people looked to get out of the house and do things that are COVID-safe. WGO was one of the major beneficiaries of these trends. As a result, WGO’s stock price had moved in tandem with search interest in RV’s, rapidly rising in the spring but fading through the summer. With the seasons’ change, search interest for things like boats and pools has waned. RV searches, however, have actually been on the rise again over the past few weeks with WGO’s price joining in. The two have continued to generally track one another well, although the decline in reaction to earnings today is turning this dynamic around.

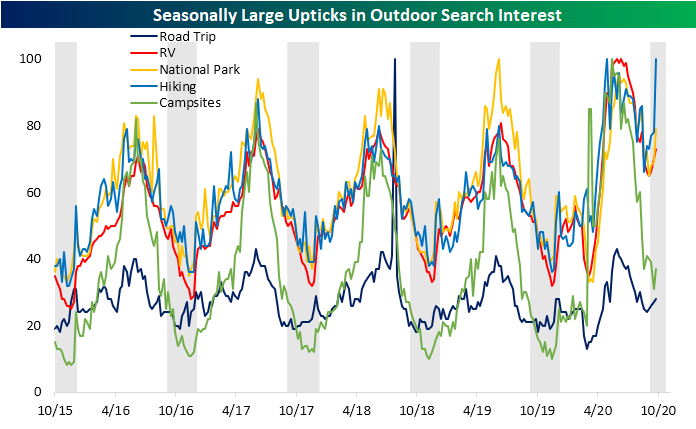

As we discussed in last week’s Bespoke Report, weaker interest in things like boats and pools are a no-brainer for the time of year and should eventually reach a seasonal trough. Turning back to RV interest in particular, over the past five years, search interest similarly has tended to fall from October through the end of the year (gray shaded regions in the chart below), with some sharp upticks at the very end of the year. This year is a bit different with a sizable uptick occurring early on in the final three months of the year. In the chart below we show Google Trend data for searches for RV’s as well as some other related terms like “Road Trip”, “National Park”, “Hiking”, and “Campsites”. These indices represent interest relative to the highest point of the respective term over the past five years. In other words, a reading of 100 is the peak whereas a reading of 50 is when interest was half of the peak.

So where are people taking these RV’s? Most likely the great outdoors, of course. National parks could certainly be one more specific possibility as search interest is similarly seeing an unusually large uptick given seasonality. To a lesser degree search interest for campsites and road trips are also experiencing unusual ticks higher for this time of year. The most impressive seasonally unusual upswing has been for hiking, which is right around some of the strongest levels of the past five years this week. In other words, COVID seems to be bringing a new fervor to leaf-peeping this fall. Just like we saw in the spring, that strength (this time around contrary to seasonal norms) would be positive for the businesses of names like WGO regardless of the sharp selling in response to earnings today.

Google Trends also provides a geographic breakdown by state of search trends which gives an even more in-depth look at this data. In the heat maps below, we show current search interest broken down on a state by state level. Search interest for these same terms are strongest in some areas of the country that are perhaps the least surprising: the Northwest (i.e. Montana and Wyoming) and Northern New England (Maine, Vermont, and New Hampshire). These are areas of the country that places like national parks or nature-oriented destinations are more prevalent especially in Autumn.

Chomping at the Bit for Bitcoin

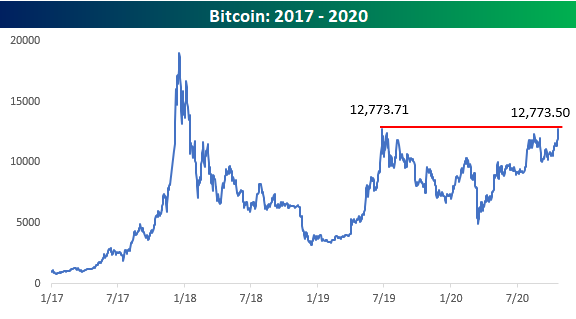

Paypal is making news this morning after the company said it will allow users to buy and sell cryptocurrencies in their accounts and use those funds to pay merchants. With increased/easier accessibility to bitcoin among Paypal customers, bitcoin is up over 7% this morning and trading at a new 52-week high.

From a longer-term perspective, bitcoin isn’t just on the verge of a 52-week high. It’s also on the verge of taking out its summer high from 2019 forming a loose cup and handle pattern in the process. We would also note that the intraday high from mid-2019 is more than $1,000 higher at $13,851.60. To most people, the highs from late 2017 seemed like levels that wouldn’t be seen for years at the earliest, but if the 2019 highs are taken out, the conversation among crypto traders will inevitably shift focus back to those levels. Start a two-week free trial to Bespoke Premium for instant access to all of our research and interactive tools!

The Software Sector’s Richest Stocks

There was a time not long ago when companies that traded at more than 20 times earnings were considered expensive. For investors in the software sector, valuing a stock based on its earnings multiple is considered a metric of a bygone era right up there with ticker-tape and trading floors. With most companies in the sector having no earnings to speak of, the more preferable way to value a company is to look at its multiple to revenues, but even by that metric, a number of companies trade at more than 20 times revenues.

The table below lists companies in the Russell 3000 Software industry that trade for more than 20 times annual sales. Of these 27 names, eight trade for more than forty times sales, and two – BigCommerce (BIGC) and Zoom Video (ZM) – trade at more than 100 times sales. With valuations like that, it’s hard to imagine what assumptions are being made about future growth. It’s not as though these companies are small either. Of the 27 stocks listed, more than two-thirds have market caps of more than $10 billion, and their combined market cap is over $750 billion. Regarding their valuations, you can say all you want, but investors have gotten rich owning them this year as their average YTD performance is a gain of 159.1%. The median is not as strong but is still an impressive 113.6%.

With a group of highflyers like this, you would think that this would be a good group to watch in terms of gauging the risk appetite of the broader market. To that end, the chart below compares an equally-weighted basket of the 27 stocks listed above to the S&P 500 over the last year. What’s interesting to note about their performance is that leading up to prior peaks in the last twelve months, the group peaked at the same time as the S&P 500. While the pricey software stocks provided no ‘advance warning’ of a market decline, following declines, it was helpful to watch. As shown by the three gray circles in the chart, during each of the notable market declines of the last year, investors started to rotate back into the group before the market made its ultimate low. Based on the last year, when these stocks start to take off, the rest of the market has followed suit.Start a two-week free trial to Bespoke Institutional to use our extremely useful Earnings Explorer tool today!

Tesla (TSLA) Driving Into Earnings

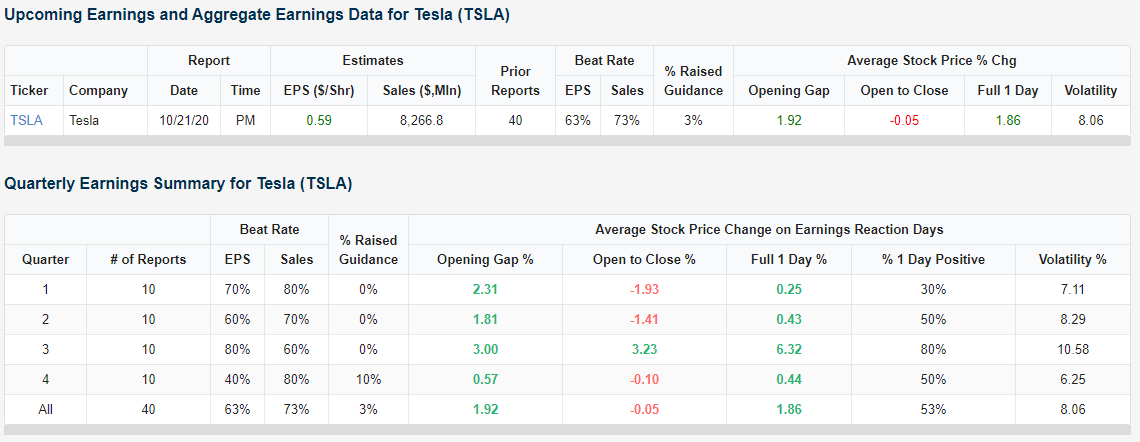

Electric vehicle behemoth Tesla (TSLA) reports earnings Wednesday (10/21) after the closing bell. Headed into earnings, the stock has been consolidating since the end of August with highs roughly around $460 and some higher lows near the stock’s 50-DMA.

On Wednesday afternoon, the company is expected to report a fifth consecutive quarter of profit with EPS of $0.59. Frankly, that is lower earnings than those past four quarters but would mark another quarter in the black nonetheless. Fortunately for TSLA, Q3 earnings by multiple measures have tended to be the strongest quarter of the year for the stock. As shown in the screenshot of our Earnings Explorer below, Q3 for TSLA has seen its strongest EPS beat rate of 80%. Sales beat rates are a bit weaker at 60%. Despite this, Q3 earnings have been by far the best for TSLA in terms of share-price reaction to the news. Not only has TSLA traded higher 80% of the time on Q3 earnings days (compared to 53% for all earnings days), but its average gap up, open to close, and full-day performance are stronger than any other quarter. Throughout its history as a public company, TSLA has averaged a one-day gain of 6.32% in reaction to its Q3 earnings report. No other quarter has seen the stock even average a gain of 1%+.

While TSLA has the tailwind of seasonal strength with recent quarters having seen strong results, the past year’s reaction to earnings have been pretty mixed. On its past two earnings reports, TSLA gapped up more than 5% at the open each time only to erase all of those gains intraday to close lower. In the two quarters prior to that, the stock rallied double digits on earnings. Last October when TSLA reported after the close on 10/23/19, the stock gained 17.67% in reaction to the news the following day. Start a two-week free trial to Bespoke Institutional to use our extremely useful Earnings Explorer tool today!

It’s Singles Month!

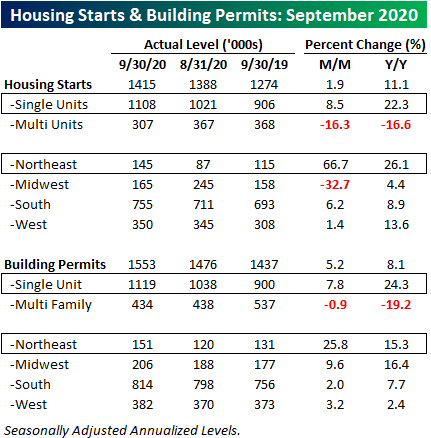

Today’s release of September data on Housing Starts and Building Permits was mixed at the headline level as Housing Starts missed expectations while Building Permits topped consensus forecasts. In each case, the magnitude of the beat or miss was similar, so in the end, it was basically a wash from a top-level perspective.

Within the details of the report, two trends stood out. First, in terms of both starts and permits, single-family units were the star of the show. Single-family Housing Starts rose 8.5% m/m and more than 22% on a y/y basis, while single-family Building Permits also saw similar levels of increases. In both cases, September’s levels for single-family units were the strongest since mid-to-early 2007. The second notable trend evident in this month’s report was a very strong environment in the Northeast. On a m/m basis, Housing Starts in the Northeast surged 66.7% while Permits increased over 25% m/m. There’s been no shortage of stories out there highlighting the exodus out of big cities like New York, and these trends suggest former residents of the Big Apple are moving out to the greener pastures of the suburbs.

From a longer-term perspective, the quickly improved residential housing market bodes well for the broad economy. Housing Starts and Building Permits typically roll over leading up to and then plunge during recessions. This time around, the nature of the pandemic and the shutdowns were so instantaneous that economic data didn’t have time to roll over, and the massive amounts of subsequent stimulus and liquidity made the pullback short-lived. What’s most amazing about where things stand now is that even as the NBER hasn’t even announced the official end of the recession, Housing Starts on a 12-month average basis are already near their pre-recession highs! Normally, once a recession ends, it takes years before Housing Starts get back to their prior highs.

Taking a closer look at more recent data, the chart below shows the 12-month average of both Housing Starts and Building Permits over the last ten years. Incredibly, from their late 2018 highs through mid-2019 lows, both saw larger declines than they did during the pandemic.

While the 12-month average of Housing Starts and Building Permits are knocking on the door of new multi-year highs, the strength in single-family units has already pushed those readings to new post-financial crisis highs. Whether or not the economy rolls over again as economic momentum stalls out is up for debate, but looking at this data and the homebuilder sentiment data from Monday, it’s hard to look at it and say that the recession is not over. Click here to view Bespoke’s premium membership options for our best research available.

October Optimism For Homebuilders

Given housing inventories remain historically low thanks to still strong demand, homebuilders have plenty to be optimistic about. The National Association of Home Builders (NAHB) has continued to show this strength as its monthly sentiment survey set a record high for the month of October. Back in August, the index tied the previous record level of 78 from December of 1998. Over the past two months, it has only raised that bar, coming in at 85 this month; 2 points above forecasts and last month’s reading of 83.

The rise in the index comes on broad strength across each of the sub-indices. Present Sales, Future Sales, and Traffic all matched or made record highs in October. The only sub-index that was not higher was for Traffic, though, it was unchanged at a record high.

As for the look across each of the four US regions, the West and Northeast both saw sizeable upticks to new records, but sentiment in the Midwest and South were actually slightly lower. For the Northeast, this is the third record in a row. Meanwhile, the West’s record high in October finally surpassed the prior high of 91 from October of 2005. Finally, even though sentiment fell in the Midwest and South, both remain at higher levels now than any month other than September’s record highs. Click here to view Bespoke’s premium membership options for our best research available.

Rocketing Restaurants

In Friday’s Bespoke Report sent to members, we noted two groups that have been surprisingly strong performers over the past several months: brick and mortar retailers and restaurants. Focusing on the latter, in the chart below we show the S&P 1500 Restaurants index over the past five years. As shown, up until last week the index’s last high prior to the pandemic actually came well before the rest of the market’s peak in February. The S&P 1500 Restaurants peaked in August of last year and only made a lower high on February 20th before falling over 40% during the course of the COVID Crash in late February and early March. Since the low on March 18th, the index has now risen over 77% and just broke out to a new all-time high.

COVID lockdowns and restrictions on in-door dining have impacted the restaurant industry like nothing ever seen before. Based on the monthly Retail Sales report, the Bars & Restaurants category has seen its share of total retail sales fall more than any other group since COVID began, while the Food & Beverage Store (grocery stores) category has been one of the biggest gainers. This is what makes the recovery for the S&P 1500 Restaurants group so noteworthy. While single-location restaurants run by individuals may be having a tough time with capacity limits depending on their geographic location, the publicly-traded restaurant companies with locations throughout the US have seemingly adapted much better in the post-COVID world. That’s what their share prices are telling us at least.

As shown in the table below, nearly all of the stocks in the S&P 1500 Restaurant group made 52-week lows around the time of the broader market bear market low in mid-March. All but four have since seen their stock price double. Brinker (EAT), the parent company of Chili’s, has risen the most since its low having gained well over 500%. Even after those massive rallies, there are still eleven that are down over the past five years and eleven that are down on a year-to-date basis. Dave & Busters (PLAY) and Red Robin (RRGB) are both down by more than 50% in 2020.

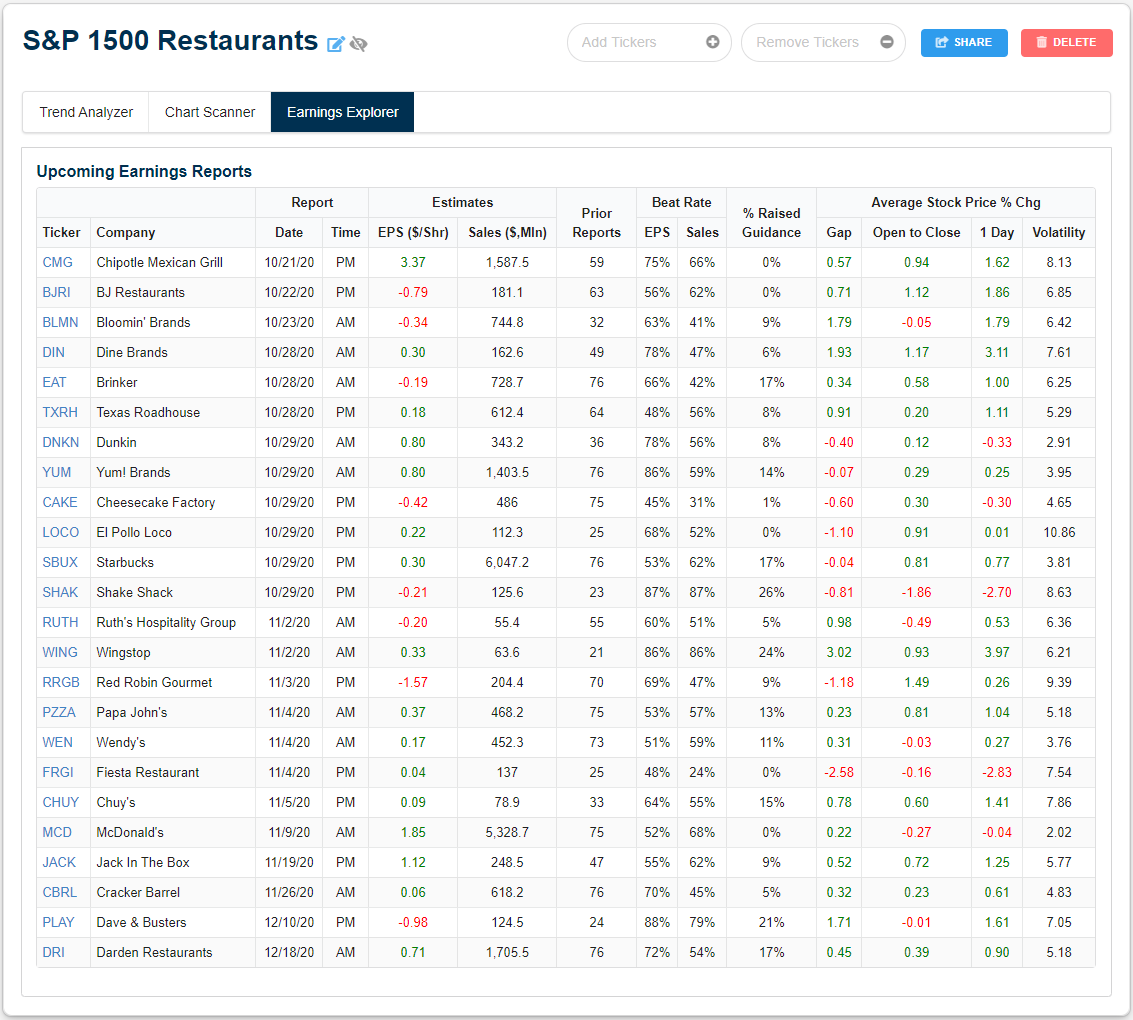

Of this group, Domino’s Pizza (DPZ) is the only one that has reported third-quarter earnings so far this earnings season with overall decent results beating on both the top and bottom line. As shown in the screenshot below, we created a Custom Portfolio of these stocks so members can track these names as earnings season carries on. From our Earnings Explorer data, the rest of the stocks in the group are scheduled to release earnings over the next several weeks. Click here to access our Earnings Explorer and Custom Portfolios tool free for the next two weeks.

Bespoke’s Morning Lineup – 10/19/20 – Back to a Million

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“You can’t have a mid-life crisis in the airline industry because every day is a crisis.” – Herb Kelleher

We hope you enjoyed your weekend because while the economic calendar is relatively light this week, the flow of earnings will pick up in pace as earnings season kicks into high gear. Today, however, is on the quiet side with Homebuilder sentiment the only report scheduled and just a handful of companies reporting earnings.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, key earnings data from the US and Europe, Chinese economic data released over the weekend, trends related to the COVID-19 outbreak, and much more.

The airline industry may always be in crisis but yesterday marked a big milestone for the industry as US total passenger throughput crossed back above the one million level for the first time since March 16th.

Yesterday’s increase in passenger traffic wasn’t just a one-day blip either. On a seven-day average basis, daily passenger traffic has also been steadily rising. Ten days ago, the seven-day average jumped back above the prior post-COVID high of ~780K from early September. Since then, we have seen a steady increase to the current level of ~872K which is nearly 100K above the prior high.

While airline passenger traffic has seen a steady increase off its lows, why aren’t the airline stocks doing better? The reason is that while passenger traffic has been steadily rising, we still have a LONG way to go before things get anywhere near back to normal. The chart below compares the performance of the airline ETF (JETS) to the y/y change in passenger traffic on a seven-day average basis (blue line). The trend is higher but still down by a lot. Yesterday’s million total, for example, was still down over 60% from the same day last year.

Bespoke Brunch Reads: 10/18/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

China

Behind the Stability in China’s Currency: Beijing’s Hidden Hand by Matthew C. Klein (Barron’s)

While official foreign exchange reserve data has been very stable in recent years, the fact that the yuan has traded in an extremely tight range is evidence of interventions by state banks; those interventions are starting to show up in other data as well. [Link]

Can China’s reported growth be trusted? (The Economist)

Private indicators of economic activity have been much more volatile than official indicators. Which is to be trusted? [Link; registration required]

Concerns Abound

Top Fund’s Blacklist Shows ESG Coming for Emerging Markets by Natasha Doff and Selcuk Gokoluk (Bloomberg)

A top-performing bond fund excludes investments that have low ESG ratings, excluding investments in countries like Russia, China, and Saudi Arabia. [Link; soft paywalls]

Ad Tech Could Be the Next Internet Bubble by Gilad Edelman (Wired)

While there are huge questions about the influence of social media networks and their ads on our behavior, some are concerned that the opposite problem is of greater concern: that highly specific targeting of advertisements doesn’t work at all. [Link; soft paywall]

History

Which Constitution Is Amy Coney Barrett Talking About? by Jamelle Bouie (NYT)

An excellent history lesson on the massive changes that Reconstruction brought to the Constitution, with the 13th, 14th, and 15th amendments fundamentally changing the nature of the basic rules of American society. [Link; soft paywall]

One of the Largest Checks Ever (Morgan Stanley/Twitter)

Mitsubishi UFJ invested $9 billion into the collapsing American broker at the height of the financial crisis, leading to a 10-figure check. Here’s the inside story. [Link]

Aliens

Dissolving the Fermi Paradox by Anders Sandberg, Eric Drexler, and Toby Ord (arXiv)

The Fermi Paradox (specifically, given some reasonable assumptions, that there are very high odds that intelligent life exists elsewhere in our galaxy, but there’s no evidence for it) was conclusively disproven back in 2018 to little fanfare. An excellent paper discusses why basic probability theory makes the Drake Equation which the Fermi Paradox rests on useless. [Link]

Rule of Law

‘Straight to Gunshots’: How a U.S. Task Force Killed an Antifa Activist by Evan Hill, Mike Baker, Derek Knowles and Stella Cooper (NYT)

A deep investigation into the killing of a murder suspect by US Marshalls, who opened fire with no verbal warning when they located a man accused of killing a right-wing protestor. [Link; soft paywall]

Birds

‘Jet fighter’ godwit breaks world record for non-stop bird flight by Daniel Boffey (The Guardian)

An absolutely incredible feat of flying saw a migratory bird fly from southwest Alaska to Auckland, New Zealand in 11 days, passing over 12,000 kilometers without touching down for rest or sleep. [Link]

Renewables

Solar-plus-storage replaces coal plant in New Mexico, makes carbon-capture retrofit moot by Tim Sylvia (PV Magazine)

A landmark deal in New Mexico shows how cheap solar has gotten, with multiple installations of production and storage (in batteries) at prices that make coal completely uncompetitive. [Link]

Media Matters

An Arrest in Canada Casts a Shadow on a New York Times Star, and The Times by Ben Smith

The high profile New York Times audio project Caliphate has largely unraveled after its central source was arrested in Canada for violations of the country’s hoax law. [Link; soft paywalls]

COVID Business

Covid Recession Spawning Entrepreneurs in U.S. Amid Joblessness by Michael Sasso and Alexandre Tanzi (Bloomberg)

Business formations are exploding in the wake of the COVID recession, a big difference from the post-financial crisis period, and one we also discussed this week on the blog. [Link; soft paywall]

Is this how theater gets saved? Geffen magic show mines virtual box-office gold by Jessica Gelt (LAT)

Theaters are turning to magic shows broadcast via Zoom to keep the lights as the pandemic prevents Americans from gathering for performances. [Link; soft paywall]

Encore at Wynn Las Vegas changes operating hours due to low demand (KLAS)

After re-opening, Wynn’s Encore property will reduce operating hours thanks to low demand for gambling and other amenities. [Link; auto-playing video]

The Bitter End and Other Concert Venues Say They Won’t Survive Without a Bailout by Lucas Shaw (Bloomberg)

Clubs and bars in New York are at the end of their rope as restrictions on patronage and the general lack of demand for crowded indoor spaces put the industry into dire straits. [Link; soft paywall]

Quarantine Blues

It’s been 214 days since Disneyland closed. For these superfans, it’s agony by Lisa Boone (LAT)

Disneyland remains closed, and that’s been a brutal experience for Disney superfans who have spent years making regular visits to the park. [Link; soft paywall]

Goodbye, Sunny Florida. Hello, Frigid Winter. Covid Strands Canadian Snowbirds. by Paul Viera (WSJ)

“Snowbirds” are Canadians who spend the frigid winters of the Great White North in sunnier, warmer American climes. But border closures and the COVID epidemic mean the million Canadians who fly south for the winter won’t be doing so this year. [Link; paywall]

Teens Did Surprisingly Well in Quarantine by Jean M. Twenge (The Atlantic)

Despite concerns that lockdowns would be extremely hard on young people, teenagers appear to have done better or about the same in terms of mental health in 2020 relative to a similar assessment in 2018. [Link; soft paywall]

Rational Pragmatism

Emily Oster’s Pandemic Parenting Guidance Is All About the Data by Esmé E. Deprez (Bloomberg)

A Brown university economist has developed a huge following by boiling down complex risk families face in dealing with COVID-19. [Link, soft paywall]

The real lessons from Sweden’s approach to covid-19 (The Economist)

Sweden is neither a libertarian paradise nor a herd immunity-seeking disaster, but a pragmatic, high-trust example of how strong social cohesion can help fight COVID. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!