Bespoke Brunch Reads: 3/14/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Cars

Standstill Traffic May Be the Only Thing Keeping Crash Deaths From Skyrocketing by Alissa Walker (Curbed)

Despite a pandemic-fueled collapse in the number of vehicle miles travelled, traffic deaths soared in 2020 as clear roads meant higher speeds and more death. [Link]

We Called 8 Dealerships Asking About EVs. Here’s What They Told Us by Adam Ismail (Jalopnik)

Whether or not dealerships embrace electric vehicles will be a key to how fast they roll out in the United States, and the early indication from this informal review of dealerships across the country. [Link]

Speculation

Young retail investors plan to spend almost half of their stimulus checks on stocks, Deutsche survey claims by Holly Ellyatt (CNBC)

A survey of retail investors suggest that the latest round of stimulus checks are in large part destined for the equity market, driven mostly by younger stock buyers. [Link]

The most frequently asked questions by Robinhood traders reveal ‘new type of uninformed equity-market participant’ by Andrew Keshner (MarketWatch)

During Robinhood platform outages, stocks that were widely owned by Robinhood traders became more liquid and less volatile, suggesting that high volume free to trade buyers and sellers on the platform are adding noise to market prices. [Link]

SPAC Pioneers Reap the Rewards After Waiting Nearly 30 Years by Amrith Ramkumar (WSJ)

Blank check companies were first introduced in 1993 but didn’t really catch on until the last few years; they’re now 70% of IPOs and have raised $75bn this year alone. [Link; paywall]

NFTs

The Whales of NBA Top Shot Made a Fortune Buying LeBron Highlights by Ben Cohen (WSJ)

Digital trading cards known as non-fungible tokens have proven to be a spectacular speculation, with unique clips (which are of course widely available on YouTube or other sites) trading for millions of dollars. [Link; paywall]

Why the NFT Craze Is a Bubble Waiting to Pop by James Surowiecki (Marker)

Unique digital assets are the latest mania fueled by blockchain technology and rabid speculator enthusiasm for the next big thing. [Link]

Tech

This Chip for AI Works Using Light, Not Electrons by Will Knight (Wired)

Instead of running electrons through transistors, a startup that got its beginnings at MIT is using light to build chips that have radically higher throughput potential…if they work. [Link; soft paywall]

Tesla Is Plugging a Secret Mega-Battery Into the Texas Grid by Dana Hull and Naureen Malik (Yahoo! Finance/Bloomberg)

A subsidiary of the electric vehicle company is developing a battery near Houston that can store 100 megawatts, enough to power 20,000 homes on a hot day in Texas. [Link]

POLITICO Playbook: Scoop: Biden taps another Big Tech trustbuster by Ryan Lizza, Tarra Palmeri, Eugene Daniels, and Rachael Bade (Politico)

The Biden Administration has made multiple appointments that suggest a tight focus on antitrust in the tech industry, with a White House economic advisor and a Federal Trade Commission member both falling inside that category. [Link]

Weird News

The bizarre tale of the world’s last lost tourist, who thought Maine was San Francisco by Andrew Chamings (SFGate)

Back in 1977, a German tourist got confused on a layover and mistook Bangor, Maine for San Francisco, sparking an international media frenzy over a very confused man who spoke no English. [Link]

Brood X cicadas are about to put on one of the wildest shows in nature. And D.C. is the main stage. by Darryl Fears (WaPo)

The Delaware Valley, central Midwest, Hamptons, and eastern Tennessee are all due to receive an unholy storm of cicadas this summer as Brood X emerges from its long slumber. [Link; soft paywall]

Tax Trouble

He Got $300,000 From Credit-Card Rewards. The IRS Said It Was Taxable Income. by Richard Rubin (WSJ)

A physicist who spent $6.4mm on gift cards which he rolled into money orders deposited to his bank. The transactions were so large and numerous that they were flagged by the Treasury Department, eventually leading to an IRS investigation. [Link; paywall]

Food & Drink

Union officials: Tate’s Bake Shop workers threatened with deportation if they unionize (Long Island News 12)

Undocumented workers for Long Island bakery Tate’s are being threatened with deportation in response to a unionization drive. Tate’s is owned by Mondelez. [Link; auto-playing video]

The True Cost of a Cocktail by John Debary (Punch)

Ever wonder why a drink at a cocktail bar hits your wallet so hard? A breakdown of the costs that a cocktail typically embeds in its high menu price. [Link]

Furniture

Booming furniture sales mean ‘unprecedented’ delays for sofas and desks by Abha Bhattarai (WaPo)

Huge demand for furniture to upgrade homes that Americans are spending far more time in than usual is driving an unprecedented disruption to supply chains. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Households’ Equity Market Exposure Continues To Rise

Last night the Federal Reserve updated its quarterly Flow of Funds (Z.1) report for Q4. The quarterly report measures income, savings, assets, and liabilities of various macroeconomic sectors. Looking at households specifically, we can measure aggregate exposure to stocks by looking at their holdings of equity investments relative to other assets. We note that this does not include mutual fund shares but it does include ETFs, closed-end funds, and REITs.

As shown below, the value of equity market assets held by households is up to 16.8/% of total assets, the highest since Q3 of 1969 and surpassing the 16.7% peak from the tech bubble. Looking at financial assets only, equity exposure is the highest since the 24.2% peak from 2000, but is nonetheless extremely elevated. We should note that while this signal is certainly a contrarian indicator, it doesn’t necessarily mean that equity markets must decline in value; there’s no reason that markets can’t continue to climb and raise the share of equity ownership further.

Things look different when we include household holdings of mutual funds and other exposure to equities. In the chart below we account for indirect allocations to equities. By this measure, Q4 equity market exposure rose to 38.0% of financial assets (versus the Q1 2000 peak of 38.3%). Equity exposure as a percentage of all financial assets hit a record, surpassing the old peak of 26.4% with a 27.0% reading in Q4. In short, households are very aggressively exposed to equity markets. This blog post is adapted from an analysis included in our nightly Closer report. Click here to start a free trial of Bespoke Institutional to get immediate access.

Bespoke’s Morning Lineup – 3/12/21 – More Yield Drama

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“If you work really hard, and you’re kind, amazing things will happen.” – Conan O’Brien

With US Treasury yields rising overnight, tech stocks are under pressure this morning, while DJIA futures are higher as shares of Boeing (BA) are taking off in the pre-market. At current levels, the 10 and 30-year US Treasuries are on pace to close at post-pandemic highs in terms of yields. The only other report on the calendar this morning is Michigan Confidence at 10 AM.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, including a recap of moves in the rates market overnight, an update of moves in the Asian and European market, European Manufacturing, an update on the latest national and international COVID trends, including our series of charts tracking vaccinations, and much more.

Overall breadth in the market has and continues to be strong. This morning’s example comes from the percentage of S&P 500 Industry Groups trading above their 50 and 200 moving averages. Starting with the percentage of Industry Groups above their longer-term 200-DMA, that reading currently stands at just above 90%. During the recent equity market sell-off, that reading dropped down to as low as 75.0% but has rebounded back towards its recent highs.

Relative to the shorter-term 50-DMA, the breadth reading isn’t quite as strong but still stands at a healthy two-thirds and is up from under 50% during the recent sell-off. Obviously, this is a more volatile reading, but the longer it churns around the 50% level, the more likely it is that we see these lower readings start to drag down the strong readings in the percentage of groups above their 200-DMA. Not much of a worry yet, but something to watch going forward.

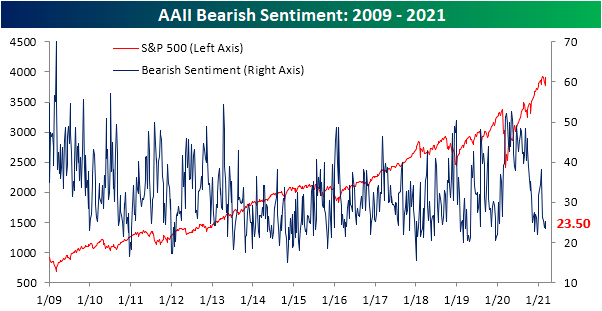

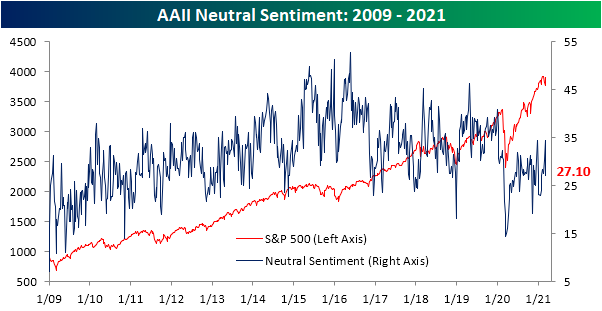

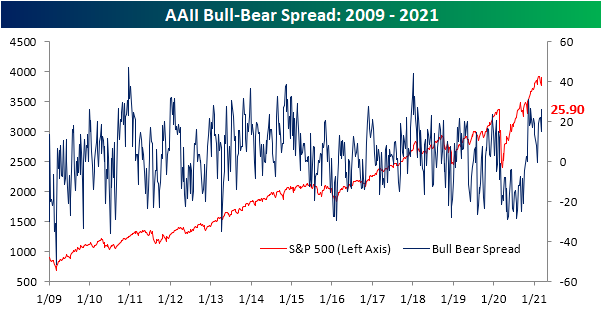

Two Sentiment Surveys Go In Opposite Directions

As equities have rebounded in the past week with the S&P 500 and Dow returning to all-time highs today, sentiment has gotten a boost. After falling in back-to-back weeks, bullish sentiment as measured by the AAII’s weekly survey snapped back rising 9.1 percentage points to 49.4%. That was the biggest one-week increase since the week of November 12th when it rose 17.88 percentage points, and it is also the highest level of bullish sentiment since then.

The declines in bullish sentiment of the prior two weeks saw neutral rather than bearish sentiment pick up the difference. This week again bearish sentiment went less changed than bullish or neutral. Bearish sentiment was only slightly lower falling 1.8 percentage points to 23.5%. That is the lowest level of bearish sentiment since the second to last week of 2020 when it bottomed out at 21.99%.

That means the gains in bullish sentiment took from the big decline in the percentage of respondents reporting as neutral. Only 27.1% of respondents reported as neutral this week, down 7.3 percentage points from the prior week. That was the largest single-week decline since the end of 2020 as sentiment is back to the same level as the start of February.

These changes in sentiment have meant that the bull-bear spread took a sharp move higher rising to 25.9. That is the highest level in the spread since the first week of December when it was slightly higher at 26.41. Prior to that, the only recent reading that was as high was November 12th which was the highest level in over two years.

While the AAII’s survey has reflected the bounce in equities over the past week, another sentiment survey is not yet reflecting this week’s price action. The Investors Intelligence survey of equity newsletter writers showed bullish sentiment fell 2.9 percentage points to 51%. That is the lowest level since the end of last May when it was 50.5%. Meanwhile, bearish sentiment rose 2 percentage points to 20.6%; the highest since early November. This survey also queries respondents on whether or not they are looking for a correction. With the Nasdaq having met the technical definition of a correction earlier this week (a 10% decline from a high), it’s not surprising that the highest share of respondents, 28.4%, reported that they are looking for a correction since late September. Click here to view Bespoke’s premium membership options for our best research available.

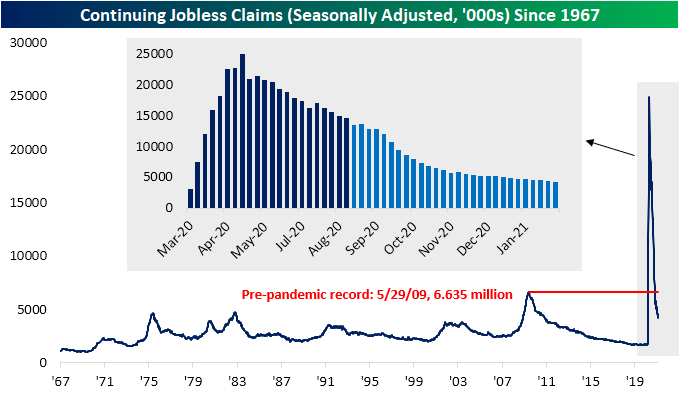

Jobless Claims Weaker Under The Surface

After a small uptick last week, initial jobless claims have resumed their move lower coming in at 712K this week and 13K below expectations. The 42K decline from last week’s upwardly revised reading (745K previously to 754K) entirely erased the prior week’s 18K increase as claims now stand just 1K above the pandemic low of 711K reached in the first week of November. While that is still a historically elevated reading, it is only within 17K of the pre-pandemic record of 695K.

While the adjusted number is just off the pandemic low, on a non-seasonally adjusted basis claims did reach a new low. At 709.5K, claims have taken out the previous 716.6K low from two weeks ago. From a seasonal perspective, declines during the current week of the year are the norm. Historically, the current week of the year (10th) has seen claims fall two-thirds of the time.

Adding in Pandemic Unemployment Assistance (PUA), the improvement in claims data was less impressive. PUA claims were actually higher by 41.86K on a week over week basis bringing total claims between that program and regular state claims to 1.188 million from 1.193 million last week. That is still roughly 181K above the pandemic low from early November and little changed from the past few weeks’ readings.

On a state-level basis, while a majority of states continue to report lower initial claims for both programs, the single biggest contributor to national claims continues to be Ohio. Ohio reported 126.9K regular state claims which is 20K more than the next biggest contributor, California (105.9K). For PUA claims, Ohio’s 261.7K claims in the most recent week are over 45K more than the combined total PUA claims for all other states and territories. For continuing claims, things are a bit less extreme with Ohio only accounting for 4.13% of all regular state continuing claims and 8.67% of total PUA continuing claims.

Like initial claims, continuing claims have also continued to improve, coming in below expectations (4.144 million vs. 4.2 million expected) which was also a new low for the pandemic. The 193K decline was the eighth weekly decline in a row as claims have fallen every week except for three in the past half-year.

Including all programs adds an extra week’s delay to the data. For the data as of the week of February 19th, total claims were an entirely different story as they rose by over 2 million rising back above 20 million for the first time since early December. That week saw an uptick across programs, but the biggest factors were PUA claims and Pandemic Emergency Unemployment Compensation (PEUC) which rose by 1.058 million and 986.35K, respectively. For PUA claims, that was the largest increase since January 8th when there was some catch-up following the signing of the spending bill. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 3/11/21 – Five in a Row?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The key to making money in stocks is not to get scared out of them.” – Peter Lynch

The Dow is looking to make it five in a row today as equity futures are higher across the board. Weekly jobless claims came in lower than expected on both an initial and continuing basis, and are also both at or near their lowest levels of the pandemic. Futures were already higher this morning, but dovish comments from ECB President Lagarde have boosted the mood even further.

Trends related to COVID continue to show improvement on both a national and international basis, as vaccine doses continue to pile up across the country. Also, news from Pfizer (PFE) suggesting strong (94%+) real-world effectiveness of its vaccine based on a study in Israel only makes the outlook for once those doses are administered more broadly even more optimistic.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, including a recap of Asian and European markets, the latest ECB rate decision, Japanese bond flows, an update on the latest national and international COVID trends, including our series of charts tracking vaccinations, and much more.

Looking at the chart of QQQ, it’s in a bit of limbo heading into today. Last week, the index appears to have successfully tested support at its peak from last September. Despite the bounce, QQQ still remains below its 50-DMA, and even after what is on pace to be a 2% gap at the open, it will still be trading below its 50-DMA. Large-cap tech still has some catching up to do!

Short Interest Update

Short interest numbers as of the end of February were released yesterday. In aggregate across all Russell 3,000 stocks, short interest as a percent of float came in at 3.21%, down from 3.6% at the start of the year. In the table below, we show the 25 stocks in the Russell 3,000 that currently have the highest short interest as a percent of float. Topping the list is Academy Sports and Outdoors (ASO) with 40.6% of shares shorted; unchanged in its ranking from the last report for the period ending February 12th. While it is still the most heavily shorted name in the index, ASO did see short interest as a percent of float fall 1.25 percentage points since the last report, and it is down even more considerably since the start of the year given its over 20% rally in that time. Including ASO, 13 of the top 25 most shorted stocks have lower short interest than they did in the last report. Of these, GameStop (GME) has seen the largest decline. GME has been on another massive rally over the past couple of weeks which has left the stock within 16.5% of its January closing highs. With that rally likely causing some shorts to close out their positions, the stock has seen a 6.36 percentage point drop in short interest as a percent of float in the most recent period, though, it remains one of the most heavily shorted stocks. Conversely, GEO Group (GEO) and Solid Biosciences (SLDB) are the two stocks in the top 25 that have seen short interest rise the most since the last report and YTD. For SLDB, the increase in short interest comes on what have been big gains year to date (+39.84%) while GEO has actually fallen double digits this year.

Not only has SLDB seen the biggest uptick in short interest among the most heavily shorted stocks, but it is also the stock that has seen the biggest increase of the entire index. In the table below, we show the Russell 3,000 stocks that have seen the biggest increase/decrease in short interest as a percent of float since the last report in mid-February. Other than SLDB, no other name saw a double-digit increase from the previous report with the next largest increase coming from Workhorse Group (WKHS) which saw short interest as a percent of float rise 8.4 percentage points. While WKHS saw higher short interest from the last report, the stock is still less heavily bet against than it was at the start of the year. Of the 20 stocks to see the biggest increases, WKHS is the only one that this applies to.

As for the stocks that have seen the biggest declines in short interest, there are three that fell by more than 10 percentage points: Corbus Pharma (BRBP), Dillard’s (DDS), and Kymera Therapeutics (KYMR). It should come as no surprise that once again, GME is not much further down this list with its 6.36 percentage point drop in short interest. On a year-to-date basis, GME is also the stock that has seen the biggest decline in short interest. Dillard’s (DDS), BigCommerce (BIGC), and Ligand Pharma (LGND)—all of which saw some of the biggest declines since the last report—are the runners-up in terms of YTD declines each having seen short interest fall by over 50 percentage points.

Looking across the names in the tables above, one industry group pops up more than any other: the Pharmaceuticals, Biotechnology, and Life Sciences industry. Of the 25 most heavily shorted names, 7 stocks are part of this industry. Meanwhile, of the 20 stocks that have seen short interest increase the most since the last report, 11 are from this industry, though, even 8 of the 20 biggest decliners also belong to the Pharma, Biotech, & Life Sciences industry.

Given this, on an aggregate basis, this industry has the highest short interest as a percent of float; up 6 bps from the last report to 5.46%. That replaces Retailing in the number one spot of the most heavily shorted industry groups. Further, the massive amount of short interest in retail names has appeared to have normalized. Whereas the industry came into the year with over 8% of float shorted, the current reading has fallen down to 5.36%. Similarly, Energy and Transportation stocks have seen aggregate short interest as a percent of float fall by more than 1 percentage point since the start of the year. Not everything has seen short interest decline though. Food, Beverage, & Tobacco, Household & Personal Products, Banks, and Insurance have all seen short interest rise since the start of the year. Since the last report, Food & Staples Retailing, Commercial & Professional Services, and Insurance all have seen the biggest upticks in short interest. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 3/10/21 – Inflation Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.” – Ernest Hemingway

Nothing like a quote on the perils of inflation for a day when inflation is on everyone’s mind in the wake of recent market performance and today’s release of the February CPI. Equity futures were modestly higher heading into the release, treasury yields are higher, and bitcoin is above $55K. With the report coming in right in line with expectations at the headline level and slightly weaker than expected ex-food and energy, the positive tone looks to be continuing. We would stress, though, that this is only the initial reaction. There’s lots of time left in the day and even to the opening bell!

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, including a recap of Asian and European markets, French manufacturing output, credit growth and inflation in China, an update on the latest national and international COVID trends, including our series of charts tracking vaccinations, and much more.

After Tuesday’s surge in the Nasdaq and strong rally in the S&P 500, US equities are back in the black for the week, but in many ways, the stocks that led the rally on Tuesday were the exact opposite of the ones that outperformed on Monday. For starters, within the entire Russell 1000, there were only 36 stocks that outperformed the index by more than 1% on both days.

The decile performance of stocks in the Russell 1000 on Tuesday based on their performance Monday also illustrates this trend. As shown in the chart below, the five deciles of top performers Monday all averaged declines on Tuesday, while the five deciles comprising the worst-performing stocks from Monday all saw positive returns on Tuesday. Outside of decile one which was only down slightly less than decile two, the performance rankings of the ten deciles on Monday versus Tuesday was a complete reversal. As noted in the Bible, “the last shall be first, and the first last:”

Small Business Sentiment Slow to Come Back

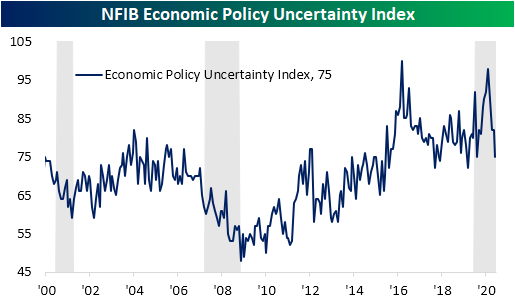

After crashing following the election, optimism on the part of small businesses remains pretty beaten down, though there was finally an improvement in February. The NFIB’s Small Business Optimism Index was expected to see a 2 point rebound in the month of February, but the increase was even smaller as the index rose from 95 to just 95.8.

While small business sentiment is far from recovered, uncertainty has improved. After spiking to a near-record high of 98 headed around the election last fall, the index for Economic Policy Uncertainty has continued to fall dropping to 75 in February. That 7 point month-over-month decline stands in the bottom 5% of all monthly changes which brings the index to the lowest level since last April.

Breadth in the report was mostly positive with 10 of the 18 categories higher in February while another 3 went unchanged and the remaining 5 were lower. Although most categories saw an improvement, several readings remain at historically low levels. For example, the indices for Expect Economy to Improve and Expect Real Sales Higher were both in the 3rd percentile of all readings. Other indices also remain at the low end of their historical ranges such as Plans for Capital Outlays and Now is a Good Time to Expand.

Sales metrics generally improved although firms reported as less optimistic for the future. While sales expectations fell deeper into negative territory, small businesses reported higher nominal sales as that index rose 9 points from -7 to 2. That was in the top 5% of all monthly moves and the first positive reading since November. Additionally, the index for Actual Earnings Changes also improved rising 5 points to -11. Due to the strong pace of sales, a higher share of companies reported higher prices. That index rose 8 points to 25. That is the strongest reading for the index since August 2008.

In addition to stronger sales, lower inventory levels also played into those higher prices. The index of Inventory Satisfaction which measures how many firms report current inventory levels as “too low” was flat on the month in the top 1% of all readings. Despite this, fewer firms report plans to increase inventories. The index for Inventory Accumulation actually fell 2 points to the lowest level since May.

While small businesses do not appear to be making plans to increase inventories, they are investing in employment. The index for Hiring Plans rose slightly from 17 in January to 18 in February. Although that is off higher levels from earlier in the pandemic, it is well within the range of the past several years. Compensation Plans were also higher with the index gaining 2 points to 19. Even though firms appear to want to increase employment, they have yet to follow through with hiring. The index for Actual Employment Changes remains negative falling further to -3 in February. Meanwhile, the Compensation index went unchanged. The lack of actual increases to employment is not a demand problem but instead appears to be a labor supply problem. A record number reported job openings as hard to fill while 33% report either cost or quality of labor as the single most important problem for the business; up 5 percentage points from the prior month. That borrowed from firms reporting things like Taxes, Inflation, and “Other” as their biggest issues. Click here to view Bespoke’s premium membership options for our best research available.

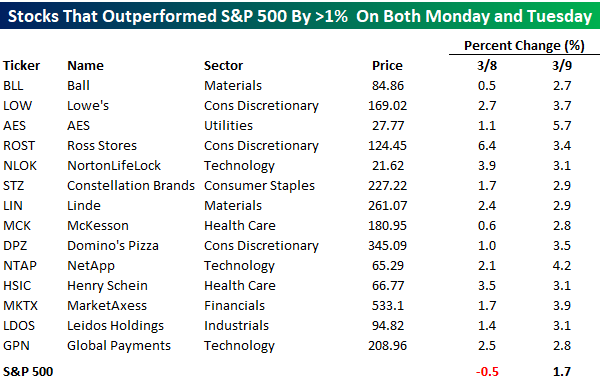

Versatile Outperformers

There’s still a lot of time left in the day, but the tone of the equity market has been much different today compared to Monday. Whereas Monday saw tech stocks get creamed while cyclical areas of the market rallied, today we’re seeing tech stocks rebound while cyclicals lag. To illustrate, within the entire S&P 500 there are just 14 stocks that have so far managed to outperform the index by at least one percentage point both yesterday and today. The table below lists each of those stocks, and looking through them, they aren’t the flashy, high-profile names that you always see discussed in the media. Who said boring is a bad thing? In terms of sector representation, there’s also no clear trend as eight of the eleven sectors are represented by the list of just fourteen names!

Below we show six-month price charts of each of the 14 names listed above from our Chart Scanner tool. Here again, no clear technical theme links the stocks together. While stocks like AES, Global Payments (GPN), McKesson (MCK), and Ross Stores (ROST) remain close to six-month highs, others like Ball (BLL), Domino’s (DPZ), and Market Axess (MKTX) aren’t far from six-month lows. Click here to view Bespoke’s premium membership options for our best research available.