Growth at a Reasonable Price (GARP) Basket

Today we are debuting our Growth at a Reasonable Price (GARP) Basket, which utilizes a proprietary algorithm in an attempt to find stocks that may be mispriced relative to their growth. In this report, we highlight some of the flaws of pure growth and value strategies before diving into the potential benefits of a GARP strategy. There are 50 stocks included in the GARP Basket, with brief descriptions provided for each one. This basket is weighted in proportion to S&P 1500 sector weightings and will be updated on a quarterly basis, which gives each company the ability to report an additional quarter of earnings.

Bespoke’s GARP Basket is available at the Bespoke Premium level and higher. You can sign up for Bespoke Premium now and receive a 14-day trial to read our GARP report. To sign up, choose either the monthly or annual checkout link below:

Small Business Expectations Disconnect

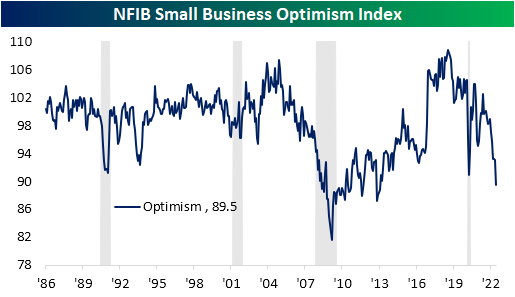

The only US release on the economic calendar today was the NFIB’s Small Business Optimism Index, and it was a big dud. Compared to last month’s low reading of 93.1, the index fell to 89.5 versus expectations for a much more modest decline to 92.8. As a result of that larger than anticipated drop, the index is now below the COVID low and down to the lowest level since January 2013.

As the headline number is now in the 6th percentile of its historical range, several other components are similarly depressed including a record low reading in expectations for the economy to improve. Although some indices have managed to hold up decently—for example, reported inventory levels and the difficulty in filling openings remain in the top few percentiles since the survey began—breadth in June was very weak with many of the declines being historically large.

As we noted in today’s Morning Lineup, labor market indicators within the report have cooled off in recent months but remain at historically impressive levels. Meanwhile, inflation readings are also continuing to come in very elevated in spite of coincident declines in sales expectations.

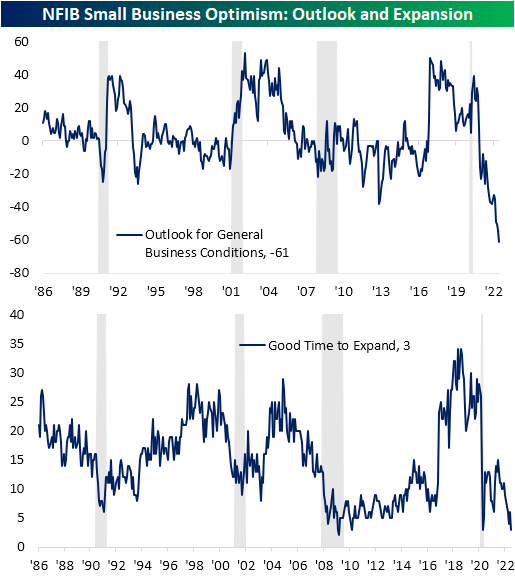

Again, the worst category of the report was the reported outlook for general business conditions. This index set the bar for a record low even lower as a net 61% of respondents reported that they expect the economy to worsen in the months ahead. Given this, there is also a historically muted share of respondents reporting now as a good time to expand their businesses. That reading came in at a meager 3, which alongside April 2020 and March 2010, was the joint lowest level since March 2009.

The NFIB also provides some detail as to why businesses are reporting such a soured outlook regarding expansion. Half of the responses blamed broader economic weakness as the reason. Ironically, that goes against the fact that only 2% reported weak sales would be a reason while another 3% reported strong sales would be the reason to expand. Additionally, while inflation remains such a major concern, only 4% blamed higher costs as a reason to not expand. So while half blamed economic conditions as the reason not to expand, there were some contradictory cross currents.

While it is a drastically lower share at only 10%, the next biggest reason for not expanding was the political climate. As we have frequently noted in the past, one issue with the NFIB survey is that there has been a sensitivity to politics, namely a bias in favor of Republicans. Given the Democratic administration, it is not exactly surprising that political climate would come in second.

Another interesting point to note on this month’s survey regarded the uncertainty index. This measure essentially tracks the number of times respondents select “uncertain” or “don’t know” as an answer to a survey question. Here was another index that has reached the lowest level in over a decade. This month’s low reading would imply that firms have a decidedly negative outlook for the economy.

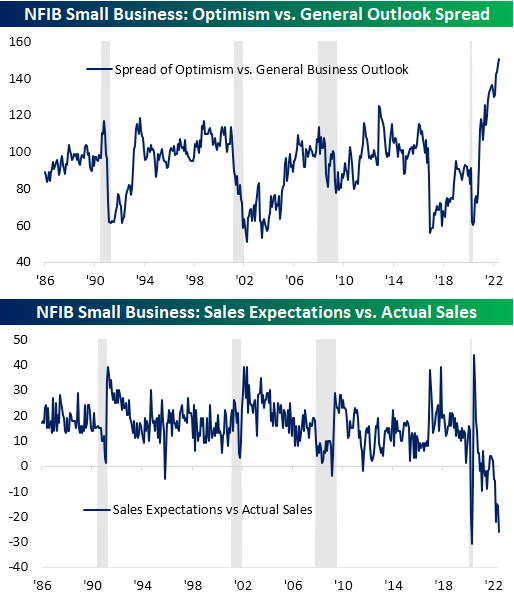

While sales expectations are down near the worst levels since the Global Financial Crisis and the COVID Crash, actual observed changes in sales have not yet cratered in the same way. That being said, on net there are more firms reporting lower sales than higher.

In other words, small businesses expect sales to get much worse than what current levels of sales would have historically implied. As shown below, the spread between those two indices has only been lower once on record and that was at the start of the pandemic. Similarly, the record low in General Business Outlook starkly contrasts with where the headline optimism index has been sitting. That spread is at a record high meaning again economic outlook is far worse than the overall level of optimism.

Another Curve Inverts

As of today, the percentage of inverted points on the yield curve reached the YTD highs seen in mid-June of 17.9%. This comes as the 10-year and 1-year invert, as well as the 5-year and 2-year. The inversion of points on the yield curve (particularly 2s&10s) tends to be cited as a leading recession indicator, due to the fact that higher near-term yields imply a higher risk in the near-term rather than the long-term, the inverse of what is typically true. The graph below shows the rolling percentage of inverted points on the curve over the last six months. Click here to learn more about Bespoke’s premium stock market research service.

As mentioned above, the spread between the 10-year and 1-year treasury inverted today, which is the first occurrence since October of 2019. Following prior inversions of this part of the yield curve since 1970, a recession has followed in the next two years 99.8% of the time which would suggest that a recession at some point in the next two years is almost certain. Following the first inversion in at least one year when a recession did follow, it has taken an average of 271 trading days to officially enter a recession. The shortest time it took to enter into a recession following 1s and 10s inversion was in 1973, when it took just 191 trading days. As mentioned, going back to 1970, recessions have followed within two years of an inversion 99.8% of the time. The only time that this part of the curve inverted and a recession did not follow within two years was after a brief stint in the fall of 1998.

KWEB Gaps Down 4%+

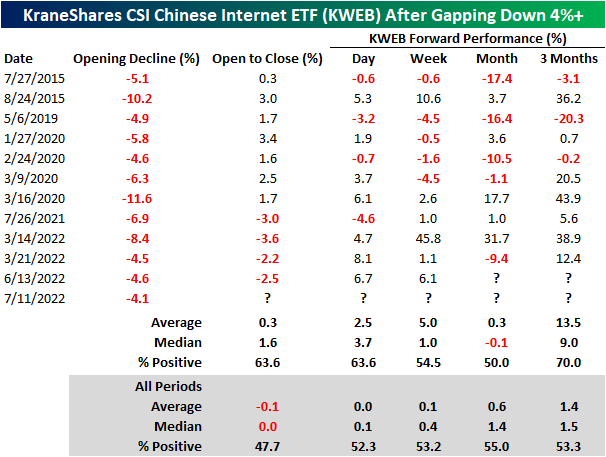

Today, the KraneShares CSI Chinese Internet ETF (KWEB) gapped down by 4.1% due to regulatory pressures from the Chinese Communist Party and an uptick of COVID cases in a few Chinese cities. Since KWEB’s inception in August 2013, the ETF has only gapped down by 4%+ 12 times, the largest of which was an 11.6% drop in March of 2020 during the height of the COVID crash. Following these weak opening gaps, KWEB has tended to partially recover throughout the day, booking a median gain of 1.6% between the open and the close. However, today the stock bucked that pattern and continued to decline from the open to close falling an additional 2%, resulting in a total loss of over 6%.

Following prior downside gaps of 4%+, KWEB has bounced back by a median of 3.7% the next day, with positive returns nearly two-thirds of the time. Over the course of the next week, KWEB has posted a median gain of 1.0%, which is 0.6 percentage points better than the average of all periods. For all the time periods that we looked at, KWEB’s median performance following these occurrences has outperformed the median of all periods, apart from the following month. Three months later, KWEB has booked a median gain of 9.0%, which is 7.5 percentage points higher than the 1.5% average for all periods. Click here to learn more about Bespoke’s premium stock market research service.

Elon Musk: The 2022 Twitter (TWTR) Catalyst

On the front page of most news sites today is the headline that Elon Musk has officially sent notice terminating his deal to acquire Twitter (TWTR). Similar to the way other celebrities have appeared to be major catalysts for a stock in the past year, like Joe Rogan and Spotify (SPOT), Musk’s interest in one of the cornerstones of social media has played a major role in the movements of TWTR’s stock this year. Below, we show a timeline of the saga overlaid on the charts of TWTR’s stock price and the daily percent change since the start of the year.

Back in early April—only a little more than a week after Musk tweeted a poll regarding the platform and free speech then following up with a tweet mentioning the “consequences of this poll will be important”—markets got confirmation that one of history’s wealthiest people had become the company’s largest single owner of Twitter with a 9.2% passive stake. That sent the stock surging 27.12% in a single day. The following day, TWTR rose another 2% when the company extended an offer for him to join the Board of Directors. That was an offer that would be rejected only a few days later as the stock began to reverse some of the massive gains. TWTR would not go on to turn around until Musk officially offered to buy the company at $54.20 per share (4/14), his financing was confirmed (4/21), and finally, when a deal was reached (4/25).

We always say how the market is forward-looking, and it appears as though Mr. Market knew the deal was fake news the entire time. On the day the deal was announced, TWTR peaked a few dollars short of Musk’s proposed price and has been on the decline ever since. The worst of the reversal occurred in mid-May as Musk expressed a hold-up regarding the company’s tracking and reporting on fake/bot accounts. A lack of resolution to Musk’s reservation has been the justification for the undoing of the deal which was confirmed last Friday, resulting in Twitter shares to fall 13.74% since last Thursday’s close.

Finally, we would also note that even though Twitter (TWTR) is a major player in the social media space, it is way down the list in terms of the S&P 500’s largest stocks; especially after the recent drop. Conversely, Musk’s Tesla (TSLA) is currently the fifth-largest stock in the index based on market cap indicating it has an outsized impact on the moves of the S&P. Given all the recent events and Musk’s involvement, Twitter and Tesla have been trading increasingly in sync with one another over the past few months implying these moves in Twitter to some extent actually have ripple effects for the broader market via sympathetic moves in TSLA. For example, while Twitter is down 9.5% today as of this writing, TSLA is falling 6.5%.

Below we show the correlation between the daily moves in TWTR and TSLA on a rolling 2-month basis which would roughly cover the period when the Twitter deal came into question and shares began to roll over. Historically, the two stocks have had a modest positive correlation with a handful of stints in which that relationship became very strong like late 2018, the COVID Crash, and the first quarter of this year when growth stocks broadly fell together. This year, that correlation weakened a bit as the Twitter acquisition news began to develop, but since the deal began to fall apart, it has started to rip higher once again with the current level entering the top decile of historical readings. Click here to learn more about Bespoke’s premium stock market research service.

Consumers Run From Stocks

The New York Fed runs a monthly survey of consumer expectations (SCE) which covers topics ranging from inflation, the labor market, and household finances, and while its history is limited (starts in 2013), it provides a great look at where US consumers see the state of the economy and financial markets. The latest update for the month of June was released earlier today and provided some really interesting insights regarding different trends, but one we wanted to focus on here is how Americans view the prospects for stock prices.

As the equity market has weakened this year amid higher inflation and the Fed’s rate hike cycle, consumer sentiment towards the stock market has been declining, but the pace has really picked up in the last two months taking the total percentage of consumers expecting higher stock prices to its lowest level (33.8%) in the history of the survey. Put another way, just about two-thirds of US consumers expect stock prices to remain flat or decline over the next 12 months. Add this to the long litany of other sentiment surveys showing investors and consumers alike have little confidence in the stock market. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Brunch Reads: 7/10/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Autos

Registrations for electric vehicles soar, signaling increasing mainstream acceptance by Jayme Deerwester (USA Today)

Electric vehicle sales industry-wide were up 60% YoY in Q1 despite an 18% drop in overall registrations. Fully electric vehicles in the US are just below 5% of total passenger sales in the US with roughly 60% of sales driven by Tesla. [Link; auto-playing paywall]

Monthly car payments have crossed a record $700. What that means by Brittany Cronin (NPR)

The combination of car price inflation and more feature-laded vehicles along with soaring interest rates are driving a surge in the monthly payment required to cover a car purchase. [Link]

New York Waterways

Give Me Your Tired, Your Poor, Your Pods of Dolphins—New York Welcomes New Immigrants by Alyssa Lukpat (WSJ)

As the rivers around New York have gotten cleaner, dolphins have returned to New York harbor in pursuit of a snack. Fins have been spotted from Brooklyn to Harlem, delighting residents. [Link; paywall]

She died in a Manhattan penthouse but was buried on an island for the poor by Mary Jordan (WaPo)

A tiny one mile slice of Long Island Sound is the largest public cemetery in America, serving as the final resting place for more than 1 million souls interred since 1869. [Link; soft paywall]

Real Estate

Roaring US Rental Market Shows Early Signs of Slowing Down by Paulina Cachero (Bloomberg)

High frequency indicators suggest that rents are starting to fall in a range of markets that were absurdly hot during 2020 and 2021, with large drops for 1- and 2-bedroom apartments alike. [Link; soft paywall, auto-playing video]

The Suburban Lawn Will Never Be the Same by Brian Eckhouse and Siobhan Wagner (Bloomberg)

As drought wracks the American West, homeowners have started to replace dead, dried out grass with artificial turf which doesn’t have the same thirst for scarce water that real blades would soak up. [Link]

Crypto

‘It’s Ruined Me’: Voyager Customers Fear Life Savings Gone After Crypto Firm’s Bankruptcy by Maxwell Strachan (Vice)

A crypto brokerage that promised huge yields for deposits of fiat currency has suspended withdrawals and declared bankruptcy, leaving customers holding the bag. [Link]

Sports

World Cup stadiums in Qatar to be alcohol-free – source (i24)

Thirsty footy fans are going to be totally out of luck at the World Cup this fall, with host country Qatar banning alcohol consumption in public…including the stands of matches at the iconic sporting event. [Link]

Fiscal Policy

Was the Paycheck Protection Program Effective? by William R. Emmons and Drew Dahl (FRB St Louis)

As COVID smashed the US economy in 2020, Congress traded off speed for precision. The consequence is that Paycheck Protection Program loan/grants were much less useful in supporting workers than unemployment insurance or economic impact payments. [Link]

Energy Shortage

Germany dims the lights to cope with Russia gas supply crunch by Guy Chazan (FT)

Russia is cutting off natural gas supplies to Germany, and the result is a nationwide energy crisis that is forcing rationing and massive price inflation onto households used to cheap and reliable gas supplies. [Link; paywall]

That’ll Leave A Mark

Markets Had a Terrible First Half of 2022. It Can Get Worse. by James Mackintosh (WSJ)

Stocks collapsed in the first half of the year, but the pessimist’s perspective offers little hope of a major rebound in the second half given how much risk still remains. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

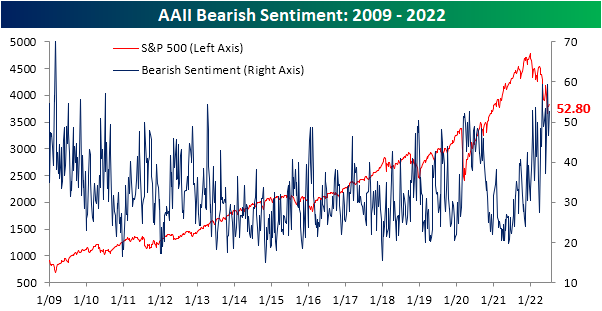

Bulls Back Below 20%

Even though the second half of June and first week of July have seen the S&P 500 climb back from its lows, sentiment appears to show that investors are not buying it. In today’s update of AAII sentiment survey, there was an overall push toward more bearish tones. For starters, the percentage of respondents reporting as bullish fell back below 20%. Even though that is not any sort of new low, this week is the fifth in a row with less than a quarter of respondents reporting as bullish. As shown in the second chart below, such a streak has been unprecedented with the last example of such an extended streak of depressed sentiment being May of 1993.

As bulls have been no where to be found, bears are plentiful with over half of respondents reporting bearish sentiment. This week’s reading came in at 52.8%, up from 46.7% last week. Mirroring bullish sentiment, that is not any sort of new pinnacle for bearish sentiment as there were even higher readings that closed in on 60% last month. Regardless, sentiment remains historically pessimistic with few other periods having seen such elevated readings for as extended of periods.

With inverse moves in bulls and bears, there is now a 33.4 percentage point gap between the two readings which is in the 2nd percentile of all readings since the survey began in 1987.

That leaves neutral sentiment to be the only normal reading of the survey. At 27.8%, neutral sentiment is in the middle of its pandemic range and only 3.6 percentage points below its historical average.

The more bearish turn at the expense of bulls witnessed in this week’s AAII survey was echoed by other readings on sentiment like the Investors Intelligence survey and NAAIM Exposure index. Combining all three of these sentiment readings into one composite, overall outlooks for the market took a further bearish turn this week with the average survey currently 1.8 standard deviations below its historical norm. That is slightly better than earlier this spring, but still, the only period since the mid-2000s with similarly pessimistic readings was in late 2008 and into 2009. Click here to learn more about Bespoke’s premium stock market research service.

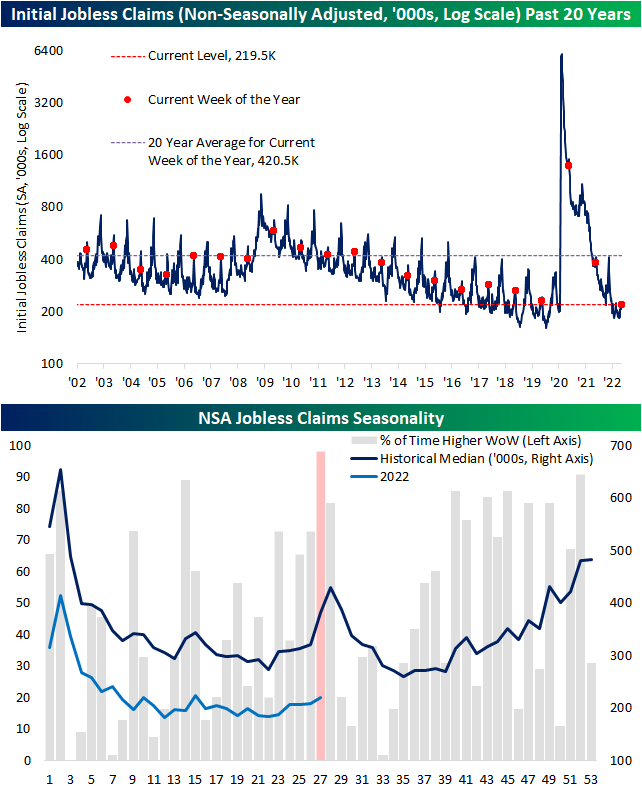

Worst Week of the Year For Claims

Initial jobless claims remain historically healthy in the low 200K range, but the most recent week’s data did mark one of the highest readings of the year. Coming off of last week’s unrevised 231K, claims rose 4K to the highest level since the second week of the year when they clocked in at 240K. That remains a much better reading than what was observed throughout much of the history of the data, but it is at the higher end of pre-pandemic readings (those from roughly 2017 through 2019).

As for the non-seasonally adjusted number, the current week of the year is essentially guaranteed to see a week-over-week increase. The current week has historically been the worst of the year in terms of week-over-week moves only having seen unadjusted claims fall once since 1967. That one decline was in 2020 when claims were working off unprecedented record highs. Given that historically consistent drift higher in claims during this point of the year, next week has historically averaged a temporary peak in claims. While that lends to the possibility of claims continuing to rise next week, the current reading is below that of comparable weeks of pre-pandemic years. In other words, claims are following standard seasonal patterns and are doing so at historically strong levels even if they have come off the absolute strongest levels of the pandemic.

Continuing claims have also begun to come off of the best levels of the pandemic. Adjusted continuing claims were expected to go unchanged at 1.328 million this week. Instead, they rose up to 1.375 million; the highest level since the week of April 22nd when claims were 12K higher. Click here to learn more about Bespoke’s premium stock market research service.

The Closer – Meaningless Minutes, Openings, Housing, Ag – 7/6/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of the minutes from the June FOMC meeting (page 1) followed by a look at job openings through today’s JOLTS report (page 2) and Indeed data (pages 3 and 4). We then pivot to housing data with the latest delinquency readings out of the Mortgage Monitor report from Black Knight (page 5) and realtor.com data covering inventories and prices (page 6). We then shift into the latest PMIs (page 7) before closing with a look into the declines in agriculture commodities (page 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!