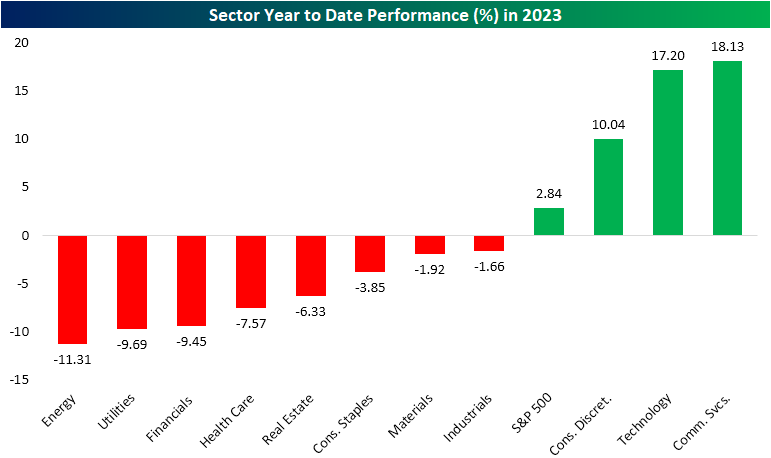

Sector Performance Experiences a Historical Divergence

The first quarter of 2023 is coming to a close next week, and checking in on year to date performance, there has been a big divergence between the winners and losers. Although the S&P 500 is up 2.84% on the year as of yesterday’s close, only three of the eleven sectors are higher. Not only are those three sectors up on the year, but they have posted impressive double digit gains only three months into the year. Of those three, Consumer Discretionary has posted the smallest gain of 10% whereas Technology and Communication Services have risen 17.2% and 18.1%, respectively. The fact that these sectors are home to the main mega cap stocks — like Apple (AAPL), Amazon (AMZN), and Alphabet (GOOGL), which have been on an impressive run of late — helps to explain how the market cap weighted S&P 500 is up on the year without much in the way of healthy breadth on a sector level.

One thing that is particularly remarkable about this year’s sector performance is just how rare it is for a sector to be up 10%+ (let alone 3) while all other sectors are lower. And that is for any point of the year let alone in the first quarter. As we mentioned in yesterday’s Sector Snapshot and show in the charts below, going back to 1990, there have only been two other periods in which a sector has risen at least 10% YTD while all other sectors were lower YTD. The first of those was in May 2009. In a similar instance to now, Consumer Discretionary, Tech, and Materials were the three sectors with double digit gains back then. With those sectors up solidly, the S&P 500 was little changed on the year with a less than 1% gain. As you can see below, though, by the end of 2009, every sector had pushed into positive territory as the new bull market coming out of the global financial crisis was well underway.

The next occurrence was much more recent: 2022. Obviously, it was a tough year for equities except for the Energy sector which had a banner year. Throughout most of the year, the sector traded up by well over 20% year to date even while the rest of the equity market was battered.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.

Bespoke’s Morning Lineup – 3/24/23 – Markets Can’t Calm Down

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.” – Henry Ford

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

They’re starting to drop like flies. The dragnet on global banks has moved on to Deutsche Bank (DB) this morning as the stock trades down over 10% following a sharp decline yesterday as well. Given the tendency of the bank to always find itself right in the middle of any issue related to banking troubles, it’s almost surprising that it didn’t happen sooner. There only potential catalyst for the decline in Deutsche Bank stock this morning is a report that suggests that the language in other CoCo bond documents gives regulators discretion to write down the value of those bonds. The fact that central banks worldwide have been happily hiking rates amid global bank runs hasn’t helped the situation.

Credit default swaps (a relatively illiquid market) for Deutsche Bank have surged to a four-year high this morning as investors poke at the bank’s stock and bonds for any evidence of underlying problems. Defenders have cited the bank’s healthy common equity tier one capital (CET1) ratio of 13.4% and the fact that the ratings agencies had been recently upgrading the bank’s credit rating, but for now, the bank’s reputation is all the probable cause the bank vigilantes need.

The trouble in European markets has made its way over to US markets as bank stocks are all trading lower, crude oil is down sharply, and treasuries are as popular as a Taylor Swift concert ticket. There have been some wild moves across financial markets in activity that has been anything but orderly. The two-year Treasury market is a perfect example where 20 bps daily moves in yield, while previously uncommon, have become the norm. Just over two weeks ago, the two-year yield was over 5%. This morning, the yield is at 3.56%. Who’s running this market? Ticketmaster?

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke 50 Growth Stocks — 3/23/23

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were 18 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

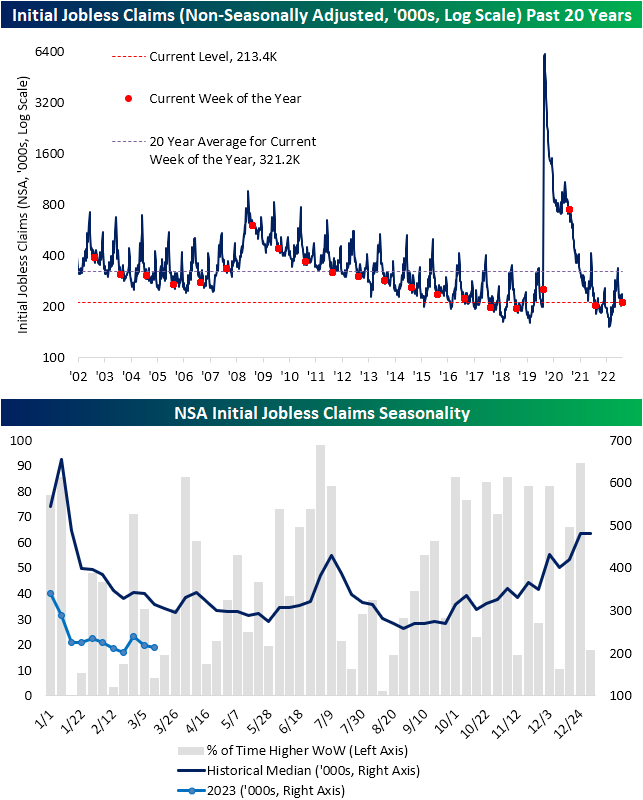

Seasonality Keeps Claims Below 200K?

Initial jobless claims remained healthy this week with another sub-200K print. Claims fell modestly to 191K from last week’s unrevised reading of 192K. That small decline exceeded expectations of claims rising up to 197K. Given claims continue to impress, the seasonally adjusted number has come in below 200K for 9 of the last 10 weeks. By that measure, it has been the strongest stretch for claims since last April when there were 10 weeks in a row of sub-200K prints. Prior to that, from 2018 through 2020 the late March and early April period similarly saw consistent readings under 200K meaning that some of the strength in the adjusted number could be on account of residual seasonality.

In fact, this point of the year has some of the weeks in which claims have the most consistently historically fallen week over week. Taking a historical median of claims throughout the year, claims tend to round out a short-term bottom in the spring before an early summer bump. In other words, seasonal strength will begin to wane in the coming months.

While initial claims improved, continuing claims worsened rising to 1.694 million from 1.68 million the previous week. Albeit higher, that remains below the 2023 high of 1.715 million set at the end of February.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.

A Fed Day Like Most Others

Yesterday’s Fed decision and comments from Fed Chair Powell gave markets plenty to chew on. As we discussed in last night’s Closer and today’s Morning Lineup, there have been a number of conflicting statements from officials and confusing reactions in various assets over the past 24 hours. In spite of all that uncertainty, the S&P 500’s path yesterday pretty much followed the usual script. In the charts below we show the S&P’s average intraday pattern across all Fed days since Powell has been chair (first chart) and the intraday chart of the S&P yesterday (second chart). As shown, the market’s pattern yesterday, especially after the 2 PM ET rate decision and the 2:30 PM press conference, closely resembled the average path that the market has followed across all Powell Fed Days since 2018.

The S&P saw a modest bounce after the 2 PM Fed decision and then a further rally right after Powell’s presser began at 2:30 PM. That initial post-presser spike proved to be a pump-fake, as markets ultimately sold off hard with a near 2% decline from 2:30 PM to the 4 PM close.

So what typically happens in the week after Fed days? Since 1994 when the Fed began announcing policy decisions on the same day as its meeting, the S&P has averaged a decline of 10 basis points over the next week. During the current tightening cycle that began about a year ago, market performance in the week after Fed days has been even worse with the S&P averaging a decline of 0.99%. However, when the S&P has been down over 1% on Fed days (like yesterday), performance over the next week has been positive with an average gain of 0.64%. As always, past performance is no guarantee of future results.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.

Bespoke’s Morning Lineup – 3/23/23 – Always Keep ‘Em Guessing

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“These contradictions are not accidental, nor do they result from ordinary hypocrisy: they are deliberate exercises in doublethink” – George Orwell

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

In foreign relations, a policy of strategic ambiguity can often be effective. Conflicting messages regarding responses to a potential action leave all actions on the table and keep the parties involved guessing regarding any reaction you might have. The US has been employing this strategy with respect to China and Taiwan. Over the years, various officials have repeatedly given conflicting messages regarding how we would respond to a Chinese invasion or if Taiwan sought to declare independence. By doing this, it keeps China from invading under the threat of a US military intervention, but by also supporting the one-China principle, Taiwan has refrained from declaring independence from China. It may not be a long-term answer, but in the short term, it maintains the status quo.

One area where a policy of strategic ambiguity may not be as effective is in the handling of a banking crisis. Within the span of under 30 minutes yesterday, we saw the heads of the Federal Reserve and US Treasury give somewhat conflicting signals regarding the US banking sector. At 3 PM Eastern, Treasury Secretary Janet Yellen told a Senate Committee that she is not considering a broad increase in deposit insurance at US banks. Besides the fact that she made somewhat contradictory remarks just a day earlier, her statement seemed to be the complete opposite of FOMC Chair Powell who said just a few minutes later in his post-meeting press conference that the Fed has the tools to protect depositors and is prepared to use them in order to safeguard deposits. Given the conflicting signals, most rational investors would not stay put thinking that there is a good chance their deposits are safe, they would step on the gas and get out of dodge!

The conflicting signals given by Powell and Yellen yesterday certainly didn’t instill a whole lot of confidence on the part of investors, and that helped spark a sharp late-day sell-off in equities towards the close. From the end of Powell’s press conference through the closing bell, the S&P 500 sold off more than a full percent to finish right near the lows of the day.

Powell made another subtle shift in his messaging yesterday. While he has tended to kick off prior speeches lately with an adamant anti-inflation message (remember Jackson Hole), that wasn’t in yesterday’s speech. Instead, he used the opportunity to highlight the ‘decisive’ actions taken by the Federal Reserve and Treasury to address and contain the crisis and keep the banking system ‘sound and resilient’. If you thought the omission of the anti-inflation message was a sign of a more dovish Powell, though, he tried to dispel any notions of that when he closed out his press conference with the statement “I mentioned with rate cuts, rate cuts are not in our base case. And you know, so that’s all I have to say, so.” Always keep them guessing!

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

FANG+ Flying

As we noted in today’s Morning Lineup, sector performance has heavily favored areas like Tech, Consumer Discretionary, and Communication Services in recent weeks. Playing into that sector level performance has been the strength of the mega-caps. The NYSE FANG+ index tracks ten of the largest and most highly traded Tech and Tech-adjacent names. In the past several days, that cohort of stocks is breaking out to the highest level since last April whereas the S&P 500 still needs to rally 4% to reach its February high.

Although FANG+ stocks have been strong recently, that follows more than a full year of underperformance. As shown below, relative to the S&P 500, mega-cap Tech consistently underperformed from February 2021 through this past fall. In the past few days, the massive outperformance has resulted in a breakout of the downtrend for the ratio of FANG+ to the S&P 500.

More impressive is how rapid of a move it has been for that ratio to break out. Below, we show the 2-month percent change in the ratio above. As of the high at yesterday’s close, the ratio had risen 22.5% over the prior two months. That comes up just short of the record (22.6%) leading up to the pre-COVID high in February 2020. In other words, mega-cap Tech has experienced near-record outperformance relative to the broader market. However, we would note that this is in the wake of last year when the group had seen some of its worst two-month underperformance on record with the worst readings being in March, May, and November.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.

Bespoke’s Morning Lineup – 3/22/23 – Now Batting

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Those who have the task of making such policy don’t expect you to applaud.” – William McChesney Martin

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

There’s no economic data on the calendar and there’s little in the way of earnings news to focus on this morning, so for the next six hours, we’ll only have the Fed to worry about. Markets are still overwhelmingly pricing in a 25 bps hike with the current odds at close to 90%. It’s hard to imagine a rate hike given the weakening macro backdrop and the crisis in the banking sector, but those are the numbers, and at this point, there have been little signs of the problems spreading.

The fact that UK CPI just printed its sixth straight month of double-digit y/y increases and ECB President Christine Lagarde was out saying she doesn’t see clear evidence that inflation is trending down doesn’t help the cause of those calling for a pause. Those are trends literally an ocean away, though, and over on this side of the Atlantic, just about every inflation indicator we track has been trending lower. Whatever decision the FOMC makes, it’s safe to assume that there will be no shortage of critics after the fact, and we don’t envy the position that Powell is in.

Heading into today’s rate decision, most sectors have traded down over the last week with Real Estate and Energy leading the way lower. Surprisingly, in the middle of a banking ‘crisis’ Financials isn’t even the worst performing sector as it is down less than 1% over the last five trading days and isn’t even the worst performing sector on a YTD basis. Sure, it’s down over 6.5%, but Utilities and Energy are also both down more than the Financials.

While Financials, Utilities, and Energy have been a drag on the market, Communication Services, Technology, and Consumer Discretionary have been the main drivers of gains this year. Not only are they the only sectors up more than 1% on the year, but they’re also all up over 10%, so these three sectors are basically in a league of their own versus the rest of the field.

Lately, Technology has been the clear leader. It’s only the second-best performing sector YTD, but its further above its 50-DMA than any other sector, and it’s on the verge of breaking out of the sideways range it has been in for the last two months.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Morning Lineup – 3/21/23 – All Quiet (For Now) on the Banking Front

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Bank failures are caused by depositors who don’t deposit enough money to cover losses due to mismanagement.” – Dan Quayle

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

There’s been no new news on the banking front this morning, and investors are taking the lack of news as an excuse to rally. US futures are up about 0.80% as treasury yields spike higher. Ahead of tomorrow’s fateful Fed decision, the only economic report on the calendar is Existing Home Sales at 10 AM today.

With an increase of ‘just’ 14 basis points (bps), yesterday broke a streak of seven straight days that the yield in the yield of the 2-year US Treasury had a daily move of more than 20 bps. Another record streak that continued, though, was the fact that the 2-year yield traded with an intraday range of at least 30 bps. Going back to 2000, which is as far back as we have intraday data for the 2-year yield, the current six-trading day streak of 30+ bps intraday moves is now longer than the five-trading day streak in September 2008 after the Lehman bankruptcy.

Not only is the current streak of wide daily ranges a record, but it also included what was a record single-day intraday range. Last Wednesday, the 2-year yield’s intraday range spanned a low of 3.71% to a high of 4.41%. That 70-bps range was a full 10 bps more than the prior record of 60 bps back on 9/19/08. Is that enough action for you?

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke Triple Play Report — 3/21/23

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with above-expectations results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 14 stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan