Morning Lineup – Hamptons Houses Piling Up

100 companies have reported earnings so far this morning, in what is the busiest day of earnings for the reporting period. This also comes on the heels of a busy after-hours session on Wednesday where Microsoft surged and saw its market cap exceed $1 trillion. Facebook (FB) also reported a strong quarter pushing that stock close to $200 per share. This morning, the mood is not as positive as a big earnings miss from 3M (MMM) has that stock trading down over 8% and taking the DJIA futures down with it. In economic data, South Korea reported a surprise contraction in GDP overnight (weakest in ten years).

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

If you are looking for a real-world example of how tax policy can impact the economy, look no further than the Hamptons area of Long Island. With last year’s GOP tax overhaul capping deductions for mortgage interest and property taxes, sales of second homes have been hit hard. According to a Bloomberg article this morning, the number of Hamptons luxury houses with “For Sale” signs in front of them swelled to 869 at the end of the first quarter. That’s nearly triple the number that were listed for sale at the same time last year and is the highest level in at least seven years. While inventories of luxury homes in the Hamptons are ballooning, sales are falling off a cliff as Q1 sales in the region were the lowest for the first three months of the year in at least seven years!

Based on the trends of rising inventories and slowing sales, the article goes on to say that at the current pace it would take 7.5 years to sell the available inventory of luxury homes- another record. The article went on to quote the President of one firm as saying that the market is in a period of ‘transition’. That would be putting it mildly!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Flat Morning After Record Highs

In another busy morning for earnings, we have already seen more than 50 companies report, and like yesterday, the EPS beat rate among these companies has been very strong at 67%. Unlike yesterday, though, the revenue beat rate hasn’t been nearly as strong as just under half of the companies reporting so far have managed to post better than expected revenues.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

With the S&P 500 closing just above its former record high yesterday, one would think the last seven months have been nothing more than running on a treadmill for the stock market. A look deeper, though, shows that there has been no shortage of big winners (and losers) in terms of industries.

The table below shows the ten best and worst performing S&P 500 industries since the S&P 500’s 2018 closing high on 9/20. Eight of the biggest winners are all up over 10%, including one – Power & Renewable Electricity- which is up over 20%. Who would have thought that an industry from the Utilities sector would have led the market? Outside of Utilities, Technology has been a big contributor to the market’s strength with three industries in the top ten (Communications Equipment, Software, and Semis). Another surprising sector with representation on the list is Consumer Staples. Both the Personal Products and Household Products industries are up 14.8% since the S&P 500’s 2018 high.

On the downside, Energy has been a drag as Energy Equipment and Services has dropped over 23% since 9/20 while Oil, Gas & Fuels is down 6%. One would think that with oil prices so high, that this group would have done better, but no such luck. Two groups that have felt the pinch from higher energy prices (and other issues like the 737) are Airlines and Air Freight. Both of these industries from the Industrials sector are down close to 10%.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Earnings Season Wakes, Gold Goes to Sleep

With markets around the world all open following a holiday on Monday for many, the mood is mixed although US futures are right near their highs of the morning. The catalyst in the US is solid earnings reports. Of the nearly 50 names that have reported so far this morning, two-thirds have exceeded EPS forecasts. More impressive, however, is the fact that two-thirds of those companies reporting have also exceeded top-line revenue estimates. It’s only one morning’s worth of data, but it is also the busiest day of earnings so far this reporting period.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s an interesting chart to start your day:

As earnings season has come to life, gold has completely flat-lined in the last few trading days. Take a look at the chart below which shows the YTD performance of the SPDR Gold Trust ETF (GLD). Over the last four trading days, the spread between the intraday high and low over that period has been just 0.40%. While that narrow a spread is notable enough, its the third time this year that GLD has gone into one of these four-day nap periods where the spread between the intraday high and low was less than 1%! Like the last two, will this one be another pause that refreshes?

What’s even more notable about the recent narrow range for GLD is that since the ETF started trading in 2005, there has never been a four-day period where the spread between the intraday high and low over those four days has been narrower. Volatility isn’t just lower in the equity market as gold has become increasingly less volatile in recent years.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Slow Start to a Busy Week

Markets are easing investors back into the mix after the three-day weekend as European markets remain closed. US futures are trading lower this morning, while crude oil is ripping after the US will reportedly not extend Iranian oil waivers when they expire on 5/2. The economic calendar is relatively quiet today with the Chicago Fed NAI at 8:30 and Existing Home Sales at 10:00 Eastern.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

You wouldn’t know it by the pace of reports today but this week and next are the two busiest of the Q1 earnings season as more than 300 companies in the S&P 500 are scheduled to report. The peak day for earnings of S&P 500 companies comes on Thursday (4/25) when 64 companies will report. Today, though, only seven companies are on the calendar. The next time there will be a day with fewer reports isn’t until May 10th!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – A Flood of Data

Futures have turned a little higher this morning ahead of what is an absolute flood of economic data. Retail Sales, the Philly Fed, and Jobless Claims were just released, and the results were mostly better than expected with Retail Sales coming in better than expected, Jobless Claims dropping to an astonishingly low level of 192K, but the Philly Fed slightly missing consensus forecasts. There’s still a lot more data to contend with, though, as Markit Flash PMIs, Leading Indicators, and Business Inventories are still on the docket. Tomorrow is a holiday for the stock market in observance of Good Friday, but both Housing Starts and Building Permits will be released at 8:30. If you are off, enjoy the three day weekend.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

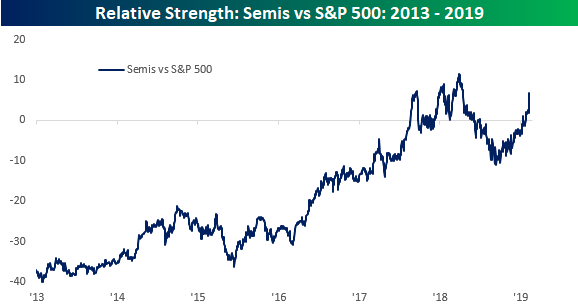

Here’s a snippet from today’s report:

Following the recent settlement between Apple and Qualcomm (QCOM), we wanted to check up on the status of our comparison between the relative strength of semiconductors and the performance of the S&P 500. We have highlighted the leadership of semis numerous times in the last several weeks, and QCOM’s surge over the last two days has caused the group’s relative strength to soar to levels not far from last year’s high. As we have mentioned in the past, every major decline and rally of the last six years has been preceded by a move higher or lower in the relative strength of the semis. Emphasis is often placed on the importance of the transports in determining the direction of the market, but in recent years the semis have been a much better tell.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Still Settling Up

After a big surge yesterday, shares of Qualcomm (QCOM) are still finding an equilibrium in the wake of yesterday’s settlement with Apple (AAPL). After a bunch of upgrades this morning, the stock is up another 11%. Yesterday’s news between the two companies also gave Intel (INTC) an opportunity to exit the smartphone modem business (AAPL was its primary customer), which was considered an inferior offering to QCOM’s. With that news, INTC’s stock is rallying close to 5% as the knock-on effects of this major deal (details of which are scant) continue to shake out.

In earnings news this morning, the picture isn’t quite as pretty as it was yesterday. Of the thirteen companies that have reported so far today, just 62% have exceeded EPS forecasts while slightly more than half (7) have managed to exceed top line results.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Here’s a snippet from today’s report:

We have a lot to get to in this morning’s report, but below we wanted to highlight one interesting aspect in terms of where global equity markets stand now compared to three months ago. If you haven’t looked at equity index charts from around the world recently, it may surprise you to know that as of yesterday’s close no less than seven major national indices are within 1.5% of new 52 week highs on a closing basis with India and China marking their best closes of the past year. Another 7 major country indices are within 6% of that level, and only one (Malaysia’s Bursa Malaysia Index) is more than 11% below 52-week closing highs.

In the left chart below, we show distance from 52-week closing and intraday highs for the global markets covered in our Global Macro Dashboard. What a change it’s been over the last three months. In the second chart at right below, we show the same metrics as-of three months ago. Only 2 indices were within 6% of 52-week highs at that point, and seven were at least 15% below their best levels of the year prior. The risk asset rally since the end of December has lifted a lot of ships. With this kind of backdrop, one would think central banks around the world would be more biased towards tightening than cutting! For an updated set of charts and other metrics covering each of the countries below, make sure to check out our weekly Global Macro Dashboard.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.