Jul 11, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have thought it my duty to exhibit things as they are, not as they ought to be.” – Alexander Hamilton

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After a nice week to kick off the quarter, we are seeing some giveback this morning as all of the major US averages are indicated to open lower. Along with weaker stock prices, crude oil, gold, and crypto are joining the downward bias. Treasuries, however, have bucked the trend with the 10-year yield trading down near 3%.

This week will be an important one for the markets with some key economic data (CPI, PPI, and Retail Sales) as well as the start of earnings season, but it’s starting off slow as there are no significant economic reports and the only earnings report of note is from Pepsi (PEP) after the close.

In today’s Morning Lineup, we discuss moves in Asian and European markets and economic data from around the world.

Last week was a pretty good one for US equities with the S&P 500 up nearly 2% and the Nasdaq up over 4%. Even after the gains, both the Nasdaq and the S&P 500 failed to close above their 50-day moving averages (DMA). The Nasdaq is just fractionally below that level, and the S&P 500 is over 1.5% below its 50-DMA. While the Nasdaq wasn’t able to re-take its 50-DMA, it does appear to have broken a downtrend that has been in place since the Spring. The S&P 500, on the other hand, also remains below its downtrend from the Spring, so it still has more work to do on the upside. Just as the 50-DMA tends to act as support in uptrends, it tends to act as a headwind during downtrends, so this week should prove to be a critical one as we get deeper into Q3. A failure on the part of the indices to break above their respective downtrends or reclaim their short-term moving averages could set the market up for a long earnings season.

Last week’s rally was dominated by the ‘trash’ as the year’s three worst performing sectors were the leaders last week. Consumer Discretionary rallied 6.5% over the last five trading days (July 1st through last Friday), while Technology and Communication Services both surged 4%. Even after these gains, all three sectors are still down well over 20% YTD. On the downside, it was generally the year’s winners that lagged last week as Energy and Utilities both experienced fractional declines. One outlier to the trend was Materials. It was the worst-performing sector over the last five trading days and it is also the fifth worst-performing sector YTD, and one of just two oversold sectors.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jul 8, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Our predecessors overcame many troubles and much suffering, but each time got back up stronger than before.” – Shinzo Abe

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

US futures have been negative most of the morning ahead of today’s jobs report, but they have been improving from earlier levels, and the Dow is even indicated to open slightly higher as we type this. This is all subject to change, though, as the June employment report will be released shortly. Expectations are for an increase of 268K, which would be the lowest monthly reading since the start of 2021, but the real focus will likely be on average hourly earnings which are expected to increase by 0.3%.

Outside of equities, US treasury yields are modestly lower, but the 2s10s yield curve remains inverted for the fourth straight day. Crude oil and gold are basically flat, and copper is down nearly 2%.

In today’s Morning Lineup, we discuss moves in Asian and European markets and economic data from around the world.

With a good deal of emphasis being placed on today’s employment report, we wanted to take a quick look at how the headline payrolls report has come in relative to expectations over the last year. In the last 12 monthly reports, the headline number has exceeded expectations seven times and missed forecasts five times. Looking at the chart, though, the margin of the misses has been much larger than the magnitude of the beats. In four of the five misses, the actual reading came in more than 250K below forecasts, and the overall average miss was 291K. In the seven beats, however, the average beat was just 143K or less than half of the magnitude of the average miss. Applying the average miss to today’s report, if the June report missed expectations by the ‘average’ amount of the last year, it would be a negative reading. A lot of ifs there, but just helps to put things in perspective.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jul 7, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Politics is not a game, but a serious business.” – Winston Churchill

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Given the state of politics on both sides of the Atlantic, most would probably take issue with Churchill’s description of the political process, especially the second part. Anyway, it’s always interesting to see instances where a CEO announces his or her resignation from a company and its stock rallies. How must the individual leaving the company feel watching the market cap of the company rise now that they’re gone? Talk about a lack of a value-add! Anyway, as bad as it must make a CEO feel, how must Boris Johnson feel today that British stocks and the pound are all rallying on news of his resignation? There’s a reason you need a thick skin to be successful in politics.

Stocks aren’t just rallying in Europe this morning as major indices around Europe and the world along with US futures are all in positive territory. The S&P 500 has been higher in each of the last three trading days, and if early gains hold today would be the fourth straight day of gains. In order to get there, though, we’ll have to get through Jobless Claims at 8:30, Energy inventories at 10:30, and then two Fed speeches from Waller and Bullard this afternoon. Jobless claims came in at 235K which was slightly higher than expected and the highest level in nearly six months.

In today’s Morning Lineup, we discuss moves in Asian and European markets, reports of a $200+ stimulus plan in China, and economic data from around the world.

As mentioned above, if today’s early gains hold today would be the fourth straight day of gains for the S&P 500. That may not sound all that impressive (it isn’t), but in a year like 2022, it is enough to be tied for the longest winning streak of the year. Earlier this year in Q1, there were three other streaks of similar duration, but in Q2, the best the S&P 500 could do was three days.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jul 6, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no free market for oil. It’s controlled by a cartel, OPEC.” – Frederick W. Smith

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Stocks are poised for a lower open this morning, oil prices are clinging to $100, and the 2s10s yield curve is modestly inverted. While equity futures have been lower all morning, they have been trading in a relatively tight range. That’s likely to change at around 10 AM Eastern with the release of the ISM Services report and the May JOLTS report. Then at 2 PM, we’ll get the release of the Fed minutes from the June meeting.

In today’s Morning Lineup, we discuss moves in Asian and European markets, along with a quick look at the latest moves in the euro and the developments in UK politics.

Less than a month ago today on June 8th, the S&P 500 Energy sector was up over 65% YTD, up more than 60 percentage points more than the next closest sector, and 90 percentage points ahead of the worst performing sector (Consumer Discretionary). Since then, Energy stocks have come crashing back down to earth, and while it remains the only sector up YTD, its lead over other sectors has narrowed.

With a YTD gain of 28.1%, the Energy sector ETF (XLE) leads the next closest sector, Utilities, by nearly 30 percentage points and still has a lead of nearly 60 percentage points over the worst-performing sector – Consumer Discretionary.

When we look at how far the Energy sector has declined from its 52-week high and compare that decline to how far other sectors have dropped from their 52-week highs, Energy is no longer a standout. In fact, with Energy down 25.3%, it has now declined more from its 52-week high than the S&P 500 has declined from its high (-20.4%). Of the eleven sectors, only three – Technology (XLK), Consumer Discretionary (XLY), and Communication Services (XLC) – have seen larger drawdowns from their respective highs than the Energy sector.

Investors tend to view their holdings from the lens of where they are trading relative to their peaks. With Energy now down just as much or more than most other sectors, plus the fact that a lot of inflows into the sector likely came closer to the June high, even the one sector that has been a bright spot for the market is probably not making too many investors happy these days.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jul 5, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Know your strengths and take advantage of them.” – Greg Norman

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Bulls checking the market before they went to sleep last night probably breathed a little sigh of relief that futures were higher following Friday’s rally. At least they slept OK. Waking up this morning, those dreams of gains turned into the reality of losses, and stocks are poised to open back up in the red for the quarter. Welcome back to 2022.

Recession fears are front and center again this morning, especially in Europe as concerns of natural gas shortages heading into the winter months put the likelihood of recession as near certain with the only question being how long and how deep.

On the calendar today, the only economic reports of note are Factory Orders and Durable Goods at 10 AM.

In today’s Morning Lineup, we discuss moves in Asian and European markets, a recap of the plunge in the euro, and more.

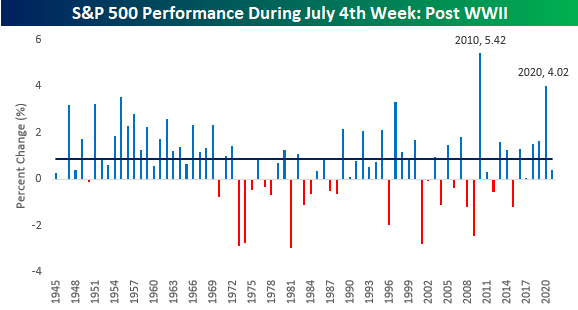

July 4th is usually a period when Americans are brimming with patriotism and that possibly helps to explain why equities have historically performed so well during the holiday week. In the post-WWII period, the S&P 500 has had a median gain of 0.88% during the July 4th holiday week with positive returns over 70% of the time (71.4%). The two best July 4th holiday weeks were in 2010 (5.42%) and 4.02% just two years ago in 2020. As shown in the chart, the S&P 500 heads into this year with a six-year run of positive returns during July 4th week, but that pales in comparison to the 19-year run from 1951 through 1969 when the S&P 500 averaged a 1.79% average weekly gain.

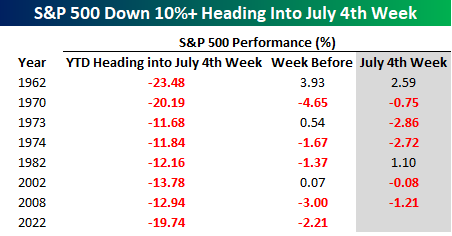

With the S&P 500 down just under 20% heading into this week and down 2.2% last week, will the patriotism of July 4th be enough to offset the pessimism regarding the market and economy? It’s going to be tough. The table below lists the seven prior years since WWII that the S&P 500 was down more than 10% heading into July 4th week. In those seven years, the S&P 500’s average performance during the July 4th week was a decline of 0.56% (median: -0.75%) with positive returns just two out of seven times.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Jul 1, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Remember too that your time is your one finite resource, and when you say “yes” to one thing you are inevitably saying “no” to another.” – Andrew S Grove

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures are picking up in Q3 right where they left off in Q2, but the declines have been contained to this point. Weak guidance from Micron (MU) as well as further concerns regarding the health of the consumer following profit warnings in the retail sector haven’t helped sentiment. Concerns are only more elevated that the economy is either already in or on the verge of a recession even as the Fed continues to press its case for more aggressive policy moving forward.

The only economic indicators of note today are the ISM Manufacturing for June and the May Construction Spending report. If global PMI data that has already been released today is any indication, don’t set your expectations all that high. Given the holiday weekend coming up, we would normally expect a Summer Friday like today to be on the quiet side, but given the way this year has played out, who knows.

In today’s Morning Lineup, we discuss moves in rates markets and what they’re pricing in regarding Fed policy, movements in Asian and European markets, a recap of global PMI data, and more.

As economic concerns have been ratcheted higher in recent weeks, we’ve seen a sharp pullback in US Treasury yields across the curve that followed the mid-June spike in reaction to the May CPI report and the preliminary UMich Confidence report. While yields remain elevated, the uptrend that had been in place since earlier this year appears to have been broken. Going forward, the path of interest rates, especially the yield on the 2-year, will go a long way in determining how stocks perform in the second half. If the pace of increases experienced in the first half continues in the second half, investors may be facing a long six months.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.