Nov 16, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You always hear the phenomenon that people are trading down, that’s not happening in our space.” – Marvin Ellison, CEO Lowe’s (LOW)

“Based on softening sales and profit trends that emerged late in the third quarter and persisted into November” Target (TGT) Earnings Release (11/16/22)

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After some geo-political tensions yesterday afternoon following reports of a Russian missile strike on Poland, markets are breathing a sigh of relief this morning after NATO said that the missile likely did not come from Russia and wasn’t an act of aggression. Despite the eased tensions, futures are modestly lower this morning following a mixed batch of earnings reports. Treasury yields are lower on continued optimism that inflation pressures in the US are easing (we’ll see what Fed officials think throughout the day as a number of speakers are on the calendar), but over in the UK, CPI rose by a 40+ year high of 11.1% y/y.

It looks like it’s a morning of the haves and have-nots in retail. Target (TGT) noted in its earnings release that sales trends are softening after reporting weaker-than-expected EPS and sales. Lowe’s (LOW) seems to be operating on a whole different landscape, though, as the company reported better-than-expected EPS and sales while raising guidance. In an interview on CNBC, CEO Marvin Ellison noted that he has seen no signs of a consumer slowdown and no sign of trading down. Two large American retailers with two entirely different viewpoints on the consumer. It will be interesting to see which comments today’s Fed speakers decide to place more weight on. Getting back to the Lowe’s report, while Ellison noted that consumer trends remain strong, he also added that input prices are starting to trend down, so even from the strong report, there were some positive signs on the inflation front… but it’s just ‘one data point‘.

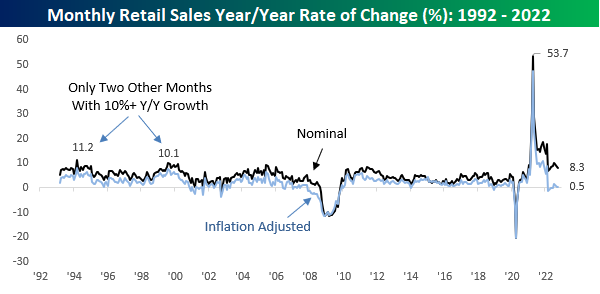

It’s only fitting that right in the thick of retail earnings season, we’re also getting the monthly update on Retail Sales for October this morning. The report came in stronger than expected with headline Retail Sales rising 8.3% on a y/y basis. While that’s strong at the surface, keep in mind that Retail Sales are a nominal reading. After adjusting for inflation, the y/y reading was up 0.5%.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Nov 15, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Hunches and the mysterious ticker-sense haven’t so very much to do with success.” – Edwin Lefèvre, Reminiscences of a Stock Operator

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We’re now in the thick of retailer earnings season, and this morning’s two big reports were from Home Depot (HD) and Walmart (WMT). The former is trading modestly lower after reporting better-than-expected EPS and sales while reaffirming guidance. WMT, meanwhile, is surging over 6% after a better-than-expected report and announcing a $20 billion stock buyback. More importantly, inventory levels at the company appear to be coming under control as management guided last quarter. It’s been a roller-coaster ride for WMT this year. After plunging this summer on a profit warning, the stock has recovered all of its losses, and based on where it is trading in the pre-market is now up on the year.

WMT’s positive report has contributed to a positive tone in the futures market. Equities are firmly higher, led by the Nasdaq which is up well over 1%, crude oil is marginally lower, and the ten-year yield is lower. This could all change at 8:30 with the release of the October PPI, but for now, rising stock prices accompanied by lower rates and lower oil prices are more than any bull could ask for.

The spread of the internet during the mid to late 1990s is traditionally regarded as a key catalyst behind the birth of day trading in the stock market. The internet spawned online investing which enabled anyone with available funds to set up a brokerage account and point and click their savings away. Day trading became popular during the dot-com bubble (and again during the COVID lockdowns when consumers flush with cash and nothing to do started trading on their mobile phones on apps like Robinhood), but day traders have been around much longer than that. The founding of the Nasdaq in 1971 and its electronic platform facilitated the practice of more rapid trading, but day trading traces its roots all the way back to the late 1800s following the invention of the ticker tape which was first unveiled on this day 155 years ago.

Prior to Edward Calahan’s invention of the ticker tape, the only way stock prices were disseminated was by word of mouth, through the mail, or by messenger, and you can’t really day trade when you’re getting stock quotes through the mail (even FedEx didn’t start until 1971). Calahan’s invention unlocked the opportunity for anyone with a telegraph line and enough money to pay for a feed to set up a ticker tape and get ‘real-time’ stock quotes (actually delayed by a minimum of 15 minutes but still real-time in 1800s terms). The ticker tape sped up the flow of information and enabled investors to make more well-informed decisions, but it also spawned the creation of bucket shops and other types of venues in cities across the country where traders could go and bet on the direction of stock prices intraday.

Throughout society and culture, we use all sorts of common phrases without even thinking about them (bite the bullet, hands down, etc). In the investment sphere, ‘don’t fight the tape’ is one of them. Without the invention of the ticker tape, there would have been no tape to fight for the last 155 years! Instead, investors would be ‘fighting the mail’ or the messenger (although from a messenger’s perspective being fought with certainly sounds a lot better than being ‘shot’).

When it comes to sentiment lately, consumers don’t seem to be fighting the tape. The latest example we can cite came in yesterday’s monthly update to the NY Fed’s Survey of Consumer Expectations. You may have seen some headlines highlighting the fact that both short-term and long-term inflation expectations ticked higher, but sentiment toward the stock market remains right near the lowest levels in the history of the survey (2013). As shown in the chart below, barely more than a third of investors expect the stock market to be higher one year from now. The only month with a lower reading was in June when it ticked down to 33.8%.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Nov 14, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is not down on any map; true places never are.” – Herman Melville, Moby Dick

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

After a CPI-fueled monster rally last week where US stocks had one of their best weeks of the year, the tone in equities to kick off the new week has been muted. Futures were lower overnight and remain in the red as we type this, but they have been gradually moving up off their overnight lows. Treasury yields are higher this morning, but the 10-year yield is still below 3.90% for now. If you were looking for signs of a Fed pause after last week’s relatively benign inflation print, Fed Governor Christopher Waller wants you to think again. Bloomberg is reporting that the governor says “we’ve still got a ways to go” not before the Fed starts cutting rates but before it even stops raising rates. He went on to say that last Wednesday’s CPI report was good news but just one data point. We’ll grant the governor that October’s CPI may have been just one data point in the CPI series, but has he noticed the myriad of other pieces of data in the last few months that show inflation pressures have been easing, not to mention the fact that we’ve just seen one of the most aggressive paces of monetary tightening in a six-month span?

After rallying more than 14% off its October lows, Europe’s benchmark STOXX 600 index opened and traded above both its 50 and 200-day moving average for the entire session on Friday and is on pace to do the same thing again today. That’s something we haven’t been able to say since January. Perhaps even more impressive than the 14% rally in local currency is the fact that in dollar-adjusted terms, the STOXX’s performance off the October lows has been a gain of just over 20%. The next level to watch for European stocks is the high from August. Despite their short-term outperformance, European stocks remain in a deep hole relative to the US. Over the last five years, the STOXX 600 is up 32% in dollar-adjusted terms while the S&P 500 has rallied 69%.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Nov 11, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Honor to the soldier and sailor everywhere, who bravely bears his country’s cause. Honor, also, to the citizen who cares for his brother in the field and serves, as he best can, the same cause.” – Abraham Lincoln

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We’re seeing some modestly positive follow-through to yesterday’s ripper in early trading as the bond market is closed for Veterans Day. With banks and the bond market closed, there’s little in the way of earnings news or economic data. The only report on the calendar is the Michigan Confidence report at 10 AM. The key metric to watch in that report will be inflation expectations. Outside of the US, Asian markets rallied sharply in a continuation of Thursday’s rally here in the US, but signs of some loosening in China’s strict zero-Covid policy have also contributed to the positive mood. A reopening of China would likely have some upside inflationary pressure in terms of energy prices, but it would also loosen some supply chains which remain constrained.

There’s been nothing ‘semi’ about the performance of chip stocks over the last week, and some of the gains we have seen in individual stocks have been unbelievable. Just yesterday, the Philadelphia Semiconductor Index (SOX) was up over 10%, and over the last five trading days, the index is up over 16%. With gains like that, you can only imagine how some of the individual components of the SOX have performed, and below we summarize the performance of the 15 largest stocks in the index based on market cap. All 15 of them have experienced double-digit moves and four are up over 20% in the last five trading days. Even Intel (INTC) is up over 10%!

While the short-term gains have been mouth-watering, coming back to reality, all 15 stocks listed below are still down YTD, and most are down sharply. While Texas Instruments (TXN) and Analog Devices (ADI) have managed to get by with declines of less than 10%, more than half of the 15 stocks listed below are still down over 30% YTD. AMD has declined over 50% while NVIDIA (NVDA) and Taiwan Semiconductor (TSM) are both down over 40%. Whether this is the beginning of a new rally or just a bear market rally remains to be seen, but rallies have to start somewhere.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Nov 10, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“This is the most disappointing loss I have ever been associated with.” – Jimmy Johnson, 11/10/1984

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

You can take the positive futures with a grain of salt this morning as everything is likely to and will change following the 8:30 Eastern release of October CPI. Economists are currently forecasting the headline reading to increase by 0.6% m/m while the core reading is expected to be slightly more subdued at 0.5%. That report will be the main course, but don’t forget about jobless claims. Initial Jobless claims are expected to remain right around last week’s level of 217K. Not much is expected to change with regard to continuing claims either, but if the consensus reading of 1.487 million comes in, it would be the highest reading since April.

The words above could really be attributed to anyone who invested in financial assets of any type this year, but when Jimmy Johnson uttered them on this day in 1984, he was referring to his Miami Hurricanes and their role in one of the biggest blown leads in college football history. Playing Maryland, the Hurricanes took a 31-0 blowout into halftime in what was looking like a laugher. The Hurricanes of the 1980s were brash and known for their attitude, and they were also a team that most people outside of Miami eagerly rooted against.

That trash-talking Miami attitude was on full display back in 1984. As Maryland’s Jess Atkinson described it, “No question about it. Those guys were the biggest cheap-shot, trash-talking, classless outfit of football players I’ve ever seen in my life…You can almost take getting beat if a team is kicking your butts and they’re doing it cleanly. And there was no question that they were kicking our butts in the first half. But that team made us mad, and it gave us a little extra incentive.” Well, the Terps came out determined in the second half and led by QB Frank Reich coming off the bench and throwing six touchdowns, they were able to somehow complete one of the most unfathomable comebacks in college football history.

It’s amazing enough to lead a team to one of the greatest comebacks in college football history, but Reich also managed to find himself on the winning side of one of the greatest comebacks in NFL playoff history nine years later on a freezing January Buffalo afternoon. After trailing the Oilers 35-3 early in the second half, more than a few Bills fans left the cold and damp Rich stadium stands thinking about what could have been and looking ahead to next season. The Bills didn’t give up, though. One of his teammates reminded Reich that he had already been part of the greatest comeback college win, so perhaps he could do it again. Reich then went on to tell the team that they had to take the rest of the second half one play at a time. Using that play-by-play approach, the Bills staged a miraculous comeback as a wave of fans came back from the parking lots and filled the stands again to witness the 41-38 “Comeback” win.

As good a run of luck that Reich had in his football-playing career, his coaching career hasn’t been as lucky. While he had a big turnaround in his first season when the Colts made the playoffs after starting off the season at 1-5, the years since then have been somewhat uneventful. After starting this season with a record of 3-5-1, including a blowout loss to the Patriots last Sunday, Reich was unceremoniously fired by Colts owner Jim Isray.

Like the lucky streaks often seen in sports among teams or individual athletes, they all eventually end. 2022 has been a year where the market’s luck looks to have run out, and a Frank Reich comeback isn’t in the cards. Judging by various measures of sentiment, the only question now seems to be how much worse things will get. Even though we’re in what has historically been the best time of year for equities, individual investor sentiment, as measured by the American Association of Individual Investors, has shown a higher percentage of bears than bulls every week this year except one! As shown in the chart below, sentiment this year has been especially negative as there has only been one week where bullish sentiment exceeded bearish sentiment. Prior to 2022, there was no other year since 1987 where fewer than 25% of all weeks had more bulls than bears.

It’s been a terrible year. Everything that has happened, though, is in the past. Rather than looking back on the year and thinking about what could have been, investors always need to be looking forward and thinking of what could be.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Nov 9, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Once you replace negative thoughts with positive ones, you’ll start having positive results.” – Willie Nelson

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

If you thought the midterm elections were behind us, think again. Polls have been closed for nearly 12 hours in most jurisdictions, but the results of many contests are still up in the air. Markets hate uncertainty, so as you might expect, equity futures are lower heading into the opening bell, but the losses at this point, have been relatively contained. The economic calendar is quiet today, but tomorrow’s CPI looms on the horizon, and we’re still getting a heavy dose of earnings reports. The recent trend has not been nearly as strong as it was earlier in the reporting period as instances of lowered guidance have become increasingly common.

No matter what the results of the midterm elections were, people were going to wake up in a bad mood this morning. In some ways, the fact that there has been so little change in either direction only makes things worse since no one will be happy. Relative to expectations, Democrats clearly outperformed most expectations, though. Whatever your mood this morning, though, get over it. Like oil and water, politics and investing don’t mix, and you should never let your political ideology cloud your investment decisions. Relative to yesterday, very little has changed. The Fed is still aggressively hiking rates, the economy is weakening, and the stock and bond markets are at the tail end of one of their worst years in history.

As far as last night’s results go, nothing is final, but based on current estimates, the House looks like the razor-thin majority is going to shift from the Democrats to the Republicans, while Democrats are expected to maintain control of the Senate. Going back to WWII, it hasn’t been unprecedented to see smaller changes in the makeup of Congress during a midterm election, but this year’s results will likely end up near the more muted extreme at a time when no side had a decisive majority. Obviously, this is all subject to change, but what really stands out to us is how evenly divided the country is right now. The current rivalry between Republicans and Democrats stacks right up there with some of the biggest sports rivalries in history. Every two years the two sides completely go at it, taking things right down to the wire, and even many times ending up in overtime or a runoff somewhere to see which party comes out on top.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.