Dec 5, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What America needs now is a drink.” – Franklin Roosevelt, 12/5/33

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been a modestly positive week already, and futures are looking to modestly add to those gains with the S&P 500 up 0.20% and Nasdaq futures pointing to a gain of 0.3%. Bond yields are marginally higher on the day ahead of important (but stale) inflation data, and the 10-year yield is just below 4.12%. Crude oil and gold are little changed, but silver prices are up another 1.5% while copper is up just over 1%. Lastly, crypto prices are lower across the board, but the losses are contained at just 1.3% for Bitcoin.

In Asia, the Nikkei fell 1.1% but still managed to finish the week up 0.5% as yields at the long end of the curve continue to hit multi-year highs. Outside of Japan, though, other indices in the region are trading higher, finishing in positive territory for the week.

European stocks are higher across the board again this morning. The STOXX 600 is poised to close out the week with a gain of nearly 1%, while German stocks lead the region higher as factory orders rose more than expected. Q3 GDP for the entire Eurozone also rose slightly more than expected (0.3% vs 0.2% forecast).

It may have been a Tuesday, but for many Americans, December 5, 1933, probably felt like a Friday. Earlier in the day, Pennsylvania and Ohio had already ratified it, but at 5:32 PM Eastern time, the state of Utah became the 36th state to ratify the 21st Amendment. The amendment repealed the 18th Amendment, and with Utah’s passage, the 21st Amendment achieved the three-fourths majority required for it to become law, ending the nearly 14-year period of national Prohibition in the United States.

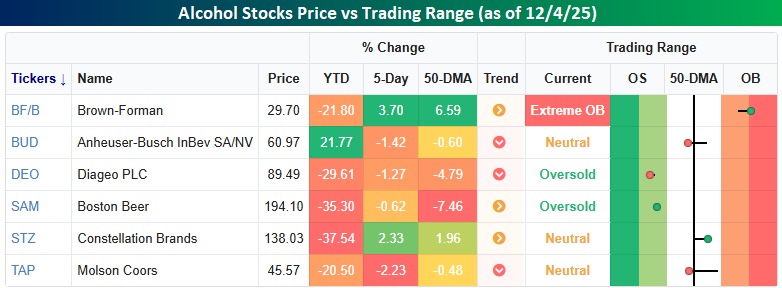

Liquor and tobacco stocks have historically been considered recession-proof investments for most of the last 100 years. However, in the last few decades, tobacco stocks have fallen out of favor due to escalating health concerns and heavy government regulation. In recent years, many of the same pressures surrounding tobacco have begun to affect the stocks of alcohol companies. Between emerging health concerns, the proliferation of GLP-1 treatments that suppress the urge to drink, and the rising popularity of cannabis, alcohol stocks have been taking punches from multiple directions.

As the snapshot illustrates, the majority of major alcohol purveyors have experienced significant Year-To-Date (YTD) declines, with most falling over 20%. While Anheuser-Busch InBev (BUD) may appear to be an outlier and is not down by the same extent, the broader trend is one of sharp underperformance across the sector. More recently, individual stock performance has been mixed: Brown-Forman (BF/B) has seen a multi-week rally, and Constellation Brands (STZ) is also currently trading marginally above its 50-day moving average (50-DMA).

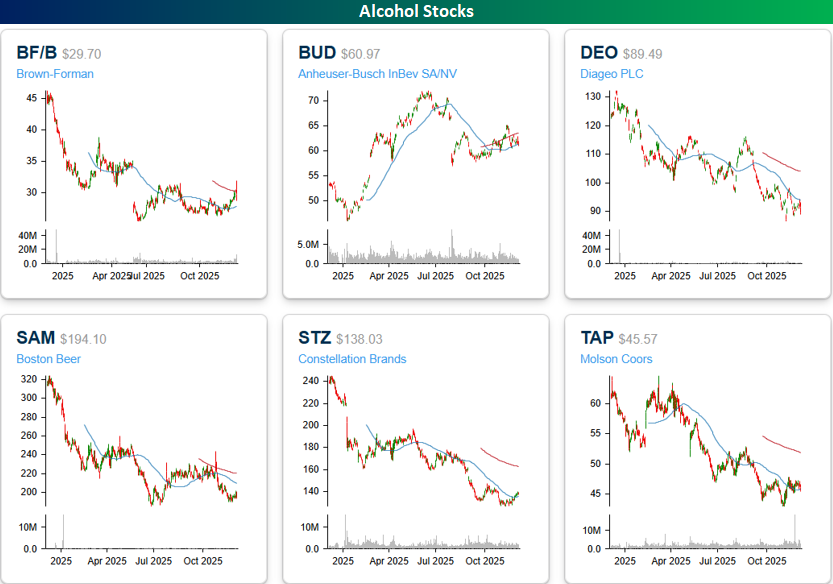

The one-year charts of these six stocks are a sobering picture of underperformance, making you want to grab a drink and drown your sorrows rather than celebrate. Even BUD, while up YTD, is down sharply off its high, but the other five stocks remain mired in steep downtrends.

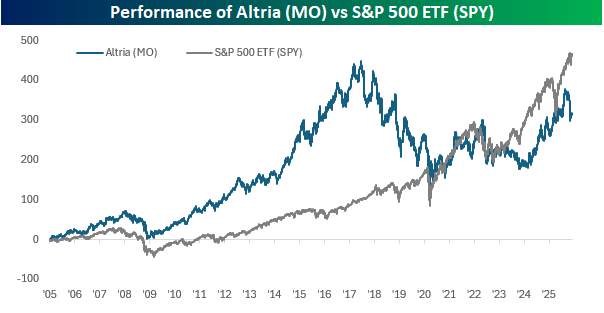

Finally, just because tobacco stocks have fallen out of favor, you could have done worse. As shown in the chart below, from a price perspective, shares of Altria (MO) underperformed the S&P 500, but not by a ton. What the price chart doesn’t account for is dividends. MO has a much larger dividend than the S&P 500, and when you take those dividends into account since the start of 2005, they add up. Had you reinvested dividends back into the stock, MO’s total return would have been over 1,300% compared to a total return of 730% in the S&P 500. Whatever you think of tobacco stocks and their impact on the health of the population, investing in them over the last twenty years has been anything but putting your money up in smoke. See you all at 5:32!

Dec 4, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s not the pace of life I mind. It’s the sudden stop at the end.” – Thomas Hobbes

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s very little going on in futures trading this morning as the S&P 500 and Nasdaq are both indicated to open ever so slightly higher. Treasury yields, meanwhile, are moving up about 3 bps across the curve, with the 10-year yield up near 4.10%. Crude oil is modestly higher, up 0.7%, but the big move remains in the natural gas space as prices are now above $5 for the first time in close to three years. In the metals space, gold and other precious metals are all lower, but the losses are contained at less than 1%. Even the crypto space is quiet as Bitcoin, Ethereum, and Solana are all up or down less than 1%.

In Asia, equities were mixed. While South Korea and China were marginally lower, Hong Kong finished up 0.7% while Japan surged 2.3%. Two catalysts behind the move were a strong 30-year JGB auction and a rally in tech stocks. Shares of Softbank rallied more than 9% following reports that it plans to increase its investment in OpenAI before the end of the year.

European stocks have been trading broadly positive this morning. The STOXX 600 is up 0.4%, and every major country’s benchmark index is trading up on the day. Germany is leading the way higher, up 0.8% as auto stocks rally following yesterday’s announcement from the Trump Administration that it would lower fuel-efficiency standards. Italy and the UK, however, are just barely hanging on to gains of 0.1%. In economic data, Retail Sales for the Eurozone were unchanged in October, and slightly higher than expected on a y/y basis (1.5% vs 1.4% forecast).

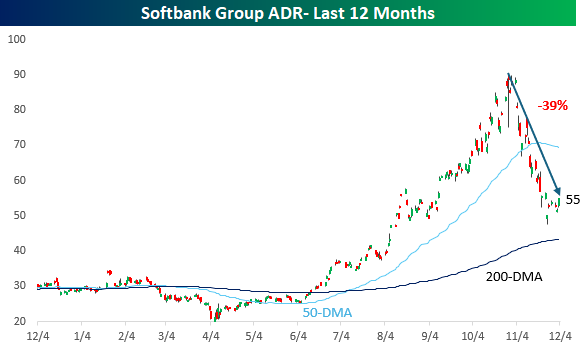

Getting back to Softbank, shares rallied 9% overnight, following a 6% gain on Wednesday. The chart below shows the performance of Softbank ADRs over the last year, and the last three months have been, to put it mildly, a roller coaster. Heading into today’s session, the stock is down 39% from its high in late October. Yet, despite that plunge, it was still 26% above its 200-DMA and 4% above where it closed 3 months ago. It’s hard to remember a stock that has plunged that much over six weeks, yet was still well above its long-term moving average and positive over the last three months.

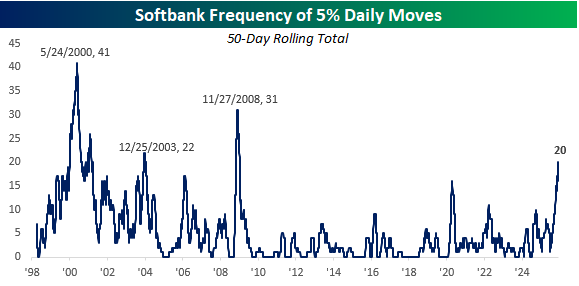

The volatility in Softbank is also evident in the day-to-day moves of Softbank stock. With last night’s 9% rally, the stock has now moved 5% or more in 20 of the last 50 trading days. To find a period where the stock saw more volatility in its day-to-day moves, you have to go back to November 2008. In the stock’s entire history, there have only been three periods when the stock had more 5% daily moves in a 50-trading-day span. The other two were in December 2003 and May 2000, when there were 41 in 50 trading days! It’s not like Softbank is a small-cap stock either. With a market cap of over $150 billion, it’s the fourth-largest stock in the Nikkei 225!

Dec 3, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Sometimes reality is too complex. Stories give it form.” – Jean Luc Godard

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view this morning’s Squawk Box interview, please click the image below.

Yesterday was a true turnaround Tuesday as the S&P 500, Nasdaq, and even Bitcoin erased most, if not all, of Monday’s declines. This morning, risk assets continued to move higher as the S&P 500 and Nasdaq both look to open 0.2% higher while Bitcoin tests $93K. Gold and other metals are also up 0.5% to 1%, and even crude oil is up 1% and back above $59 per barrel. Treasury yields are also moving lower for the second day in a row, with the 10-year yield back down to 4.06%.

After being starved of economic data for several weeks, this morning we’ll get ADP Employment and PMI readings for the services sector, both current reports. In addition, the backlog of data will continue to ease as September reports covering Import Prices (8:30), Industrial Production (9:15), and Capacity Utilization (9:15) will also hit the tape.

In Asia overnight, the Nikkei rallied over 1% as Hong Kong fell 1% while South Korea added on another 1.0% after Q3 GDP came in higher than expected (1.3% vs 1.2% q/q). In Europe, the picture is more muted as the STOXX 600 gains 0.2%, and the only other countries moving up or down 0.2% or more are Italy (+0.5%) and Spain (+1.5%). Europe’s gains come as PMI reading for the services sector generally surprised to the upside. The only exception was Spain, which ironically is also the country with the largest gain on the day so far.

In last night’s Closer, we highlighted multiple equity baskets, which shed some light on how the economy is doing, and their performance is especially important given the lack of official economic data. Another index we follow closely as a gauge of the economy is semiconductors, which, many years ago, we branded the transports of the 21st century. When semis rally and outperform the market, it usually serves as a confirmation of a rally in the broader market and economy. Conversely, when semis falter and underperform, it serves as a red flag.

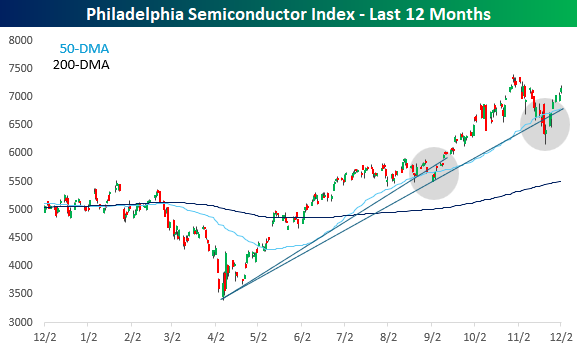

As shown in the chart below, the Philadelphia Semiconductor Index (SOX) has performed extremely well since the April low. In retrospect, it’s been a smooth ride higher, although there were two speed bumps – in September and just recently – where the trend higher and the 50-DMA was briefly violated. In the moment, both pullbacks felt concerning, but as semis recovered, the selloffs were chalked up to consolidation. The SOX isn’t out of the woods yet, but through yesterday’s close, it was less than 3% from a new high.

On a relative strength basis, semis have also bounced back nicely. In late October and early November, the relative strength of the SOX briefly made a new high, and now just seven trading days after the recent low, it’s back within a 3% range of that high.

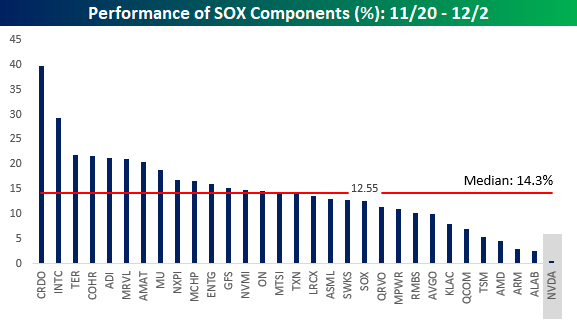

What really stands out about the rally in the SOX off the closing low on 11/20 is the breadth. Since the low, every stock in the index has traded higher, and the median gain has been 14.3%. What’s most impressive, though, is that Nvidia (NVDA) has sat out the rally with a gain of just 0.45% making it the worst-performing stock in the index. NVDA is the largest stock in both the SOX (by a wide margin) and the S&P 500, and during a period when it has essentially been flat, the two indices rallied 12.55% and 4.44%, respectively. It looks like the market can, in fact, rally without NVDA.

Dec 2, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Colonel Jessup! Did you order the Code Red?!” – Lieutenant Daniel Kaffee, A Few Good Men

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Silicon Valley is abuzz this morning following reports that OpenAI CEO Sam Altman declared a ‘code red’ on Monday as competition from Google and Anthropic intensifies. To fight the threats, initiatives like an advertising model, AI agents, and a personalized “Pulse” service for individual users have been temporarily put on hold. This latest story is just another example of how quickly the currents can change in the AI space, and that no one’s lead is safe.

Going back to the internet era, remember the ‘browser wars’? Google Chrome now dominates the browser space with about 70% market share, but you may find it hard to believe that it wasn’t released until 2008, more than eight years after the Internet bubble burst! There’s still a lot of runway left in the battle for AI supremacy.

US stocks started off December with broad-based declines as the S&P 500 fell 0.5%, but the Dow fared worse, falling nearly 1% as the Nasdaq outperformed, falling just 0.38 as Nvidia’s 2% gain propped that index up. The real area of weakness, though, was in the small-cap Russell 2000, which fell 1.25%. So much for the broadening trade.

Bulls started off the overnight session looking to put up a fight as S&P 500 futures rally 0.25% while the Nasdaq looks to open 0.38% higher. Crude oil is down fractionally as it wasn’t able to trade back above $60 in yesterday’s rally, while gold falls 1%, silver plunges 2%, and platinum falls even more (-2.38%). Crypto had a rough start to December, but has bounced back over 2% this morning, trading back above $87K.

Asian stocks saw mostly muted moves overnight. The one exception was South Korea, as the Kospi rallied nearly 2% following confirmation from US officials that tariffs on exports to the US would be cut to 15%. In Europe, the tone is also positive as the STOXX 600 bounces 0.3% with Germany rallying 0.60%.

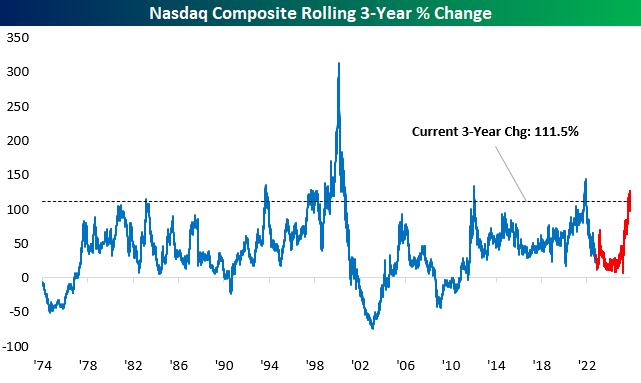

In last night’s Closer, we looked at the performance of the Nasdaq over the three years since the release of ChatGPT and compared that performance to other major tech releases of the last 50 years. Since the launch of ChatGPT in late 2022, the Nasdaq has rallied more than 100% ranking as the strongest three-year return since the period coming out of Covid and the massive tech investment to facilitate the work-from-home era. Outside of that period, the only other three-year period that was stronger was the one coming out of the Financial Crisis.

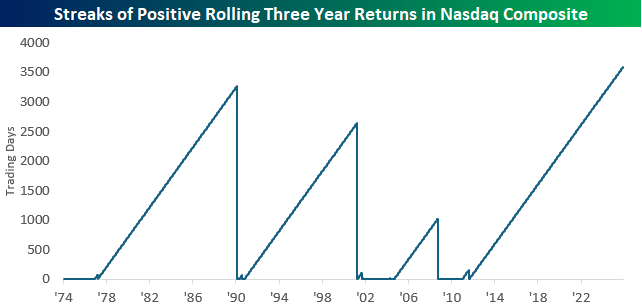

In addition to the massive rally of the last three years, what stood out in the chart was how long it has been since the Nasdaq had a negative rolling three-year return. The last time it was negative was in August 2011, just after S&P downgraded the AAA sovereign US credit rating more than 14 years ago! The chart below shows streaks of positive readings in the Nasdaq’s rolling three-year return, and at a length of 3,590 trading days, the current streak easily ranks as the longest. Besides that, three years ago the Nasdaq was under 11,500, or more than 50% below current levels. In other words, barring a large decline, the current streak of positive three-year returns isn’t going away soon.

Dec 1, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Many people are busy trying to find better ways of doing things that should not have to be done at all. There is no progress in merely finding a better way to do a useless thing.” – Henry Ford

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a zero-gravity rally on Friday that pushed the S&P 500 into positive territory for the month and extended the S&P 500’s monthly winning streak to seven, equities are rediscovering gravity to start December as futures on the major averages all trade lower. The Nasdaq is poised to open down nearly 1% while the S&P 500 faces a 0.7% decline. Even with equities falling, treasury yields are also higher as the 10-year ticks up 3 bps to 4.05%. Crude oil is up just over 1% as OPEC+ announced plans to maintain output levels rather than raise them, and gold is back near $4,300, gaining about 0.8%. The big loser on the day, though, is Bitcoin. With a decline of over 6%, the largest crypto is on pace for its worst day since March, and part of the weakness could be related to reports that Strategy (MSTR) could potentially be forced to sell some of its holdings to fund its dividend.

The weakness started in Asia as the Nikkei fell close to 2% as JGB yields continue hitting levels not seen since before the Financial Crisis, as expectations for a rate hike later this month solidify. In China, stocks went the other way with the Shanghai Composite rallying 0.7%, even as November Manufacturing and Non-Manufacturing PMIs remained in contraction territory.

In Europe, the losses have been more uniform as the STOXX 600 falls 0.5% as Manufacturing PMIs for the economic bloc and individual countries missed expectations. The biggest loser on a country basis is Germany, as the DAX declines more than 1.5% as defense contractors have been especially weak on reports of progress in the Russia-Ukraine war talks.

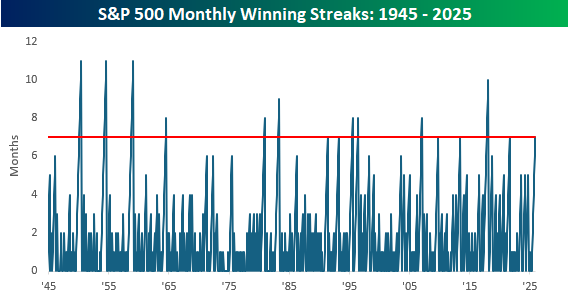

As mentioned above, the S&P 500’s winning streak extended to seven in November, and that’s the longest streak of gains for the index in more than four years (August 2021). Since the end of WWII, there have been 15 other seven-month winning streaks, with the longest being eleven. Believe it or not, that happened three times, all of which were all in the 1950s. So, while history always talks about the roaring twenties, don’t forget about the fantastic fifties.

Outside of those three eleven-month winning streaks in the 1950s, the only other streak that extended into the double-digits was the 10-month streak that kicked off President Trump’s first term in office, ending in January 2018 (seventh month was October 2017). Getting back to the most recent streak, the seven months ending in August 2021 were followed by a sharp decline of 4.8% the following month, and weak returns thereafter.

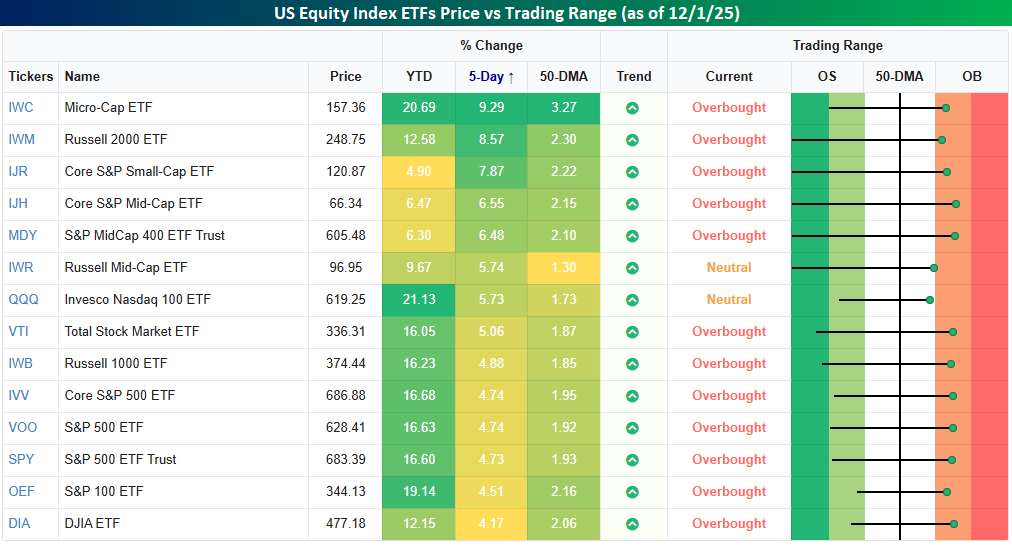

Last week, right before Thanksgiving, we pointed out that the S&P 500 and other major US equity indices had quickly gone from oversold to neutral. In the two trading days since then, the rally kicked into another gear with little selling resistance (as evidenced by Friday’s rally), and all but two of the major equity index ETFs in our Trend Analyzer snapshot have moved into overbought territory. The only exceptions are the Russell Mic-Cap ETF (IWR) and the Nasdaq 100 (QQQ), and while they may not be overbought, they still rallied over 5% in the five trading days through last Friday’s close (from close on 11/20).

Of all the ETFs shown, every one of them was up at least 4% in the trailing five trading days. While large-cap ETFs lagged with gains of less than 5%, small caps had a day in the sun with the Russell Micro Cap ETF (IWC) surging 9% while the Russell 2000 ETF rallied over 8.5%. While usually not the case in recent months, this rally has been one where big gains came in small packages.

Nov 28, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Scientific knowledge advances haltingly and is stimulated by contention and doubt.” – Claude Lévi-Strauss

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Hope everyone in the States had a great Thanksgiving! Futures are halted this morning following a technical glitch on the CME, but equity ETFs tracking the S&P 500 and Nasdaq are indicated to open up 0.34% and 0.51% respectively, on this holiday-shortened day. Small caps are also higher with the Russell 2000 poised to open up 0.33%, although that won’t even be enough to erase the declines seen in the final half hour of trading on Wednesday. Treasury yields are little changed relative to Wednesday’s close, while crude oil and gold are both up about 0.60%. Even Bitcoin isn’t doing much this morning as it hovers just above $91K, although that’s a big improvement from the $86K level it was at on Wednesday afternoon.

Today may not seem like an important day, with many people taking the day off and the market open for only 3.5 hours, but it is coming down to the wire on the S&P 500’s six-month winning streak. Heading into today, the S&P 500 is down 0.40%, which is only slightly more than SPY’s current pre-market gain. So grab your popcorn, and don’t hit the mall just yet!

In most Asian markets, trading activity to close out the week was generally positive, adding to an already positive week. The one exception was South Korea, where the KOSPI fell 1.5%, taking its YTD gain down to just below 2% on the week. In Japan, CPI came in at 2.8% y/y, which was slightly higher than expected. Despite that increase, a BoJ policymaker contended that underlying inflation remains below their 2% target.

In Europe, trading is very quiet so far this morning, with the STOXX 600 up 0.1%, but the index and the individual country benchmarks that underly it are all firmly in positive territory for the week. French CPI data for November unexpectedly declined 0.1% versus expectations for an unchanged reading.

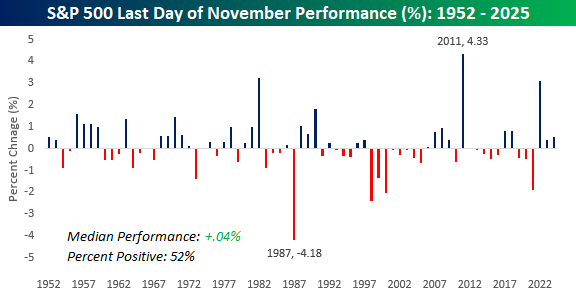

From a market perspective, there was a lot to be thankful for yesterday, especially given where it stood at various points in the year. As we head into the last day of the penultimate month of 2025, we wanted to take a quick look at how the S&P 500 has historically performed on the final trading day of November and the first trading day of December.

Earlier this week, we showed how Black Friday has historically been a positive day for stocks, with the S&P 500 averaging a one-day gain of 0.24%. However, Black Friday isn’t usually the last trading day of the month, and market performance hasn’t been particularly strong on that day. Since the five-trading-day week in its current form began in late 1952, the S&P 500’s median performance on the last trading day of the month has been a gain of 0.04% with positive returns 52% of the time.

The worst year was in 1987, when the market was still reeling from the October crash, and the S&P 500 fell 4.18% while the best day was in 2011 – another volatile year – when the S&P 500 rallied 4.33%. 2022 was the third-best performance for the last day of November when the S&P 500 saw a nice gain of 3.09% in the early weeks of the bull market. That also happened to be the exact day that ChatGPT came into our lives!

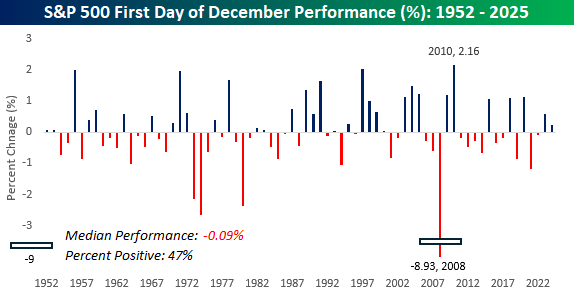

The first trading day of December has also been as bland as an overcooked turkey with no gravy. Since 1952, the S&P 500’s average performance on the first trading day of the month has been a decline of 0.09% with positive returns just 47% of the time. The best performance was a gain of 2.16% in 2010, while the worst was a year earlier in 2008, when the S&P 500 plunged 8.93%. 8.93%! Think about that for a second. We didn’t even fall that much in the latest market pullback (at least not yet), and some people were already acting like it was the end of the world, but in 2008, the S&P 500 fell that much in a single day!

If you’ve been around the block a few times, it may sound hard to believe, but there are now people with driver’s licenses and/or who are applying to college that were born after Lehman Brothers filed for bankruptcy in 2008. Time has a way of dulling memories, especially the bad ones, so for both people who weren’t around during the Financial Crisis and those who were (and just may not have been paying attention), it’s easy to forget how crazy that time was.

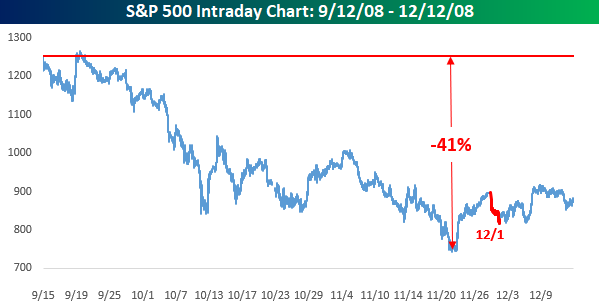

That 8.93% decline on the first trading day of December wasn’t just an outlier. In November 2008, the S&P 500 had a daily move of +/-5% on eight of the month’s 19 trading days, and in the three months after Lehman’s bankruptcy, there were 18. That’s more than once every four days!

A better way to show this, though, is to look at an intraday chart of the S&P 500 in the three months following Lehman’s bankruptcy. On the Friday before Lehman went belly up, the S&P 500 closed at 1,251.70. Besides a brief period in the following days, it didn’t reach that level again for a few years, and by Thanksgiving, just over two months later, more than 40% of the S&P 500’s market value was vaporized. Also, you almost need to squint to see it, but that red ‘scratch’ on the right of the November low represents the 8.93% one-day decline from 12/1/08. In the markets, just like life, everything is relative.