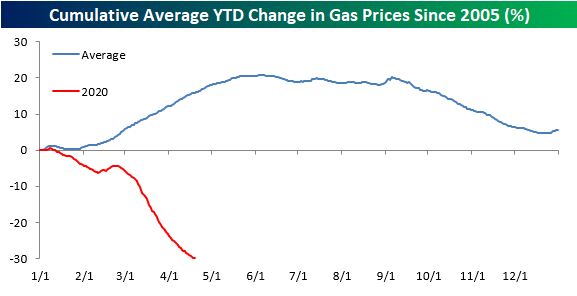

Two Months Without an Increase in Prices at the Pump

While consumers staying home have not had much of a chance to enjoy the decline in gas prices, the decline has been relentless. The last time the national average price of a gallon of gas increased was on February 22nd. That’s 59 days ago. The chart below shows historical streaks where the national average price of gasoline did not show a day/day increase. At 59 days, the current streak is the fourth-longest on record dating back to 2005. The longest streak ended at 123 days in January 2015, while the next two ended at just under 90 days.

With the current streak of days without an increase at just 59 days, it sure doesn’t seem extreme relative to those other periods. So what gives? Even though the current streak is much shorter than the three longest streaks, this one is perhaps even more extreme given the time of year when it is occurring. Looking at the chart above, each of the three longest streaks on record all ended in December and January. The blue line in the chart below shows the seasonality of gas prices throughout the year, and the weakest time of year is typically from the beginning of December through year-end. Therefore, it shouldn’t be too much of a surprise that the three longest streaks on record took place during that time of year. The current streak, however, has occurred during a time of year where prices at the pump are normally at their strongest. In fact, this is the first time since 2005 that gas prices have ever been down on a YTD basis at this time of year. In other words, this current streak of declines is rather extraordinary. Start a two-week free trial to Bespoke Premium to access our full range of research and interactive tools.

Chart of the Day: Stocks vs. COVID Symptom Search Trends

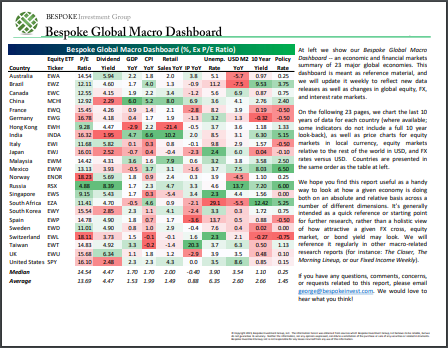

Bespoke’s Global Macro Dashboard — 4/22/20

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Bespoke’s Morning Lineup – 4/22/20 – Third Time the Charm?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

After two down days to start off the week, equity futures are indicated to recoup some of those losses at the open. Hopefully, the market can hold onto these early gains, but only time will tell. One positive for the bulls is that semis are trading up over 2% as a group following positive reports from Texas Instruments (TXN) and Teradyne (TER).

Read today’s Bespoke Morning Lineup for a discussion of the latest moves in the crude oil market, major earnings releases, the latest trends in the COVD-19 outbreak, and other stock-specific news of note.

After the May contract for WTI crude oil moved back above zero yesterday and the now front-month June contract is ‘only’ down 3% today, one might be tempted to think that a sense of normalcy is moving back into the crude oil market. Don’t be fooled.

First, let’s look at the historical one-day change for WTI going back to 1983. After Monday’s 306% record (in more ways than one) decline, yesterday’s rally of 126.6% rally out of negative territory was the strongest one-day gain in WTI’s history.

It’s not only the one-day daily changes that suggest the crude oil market is nowhere anywhere close to normal. In looking at the spread between the prices of the current (front month) contract and the price six months from now, the current spread is at levels rarely seen. Through yesterday’s close, the spread between the two contracts was -$14.89 per barrel indicating that crude for delivery six months from now is nearly $15 more expensive than crude oil for delivery in the current month. While that’s well off the record $68 spread seen at the close on Monday, going back to 2006, the only time the spread was at similar levels was during the depths of the financial crisis. One thing we know about the 2008/09 period is that there was nothing normal about then.

Daily Sector Snapshot — 4/21/20

Bespoke Stock Scores — 4/21/20

S&P 500 Dividend Yield vs. 10-Year Yield Blowout

With the dramatic plunge in equities in late February and March, the S&P 500’s dividend yield rose all the way up to a high 2.81% on the March 23rd low. The subsequent rally off of that March 23rd low has seen the dividend yield pull back to 2.15%. While dividend cuts on account of slowed business could result in that yield falling further as earnings season progresses, at the moment, the S&P 500’s yield remains far more attractive than that of US Treasuries which are historically low after the flight to safety recently. As of today, the 10-Year Treasury only yields 55 bps which is just off of the March 9th low of 54.07 bps.

On March 23rd the difference between the S&P 500’s dividend yield and that of the 10-Year Treasury was around 1.915 percentage points; the most in the past half century. Today the spread has narrowed a bit to 1.59 percentage points, but as shown below, that still remains wider than anything we’ve seen over the last 50 years. Start a two-week free trial to Bespoke Premium to access our full range of research and interactive tools.

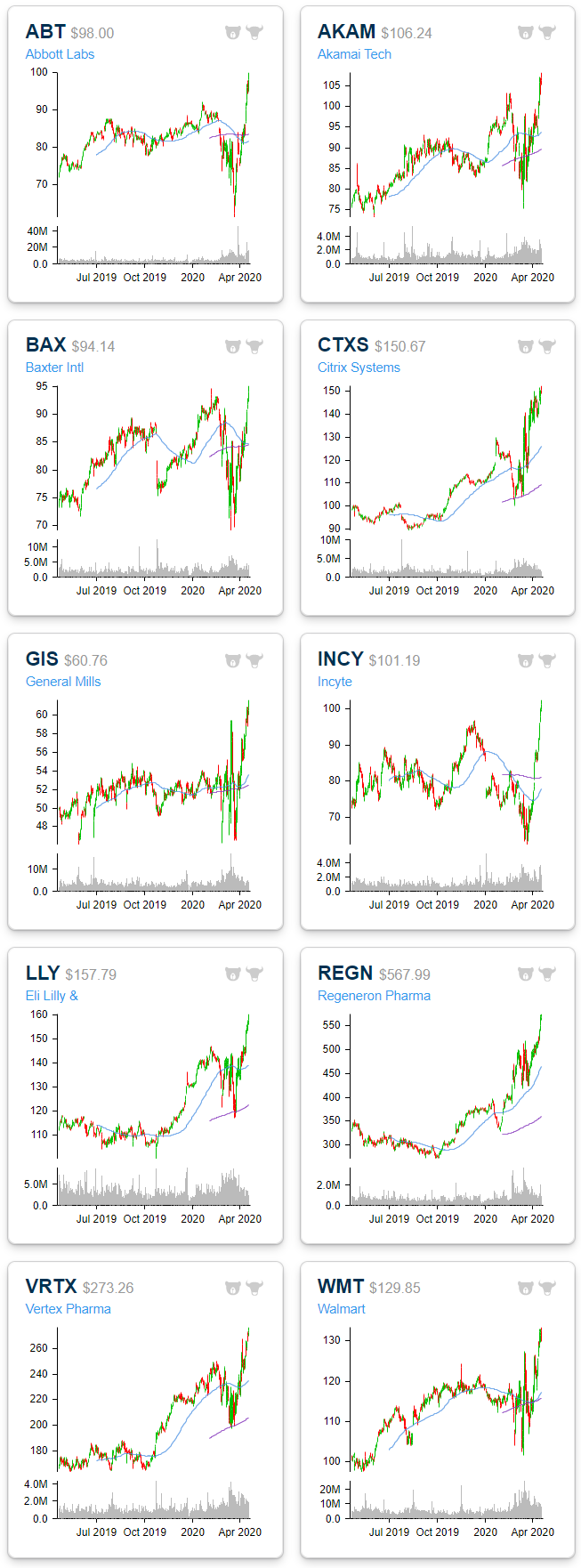

Health Care Leading in New Highs

Breadth was pretty lackluster yesterday with only about 15% of the S&P 500 finishing the day higher. Despite this, of the stocks that did rise, there were a handful that reached new 52-week highs. As shown below in charts from our Daily Sector Snapshot, with yesterday being no exception, recently the stocks reaching 52-week highs have been predominately concentrated in the Health Care sector which saw a net of 10% of its stocks at new highs yesterday. Meanwhile, Technology and Consumer Staples were the only other sectors that saw an uptick in net 52-week highs yesterday. While there were no other highs across each of the other sectors, there was not an increase in 52-week lows either. In other words, for the most part, S&P 500 stocks are now trading somewhere within the past year’s range rather than breaking out or down.

The charts below are from the 52-week highs screen at our Chart Scanner tool. These are the 10 S&P 500 stocks that broke out to new 52-week highs yesterday. Most of these have been in uptrends for the past year while the recent spike in volatility has ended patterns of sideways trends for others like Abbot Labs (ABT) and General Mills (GS). As previously mentioned, the bulk of these stocks are Health Care names including Abbott Labs (ABT), Baxter (BAX), Incyte (INCY), Eli Lilly (LLY), Regeneron (REGN) and Vertex (VRTX). Additionally, Consumer Staples stocks benefiting from the COVID economy like major grocery chain Walmart (WMT) and food manufacturer General Mills (GIS) also make the list. Start a two-week free trial to Bespoke Institutional to access our Chart Scanner, custom screens, and much more.

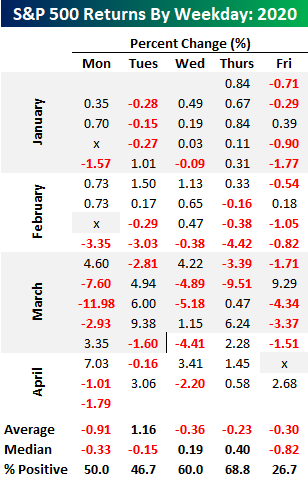

Not Your Typical Tuesday. Or Is It?

While every other day of the week has seen multiple gaps down of more than 1.5% since the peak in February, today is the first time in that span that there will be a gap down of more than 1.5% on a Tuesday. Given the lack of big gaps down, Tuesdays have also seen the strongest average return of any weekday so far in 2020. While every other day of the week has averaged declines, Tuesday has seen an average gain of 1.16%. That’s quite a disparity!

While average returns for Tuesday relative to other weekdays have been stellar, it doesn’t tell the whole story. The table below shows the S&P 500’s daily returns so far in 2020. Looking at the individual occurrences, Tuesdays have actually been up days less than half of the time. If it wasn’t for three strong Tuesdays in the month of March, returns for the second trading day of the week wouldn’t be nearly as positive.

Looking at median returns instead of averages shows how Tuesdays haven’t been nearly as strong as they seem. Looked at this way, Tuesday’s median decline of 0.15% ranks right in the middle of the pack behind gains for Thursday and Wednesday but well ahead of the 0.33% decline for Mondays and the 0.82% decline on “Corona Fridays”. Outside of a couple of outliers, Fridays have not been a good day for equities this year. Start a two-week free trial to Bespoke Institutional to access our full range of research and interactive tools.