Bespoke’s Morning Lineup – 6/11/20 – A Dose of Reality

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Markets have seemingly been moving in one direction for the last several weeks, but today are getting a dose of reality on concerns over the pace of the economic rebound and whether it will be derailed by a new surge in cases around the country. No one said the recovery would be a smooth one.

If the current pace of declines holds, today will be the first 1% decline at the open for SPY since May 1st, and the 7th since the March 23rd low. If those prior periods are any indication, don’t look for much in the way of a rebound. In the six prior occurrences, the S&P 500 continued lower from the open to close four out of six times.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, moves in overseas markets, global and national trends related to the COVID-19 outbreak, and much more. In today’s report, we have also started to include data on state by state trends in hospitalizations.

In yesterday’s Chart of the Day, we highlighted the strong performance of large-cap tech as measured by the FANG+ Index over the four weeks. This morning we wanted to highlight the recent strength in another way by noting that yesterday’s rally was the fourth straight day where the FANG+ Index rallied 1% or more. As indicated by the red dots in the chart below, that’s only happened four other times in the index’s history dating back to 2014.

Chart of the Day: FAANG+ In Uncharted Waters

Daily Sector Snapshot — 6/10/20

Are Retail Investors Driving Price Action?

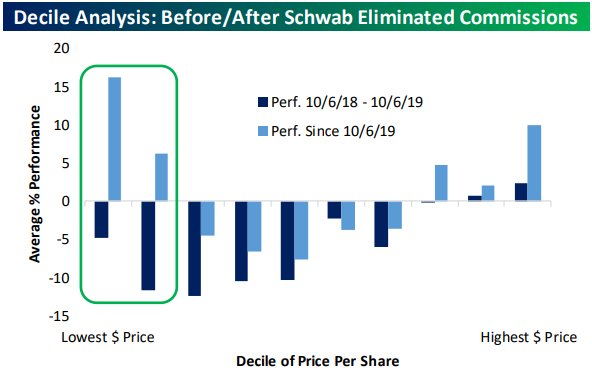

We’ve seen a lot of media coverage focused on the idea that small investors are piling into the market and driving lots of the aggressive price action in recent months. This phenomenon was around before the March plunge in the market, but with bankrupt rental car companies (HTZ), flailing airlines (AAL), and Chapter 11 energy names (CHK) showing up in lists of stocks most widely-held by retail investors along with hyper-speculative plays on hot new products like electric truck manufacturer NKLA, it’s easy to see why people might get the idea that small retail investors flush with commission-free trading confidence might be having an outsized impact.

To test this theory, we started with the theory that relatively small traders are more likely to buy lower dollar price stocks. It’s easier to dip your toe into a $1 stock than a $150 stock, even if the division of the company’s value is arbitrary. For small-dollar accounts, that truism is the most important. Starting on October 7th of last year, Charles Schwab (SCHW) started offering commission-free trading to brokerage clients, competing with popular zero-commission product Robinhood. Fidelity and other brokers followed shortly after. In the year before October 7th, stocks with low dollar prices were notable underperformers relative to the rest of the market. The chart below uses the Russell 3000 as its sample and breaks the index into deciles (10 groups of 300 stocks each) based on share price. Since Schwab went to $0 commissions, the lowest priced stocks have been huge outperformers, and in fact the decile of stocks with the lowest per share prices are up 15%, substantially more than the rest of the market. To us, this looks like plausible evidence that smaller traders are playing at least some role in the performance of the market. We discussed this chart and other retail enthusiasm indicators in last night’s Closer report, which is available to Bespoke Institutional members. Click here to start a two-week free trial.

We’d note that the decile of the highest priced stocks has also outperformed over the same time period. Since $0 commissions began, we’ve also seen the introduction of fractional share trading on many online brokerage platforms, which allows investors to buy stocks by dollar amount instead of share amount. This now lets a small-dollar investor easily invest in high-priced stocks above $1,000/share like AMZN and GOOGL. Instead of having to buy a share of AMZN at $1,400, an investor can now simply buy $100 worth of AMZN and own a fraction of a share.

Inflation Data Catching Up to ISM Commodities Survey

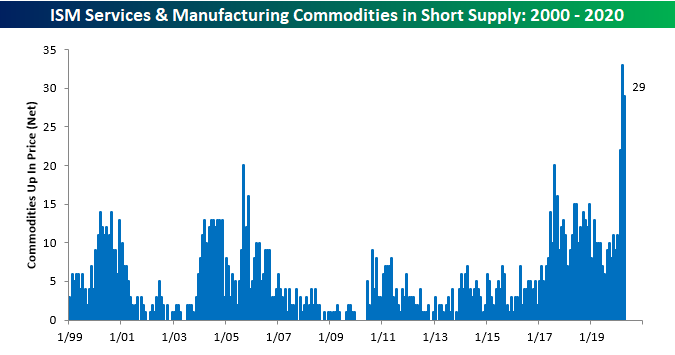

In each month’s ISM reports, respondents are asked which commodities they have seen price increases and decreases in, as well as which ones are in short supply. Over the years, we have highlighted trends in this survey as they have often been a good leading indicator of overall trends in inflation. The chart below compares the y/y change in CPI versus the six-month average of the net combined number of commodities up in price in the ISM Manufacturing and Services reports. All the way back in late 2018, the average net number of commodities rising in price peaked and started to decline from readings in the 30s. While this reading was on the decline, overall inflation, as measured by y/y CPI, wouldn’t budge below 1.5%. While it took a global pandemic, the lower prices implied by weaker commodity prices finally flowed through to inflation readings in the last few months as y/y CPI is barely above zero and at levels not seen in nearly five years.

While overall price levels may be rising a lot more slowly, the number of commodities in short supply is coming off levels not seen in at least 20 years. The chart below shows the number of commodities reported as being in short supply in the monthly ISM Manufacturing and Non-Manufacturing reports. In this month’s reports for the month of May (reported last week), the total number of commodities in short supply was at 29, which was down from April’s record reading of 33.

Given the basic laws of supply and demand one would think that with a record number of commodities in short supply, inflation pressures would be rising rather than falling. So, what gives? The table below lists the commodities that are currently noted as being in short supply along with which report(s) they were noted in. As you can see, just about all of these commodities are related to the COVID outbreak, and while their prices have surged in the last few months, as a percentage of the overall inflation picture, they still take up a small share of the overall pie. In other words, shortages are rampant in one sector of the economy, but it’s a very small slice. Click here to view Bespoke’s premium membership options for instant access to our research and analysis.

Big Tech Breakout

As we noted yesterday, the Consumer Discretionary sector (XLY) was the first and only sector above its 2/19 levels (date of the last all-time high for the S&P 500). But with further gains yesterday, Technology (XLK) is looking to join XLY in moving above its 2/19 levels. On a closing basis, XLK finished yesterday $0.15 above its last all-time high. While the ETF has broken out slightly, the same cannot be said just yet for the S&P 500 Technology index that the ETF tracks which finished yesterday still 0.2% below its highs; the closest to its 2/19 high of any sector excluding Consumer Discretionary. Communication Services, Materials, and Health Care are likewise within tangible reach of their prior highs.

Within the Tech sector, there are several stocks that have begun to break out as well. As shown in the charts below from our Chart Scanner, there are some like Apple (AAPL), Adobe (ADBE), Microsoft (MSFT), OneSpan (OSPN), and Texas Instruments (TXN) that have broken out to or are very close to new 52-week highs after taking out their highs from earlier this year within the past several days. Though they are not at 52-week highs, there are others like Advanced Micro Devices (AMD) and Hewlett Packard (HPE) which are experiencing other types of breakouts. For AMD, the stock was quick to recover most of its 2/19 to 3/23 losses retesting those prior highs as early as mid-April, though, it had done so unsuccessfully. Ever since AMD has been in a short term downtrend as Tech shifted from a market leader to somewhat of a laggard in the past month. But surging 6.5% yesterday and another 2.87% today, the stock has broken that downtrend. HPE on the other hand had peaked last fall with losses accelerating during the bear market. Since March, the stock has not shared the massive recovery of other stocks as it has consolidated between roughly $9 and $10.5. In just the past week, though, HPE has managed to break out above this range.

As previously mentioned, AAPL has experienced a significant breakout in the past week and the same can be said for other mega-cap stocks as well. Of the FAANG stocks, Amazon (AMZN) also broke out (again) yesterday to its own 52-week high. Facebook (FB) has nearly done the same after successfully retesting former resistance around $223 in the past couple of weeks. At the same time, Netflix (NFLX) has held up at its 50-DMA while Alphabet (GOOGL) has moved back into its range from earlier this year leading up to its 2/19 high. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 6/10/20 – Mortgages Still Ripping

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

After a relatively large dip lower right around the time Europe opened for trading, today was looking like it was going to be some sort of repeat of Tuesday’s action when pre-market gains in the futures were erased after Europe opened. At their 6:00 AM eastern lows, futures were down over 1% from their overnight highs, but since then they have rallied back more than 0.70% and firmly back in positive territory. The initial cause of the dip was a report from the OECD that estimated global growth would decline 6.0% this year and even more if a strong second wave of the virus emerges in the Fall and Winter. Tell us something we don’t know.

CPI for May was just released and while economists were expecting both the headline and core readings to come in unchanged versus April, they both showed a 0.1% m/m decline.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, the rally in iron ore and copper, credit creation data in China, global and national trends related to the COVID-19 outbreak, and much more.

We’ve been highlighting the trend for a couple of weeks now, most recently in last Friday’s Bespoke Report, but mortgage purchase applications continue to rip higher. The latest figures released this morning confirmed that trend as overall applications increased 9.3% while purchase applications increased 5.3%.

With this past week’s increase, purchase applications have now increased for a record eight straight weeks. Even more impressive is the fact, that the index for purchase applications is just a whisker below the 10+ year high of 313.7 from back in January. Historically low rates are fueling what looks like an extremely strong housing market.

Daily Sector Snapshot — 6/9/20

Valuations Stretching

With equities recovering a massive share of the declines from earlier in the year, valuations have gotten a bit elevated. As shown in the chart below, the trailing price to earnings ratio of the S&P 500 is now in the 99th percentile of the past decade. At the moment, the S&P 500’s P/E ratio of 22.5 is the highest since January and February of 2018. Prior to that, the last time that the S&P 500 had a P/E around this elevated level was in late 2009 and it was even more elevated in the late 1990s/early 2000s. As for the individual sectors, Technology is also in the 99th percentile of the past decade’s range with the only higher readings being in February of this year right around the time of the last all time high for the S&P 500. Consumer Discretionary is trading at even more of a premium. Its 33.4 P/E is at its highest level since September of 2009 after rocketing higher over the past few weeks. As for the other sectors, Communication Services is the only other sector in the 90th percentile or better of the past decade while Health Care, Real Estate, Industrials, and Materials are all in the 75th percentile or higher. Financials and Utilities have more modest valuations on a P/E basis in the 39th and 57th percentiles, respectively.

For the sectors like Consumer Discretionary, Communication Services, and Technology as well as the S&P 500 itself, these premiums are similar to earlier this year at the last all time high on 2/19 (second chart below). Back then, all of these sectors were trading in the 99th or 100th percentile of their 10 year range. Utilities was another sector with an elevated valuation, but fast-forwarding to today, its valuation is much more modest. Other sectors like Real Estate and Consumer Staples are similarly at less of a premium than back on 2/19.

Additionally, valuations are appearing a bit stretched relative to their 10 year range on a price-to-book basis. In the past ten years, the S&P 500 has only had a higher PB ratio (currently 3.66) earlier this year in January and February. Prior to that you would need to go back to the late 1990s around the dot com bubble to find a higher PB ratio for the index. Meanwhile, the PB ratios of Consumer Discretionary, Health Care, and Technology are at their highest levels of the past 10 years. Energy on the other hand is still at the low end of the past decade’s range similar to Materials and to a lesser extent Financials. Click here to view Bespoke’s premium membership options for our best research available.

Back in November of last year through February of this year, the S&P also had its price to book, similar to its price to earnings, at the high end of the past ten years’s range. Yesterday marked the first time that the PB ratio was in the 99th percentile of the past ten years without another occurrence in the prior 60 days since November of last year. For the PE ratio it was the first time since February. As shown in the tables below, for the PB ratio that is also only the sixth time that has happened since 2000. Following such occurrences, the S&P 500 has leaned towards weaker than normal performance, especially in the short term (week and month). Although a very small sample size, the same can also be said for the price to earnings ratio. Click here to view Bespoke’s premium membership options for our best research available.