B.I.G. Tips – Stocks Trump Bonds

Bespoke Stock Scores — 2/9/21

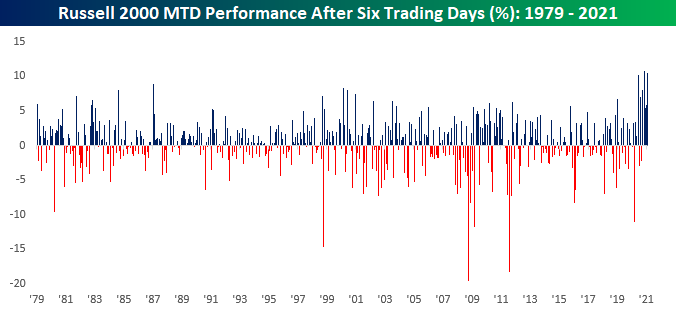

Rabid For Small Caps

We’ve seen some pretty extreme trends over the years, but the recent run of small caps ranks right up there with the best of them. As noted in our Closer report from Monday, the Russell 2000 was further above its 200-day moving average (DMA) than it has ever been before. After Monday’s close, the Russell 2000 was also already up 10% for the month. While a 10% MTD gain in just six trading days may sound impressive, this month’s performance to start the month was only the best since November – three months ago! Not only that but in the two months (December and January) between those two 10%+ gains, the Russell 2000 was up over 5% in the first six trading days of the month, and in October it was up over 8%. In other words, in each of the last five months, the Russell 2000 has been up at least 5% MTD after just six trading days. It gets even crazier too. Back in June and August, the Russell 2000 was up 10.25% and 7.04%, respectively, after just six trading days.

In the entire history of the Russell 2000 dating back to 1979, the Russell 2000 has been up at least 5% MTD after six trading days 35 times (7% of all months) and there have never been more than two months in a row of back to back 5%+ starts to the month. In the last nine months, however, there have been seven 5%+ starts to a month including a streak of five straight. Included in those seven months, three have also been gains in excess of 10%, and prior to June 2020, that had never happened before. In the wake of last year’s COVID crash, the rotation into small caps has been unprecedented. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day – Little Vs

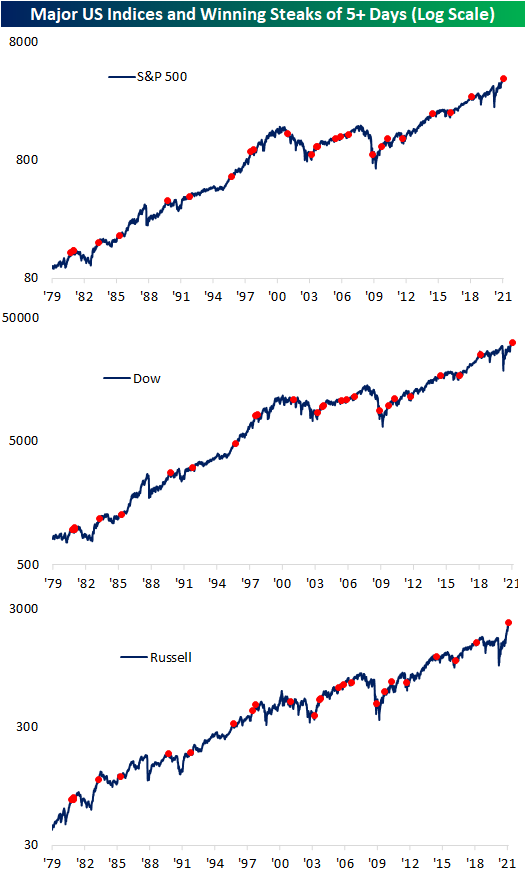

Winning Streaks Coming to an End

With lower closes for both the DJIA and S&P 500 (Russell 2000 was up), both indices ended six-day winning streaks. The last time that the S&P 500, Dow, and Russell 2000 all simultaneously ended winning streaks of 5 trading days or more was nearly three years ago in February of 2018. Just like now, each of the indices were going on six days of consecutive gains. June 2014 and April 2010 also saw identical six-day winning streaks for these three indices.

In the table below, we show the past 24 times since the start of 1979 when the Russell 2000 first began that the S&P 500, Dow, and Russell 2000 saw simultaneous winning streaks of at least five days come to an end. From the close of the first down day that snapped these past streaks, performance has generally leaned positive over the following year. The next week has averaged gains for each of these indices, though we would note, median returns are weaker as big gains following the 2008 occurrence have a heavy impact on the average. In fact, median performance one week after the end of these streaks is actually weaker than the norm for the one-week performance of all periods for each index. For the Dow, in particular, there is a median decline over the next week with positive returns only half the time. One month later has also only seen the index higher half the time while the S&P 500 and Russell are more frequently higher. The performance further out is generally more positive although there is some underperformance relative to the norm. Although the indices are consistently higher three, six, and twelve months later, only the six month period has tended to outperform the norm across each index. Specifically for the Russell 2000, performance is notably strong with positive returns 91.67% of the time. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 2/9/21 – Blink and You May Miss it

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The desire to perform all the time is usually a barrier to performing over time.” – Robert Olstein

After six straight days of gains, US equity futures are poised to open lower this morning. If the S&P 500 finishes the day lower, it will be the first down day since 1/29 when the S&P 500 closed below its 50-day moving average. The data calendar is on the light side this morning. NFIB Small Business sentiment was released earlier this morning and came in lower than expected (95.0 vs 97.0) falling to its lowest level since May. Later on, we’ll get the release of the JOLTS report for December.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports from around the world, recent moves in the dollar, a preliminary analysis of Japanese Machine Tool Orders, an update on the latest national and international COVID trends, and much more.

One of the hallmarks of a bull market is that corrections are swift and shallow, and windows of opportunity for investors on the sidelines is usually narrow. The pullback we saw in late January provides an excellent example. On January 20th, the S&P 500 closed at ‘extreme’ overbought levels which we classify as more than two standard deviations above its 50-day moving average (DMA). Seven trading days later on 1/29, the S&P 500 was down 3.7% from its high and below its 50-DMA for the first time since early November. Faster than the S&P 500 sold off from ‘extreme’ overbought levels to below its 50-DMA, though, it rebounded back to ‘extreme’ overbought levels again. Yes, just six trading days after closing below its 50-DMA for the first time since November, yesterday the S&P 500 finished the session back above its 50-DMA by more than two standard deviations.

Daily Sector Snapshot — 2/8/21

50 Days Below the 50-Day

While the yield on the 30-year Treasury bond briefly rose above 2% overnight for the first time in a year, in general, long-dated government yields are lower today. As such, the iShares 20+ Year Treasury Bond ETF (TLT) is bouncing from extreme oversold territory today rising over 0.6%. Even after today’s rally, though, TLT continues to trade well below its 50-DMA as it has for 51 consecutive trading days.

The current streak of consecutive closes below the 50-DMA for TLT has now joined a list of 13 prior streaks of at least 50 trading days long. The two longest of these went on for 93 consecutive trading days ending in February of 2011 and September of 2013. While the current streak has plenty of time to go to even tie those records, the last streak was very recent ending on November 19th of last year at 63 trading days long. In fact, between the end of that streak and the start of the current streak, there were only two days. In other words, since August 24th, there have only been two days in which TLT did not close below its 50-DMA. Not only that but with TLT currently trading more than 4% below its 50-DMA, the streak isn’t likely to end any time soon.

In the table below, we show each of the past TLT streaks when they first reached 50 trading days long. For each streak, we also show how TLT and SPY performed going forward. On average TLT has continued to drift lower over the following month, but three months to one year out, performance is generally much more positive. Returns have been positive better than two-thirds of the time three and six months out with average gains of 1.81% and 5.75%, respectively. One year later, TLT has traded higher all but once (in November of 2005 when it only fell 8 bps). As for equities, the S&P 500 (SPY) is similarly weak one week after these streaks averaging a decline of 0.46% with positive performance less than a quarter of the time. Again, returns further out are generally more positive with SPY higher 83% of the time 6 months later and 75% one year later. Click here to view Bespoke’s premium membership options for our best research available.

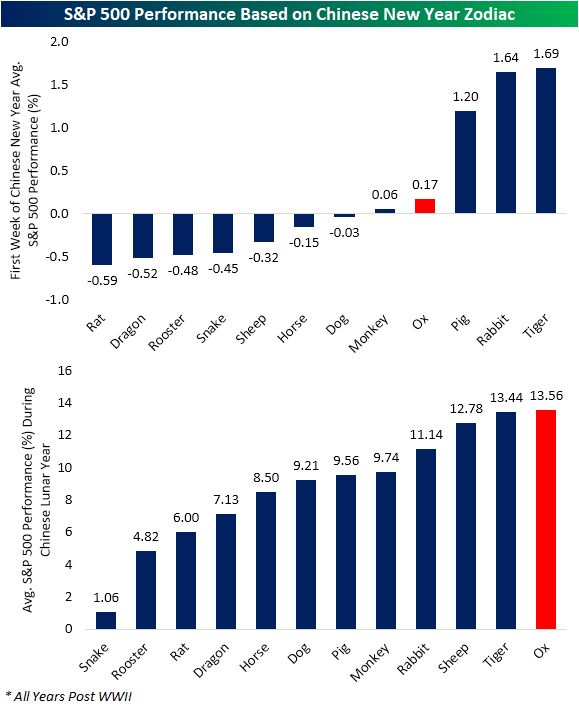

Bullish Returns During the Year Of the Ox

Friday starts off the Chinese Lunar New Year. Celebrations will last for about two weeks though the official legal holiday is seven days long. As such, Chinese markets will be closed from Thursday (New Year’s Eve) through next Wednesday. The Chinese lunar calendar is also associated with a cycle of 12 animal zodiac signs, and 2021 will be the year of the ox. While we would be the first to caution against investing based on zodiac signs, ironically, the year of the ox has historically been met with some of the most bullish market performance in the US. As shown below, in the first week of Chinese New Years that have been marked by the Ox, the S&P 500 has seen an average gain of 0.17%. Only the years of the pig, rabbit, and tiger have seen a stronger performance in the first week of the Chinese lunar year for the S&P 500.

But as for annual performance, from the start of the Chinese lunar year until the end, years of the ox has been marked by the best performance for the S&P 500 with a 13.56% average gain. The past few years that were the year of the ox were 2009, 1997, and 1985. The year of the tiger, which the last one was in 2010, comes in with the second-best performance.

As for the performance of the S&P 500 in the shorter term—particularly around the time when the Chinese markets are closed—in the chart below we show the average intraday performance for the first five trading days of the Chinese New Year for all years since 1990. Despite market closures abroad, the US tends to move steadily higher- and that’s no bull! Click here to view Bespoke’s premium membership options for our best research available.