Chart of the Day: Masco (MAS) May Move

Good and Bad From Jobless Claims

Last week’s initial jobless claims print was higher by 33K to 812K which means it was unchanged from the prior week’s reading. While this week’s number didn’t meet expectations of a decline to 760K, it is not all bad news considering claims did drop to 793K which is the lowest level since the first week of the year.

On a non-seasonally adjusted basis, consistent with seasonal patterns, claims continue to fall with a 36.6K drop this week down to 813.1K. That is the lowest level in the unadjusted number since the week of November 27th when claims stood nearly 100K lower.

As for other programs, initial jobless claims through the Pandemic Unemployment Assistance (PUA) program also declined by a little over 34K this week just as they did last week. At 334.5K, PUA claims are at the lowest level since the week of January 8th. Combined with regular state claims, total initial claims stood at 1.148 million, down by 71K week over week and marking a fourth consecutive weekly decline. While total initial claims remain off the lows of just above 1 million from November, this week’s print marked a five-week low.

Regular state continuing claims—lagged one week to initial jobless claims—persistently keep moving lower with the most recent week falling to a new pandemic low of 4.545 million from 4.69 million last week. That week over week decline was a fourth straight also meaning 18 of the past 20 weeks have been met with a decline in continuing claims.

The addition of other programs adds another week’s lag to the data. That means the most recent data on continuing claims across all programs covers the week of January 22nd. In spite of the consistent declines in regular state continuing claims, the overall picture including these other programs muddies the water. There have been significant upticks in other programs that led total claims to significantly rise from 17.87 million to 20.47 million; the highest level since late November. Again, that uptick was not on account of regular state claims. In fact, it was one of the only programs to see a decline week over week falling by 29.6K. On the other hand, PUA claims rose by 1.497 million which comes after a 1.636 million increase two weeks prior. That was not the only program to see a week over week increase of over 1 million though. Pandemic Emergency Unemployment Compensation (PEUC)—which is an extension program for those whose benefits have or are set to expire—saw claims rise by 1.173 million. That is the single largest uptick since the program began earlier in the pandemic.

Those surges between the two programs meant that they also account for much larger shares of total claims than before. While the regular state claims only account for around a quarter of total claims- the lowest share since the pandemic related programs began in March- PUA claims take up 42.6% of all claims and PEUC claims account for 23.3%. That is the most since mid-December for both of these programs. While those significant increases are a concern and should continue to be watched for a better read on how material of an increase they are, it is possible that the upswings are due to continued catching up in reporting after these programs narrowly avoided expiration at the end of last year. For example, looking at individual states, PEUC claims out of California alone nearly tripled rising by over 1 million between the weeks of January 16th and January 23rd. Ohio also saw these claims more than double. As for PUA claims, after reporting zero claims the previous week, Colorado and Ohio reported claims of 30,659 and 10,156, respectively. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 2/11/21 – All Quiet…Except Bitcoin

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Be willing to make decisions. That’s the most important quality in a good leader. Don’t fall victim to what I call the Ready- Aim-Aim-Aim Syndrome. You must be willing to fire.” – T. Boone Pickens

With China celebrating the lunar new year, Asian markets had a quiet overnight session with little in the way of market action or economic data. The quiet trend continued into European and US markets as well with major averages and futures markets little changed on the sessions.

The only area of real action right now is in the crypto space. Bitcoin just briefly rallied to record highs on news that Mastercard (MA) would support crypto-currencies in its network, and then just about a half-hour ago Bank of New York Mellon announced that it was establishing a digital asset unit to support and service the digital asset needs of clients. Bitcoin’s price is off its highs from earlier, but it is still up over 6% on the day.

In economic data, jobless claims were just released, and while they both came in higher than expected, they did manage to decline from last week’s upwardly revised readings.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports from around the world, an update on the latest national and international COVID trends, and much more.

In yesterday’s Chart of the Day, we discussed the massive rally in crude oil over the last several weeks and how it stacked up to prior periods in the past. Another short-term aspect of the recent rally has been the fact that yesterday marked the fifth straight day that WTI closed more than two standard deviations above its 50-DMA. That’s the first time we’ve seen a streak like that in over three years. Looking at past streaks going back to 2010, these readings didn’t necessarily mark the top of a short-term rally, but they usually occurred closer to the end of a move than the beginning.

Daily Sector Snapshot — 2/10/21

Chart of the Day – Crude Oil Gushes

Short Interest Update

Yesterday, bi-weekly short interest data was released for the period ending January 30th. In the chart below, we show the Russell 3000 broken up into deciles based on short interest as a percent of the float at the end of 2020 and these decile’s stock’s median change in short interest from then to yesterday’s release. As shown, with the short squeeze episode playing out in the second half of January, the stocks that came into 2020 the most heavily shorted have seen the biggest declines in short interest. That decile of what had been the most heavily shorted names has seen short interest as a percent of float fall for a median of 2.65 percentage points. Deciles two and three have similarly seen sizable declines, though, they are far smaller than those of the most shorted stocks. On the other hand, the decile of the least shorted stocks is the only one that has seen the median short interest reading move higher since the end of 2020.

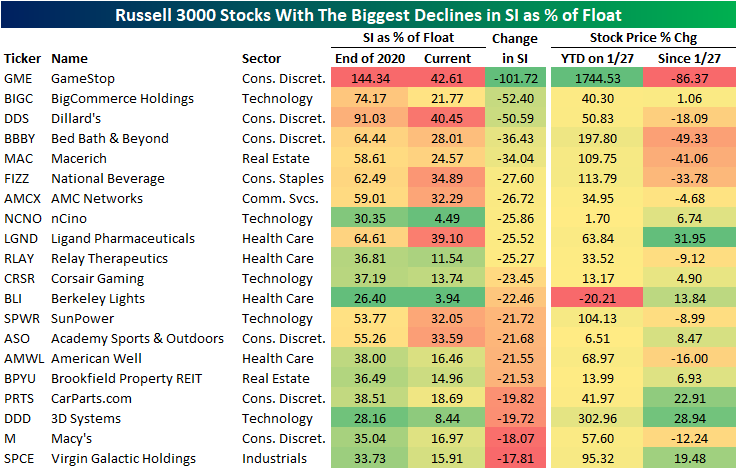

In the table below, we show the stocks that currently have the highest short interest as a percent of float. After the historic move higher, short squeeze poster child GameStop (GME) is no longer the Russell 3000’s most heavily shorted name! Having dropped over 100 percentage points since the start of the year, only 42.61% of shares are now short compared to 43.57% for Gogo (GOGO); currently the most shorted stock in the index. GOGO has actually seen its shorts come off a bit this year as well but that decline has been far more modest of only a little more than one percentage point. Of the other stocks in the index, only Tanger Outlets (SKT) and Dillard’s (DDS) also currently have more than 40% of the float sold short.

On the January 27th closing high, GME was up 1,744.53% year to date. But with the short squeeze unwinding, the stock has fallen over 86%. Others of this cohort have similarly seen big reversals of their earlier surges. For example, National Beverage (FIZZ) had doubled YTD at the time of the GME peak, but since then it has been cut by 33.78%. Not all of these have been losers since the pinnacle of short selling though. Fulgent Genetics, which now has over 30% of shares short, has risen 91.01%. Clovis Oncology (CLVS) and Ligand Pharmaceuticals (LGND) have similarly seen big gains of over 30%.

Given GME came into the year with an absurd number of shares sold short, the squeeze has resulted in it being the biggest decliner in terms of short interest of any Russell 3000 stock. Short interest as a percentage of float has fallen over 100 percentage points YTD. The next biggest drop came from BigCommerce Holdings (BIGC) and Dillard’s (DDS) which both saw larger than 50 percentage point drops. Of the rest of the top twenty biggest decliners, a baker’s dozen have seen short interest drop by at least 20 points. Additionally, of these stocks that have seen short interest fall the most, only three—nCino (NCNO), Berkeley Lights (BLI), and 3D Systems (DDD)—now have a single-digit short interest as a percent of float.

Given the massive short squeezes, there are far more stocks that now have a lower short interest as a percent of float than at the start of the year. In fact, of the Russell 3000 stocks, 1887 have seen declines in short interest compared to only 1146 that have seen an increase. In the table below, we show the twenty stocks to have seen the biggest increases in SIPF since the start of the year. As shown, there is only one, International Game Technology (IGT), that has seen short interest rise by double digits since the end of 2020.

Retailers notably dominate the list of stocks with the biggest declines in short interest. To quantify this, in the chart below we show the aggregate number of shorted shares as a percent of total float for each industry group as of the most recent short interest data and the end of 2020. As shown, just as it was at the start of the year, retailers remain the most heavily shorted industry group, but it has greatly improved with only 5.86% short compared to 8.15% at the end of 2020. That is the only industry group to have seen short interest drop by a full percentage point or more. The industry group to have experienced the next largest decline was Transportation with aggregate short interest falling from 5.08% to 4.13%. Conversely, there are two industries, Banks and Materials, that have higher short interest as a percent of float than they did at the end of 2020. Click here to view Bespoke’s premium membership options for our best research available.

Not All Fixed Income is Broken

So far this year, returns in the US treasury market have gotten off to a bad start. Based on the performance of the BofA indices, long-term US treasuries are already down over 5% YTD which would be only the second time in the last ten years that the asset class started off the year so poorly. While treasuries have been weak, not all areas of the fixed income market have performed poorly. In fact, high yield debt, which tends to be more closely correlated to the equity market, is having a much better year, gaining a bit over 1%.

The chart below shows the YTD performance spread between high yield and long-term US Treasuries 28 trading days into each year since 1995. With a current spread of over five percentage points, high yield is outperforming long-term Treasures by the widest margin since 2012 and the fifth widest margin since 1995. The only other years besides 2012 where the spread was wider were 2011, 2009, and 2001.

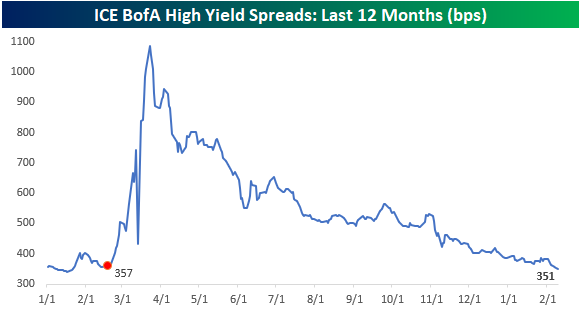

High yield has also achieved a pretty notable milestone this week as spreads relative to US Treasuries have narrowed to their lowest levels since the February 2020 pre-COVID peak in the S&P 500. On 2/19/20, when the S&P 500 peaked before the COVID crash, high yield spreads were at 357 basis points (bps). After finishing off last week at 358 bps, spreads have narrowed this week to the current level of 351 bps. It’s certainly been a wild year for the high yield market. Less than a year after spreads topped 1,000 bps and were within the 97th percentile of all historical readings, today spreads are two-thirds lower and just below the 20th percentile relative to all other readings. So, spreads are very low, but they’re not necessarily at a historical extreme. Click here to view Bespoke’s premium membership options for our best research available.

B.I.G. Tips – Charts We’re Watching – 2/10/21

Bespoke’s Morning Lineup – 2/10/21 – Russell Goes For Eight

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” – Robert Kiyosaki

Futures have been drifting higher all morning as positive momentum continues. Interest rates are modestly higher (although those increases have been erased following the release of CPI), and bitcoin is down nearly 3%. All in all, it’s been a pretty quiet morning so far. In economic data, CPI for January was just released and despite some concerns that the report would come in hot, the headline print was right in line with forecasts (0.3%) while the core reading was unchanged versus expectations for an increase of 0.2%. On a y/y basis, CPI is up just 1.4% versus expectations for an increase of 1.5%. As much as the Fed wants it, inflation just won’t seem to budge.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports from around the world, an update on the latest national and international COVID trends, and much more.

Although the S&P 500 and Dow ended Tuesday modestly in the red, small caps continued to shine as the Russell 2000 extended its winning streak to seven days. In the history of the Russell 2000 dating back to 1979, there have been seven prior winning streaks of seven or more trading days, so they are not particularly uncommon. Based on those prior streaks, the Russell’s performance on day eight has been an average gain of 0.15% (median: +0.18%) with positive returns 71% of the time. So, more often than not seven-day streaks make it to eight.

In more recent history, seven-day streaks have been a little less common. Since the start of 2019, there have only been two other streaks of seven or more trading days and they were both in 2019 (February and June).