Chart of The Day: Looking For REITurns After DHI Blows The Doors Off

B.I.G. Tips: Charts We’re Watching — 1/26/21

Bespoke’s Morning Lineup – 1/26/21 – Short Circuit

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Every once in a while, the market does something so stupid it takes your breath away.” – Jim Cramer

We’re continuing to see some crazy moves in the market once again this morning. Take a recent tweet from Elon Musk where he said that he ‘kinda’ loves Etsy. In reaction, the stock is up over 8% in the pre-market. Etsy has a market cap of about $25 billion, so that tweet alone was worth about $2 billion.

Elsewhere in the markets, US futures are higher on the heels of a rally in Europe. The overnight pattern heading into this morning is the complete opposite of yesterday. Whereas yesterday it was Europe that was trading lower after a strong session in Asia, today its Europe rallying after a so-so Asia session.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, earnings reports in Asia and Europe, Economic data out of Asia, an update on the latest national and international COVID trends, and much more.

Shares of GameStop (GME) are up another 19% in the pre-market this morning, and while a move like that in what just a few weeks ago was considered a washed-up company would normally raise eyebrows, but after the insanity we’ve witnessed in the stock over the last few days, today’s move is nothing. While this year’s moves in GME have been the biggest outlier, it’s part of a broader trend where traders have been targetting stocks with the highest short interest.

The chart below is from Monday’s Closer and shows the performance of Russell 3000 stocks so far this year grouped into deciles based on short interest. There has been a clear trend where stocks with higher short interest have outperformed their peers with lower short interest, but the most heavily shorted stocks stand in a league of their own gaining 22%! The deciles of stocks with the second and third highest average short interest levels are also both up over 10%, but they’re only up half as much as the most heavily shorted stocks.

So, which stocks make up this basket of most heavily shorted stocks? We don’t have enough space to list all of them, but in the table below we show the 16 stocks in the Russell 3000 that had more than 40% of their float sold short as of year-end. Topping the list is GameStop (GME) which had more than 100% of its float sold short as of year-end. Year to date, that stock is up an incredible 307%. The other stocks, however, haven’t been slouches either. Every single one of them is up at least 10% YTD, and half of them are up at least 50%. 50%!!!!

Daily Sector Snapshot — 1/25/21

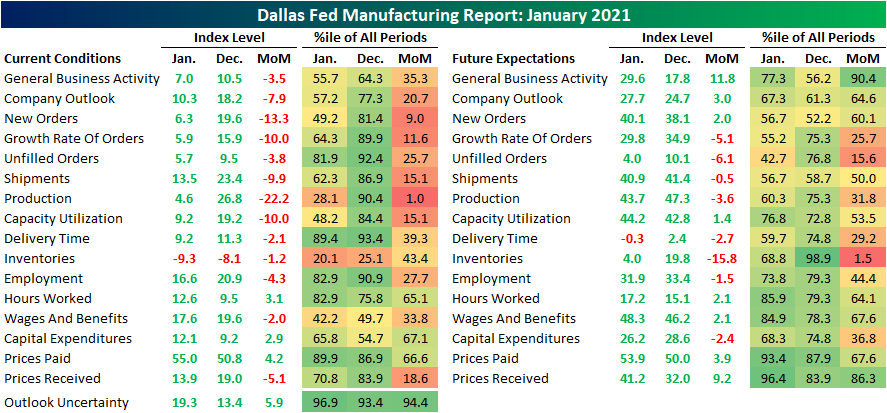

Disappointment Out of Dallas

Following very strong readings from the Philly Fed and preliminary Markit PMIs last week, the Dallas Fed’s Manufacturing report released this morning disappointed. The headline index came in at 7 compared to forecasts of a reading of 12 and last month’s adjusted reading of 10.5. That reading is still consistent with overall growth in the region’s manufacturing sector, but at a slower pace as the index fell to the lowest level since August.

The index for General Business Activity was far from being the only one to fall month over month. As shown below, breadth in this month’s report was terrible. Of the 17 different indices for current conditions, 13 fell month over month. That brought several of these readings from the top decile of historical readings down to the middle of their historical ranges. While the pullbacks were significant, only inventories remain in contraction. Meanwhile, breadth was a little bit better for the indices for future expectations.

One area that saw declines across the board were the indices concerning demand. As shown below, the indices for New Orders, New Order Growth Rate, Unfilled Orders, and Shipments were all lower in January. All of these are now at the lowest levels since June, or July in the case of order growth rate. These lower readings are still indicative of growth, but at a slower rate.

Just as we have seen in other recent manufacturing reports, survey respondents are reporting price increases. The index for prices paid rose to a reading of 55 from 50.8 in December. That is nearly in the top decile of all readings as the index sits at the highest level since April of 2011. The index for future expectations similarly ticked higher reaching its highest level since March of 2012.

While prices paid were higher, the same sort of acceleration in prices was not observed for prices received. The index for prices received fell from 19 down to 13.9. Although lower month over month, that is still around some of the highest levels of the past couple of years. Additionally, expectations are calling for prices received to follow the path of prices paid. The index for future prices received rose to the highest level since 2017 which was also in the top 5% of all readings.

Similar to prices received, the current conditions index for wages and benefits fell this month, but the index for future expectations rose much more sharply and to one of the highest readings of the past couple of years. In other words, although price hikes were not observed, they are foreseen on the horizon. For wages and benefits, that expected uptick comes as hiring continues with the index of employment remaining in expansionary territory. Additionally, hours worked rose this month from 9.5 to 12.6; the highest in September of 2018. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: S&P 500 Stocks Falling Below Their Moving Averages

Bespoke’s Morning Lineup – 1/25/21 – More Crazy Moves Beneath the Surface

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” – Robert Kiyosaki

It’s a mixed picture in futures markets this morning as the S&P 500 is set to open marginally higher while the Nasdaq is indicated up about 1%. At the individual stock level, the crazy moves of last week are continuing today as GameStop (GME) is up over 50% again, and a number of other high short interest and story stocks are trading up sharply in the pre-market. Economic data is on the light side this morning with just the Chicago Fed National Activity Index and the Dallas Fed Manufacturing Index.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, German sentiment data, an update on the latest national and international COVID trends, and much more.

The year is just three weeks old, but already we’ve seen some big moves in individual sectors. With its gain of 11%, the Energy sector has stolen the show, but the 5% gain in the Consumer Discretionary sector is nothing to sneeze at either. On the other end of the spectrum, Consumer Staples has already given up 3.8% this year while Industrials is down just marginally (-0.2%). The broader S&P 500 as a whole is up a respectable 2.3% on the year, and four other sectors – Materials, Financials, Technology, and Telecom Services – all have YTD gains within half of one percent of the overall market.

The gap of nearly 15 percentage points between the best and worst-performing sectors so far this year is one of the larger ones we have seen through the first 14 trading days of a year dating back to 1990. As shown in the chart below, just three years (2009, 2001, and 2000) have seen larger disparities to start the year while a number of other years have seen disparities nearly but not quite as wide as the one this year (1992, 1999, and 2006).

Bespoke Brunch Reads: 1/24/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Alternative Energy

Batteries Hidden Across New York Give the City a Backup Boost by Dimitra Kessenides (Bloomberg)

With disruptive natural disasters on the rise and battery prices on the fall, “microgrid” battery power facilities can be shoehorned in to cities like NYC to provide a backup to the traditional power grid. [Link; soft paywall]

Money Managers Look to Blue Seas for Green Investments by Julie Steinberg and Joe Wallace (WSJ)

As green energy capex scales up, investors are diving into all corners of production to try and make a buck, including owning and financing the ships which build and service offshore windfarms. [Link; paywall]

Chilly This Winter? Cozy Up to the Computer That’s Mining Bitcoin by Sarah E. Needlemen (WSJ)

Bitcoin mining operations are extremely power intensive and as a result of their massive processing activity send off huge amounts of heat. That byproduct is being repurposed to keep pets, vegetables, or even whole houses warm. [Link; paywall]

Housing

The Housing Market Boom Gets Another Boost From Biden by Conor Sen (Bloomberg)

Fiscal stimulus gives households who might not have the chance at owning a home a shot at cobbling together a down payment, with the possibility of reducing student loan burdens another tailwind for home buyers. [Link]

Scholarly Pursuits

The evolution of the Offshore US-Dollar System: past, present and four possible futures by Steffen Murau, Joe Rini, and Armin Haas (Journal of Institutional Economics)

A helpful review and primer of the mechanical foundations of the global financial system, focused on the role of the offshore US dollar market. [Link]

Platform Civics: Facebook in the Local Information Infrastructure by Kjerstin Thorson, Mel Medeiros, Kelley Cotter, Yingying Chen, Kourtnie Rodgers, Arram Bae, and Sevgi Baykaldi (Digital Journalism)

This paper uses quantitative and qualitative methods to identify what happens when Facebook replaces local media, with unsurprisingly toxic results. [Link]

History

What We Found in Robert Caro’s Yellowed Files by Dan Barry (NYT)

An amazing trip through the office of legendary biographer of Robert Moses and LBJ, including a fascinating anecdote about the desk that cured his bad back. [Link]

Investing

Up Is Good. Down Is Bad. by Jason Zweig (CreateSend)

Making the case that much-derided (in professional circles, anyways) traders are in fact pursuing the same sort of strategies that “fancy” quantitative investors do. [Link]

Data Security

Intel says hacker obtained financially sensitive information by Richard Waters (FT)

Hackers were able to access an infographic that was part of Intel’s earning release, forcing the company to publish the whole kit and kaboodle before the market closed. [Link; paywall]

COVID Vaccination

Israel COVID-19 ‘R’ reproduction number dips below 1 in first since vaccine drive (Reuters)

With more than one-quarter of the country vaccinated, the fastest vaccine effort in the world has helped push the previously raging COVID pandemic down in Israel. [Link]

Career Changes

Neuberger Berman’s Segal Is Retiring to Teach High School by Miles Weiss (Bloomberg)

A Neuberger fund manager that has held his seat since 1999 is retiring to pursue a masters in teaching and eventually working as a math teacher in New York. [Link]

Pay Your Lawyers

German online retailer Mytheresa valued at $3bn after US listing by David Carnevali and Sujeet Indap (FT)

Neiman Marcus acquired German online retailer Mytheresa for $200mm back in 2014, and now sits on a an impressive gain after the investment was kept remote from creditors during the company’s bankruptcy. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report: Equity Market Pros and Cons — Q1 2021

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition as we proceed through Q1 2021.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page two of the report, you’ll see a full list of the pros and cons that we lay out. We then provide slides for each “pro” or “con” that we’ve highlighted.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to Bespoke Premium. Enter “THINKBIG” at checkout to receive a 10% discount once the trial ends. You won’t be disappointed!