Bespoke’s Morning Lineup – 6/10/21 – Inflation Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Inflation hasn’t ruined everything. A dime can still be used as a screwdriver.” – H. Jackson Brown, Jr.

It’s inflation day in the US, as the May CPI is on tap for release or, depending on when you’re reading this, has already been released. The only other major report on the calendar is Jobless Claims at 8:30. Futures are mixed heading into the releases, treasury yields are modestly higher, and bitcoin is up over 4%.

Read today’s Morning Lineup for a recap of all the major market news and events including a recap of the ECB meeting, the latest economic news from around the world overnight, and the latest US and international COVID trends including our vaccination trackers, and much more.

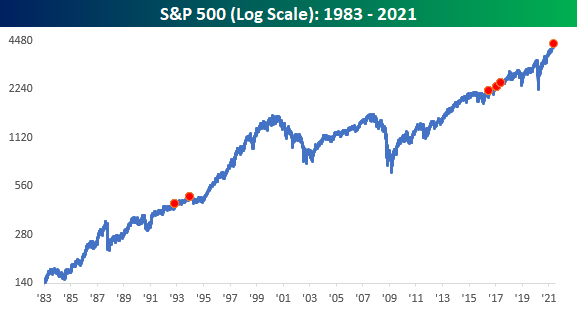

If you were up earlier this morning and in the Northeast US or parts of Eastern Canada, hopefully, you got a chance to view the eclipse. One ‘eclipse’ investors continue to impatiently wait for is the S&P 500 and its prior record high from early May. As we noted on the blog yesterday, the S&P 500 has made multiple attempts since the start of June to top the prior record, but after getting extremely close each time, either the buyers took a break or the sellers came in.

Wednesday marked the fourth straight day that the S&P 500 traded to within 0.15% of its record high but came up short each time. Since intraday data for the S&P 500 begins in the early 1980s, only five other periods have experienced either as long or longer of a stretch of days where the S&P 500 traded within 25 bps of a record high but never got there. The first of these periods occurred in the first half of the 1990s, while the last three all occurred in the year spanning the second half of 2016 and the first half of 2017.

So, does running out of steam just below record highs imply a market running out of gas or recharging ahead of a new leg higher. As shown in the chart below, the results were mixed, but more often than not, investors looked back at these occurrences from higher levels.

Daily Sector Snapshot — 6/9/21

Chart of the Day: Surging Stocks Not Just A US Phenomenon

Close, But No Cigar

It’s been quite a rangebound period for the S&P 500 over the last few days. Over the last 12 trading days, the spread between the S&P 500’s intraday high and low has been just 1.65% which ranks as narrower than any other period since July 2019. More recently, the upside has been especially capped. Ever since the start of June, the S&P 500 has made multiple attempts to take out its 5/7 record high, but each time it has failed. In just the last four trading days, if the S&P 500 doesn’t take out its record high today, the S&P 500 will have traded within 0.15% (0.11%, 0.14%, 0.03%, and 0.02%) of its all-time high from early May, but each time failed to take it out.

Coming up so close so often but falling short each time has to be disheartening for bulls, and it doesn’t happen particularly often either. The chart below shows streaks where the S&P 500’s intraday high came within 0.25% of an all-time but didn’t quite make it. Since intraday data for the S&P 500 begins in 1983, there have only been four other streaks of similar or longer duration. The first two were in the early 1990s, and then it wasn’t until 2016 that we saw a streak of six days. After that 2016 occurrence, there were two occurrences in the first half of 2017. Click here to view Bespoke’s premium membership options and sign up for a trial.

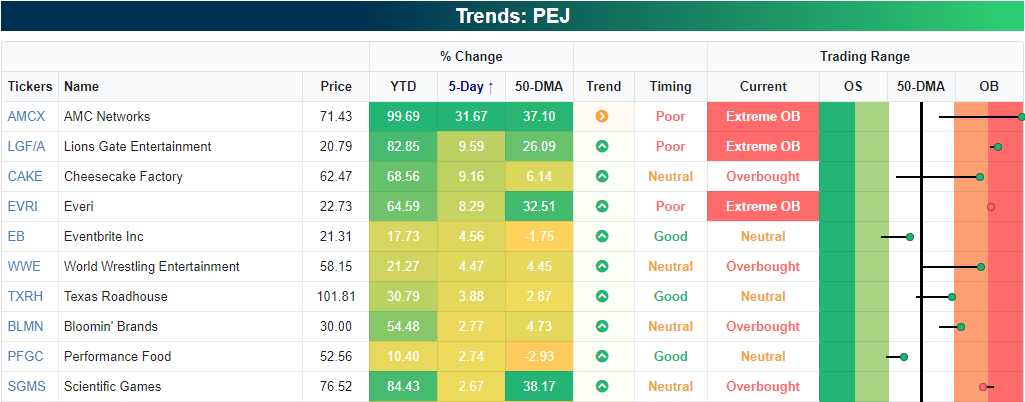

Leisure & Entertainment ETF (PEJ) and AMC Networks (AMCX) Caught In Meme Madness

Glancing through the US Groups ETF screen of our Trend Analyzer, by far the best performer over the past week has been the Dynamic Leisure and Entertainment ETF (PEJ). The portfolio is largely comprised of reopening stocks like restaurants, travel companies, and various forms of entertainment both live and otherwise. PEJ has rallied 11.77% in the five trading days ending yesterday in a move that has moved it deeply into overbought levels as it sits 16.71% above its 50-DMA. As the next best-performing ETFs in this screen, oil-related names like the S&P Oil and Gas Equipment and Services ETF (XES) and Oil Services ETF (OIH) have both risen well over 7% and are even more extended above their moving averages in percentage terms. As for the other ETFs, the S&P Biotech ETF (XBI) is another top performer and is the only one that is not overbought at the moment. Granted, it has retaken its 50-DMA in the past week, and its longer-term trend is worse than the rest of the screen.

Pivoting back to the Dynamic Leisure & Entertainment Portfolio ETF (PEJ), the double-digit move in the past week is actually part of a longer near-vertical move that began in mid-May. Since the May 12th low, PEJ has rallied 28.72% through today moving it to within 2% of its 52-week high from back on March 15th. Additionally, looking just at the nearly 12% rally of the past week, a massive portion of the move came last Wednesday when it rose over 10% in a single session. In fact, last Wednesday was so volatile that even after a few days of higher closes, it is still below last Wednesday’s intraday high.

It is hard to mention parabolic moves these days without some mention of a meme stock, and of course, the massive move for PEJ is meme-related. Below we show the ten best-performing holdings of PEJ over the past week. Topping the list is AMC Networks (AMCX) with a 31.67% gain in the past week alone. After that move, AMCX is just shy of doubling year to date. While sharing a similar name, AMCX is not to be confused (although the meme traders seem to be doing just that) for AMC Entertainment (AMC) which has taken center stage with regards to meme stocks lately. In other words, the AMCX has gotten caught up in the meme stock mania alongside AMC. While AMCX is up big, the chart is extremely extended above its 50-DMA, and at the moment is setting up in what appears to be a head and shoulders pattern. From a technical perspective, that is viewed as a bearish pattern, and for that pattern to be confirmed, it would have to fall below the past several months’ support at around $44 after failing to move above the January and more importantly mid-March highs.

While it has no doubt had an impact, the move in PEJ has not solely been due to the strength of AMCX. The stock only ranks as the tenth-largest holding accounting for 3.26% of the portfolio. There have also been a handful of other strong performers pulling weight like Lions Gate Entertainment (LFG/A) and Cheesecake Factory (CAKE) which both have risen over 9%. Everi (EVRI) has also risen considerably, notching an 8.29% five-day gain. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 6/9/21 – It’s Post Time!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The reason that you can win at poker and horse racing is the same – you are not betting against the house; you are betting against the other players.” – Steven Crist

Forty-eight years ago today, spectators in the hot, humid long island sun witnessed one of the greatest performances in the history of horse racing, and in the winner’s circle, there was Secretariat, winner of the coveted Triple Crown for the first time in a quarter-century after completing one of the greatest runs in horse-racing history. The horse ran the fastest Kentucky Derby ever, a record that still stands today, easily won the Preakness (unofficially in record time), so it was only fitting that the win at Belmont came in at a record of 31 lengths and likely barely breaking a sweat.

Like poker and horse racing, when it comes to investing, rather than betting against the house, which always wins, you are betting against the crowd. That means that the more informed you are as an investor, the better your chances of success. Just as a bettor who wagers based on the name of the horse or the color of their silks usually leaves lighter in the wallet than when they arrived, an investor chasing the hottest stocks or most popular trends usually, even during one of the greatest runs in market history usually ends worse off than the person on the other side of the trade.

US equity futures are right around the flatline this morning, and the overnight session was a snoozer as futures have traded in a range of less than 0.25%. Crypto assets have seen a bounce after yesterday’s plunge, and commodities are mixed.

Read today’s Morning Lineup for a recap of all the major market news and events including an update on infrastructure talks, the latest economic data from Asia and Europe, and the latest US and international COVID trends including our vaccination trackers, and much more.

Yesterday, investors who still read a physical newspaper were greeted with some interesting headlines related to inflation. Right below the fold on the front page of the Wall Street Journal, they saw “Commodity Prices Skyrocket, Adding to Inflation Fears”. Then on the front page of the Markets section (B1) right at the top was the headline “Traders Bet on Return of $100 Oil”. With headlines like that and a CPI report coming up on Thursday, weakness in the Treasury market would be a safe assumption. Not so fast. While the yield on the 10-year US Treasury was an already low 1.57% when yesterday’s Journal came off the presses, ever since then, it has done nothing but go down. In fact, as of this morning, the yield dropped below 1.5% and on pace for the lowest closing yield in over three months.

Inflation Issues For Small Businesses

In addition to getting a gauge on small business optimism, the NFIB’s monthly survey of small businesses also asks respondents about the biggest issue they face operating their businesses. On a combined basis, the biggest concern among small businesses is taxes or government red tape. Combined, these two issues were reported as the biggest problem for 35% of surveyed firms with taxes being the main culprit after rising 3 percentage points month over month. Right on the heels of government-related concerns, labor concerns loom large. 34% of respondents said that cost or quality of labor pose the biggest issue their business face with costs accounting for 8%, unchanged from last month, while the quality of labor jumped from 24% to 26%. For the latter, that is in the top 1% of all readings hitting the highest level since November 2019. If there is any positive to pull out of what Main Street views as the biggest problems, it is the lack of companies citing poor sales. Just 5% of respondents saw this as the biggest issue; down 13 percentage points versus last year, and it is now at the lowest level since September 2018. On the downside, the number of firms reporting problematic inflation has risen rapidly going from 2% at the end of 2020 to 8% today. Such an elevated reading has not been observed since April 2012. Click here to view Bespoke’s premium membership options for our best research available.

Daily Sector Snapshot — 6/8/21

Chart of the Day: Small Business Outlook Takes a Nosedive

Small Businesses Can’t Find Workers And Are Raising Prices

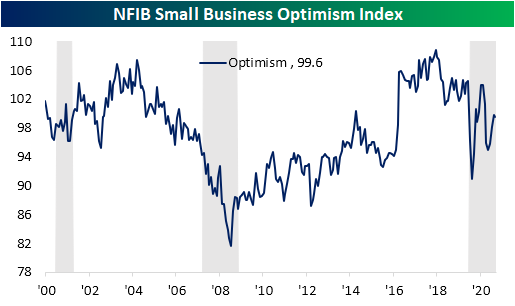

The NFIB released its monthly reading on the sentiment of small businesses this morning. In the past, we have noted how the results of this survey are often correlated with political happenings. As such, the index dropped in the wake of the election but found a bottom in January. Since then, it has remained weaker than during the Trump years, albeit it has also improved almost every month this year. That is except for the most recent month. May snapped a three-month winning streak with a slight decline from 99.8 to 99.6.

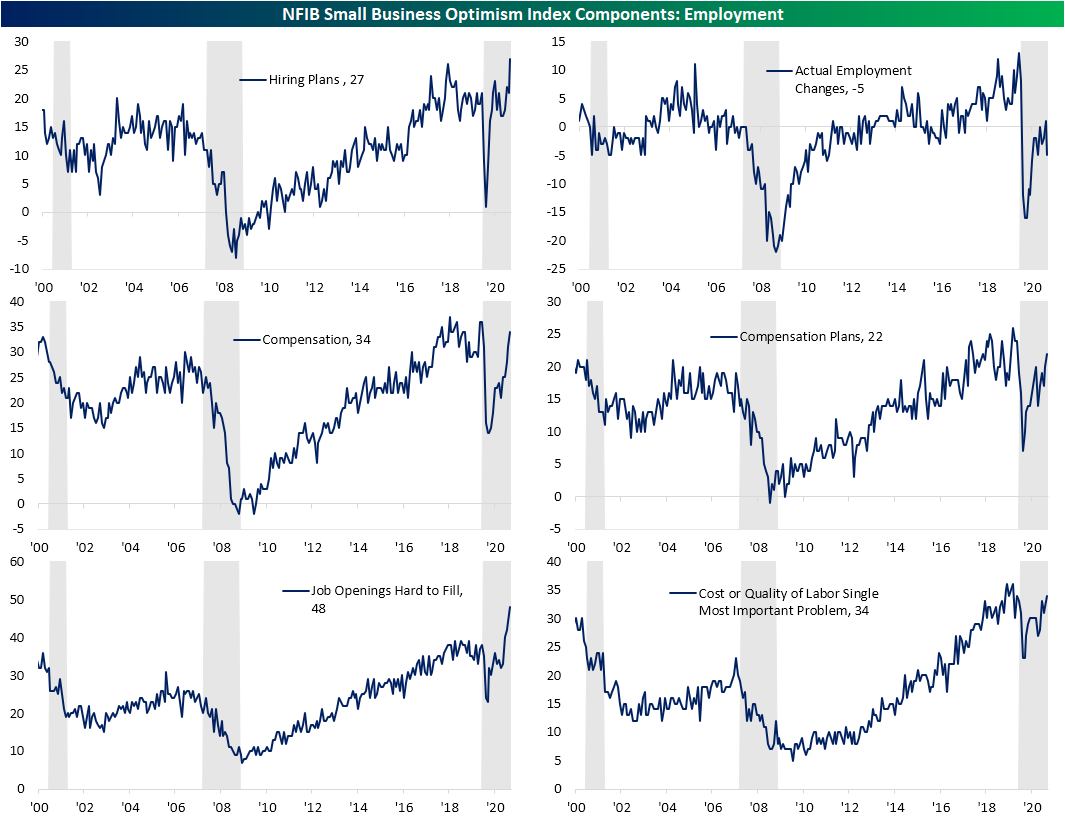

With the headline number slightly lower, breadth in the May report was fairly mixed. Of the ten inputs to the optimism index, half were higher, two went unchanged, and three were lower versus April’s readings. Three of those indices that moved higher—Plans to Increase Employment, Current Inventory, and Job Openings Hard to Fill—set new records. While it is not an input to the headline reading, the index for Higher Prices also rose to a new record high. Overall, the survey implied generally strong conditions with a few areas of concern: labor market tightness and inflation.

The report showed solid realized sales as the index of Actual Sales Changes rose 4 points to 7. That marks a return to pre-pandemic levels. On net, a higher share of businesses also expects sales to continue to improve, although only at 3, the index is still at the low end of its historical range. In spite of the higher actual sales, a higher share of businesses are reporting worse bottom-line results versus the prior three months as the index for Actual Earnings Changes fell to -11.

In an attempt to make up for those weaker margins, a record share of businesses also are reporting that prices are higher than three months ago. A net of 40% of respondents reported that they are raising average selling prices; a record high in the data dating back to 1986. The NFIB noted that price hikes were most common for wholesalers (65% reported higher prices vs. 2% lower) and manufacturers (47% reported higher prices and 1% reported lower). That is consistent with other data of the past few months showing prices are flying higher. Likely as a result of all of this in addition to other labor concerns (more on that below), the Outlook for General Business Conditions fell to -26, the lowest level since 2012 and in the bottom 1% of all months. Additionally, the share of businesses reporting now as a good time to expand ticked lower.

One major area of strength, at least in terms of demand, is employment. A net 27% of respondents reported that they plan to create new jobs within the next three months; surpassing the prior record high from August 2018 by a full point. But even though businesses are putting the offers out there, on net fewer businesses reported an actual employment change. In fact, that index fell sharply by 6 points; a move that ranks in the bottom 2% of all monthly changes. Additionally, a record share of businesses reporting job openings as hard to fill as 34% of businesses report their biggest problem to be either the cost or quality of labor. That is indicating significant labor market tightness. As a result, more businesses are or are planning to raise compensation with those indices at the highest levels of the past year and consistent with readings from 2017 up through the onset of the pandemic. Those higher costs are likely one reason for the weaker reading in actual earnings changes and higher selling prices previously mentioned.

As for the other side of the production function, capital expenditures are not being raised in any sort of significant way nor are plans to increase expenditures. Potentially to get ahead of the strong demand and labor supply mismatch, businesses are raising inventory levels with a record share of businesses reporting that current inventory levels are “too low”. Rising to 8, that index took out the joint high of 7 from last month and December. Click here to view Bespoke’s premium membership options for our best research available.