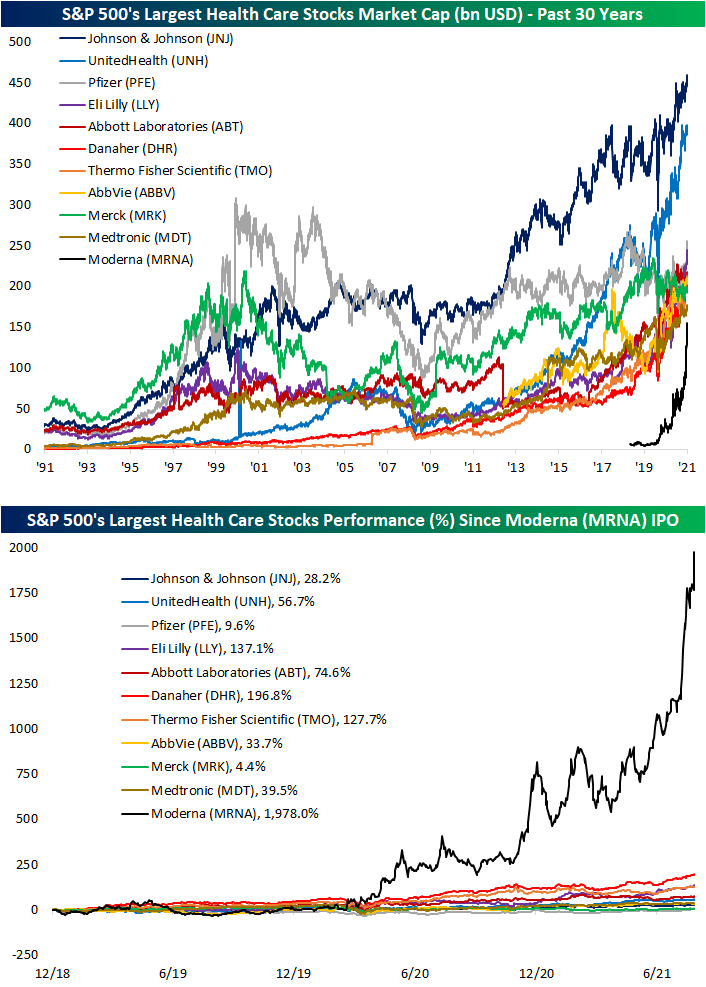

Moderna’s (MRNA) Massive Market Cap

As could have been expected in the midst of a global pandemic, one of the most rapidly growing companies has been vaccine producer Moderna (MRNA). As shown below, since the start of the year, the company has seen its market cap nearly quadruple to $162.2 billion; that is the largest growth in market cap of any S&P 500 stock year to date. In fact, those big gains saw MRNA go from the 162nd largest S&P 500 stock at the end of last year to the 58th largest today. And that compares to pre-pandemic (the end of 2019) when MRNA was only valued at $6.52 billion. While it was not part of the index back then, MRNA would have been the eighth smallest S&P 500 stock at the time with that market cap. That massive growth now leaves the stock as the tenth-largest company of all S&P 500 Health Care stocks with the next largest being Medtronic (MTD). While there are a handful of larger stocks in the Health Care sector, again, no others have seen as rapid of growth. With that said, other vaccine-related stocks like Pfizer (PFE) and Johnson and Johnson (JNJ) have also seen significant market cap growth.

MRNA joined the upper echelon of Health Care market caps in a very short span of time. As shown in the second chart below, since its IPO in late 2018, MRNA has risen nearly 2,000%. Of the ten other largest S&P 500 Health Care stocks, the next best performer has been Danaher (DHR) with just under a 200% gain in that same span of time. Click here to view Bespoke’s premium membership options.

Bespoke’s Consumer Pulse Report — August 2021

Bespoke’s Morning Lineup – 8/4/21 – Jobs Stall

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The most important investment you can make is in yourself.” – Warren Buffett

The yield on the 10-year US Treasury continues to crater this morning following the much weaker than expected ADP Private Payrolls report. As of this writing, the yield is down to 1.14% which is a level that most investors probably thought they would never see again back in early April. Coming up at 10 AM, we’ll get the latest read on the Non Manufacturing sector from ISM. Contrasting the weaker than expected economic data, earnings news has been mostly positive but hasn’t been strong enough to push futures into positive territory.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including a recap of SEC Chair Gensler’s comments related to crypto, the latest US and international COVID trends including our vaccination trackers, and much more.

Semiconductors have been trading in a range of a little over 20% for all of 2021, but as we noted in last week’s Bespoke Report, the group looked to be making a breakout attempt to close out the week. This week, that upside move appears to have been confirmed as the Semiconductor ETF (SMH) has traded further outside of its 2021 range. Going forward, look for the top of that former range to act as support in any pullback.

Daily Sector Snapshot — 8/3/21

Chart of the Day – REIT Occupancy Rates Recover

Bespoke Matrix Of Economic Indicators – 8/3/21

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

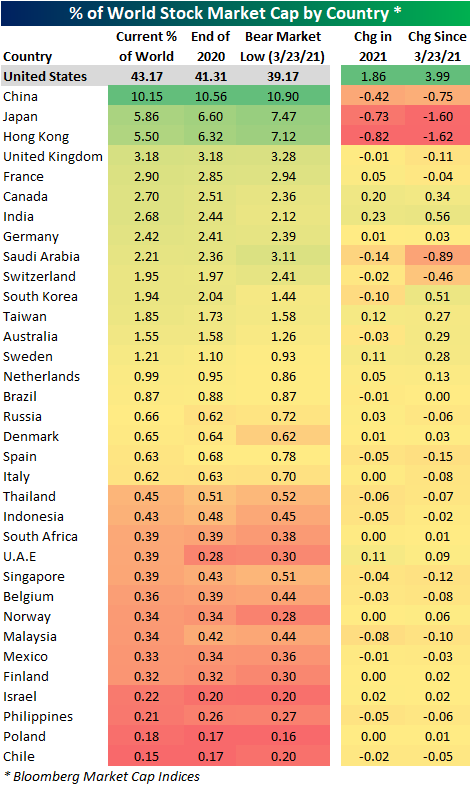

US Still Dominates Global Market Cap

On Friday, we highlighted some of the long-term charts and generally extended readings of the stock markets of various major global economies following big gains over the past year and a half. While equities around the globe have surged, it is still the US that has gained the most in terms of the percentage of world market cap. As shown below, according to Bloomberg’s market cap indices the US currently accounts for 43.17% of total global market cap. That is up 1.86 percentage points from the start of the year and is up roughly 4 percentage points since the bear market lows last year. As for the other largest countries, China is the only other one to account for a double-digit share at 10.15%, although, that is down significantly from the start of the year. Japan and Hong Kong are two others of the largest equity markets, and they have both lost even larger shares.

With US equities having continued to grow, the country’s share of world stock market cap is now around some of the highest levels since the fall of 2004. Those gains to the US’s share of global market cap are also in the context of a general upwards trend that has been in place for the better part of the past decade now.

For most of the year, Chinese and Hong Kong equities have traded off of their highs and more recently have fallen dramatically as a result of concerns surrounding the region’s regulatory picture. While the declines were quite dramatic, they have not necessarily brought the countries’ combined share of market cap to any sort of major new low. With that said, prior to the past week’s bounce, at the July 27th low, the one-month drop in the combined share of total market cap stood in the bottom 2% of all readings. Click here to view Bespoke’s premium membership options.

Bespoke Stock Scores — 8/3/21

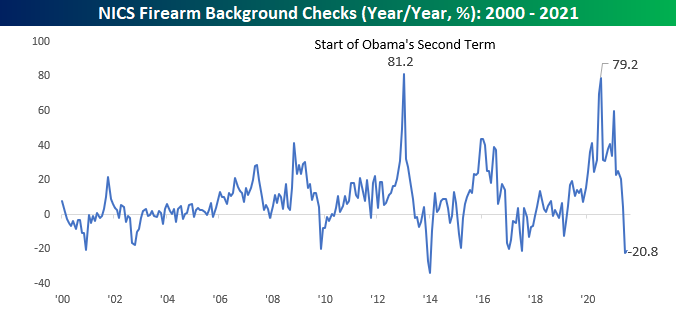

Background Checks Lose Their Spark

FBI background checks for the month of July have been published and showed another sharp decline. For the month of July, background checks totaled 2.883 million which was down 172K from June’s total. That marks the fourth straight monthly decline in which total background checks have dropped by 1.8 million from the record high of 4.692 million in March. In terms of the raw number of checks, the current four-month decline is the largest on record, and on a percentage basis, the 38.6% drop is the largest since early 2014.

On a y/y basis, the surge in background checks brought on by the pandemic and civil unrest last year looks like it has been fully unwound. After nearing a record surge of 79.2% early last year, we’ve now seen two straight months of 20%+ y/y declines. The last time we saw a y/y decline of this magnitude was back in July 2017.

With such large declines in background checks, you wouldn’t think that would be a positive backdrop for gun companies, and judging by the recent performance of the two publicly traded gun companies, you would be partially right. While both stocks up still up YTD, they have pulled back sharply from their recent highs. On July 1st, both stocks traded at 52-week highs, but since then SWBI has dropped over 38% while RGR is down 18%. In the case of SWBI, its peak from late 2020 has so far held up, but for RGR, support from the highs late last year just recently broke. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 8/3/21 – Let’s Try This Again

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A wise man will make more opportunities than he finds.” – Francis Bacon

Futures are currently trading pretty much where they were at this time 24 hours ago. Yesterday, the bulls couldn’t hang on as a new multi-month low in the 10-year yield raised concerns that economic growth was weakening. Rates are modestly higher this morning reversing a small portion of yesterday’s decline. Over in Europe, the STOXX 600 is higher and that follows a relatively weak night over in Asia. There’s not a lot of economic data to contend with today (Factory Orders at 10 AM), but the earnings stream which already picked up after the close yesterday will continue in full force today. For the entire week, nearly 30% of companies in the S&P 500 are scheduled to report. Try staying on top of all those reports!

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including a record drop in Spanish unemployment, the latest US and international COVID trends including our vaccination trackers, and much more.

One question we’re often asked is that with the Delta variant pushing COVID case counts higher, is the market being too complacent of the risks? Rising case counts are an alarm, but looking at how the wave has progressed in other areas of the world provides a blueprint that the Delta wave may be severe in terms of transmissibility, but it hasn’t been long-lasting. Additionally, the market is more concerned with consumer behavior and to this point, it appears as though Delta’s impact has not caused much in the way of a change in consumer behavior.

A case in point is airline passenger throughput from the TSA. Yesterday was the fifth straight day since the pandemic began that US airports processed more than 2 million passengers per day. The last time that happened was in mid-February 2020. Included in that 5-day run was the first Saturday since last March that more than 2 million passengers traveled on a Saturday, leaving Tuesday and Wednesday as the only two days of the week that haven’t topped the 2 million level since the pandemic began.