Chart of the Day: One Year Anniversary of the Peak in Technology

Bespoke’s Morning Lineup – 9/1/21 – Seven Down…

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Uneasy lies the head that wears a crown.” – William Shakespeare

The calendar may have changed, but the market hasn’t seemed to notice as futures are continuing the gains we saw to close out August. The first major economic report of the month was ADP Private Payrolls, and for the second straight month, it missed expectations by a wide margin (over 250K). Still ahead, we’ll have the Markit Manufacturing PMI report at 9:45 and ISM’s Manufacturing report at 10 AM.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

August marked the seventh straight month of gains for the S&P 500. That’s the longest winning streak for the index since the ten-month streak that ended in January 2018. Including the current streak, there have now been 15 winning streaks of seven or more months for the S&P 500 since 1945, and of the prior fourteen, the majority (10) went on to at least an eighth month, and whether or not the streak extended to eight months or not, the S&P 500’s median performance in the month after the seventh straight up month was a gain of 1.6%. The longest winning streaks for the S&P 500 all came in the 1950s when there were three separate winning streaks of 11 months, and the longest since then was the ten-month streak ending in January 2018.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Daily Sector Snapshot — 8/31/21

Chart of the Day: September 2021 Seasonality

B.I.G. Tips – Decile Analysis of Q3 So Far

Emerging Markets Leave China Behind

In last night’s Closer, we noted the record underperformance of Chinese equities relative to the US over the past six months. As a result of the weakness in Chinese equities, the MSCI Emerging Market ETF (EEM)—which has roughly a 37% weight in Hong Kong and Chinese stocks—is well off of its highs and has been trending lower over the past several months. Today, EEM is up a healthy 1.37%, but that brings it just short of its 50-DMA which recently fell below its 200-DMA. That is also at similar levels to the lower high from the start of this month.

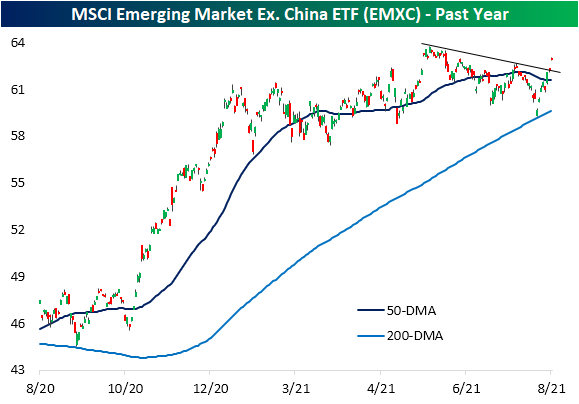

When factoring out China, emerging markets look much better. Again, the MSCI Emerging Market ETF that excludes China (EMXC) is currently 1.13% below its 52-week high, but the downtrend that has been in place since the early June highs has been on the ropes over the past couple of sessions. Yesterday saw the ETF trade and close right at that downtrend line, but the 1.15% gain today has smashed through it. That leaves EMXC at the highest level since June 15th. The ETF is also at some of the most overbought levels (1.8 standard deviations from its 50-DMA) since then.

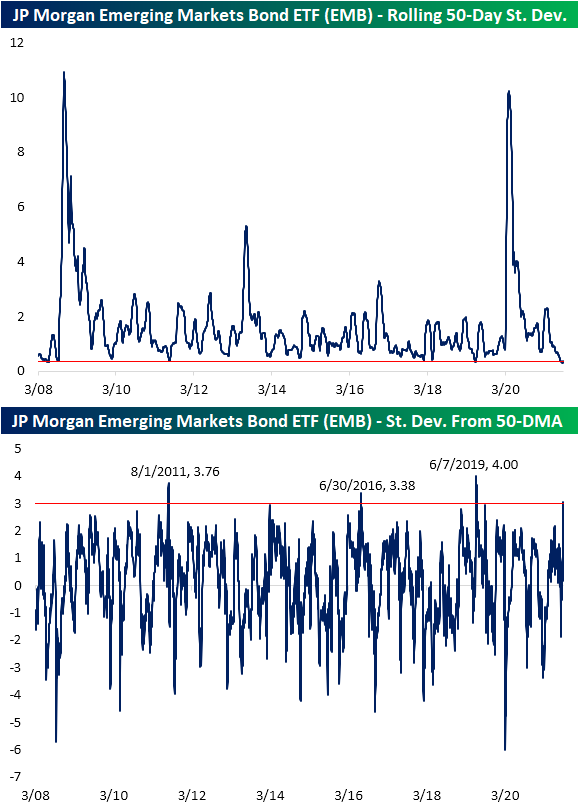

Pivoting over to bonds, looking at the Fixed Income screen of our Trend Analyzer, the best performer over the past five days is also in the EM space. The USD Emerging Markets Bond ETF (EMB) had been mostly flat throughout the summer trending right alongside its sideways 50- and 200-DMAs. Significant gains last Friday and yesterday led EMB to break out of that range as it reaches some of the highest levels since February today.

As previously mentioned, EMB has not ventured far from its 50-DMA recently. In fact, the rolling 50-day standard deviation has been right around some of the lowest levels on record since EMB began trading in 2008. Given that lack of volatility, the rip higher this week has resulted in the ETF moving well beyond the upper end of its narrow trading range. In fact, yesterday the ETF closed over 3 standard deviations above its 50-DMA. That joins only 14 other days where the ETF closed at least 3 standard deviations above its 50-DMA with the most recent of those back in June 2019 when it reached as high as 4 standard deviations above its moving average. Click here to view Bespoke’s premium membership options.

Mid-Caps Moderate

To round out the month of August, the major indices are slightly lower on the day. Overall, in the final week of the month, small caps like the Micro-Cap ETF (IWC) and Russell 2000 (IWM) have generally outperformed although they are coming from below their 50-DMAs, and yesterday they saw a reversal lower. Large caps have posted smaller gains but are reaching new record highs. The price action of mid-caps, on the other hand, has been a mix of small and large caps. Mid-caps, like the S&P MidCap 400 ETF (MDY) and Core S&P MidCap ETF (IJH), are broadly overbought and have also posted solid gains in the past several days of around 2%. Additionally, whereas this week they are on the cusp of extreme overbought territory, last week those same ETFs were still within one standard deviation of their 50-DMAs.

While mid-caps have made a solid move higher over the past five days, like small-caps, they have pivoted lower in the past couple of sessions. From a charting perspective, those moves lower also come right as IJH and MDY made a run at their highs from the final days of April. Having rejected that resistance, there is the potential for nearby support around the highs from earlier this month and early June and then the 50-DMA below that. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 8/31/21 – That’s a Wrap

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I always tried to turn every disaster into an opportunity.” – John D. Rockefeller

We’re six and a half hours of trading from wrapping up the month of August and the seventh straight month of gains for the S&P 500. Futures have been drifting lower this morning after gains overnight, but so far the declines remain modest. One catalyst cited for the weakness has been comments from an ECB Governing council member (Holzmann) suggesting that the ECB should at least start to talk about how it will remove policy stimulus.

On a brighter note related to COVID, Bloomberg reports this morning that beginning tomorrow Citigroup will increase capacity in its Hong Kong offices to 90% from an already relatively high level of 75%. Citi’s move follows similar moves from Goldman Sachs and Bank of America earlier this Summer. While Hong Kong’s case burden is considerably less than most other areas of the world, it’s encouraging to see at least one area of the world returning somewhat back to normal.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

While the ECB now joins other central banks around the world in discussing or already starting to remove accommodation, we’d note that August data hasn’t looked particularly good so far. Overnight, we had reports out of China showing that activity in the Manufacturing and Services sector slowed considerably. Here in the US, regional manufacturing Federal Reserve surveys for the month of August also showed a notable deceleration in momentum. While the headline readings of the five Federal Reserve surveys all still showed growth (with some at healthy levels), they all decelerated relative to July, and only the KC Fed survey managed to exceed expectations. We’ll get a further read on the state of the economy in August with the Chicago PMI today at 10 AM and then the ISM Manufacturing report at 10 AM tomorrow.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.