S&P 500 Sector Weightings Report

Daily Sector Snapshot — 10/13/21

A Case for the Shorter Trading Day

Since the S&P 500’s last high on September 2nd, despite an average opening gap of around 5 basis points (bps), the index has averaged a 17.7 bps decline from open to close. Looking at the intraday pattern in that time, the morning through the early afternoon typically sees the index erase any gains from the open. After a small bounce in the mid-afternoon, the final hour has averaged a sharp reversal lower.

Taking another look at intraday patterns, below we show the cumulative performance in 2021 of $100 through a few hypothetical strategies. The first is buying at the close and selling one hour into the following session (dark blue line). The next would be buying at the start of the final hour and selling at the close (red line). The third would be holding for the time between 10:00 AM to 3:00 PM (gray line). The last would be a simple buy and hold from close to close (green line). As shown, “smart money” is not looking particularly bullish this year. Had you only owned the S&P in the last hour of the day, your $100 at the start of the year would be down to just over $88. Meanwhile, owning the opening gap into the first hour only would leave an investor up almost $16. While you would be holding on for a longer period of time, owning in the middle of the day would have resulted in decent gains, but the best strategy has been to buy and hold. which captures returns both throughout the trading day and outside of regular trading hours.

Not shown in the chart below is if the trading day ended at 3PM instead of 4. If the equity market simply closed at 3 PM every day (or you sold at 3 PM and bought again at the close), that strategy would be up roughly 30% YTD! A three o’clock closing bell on the east coast has a nice ring to it! Click here to view Bespoke’s premium membership options.

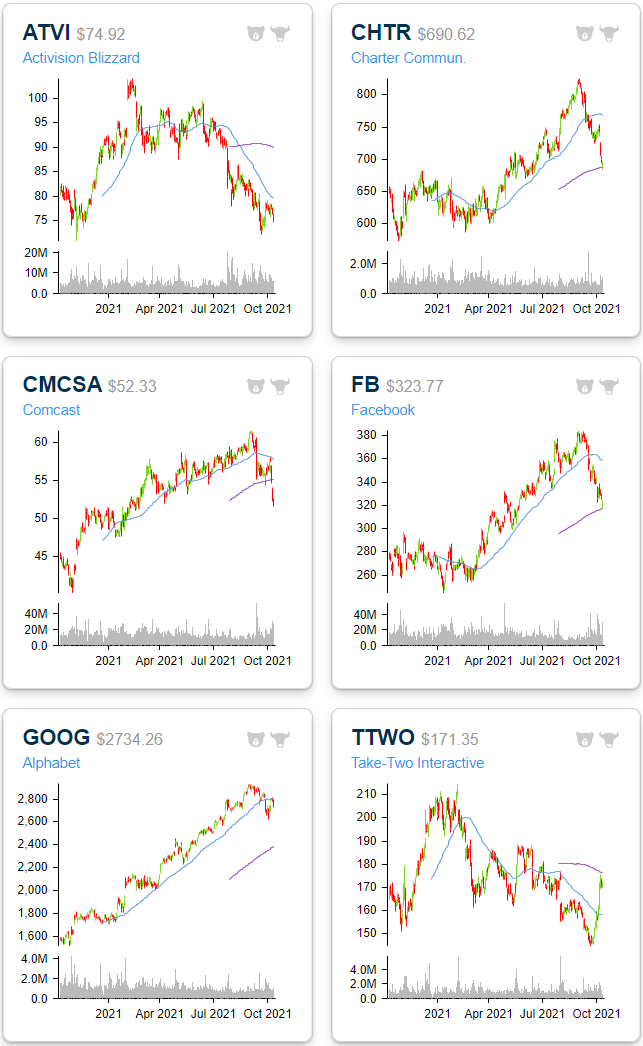

Communication Services (XLC) Breakdown

Looking at sector performance over the past week, the weakest sector has been Communication Services (XLC) with a decline of over 2% in the five days ending yesterday. That brings the sector over two standard deviations below its 50-DMA. Health Care (XLV) is the only other sector at extreme oversold levels although its recent decline has been much more modest.

Whereas most of the past year has seen XLC consistently hold above support at its 50-DMA, since the start of September, the sector has trended lower, and over the past month, it has also been below its 50-DMA. Now smack dab between its 50 and 200-DMAs, yesterday’s decline resulted in XLC falling below support around $79. That level formerly marked short-term highs in April and May of this year and a low/test of the 50-DMA in mid-July.

While that breach of support has not necessarily been dramatic, the same cannot be said for many of the sector’s stocks. For example, telecoms have gotten crushed as AT&T (T), T-Mobile (TMUS), and Verizon (VZ) have all collapsed in recent days with each one extremely oversold. Of these, only TMUS has appeared to have found any hint of support at recent lows. The other stock in this industry, Lumen Tech (LUMN), has also been moving lower but has not collapsed like the others.

As for other members of the sector outside of that industry, names like Charter (CHTR), Comcast (CMCSA), Facebook (FB), and Alphabet (GOOG) have also pulled back sharply recently breaking longer-term uptrends. Also, since many of these stocks have very large market caps, their impact on the sector’s performance is greater. On the bright side, CHTR and FB have appeared to have found some support at their 200-DMAs while the opposite is the case for CMCSA. Similarly, GOOG just recently failed to move back above its 50-DMA. As for the video game stocks, Take-Two Interactive (TTWO) also failed to move back above a moving average recently while Activision Blizzard (ATVI) has been in a steep downtrend over the past few months with a failed attempt to break out of that trend in the past several days.Click here to view Bespoke’s premium membership options.

Chart of the Day – QQQ Weak Closes

Bespoke’s Morning Lineup – 10/13/21 – Bracing For Inflation Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Inflation is bringing us true democracy. For the first time in history, luxuries and necessities are selling at the same price.” – Robert Orben

Earnings season kicked off this morning and all five of the major companies reporting before the bell topped consensus estimates. In terms of share price reactions, four of the five names are either flat or slightly higher, but SAP which reported an earnings triple play is trading up over 5% in the pre-market. So far, so good.

With all of the earnings reports out of the way, the focus will shift to CPI and how bad the inflation pressures were on the economy in September. Then, at 2 PM the FOMC will release the minutes from its most recent meeting three weeks ago.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

With consensus estimates anticipating headline CPI to rise 0.3% on a month/month basis in September, it would represent the 10th straight month that headline inflation came in ahead of the five-year average of 0.2%. That being said, if the actual m/m increase comes in close to forecasts of 0.3% it will clearly represent a slowdown in the pace of price increases from the spring and summer months. Still above average, but getting back more in line with the historical norm.

Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Bespoke Stock Scores — 10/12/21

Daily Sector Snapshot — 10/12/21

Labor Top of Mind For US Small Business

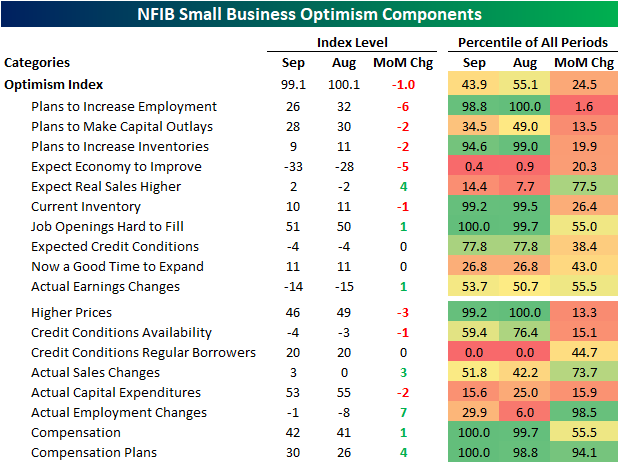

The most important problems section of this month’s NFIB report on small businesses showed one clear problem: labor. A combined 40% of businesses reported either cost or quality of labor as their single most pressing issue. While the percentage of respondents stating the quality of labor as the biggest issue went unchanged at 28%, there was a record one-month increase in the percentage of firms stating costs were their biggest problem. The percent reporting cost of labor as their biggest issue rose 4 percentage points to a record high of 12%.

While a massive share of respondents reported either cost or quality of labor as their biggest issue, the next largest share sees government-related issues as the biggest concern. A combined 28% reported either taxes or government requirements & red tape as their most important problems which is actually a muted share on a historical basis. Even though it was up 1 percentage point to 17% in September, the percentage reporting taxes as their biggest problem sits in the bottom decile of the historical range and the reading on government requirements and red tape sits in the 15th percentile.

As for the other readings, Poor Sales, Competition from Big Business, and Financial & Interest Rate concerns are at record lows. While not at a record low, the Cost/Availability of Insurance fell by a record amount. Inflation also experienced a historic drop of 3 percentage points in September. With that said, 10% of owners still reported that as their biggest problem which is still in the top 5% of all readings. The single biggest gainer in September was “Other”. This category is not as old as the other problems but the 7 percentage point surge was a record jump in a single month and leaves the reading at one of the highest levels to date. Click here to view Bespoke’s premium membership options.

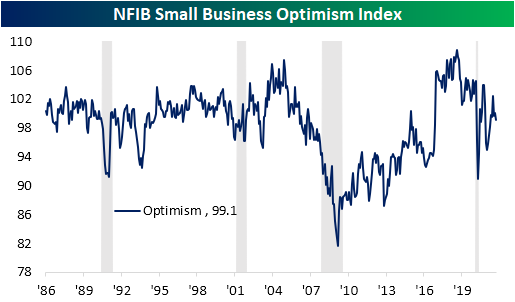

Small Business Optimism Back Below 100

Small business optimism measured through the NFIB’s monthly survey dipped in September by a full point to a six-month low of 99.1. That is in the middle of the pandemic range as small business sentiment never quite fully recovered to pre-pandemic levels let alone its August 2018 record high.

Breadth in this month’s report was mixed perhaps leaning slightly more negative with nine categories falling month over month while seven were higher. Another three went unchanged. The largest declines were for plans to increase employment and expectations for the economy to improve. While those were the two biggest decliners, they are coming from polar opposites of their respective ranges. The index tracking plans to increase employment remains in the top 2% of readings even after the six-point decline that ranks in the bottom 2% of all monthly moves. Meanwhile, the magnitude of the decline in the index for expectations for the economy to Improve ranks in the 20th percentile of all other monthly readings, but that leaves it just off of a record low. In other words, readings throughout the report are nuanced with some at or near record highs and others at or near record lows.

As previously mentioned, Outlook for General Business Conditions plummeted in September showing that a net -33% of reporting owners foresee better business conditions in six months. The only two months with weaker readings on record were November and December of 2012 just after President Obama’s re-election. Given that weak reading, the number of firms that see now as a good time to expand remains muted with this month’s reading unchanged at 11 which is short of the bottom quartile of the historical range. Actual sales changes improved back to a positive reading that sits in the middle of its range. Sales Expectations also improved to positive territory, but that reading is far lower with respect to its historic range. Earnings changes also improved as fewer businesses reported higher prices although that reading remains well above any other period in the history of the report.

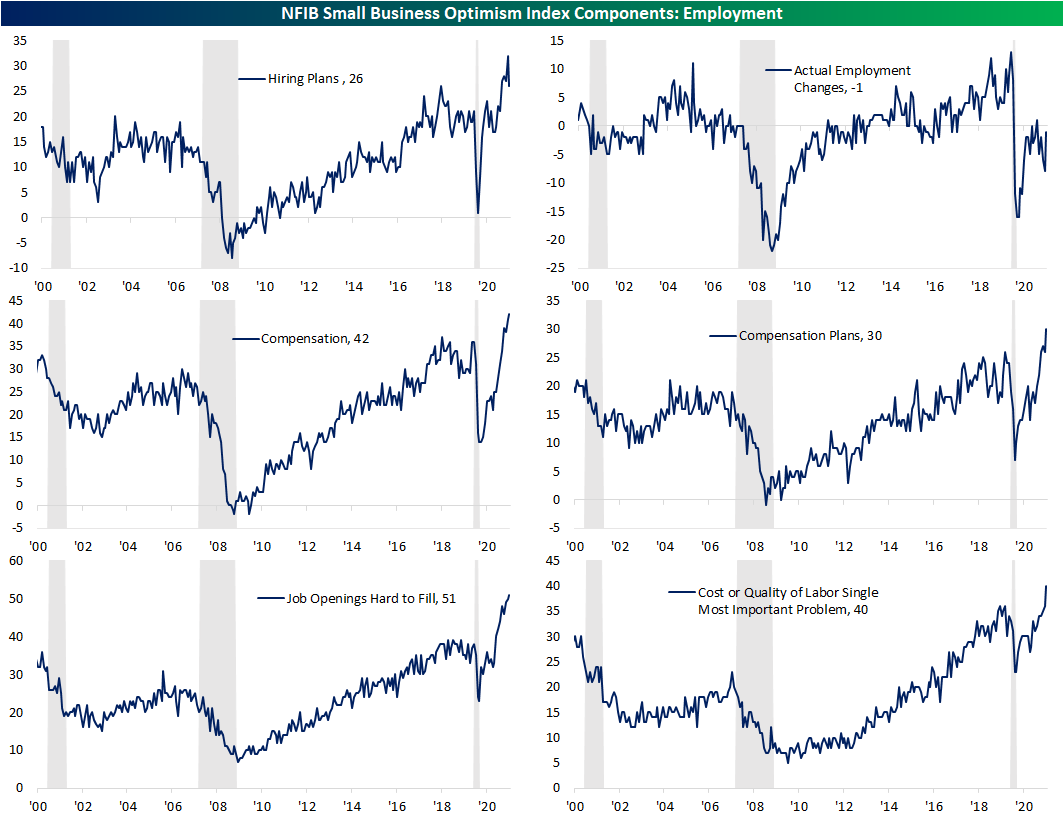

In today’s Morning Lineup, we discussed some of the price and labor pressures evident in the report. Revisiting these, firms continue to show strong albeit slowing labor demand as hiring plans remain elevated but dropping sharply month over month. Meanwhile, Actual Employment Changes rose sharply, though, this reading remains negative. Additionally, firms have continued to raise compensation and plan to continue to do so as a record number reported that openings are hard to fill.

Not only did plans for employment fall but so too did capital expenditure plans as well as actual capital expenditures. Inventory levels are also abating to a degree as fewer—but still a historically high share—report current inventory levels are too low. There was also a 2 point pullback to 9 in the net percent of businesses looking to increase inventory plans. Click here to view Bespoke’s premium membership options.