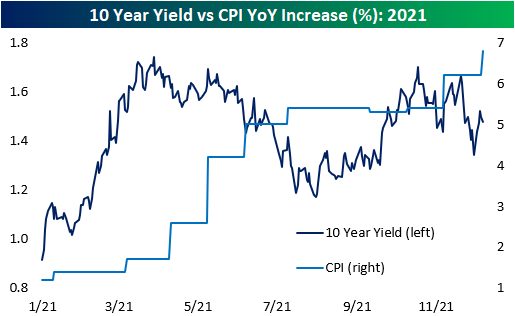

CPI vs 10 Year Yield and S&P 500

With inflation levels surging this year, you would expect to see long-term interest rates right along with CPI. As illustrated in the chart below, though, that has been far from the case. Ever since y/y CPI first crossed 2% back in Q1, the yield on the 10-year has actually declined even as CPI has surged to 6.8%! Fed purchases of treasuries have helped to keep rates low, but if the market was truly worried about inflation pressures becoming a longer-term issue, you would expect to see at least some upward pressure in rates.

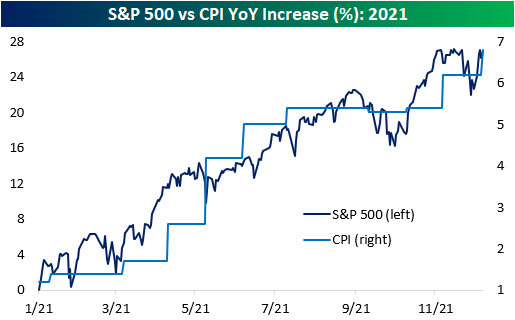

While yields have seen little upside pressure from the surge in inflation, stock prices have piggy-backed the move higher the entire time. Investors continue to pile into stocks as low yields seemingly offer no other alternative and negative real yields in the treasury market make equities look more attractive on a relative basis. . Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 12/10/21 – The Report You’ve All Been Waiting For

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Inflation is just like alcoholism. The good effects come first.” – Milton Friedman

Following yesterday’s move of just six cents (not basis points but cents) in the Dow, European markets are similarly quiet this morning with the FTSE-100, the CAC-40, and DAX, all trading within 0.1% of their respective closes on Thursday. However, just as the Dow’s move wasn’t entirely representative of the action in US stocks yesterday, the fact that indices are little changed on the day doesn’t reflect that all of those major European indices are well off their lows of the day.

There may not be a lot of direction in equity markets so far this morning, but there’s a good chance that the release of November CPI could act as a catalyst for more of a move throughout the day, although there wasn’t a lot of optimism heading into the report that the reading would come in light,

Once CPI is out of the way, investors can shift their focus to next week’s FOMC announcement on Wednesday. Given Powell’s hawkish pivot right after Thanksgiving, it’s hard to imagine what the Fed could say next week that would really be a surprise to investors at this point.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

With all the volatility we have seen in the S&P 500 over the last month, the largest stock in the S&P 500 has been remarkably calm. The S&P 500’s performance over the last month has been a marginal gain of less than half of a percent, but shares of Apple (AAPL) have rallied over 18%. With a performance spread of more than 17 percentage points, the gap between AAPL and the S&P 500 over the last month has been the widest since August 2020, and before that, you would have to go all the way back to August 2013 to find another time that the spread was wider. There have been plenty of times in the past where AAPL has followed a different path than the broader market, but you don’t often see the gap get wider than it is now.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s 10 Favorite Market Indicators

Bespoke’s Weekly Sector Snapshot — 12/9/21

Chart of the Day: VIX Do-Si-Do

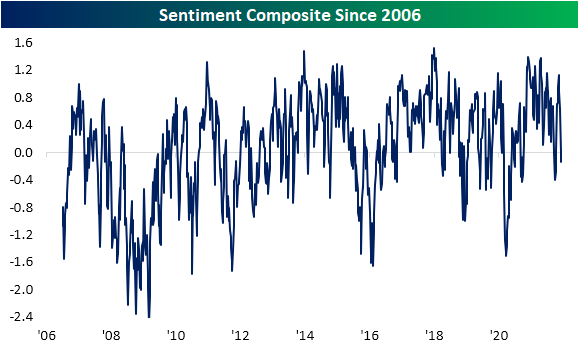

Not Pessimistic But Not Optimistic Either

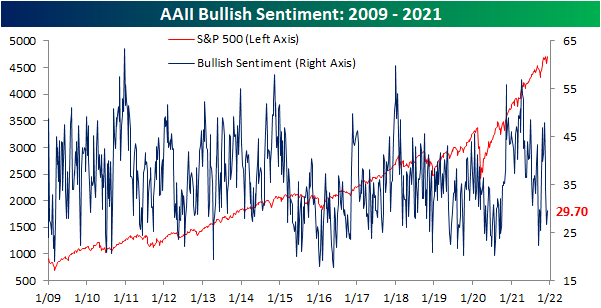

The S&P 500 has made a quick recovery in the past week closing within a few basis points of a new 52-week high yesterday. In spite of that improvement to price, sentiment has yet to fully buy-in. The American Association of Individual Investors weekly sentiment survey only saw a modest improvement to the percentage of respondents reporting as bullish. Just under 30% of respondents reported bullish sentiment versus a level of 26.7% last week. That snapped a streak of back-to-back-to-back declines but still leaves bullish sentiment 4.1 points below where it was only two weeks ago.

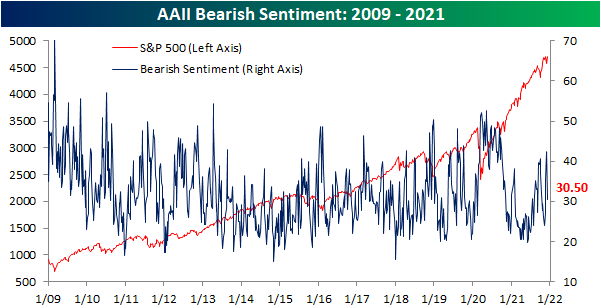

While the change in bullish sentiment was nothing to write home about, bearish sentiment plummeted 11.9 percentage points to 30.5%. That was the largest single-week decline since 10/17/19 when bearish sentiment collapsed an even larger 12.91 percentage points. Back then, that brought bearish sentiment to a similar level of 31.05%.

In spite of bearish sentiment’s big reversal lower, the bull-bear spread remains negative, albeit not by much.

Considering bullish sentiment did not meet the big drop in bearish sentiment, neutral sentiment made up the difference rising 8.8 percentage points to 39.8%. That is the highest level of neutral sentiment since the first week of 2020 when it eclipsed 40%.

While the AAII numbers showed a big reversal in bearish sentiment, other sentiment indicators took more pessimistic tones this week. The NAAIM Exposure Index collapsed further to the lowest level since mid-October while the Investors Intelligence survey saw the biggest one-week drop in bullish sentiment since October 2019 to the weakest reading since early April 2020. Bearish sentiment, meanwhile, saw the largest one-week uptick since June 2012. As a result of the combined moves across these indicators, our sentiment composite has continued to plummet and is now in negative territory and at the weakest level since late September/early October. Click here to view Bespoke’s premium membership options.

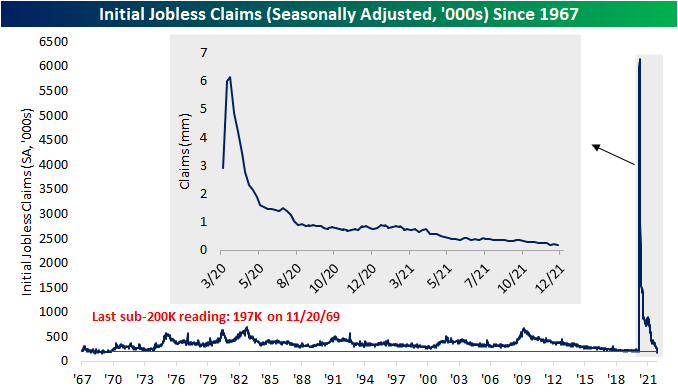

Claims Get Their Seasonal Bump

Seasonally adjusted initial jobless claims saw a substantial 43K decline this week down to not a 52-week but a 52-year low of 184K! While that marked a new low, last week’s print was revised higher by 5K to 227K.

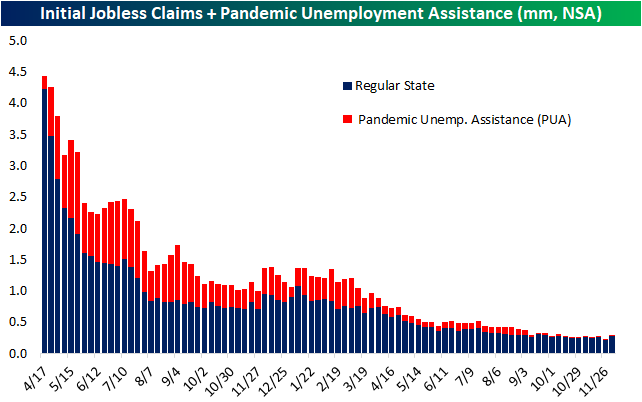

On a non-seasonally adjusted basis, claims were less impressive this week with a 63.7K increase to 280.7K. That jump erased any of the improvements to claims since the end of September.

Although unadjusted claims have now erased the past couple of months of improvements, that is less alarming in the context of seasonality. The current period of the year typically sees claims gradually rise into year-end. Up until this week, that seasonal trend has not exactly been consistent this year, though, as claims have generally trended sideways throughout the fall. Turning back to this week, the current week of the year (49th) has historically seen claims rise week over week 81.5% of the time since 1967 and the average increase to claims is the second largest of any week of the year as well. In other words, if there was a week for claims to play catch up to seasonal norms, it would have been this week. Furthermore, despite this week’s increase in NSA claims of just 64K, it was still below average.

Pivoting over to continuing claims, there was a tick higher to 1.992 million this week from the low of 1.954 million last week. Albeit higher, claims remain healthy below 2 million.

Unadjusted claims can include all other programs which are delayed an extra week making the most reading through the week of November 19th. That week saw total claims fall below 2 million for the first time since the pandemic with broad declines across programs. Regular state claims—which are currently the vast majority of claims since the expiration of pandemic era programs—were the biggest contributor to that decline. Pandemic programs still have a presence but that is dwindling with claim counts for PUA, PEUC, and Extended Benefit claims in the low 100K range. Click here to view Bespoke’s premium membership options.

The Bespoke 50 Growth Stocks – 12/9/21

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

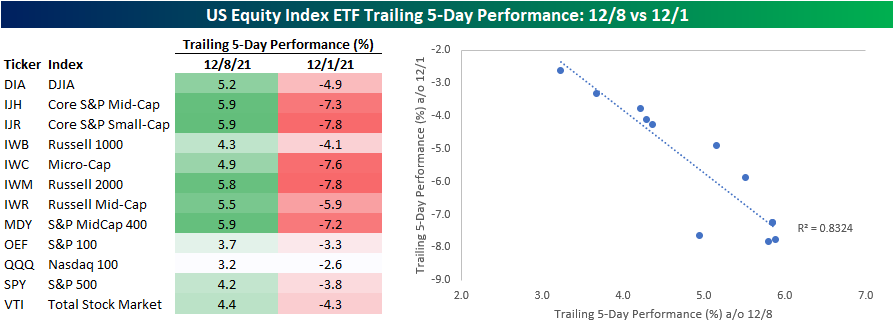

Reversals

Earlier today in our Morning Lineup, we highlighted the fact that there has been a pretty remarkable about-face in market performance at the index level between now and a week ago. The table below compares the trailing 5-day performance of the major index ETFs as of the close on 12/8 versus the trailing 5-day performance as of the close on 12/1. Whether you look at the table or chart, it’s pretty clear to see that performance over the last five days has been directly related to performance in the week prior. Indices that were down the most last week have bounced back the most this week, and indices down the least last week are up the least this week. With an r-squared of 0.8324, you can’t get much more closely correlated than that.

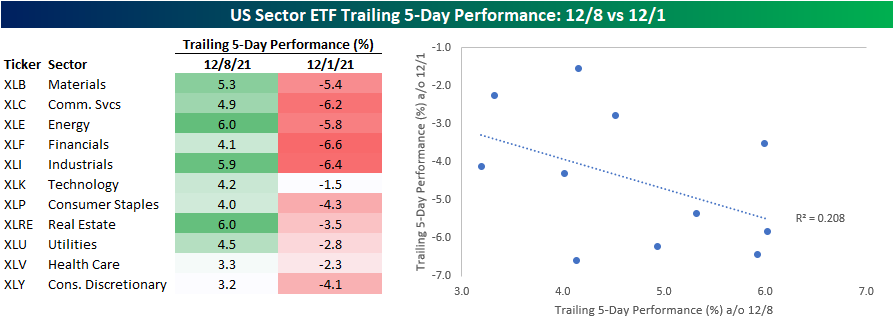

While there has been a close correlation between performance at the index level, at the sector level, the relationship — while still positive — hasn’t been nearly as strong. While some of the biggest losers in the week ending 12/1 like Industrials and Energy have been among the biggest winners over the last week, a sector like Real Estate that actually outperformed the S&P 500 in the week ending 12/1 is also one of the top-performing sectors over the last week. Additionally, Financials was the worst-performing sector on the way down last week with a decline of 6.6%, but it has also underperformed on the way up this week. As a result, while the r-squared of performance at the index level has been +0.83, the r-squared of performance at the sector level has been much lower at just +0.21. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 12/9/21 – Then Again

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Indecision may or may not be my problem.” – Jimmy Buffett

After a strong start to the week, investors are taking a step back from buying this morning as futures are firmly negative and have been gradually weakening all morning. Following big losses right after Thanksgiving and then a sharp rebound over the last week, investors can’t seem to make up their minds.

The biggest news item of the day so far has been initial jobless claims which fell to an unheard of 184K which was well below the already low estimate of about 225K. As equities pull back, treasuries have been rallying with the 10-year yield back below 1.5%. The big economic data in the US will come tomorrow with the release of November CPI, but overnight in China, CPI came in weaker than expected on a y/y basis (2.3% vs 2.5% forecast).

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

What a difference a week makes. Looking at how sector performance has changed over the last week provides a perfect illustration of indecisiveness in the equity market. The first snapshot below is from our Trend Analyzer from a week ago today (through the close on 12/1). At the time, every major index ETF was down at least 2.5% over the prior five trading days with the majority below their 50-day moving averages after trading at or near overbought levels just a week earlier. Mega-cap indices like the Nasdaq 100 (QQQ) and S&P 100 (OEF) were holding up best at the time while small and mid-cap stock indices were down over 7% in the span of just five trading days.

Fast-forwarding just a week, the picture has completely changed. Now, every major index ETF in the Trend Analyzer is up at least 3% over the last five trading days, and the majority are back above their 50-day moving averages. Leading the way higher, the same indices that were down the most have bounced back the greatest while mega-cap indices like the Nasdaq 100 (QQQ) and S&P 100 (OEF) are the only two that are up less than 4% over the last five trading days.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.