Bespoke’s Morning Lineup – 1/7/22 – Jobs Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Find a job you enjoy doing, and you will never have to work a day in your life.” – Mark Twain

There’s a modestly positive bias to futures this morning, but the release of the December jobs report could shake things up considerably. Like last month’s report, the data was mixed. Non-Farm Payrolls came in considerably below forecasts at 199K versus expectations for a reading closer to 500K. At the same time, the Unemployment Rate actually dropped below 4% for the first time in the post-COVID era. Average Hourly Earnings grew 0.6% m/m which was better than expectations for growth of 0.4% while average weekly hours were slightly lower than estimated. Despite the stronger than expected wage growth, on a y/y basis, earnings rose 4.7%, but that’s still more than two full percentage points below the y/y rate of CPI.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

The trading year is only four trading days old, but already we have seen lots of moves, and they’ve primarily been to the downside. Heading into the weekend, we wanted to provide a quick look at where each of the new major indices stand on a longer-term basis.

Starting with small caps, the Russell 2000 (IWM) broke out to new highs in November, but quickly reversed and has since broken below both its 50 and 200-day moving averages (DMA). Since then, the Russell has made several attempts to trade back above those averages, and while it has traded above the 200-DMA multiple times, the 50-DMA has been a more formidable barrier that has yet to break.

The Nasdaq 100 (QQQ) has been the weakest of the three major indices this year with a decline of over 3%, but at this point, it has been able to hold support at the prior highs from September. This more recent decline is the third time QQQ has tested support since the start of December, and while it has held so far, the more often an index tests support or resistance, the weaker it often becomes.

Lastly, the picture for the S&P 500 (SPY) probably looks the best of the three. Not only have the uptrend since the September lows and the 50-DMA held to this point, but the prior highs from mid-November and mid-December have also acted as support. As long as these levels hold, it should provide some comfort to chart watchers.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Consumer Pulse Report – January 2022

Bespoke’s Weekly Sector Snapshot — 1/6/22

Sentiment Surveys Miss Meeting Minutes

The news of the FOMC’s hawkish meeting minutes and the subsequent declines in markets in reaction to the release likely was not fully captured in sentiment indicators this week due to the timing of collection periods. Nonetheless, respondents to the AAII survey did show a drop in optimism with only 32.8% of respondents reporting as bullish versus 37.7% last week. While back below the historical average, bullish sentiment is not extremely extended below or outside of the recent range of readings.

Bearish sentiment picked up the larger portion of those losses rising from 30.5% last week to 33.3% which is only a few percentage points above the historical average (30.6%).

As a result of these moves, the bull-bear spread dipped back into negative territory, albeit not by much, after last week saw the first positive reading in five weeks.

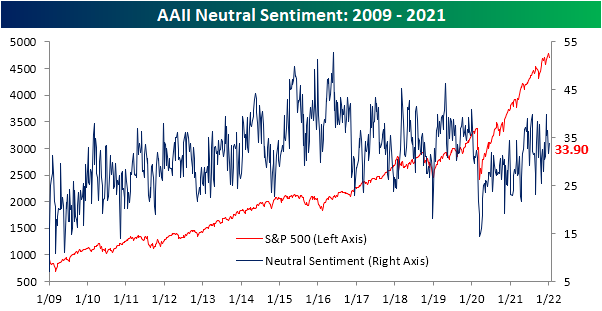

Neutral sentiment picked up the difference rising 2.1 percentage points to 33.9%. As with bearish sentiment, even with that increase, the reading remains below levels from just two weeks ago.

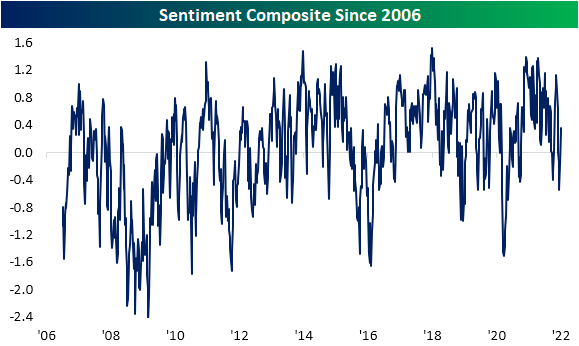

Out of three sentiment surveys—AAII, Investors Intelligence, and the NAAIM Exposure Index—the AAII reading is released the latest of the three, and as such was most likely to pick up any reaction to Wednesday’s declines. As such, both the Investors Intelligence and NAAIM Index saw more bullish readings this week. In fact, the Investors Intelligence survey—which had its first release since before the holidays—saw the largest increase in bullish sentiment since June 2016. That meant for our sentiment composite (which is an average of how many standard deviations from the historical norm the NAAIM index and bull-bear spread for the AAII and Investors Intelligence surveys are), this week saw a continued recovery in bullish sentiment. Click here to view Bespoke’s premium membership options.

Chart of the Day: Buybacks No Longer Buoyant

Year End Claims Uptick

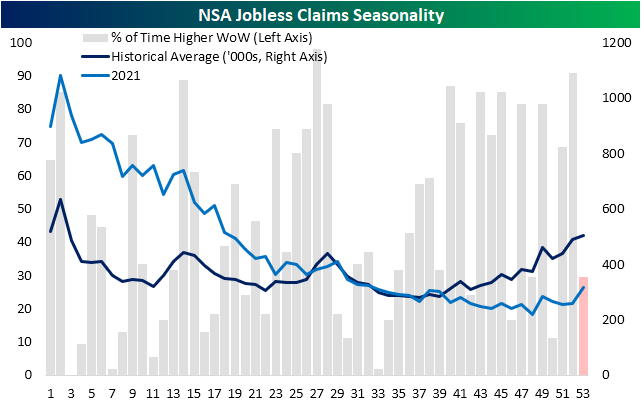

Initial jobless claims data through the final week of 2021 was released this morning remaining above 200K versus expectations of a drop down to 195K. At 207K, seasonally adjusted claims were at their highest level since the last week of November when they were 20K higher. Although claims have not been improving in recent weeks, the current levels are in line with the low end of the range from prior to the pandemic which is also around the strongest levels in several decades.

Looking back on 2021, it was an interesting year for the dataset. The first half of the year saw a steady and rapid decline in claims as they were continuing to come off of historic levels set earlier in the pandemic. By mid-year and continuing into the final quarter, they had essentially returned to levels consistent with the historical average. Then, whereas the final few months of the year have historically marked a time that claims rise into year-end, claims generally fell throughout the fall and only noticeably began to experience that seasonal uptick in November and December. That resulted in claims to finish the year well below the historical average for the current week of the year.

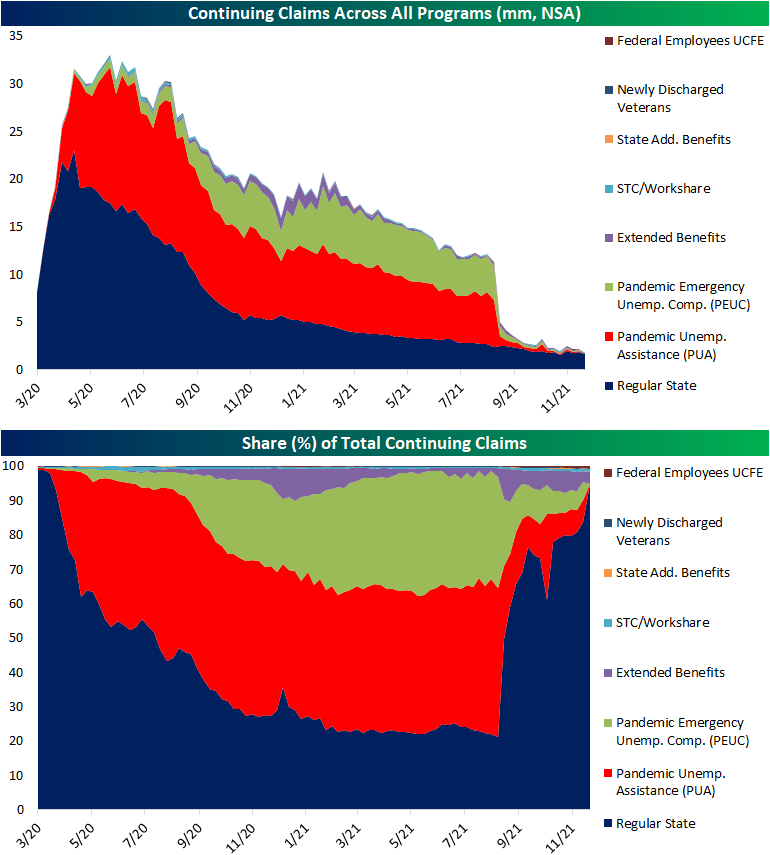

Turning to continuing claims, which are delayed an additional week to the initial claims data, the week of December 24th saw a 36K increase to 1.754 million. While higher, the current level remains over 100K below the one from only two weeks ago.

Pandemic era programs faced official expiration in September, but there were some residual claims reported in the following months. With that said, those levels declined, and by the final week reported (December 10th) total claims across PUA and PEUC programs only accounted for a combined 255.1K. With the new year, the Department of Labor is no longer reporting total national counts for these programs. With those changes over the past several months, that means the composition for continuing claims is comprised massively by regular state programs once again and the other major contributor, though to a much less impactful degree, is extended benefits programs. Total claims across all reported programs are now a fraction of their pandemic highs at only 1.73 million. Click here to view Bespoke’s premium membership options.

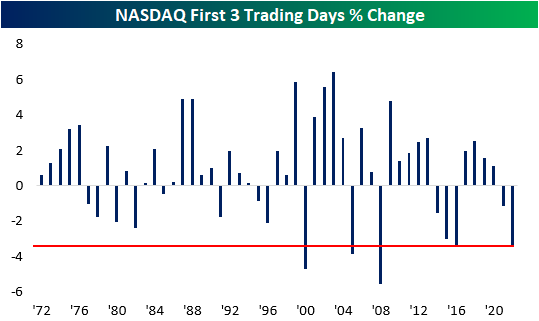

Nasdaq Down 3%+ In First Three Trading Days

Historically, the first three trading days of the year have been positive for the NASDAQ with gains more than two-thirds of the time (68.6%). This year has been a different story, though, as the Nasdaq fell 3.4% in the first three days; the fifth-worst 3-day start to a year in the NASDAQ’s history. The only years with a weaker 3-day start were 2000, 2005, 2008, and 2016.

The table below lists the five prior years where the NASDAQ started the year with a decline of 3% or more in the first three trading days. For each year, we also show the index’s performance for the remainder of January as well as the remainder of the year. In the case of these five years, first impressions have been a pretty good indicator of future performance as the NASDAQ’s performance for the remainder of January and the rest of the year was weaker than average. While the range of returns is extremely wide, the average return for the rest of January was a decline of 1.6% (median -1.4%), and the rest of the year averaged a decline of 9.5% (median +5.5%). We’d also note that the two worst three-day starts to a year for the NASDAQ (2000 and 2008) also experienced the two worst rest of year returns for the Nasdaq in its history.

Although the fact that two of the worst years in the NASDAQ’s history were also years where the index dropped more than 3% in the first three trading days of the year, by itself, investors should not take this year’s occurrence as an overly bearish sign. Throughout the index’s history, there has been very little correlation between how it traded in the first three trading days and its rest of year return, and the r-squared between the two is just 0.0132.

While any association with 2000 and 2008 is always scary, in every other year that the NASDAQ traded lower in the first three trading days of the year, its rest of year performance was positive every time. In fact, during the 15 years when the first three days were negative, the average rest of year performance was a gain of 15.7% (median: 15.13%) with positive returns 87% of the time. Meanwhile, in the 35 years where it traded higher in the first three trading days of the year, the average rest of year return was a gain of 10.92% (median: 13.22%) with positive returns 69% of the time. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 1/6/22 – Mixed Ahead of Data

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Just because the tide is out, doesn’t mean there is less water in the ocean.” – Seth Godin

Markets are attempting to regroup from the fourth worst market reaction to a release of the FOMC Minutes since at least 2007. In what has become a trend of the new year, S&P 500 and Dow futures are both modestly higher while the Nasdaq is lower. Crude oil is pushing $80 and the yield on the 10-year is pushing 1.8%.

In economic data, jobless claims were just released, and while initial claims came in just slightly ahead of forecasts, continuing claims topped 1.7 million which was nearly 100K above forecasts.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Look at the chart below. It may look like an EKG of someone watching the market yesterday with the increased amplitude coinciding with the release of the Fed minutes, but it’s actually the rolling three-day performance spread between the Technology and Financials sector since the start of 2018. With Technology down 3.3% YTD and Financials up 2.6%, the performance spread between Technology and Financials currently stands at -5.9 percentage points which is the widest gap between the two sectors since almost exactly a year ago today on 1/6/21 which also happened to be three trading days into the new year. Guess which year the headline, “Pandemic Tech Bubbles Echo Those of Dotcom Era,” was from? It was last year. Even the headlines now are similar to that point a year ago.

Technology had a rough start to 2021, but by the end of the first quarter, it started to rebound and perform in line with to better than the S&P 500. That doesn’t mean history will repeat itself, but in the last several years, there have been more than a few premature obituaries that were written for the Technology sector.

Maybe more concerning than tech’s underperformance over the last few days has been the fact that two years after the pandemic, not only are we still dealing with it, but market volatility within sectors remains much more elevated than it was pre-pandemic. What we can take some solace in is the fact that even as the bubbliest areas of the market have cratered, the last couple of days notwithstanding, the rest of the market has held up relatively well.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.