Chart of the Day: Don’t Chase A Sugar High After FOMC

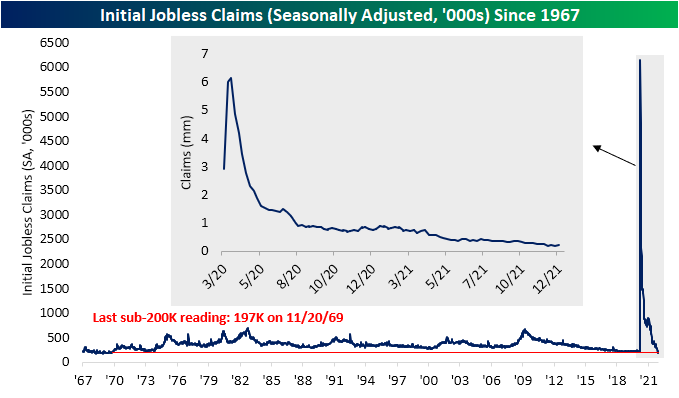

Claims Back Above 200K

After hitting a multi-decade low last week, seasonally adjusted initial jobless claims rose back above 200K. While a minor deterioration, the current level of claims remains one of the strongest readings on record.

While claims are at a healthy level, the seasonal adjustment has had a flattering effect recently. Unlike the SA number, on a nonseasonally adjusted basis, no recent week has seen a sub-200K reading with the current week falling to 267.5K from 283.9K the prior week. From a seasonal perspective, claims falling week over week is very much normal for the given week of the year (50th) with nearly 90% of years since 1967 experiencing such a decline. Only five other weeks of the year have seen claims fall WoW more consistently.

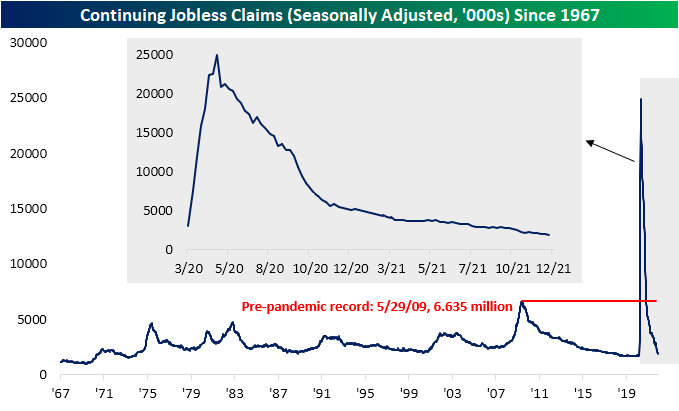

Delayed one week to initial jobless claims, continuing claims hit a new low for the pandemic of 1.845 million in the first week of December. The marks the strongest reading since the week of March 13, 2020.

Including all other programs creates an additional week of lag making the most recent data through the final week of November. Total continuing claims as of that week ticked higher to 2.46 million versus 1.95 million the previous week. That is the highest reading since the end of October. Even though pandemic era programs have now technically expired, the pickup in claims was broad across programs but regular state claims were the main driver of the overall increase. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 12/16/21 – Fourth Time the Charm?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“No one goes there nowadays, it’s too crowded.” – Yogi Berra

Sentiment towards the market may be negative these days, but that hasn’t stopped the S&P 500 from quietly hanging around right at record highs. As Yogi Berra would say, “Everyone is selling stocks because they’re going up so much.”

Futures are staging a relatively impressive follow-through this morning in the wake of yesterday’s FOMC meeting where Powell and company didn’t give the market any surprises. To maintain those gains, though, we have a lot of economic data to get through. Already released were Jobless Claims (slightly higher than expected), Housing Starts (better than expected), Building Permits (better than expected), and the Philly Fed (weaker than expected). On deck we still have to wait for Industrial Production, Capacity Utilization, flash PMI readings for the month of December, and then the KC Fed Manufacturing report at 11 AM will close out the slate of data for the week. That’s a lot to digest!

We haven’t talked a lot about earnings recently, but there are a number of notable names reporting today including Accenture (ACN), Adobe (ADBE), Jabil (JBL), and FedEx (FDX). Of those four, ACN is trading up 10%, JBL is up 5%, and ADBE is trading down 7%. FDX isn’t scheduled to report until after the close.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Earlier in the week, we referred to it as the market treading water, and that remained the case heading into yesterday’s close as the S&P 500 closed right at its recent resistance level once again. As shown in the chart of SPY below, the ETF has managed to trade above $470 multiple times in the last six weeks as it first broached that level on an intraday basis on November 5th. Since then, there have been multiple attempts to break through that level, but all of them have failed. Could today be the day? In pre-market trading, SPY is trading just above $473 which would be close to a record intraday high. If these levels hold throughout the trading day and SPY can stay above $470, it could just be the welcome Santa was waiting for.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 12/15/21

Bespoke Baskets Update – December 2021

B.I.G. Tips – Retail Sales Whiff

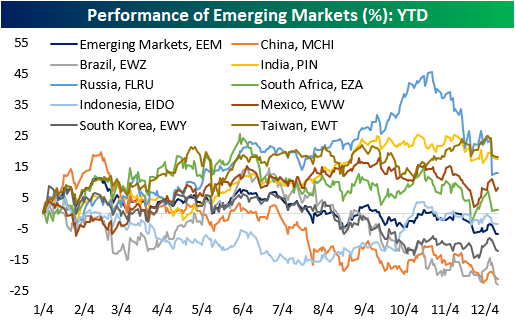

Pockets of Strength in Emerging Markets

So far this year, the US has outperformed every other country on the planet. Broadly speaking, developed economies have outperformed emerging economies. The iShares MSCI Emerging Markets ETF (EEM) has declined 6.8% in 2021, but this does not necessarily mean that performance across every emerging economy has been negative. Although China, Brazil, and South Korea have been particularly weak (three of the top six countries of exposure for EEM), countries like Taiwan, India, Russia, Mexico, and South Africa have experienced positive returns this year.

Just like individual sectors in the US cannot be expected to perform equally, emerging economies don’t always perform in unison with each other. Differences include natural resources, political & legal structure, trading partners, and much more. Although EEM has declined on a YTD basis, the average performance of the nine countries that we tracked was a modest loss of 0.1%, and the spread between the best performer (Taiwan) and the worst (Brazil) is currently 41.3 percentage points. Moving forward, investors may want to consider selecting individual countries to gain emerging market exposure, as the broader ETFs tend to have a large concentration in just a few countries. Emerging markets are inherently higher-risk investments in comparison to developed nations due to uncertainty in future prospects, but in the long run, there are excellent opportunities within pockets of emerging markets, although not all countries will see the same performance. Click here to view Bespoke’s premium membership options.

Chart of the Day: Fed Days

Bespoke’s Morning Lineup – 12/15/21 – Big Data Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

If you insist on certainty, you will paralyze yourself.“ – J. Paul Getty

Ahead of today’s FOMC meeting, we just got some important economic data in the form of Empire Manufacturing, Retail Sales, and Import Prices. Overall, the results weren’t very good. While Empire Manufacturing came in better than expected, retail sales were much weaker than expected at both the headline level and ex-autos and gas. Headline retail sales came in at just 0.3% versus expectations for a gain of 0.8%. When you factor in inflation, though, sales were negative. Lastly, import prices rose more than expected coming in at 0.7% versus forecasts for an increase of 0.6%. On a y/y basis, import prices were up 11.7%.

Futures were flat heading into the report, and have actually picked up a little steam with Nasdaq leading the way. In addition to these reports, Business Inventories and homebuilder sentiment from the NAHB will be released at 10 AM.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

While the stock is already down 4% from its intraday high on Monday, shares of Apple (AAPL) still remain about 25% above their 200-day moving average (DMA). That’s off the recent high of 28% back on Friday, but it’s still elevated relative to history. Going back to 2011, there are only two periods where the stock’s spread relative to its 200-DMA reached significantly higher levels than 25% while there are another three (2014, 2017, and 2018) where the spread reached similar levels before pulling back.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.