Bespoke’s Morning Lineup – 3/21/22 – Every Dog Has Its Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Let Hercules himself do what he may / The cat will mew and dog will have his day.” – William Shakespeare

After a big rally last week, equity markets are heading into the week a bit groggy this morning as futures are indicated lower to kick off the week. As we note in the commentary of this morning’s report, though, it’s not unprecedented to see weakness following a strong rally into a triple witching options expiration.

Oil prices are near $110 per barrel this morning as Russia-Ukraine tensions show no signs of abating. In fed-speak, there’s a number of speakers on the calendar and the week kicked off with Atlanta Fed President Bostic who said he sees a total of six rate hikes for 2022 and another two in 2023.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

In what was a strong week for the equity market, it was clearly an example of every dog having its day as the worst-performing sector’s YTD led the rally while Energy, the one sector that was up YTD heading into the week, finished in the red. Whether you want to call it a dash for trash or some other variation, sectors that had faced the most serious selling pressure had their shining moment of 2022.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 3/20/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

From The Front Lines

Ukrainian Counteroffensive Near Mykolaiv Relieves Strategic Port City by Yaroslav Trofimov (WSJ)

Russian forces have been pushed back from Mykolaiv in the biggest Ukrainian counter-attack since the start of the war. How the people are digging out as the steady steam of war dead continue to flow back from the front. [Link; paywall]

Ukraine

Economic complexity emerges as a new restraint on wars of conquest by George Pearkes (Atlantic Council)

Sanctions levied against Russia in response to the war in Ukraine illustrate the new, existential restraint on wars of conquest: the threat of broken value chains which underpin the staggeringly complex web of production that supports modern standards of living. [Link]

Aircraft Insurers Brace for Deluge of Russia Claims, With Lloyds on Hot Seat by Katherine Chiglinsky, Siddharth Vikram Philip, and Max Reyes (Bloomberg)

Companies that own commercial aircraft and lease them to airlines are facing massive losses from the requisition of those planes by the Russian government. The question is, how much of that hit will be absorbed by insurance companies? [Link; soft paywall]

Commodities

The $140 Billion Question: Can Russia Sell Its Huge Gold Pile? by Eddie Spence (Yahoo!/Bloomberg)

Gold holdings were meant to “sanctions-proof” the Russian central bank’s massive reserve hoard. In practice, it’s proving hard to deploy that hoard of value to protect the Russian economy from western sanctions, bringing in to question the utility of holding gold as reserves. [Link]

Energy traders call for ‘emergency’ central bank intervention by Claire Jones, Neil Hume, and Martin Arnold (FT)

European commodities trading firms have requested central bank liquidity facilities to help them manage unprecedented disruptions from Russian sanctions and the war in Ukraine. [Link; soft paywall]

Food Prices

How is the Egyptian government dealing with the global wheat crisis? by Nada Arafat (Mada Masr)

A detailed review of policy steps being taken by the world’s largest wheat importer (heavily dependent on Ukrainian and Russian supply specifically) to secure sufficient grain volumes amidst the loss of supply from the breadbasket of Europe. [Link]

We’re Not Facing a Global Food Crisis by Aaron Smith (UC Davis)

While the loss of wheat and to a lesser degree corn supplies from Russia and Ukraine will be significant, the overall shock is largely priced in at this point and unlikely to cause a significant global shortage. [Link]

High & Low Drama

Inside the Succession Drama at Scholastic, Where Harry Potter and Clifford Hang in the Balance by Joy Press (Vanity Fair)

A real-life version of Succession is pitting the girlfriend of the former CEO for children’s book company Scholastic against his sons. [Link; soft paywall]

California city may declare Chick-fil-A a “public nuisance” by Kate Gibson (CBS News)

Huge lines for the fried chicken purveyor in Santa Barbara are spilling into streets and blocking lanes for hours at a time, leading civic leaders to slap the business with penalties. [Link]

Tech

How the Pandemic Broke Silicon Valley’s Stranglehold on Tech Jobs by Christopher Mims (WSJ)

Remote work is becoming more prevalent, and it’s most concentrated in tech where powerful geographic network effects have historically concentrated talent in a narrow cluster of cities around the country. [Link]

Vimeo is telling creators to suddenly pay thousands of dollars — or leave the platform by Mia Sato (The Verge)

Price hikes have been rolled out on video sharing website Vimeo’s users, many of whom use the site because of its integration with popular subscription platform Patreon. [Link]

Whoops

UPS missed Nantucket ferry reservation window: ‘It’s going to put us in a world of hurt’ by Joshua Rhett Miller (NYP)

An early priority window for booking Nantucket busy season ferry capacity was missed by UPS, leaving the shipping company scrambling to figure out how it will book capacity and businesses on the island wondering how they will ship and receive packages this summer. [Link; auto-playing video]

Everyone Was Surprised By The Senate Passing Permanent Daylight Saving Time. Especially The Senators. by Paul McLeod (BuzzFeed)

Apparently the Senate was too busy deliberating this week to notice that they had accidentally passed legislation that (if passed by the House and signed by the President) would eliminate the bi-annual changing of the clocks. [Link]

Stress

Cold Showers, Hot Saunas and the New Way to Tame Stress by Betsy Morris (WSJ)

Occasional bursts of stress may help the body adapt to more permanent stress, with exercise, temperature changes, and fasting all playing a role. [Link; paywall]

Veto Points

Why America can’t build quickly anymore by Alan Cole (Full Stack Economics)

A proliferation of ways for individuals and groups opposed to development have created huge logjams for major projects, with environmental reviews raising project risks and pushing timelines for construction of everything from transit to wind energy into the years. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report Newsletter — 3/18/22

Daily Sector Snapshot — 3/18/22

Bespoke’s Morning Lineup – 3/18/22 – Finishing Up on a Down Note

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Economics is a very difficult subject. I’ve compared it to trying to learn how to repair a car when the engine is running.” – Ben Bernanke

Early weakness in the futures yesterday gave way to the luck of the Irish as the major averages all closed sharply higher bringing the string of 1%+ gains for the S&P 500 up to three. Futures are a bit weaker this morning than they were at this time yesterday, so it may prove more difficult to turn the tide again today. This morning’s call between Biden and Xi at 9 AM could be an important catalyst regarding how the war in Ukraine plays out. China has been more favorable to the Russian side and has ramped up criticism of the US in recent days, with some officials in Washington worried that the country will start providing direct assistance to Russia.

The economic calendar is relatively quiet today with Existing Home Sales and Leading Indicators (both at 10 AM) the only reports on the calendar. St. Louis President James Bullard has already been out this morning saying he advocates a 3% Fed Funds rate by year-end and a more rapid reduction in the balance sheet.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Movements in the crude oil market have been pretty nuts both recently and over the last two years. For starters, think about this. Over the last two years, crude oil has traded at both its lowest level EVER and within 12% of its highest price ever. 88% of its entire historical range in less than two years!

Over a shorter time window, prices have also been volatile. For just the sixth different period since the early 1980s, WTI crude oil has seen its average daily move exceed 4% over the last 50 trading days. As shown in the chart below, the last 50 trading days join 1986, 1990, 2008, 2016, and 2020 as one of the most volatile two-month periods for the commodity on record.

Not only has crude oil traded erratically, but the equity market’s reaction to moves in the crude oil market have also been hard to decipher. Take the equity market’s reaction to the daily moves on March 1st and yesterday. On both days, WTI rallied more than 8% and broke above $100 in the process. Yet on 3/1, the S&P 500 fell 1.55% in reaction to the move, while yesterday it rallied 1.23%. It just goes to show you that even if you could predict the future, knowing the market’s reaction would be far from a layup.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

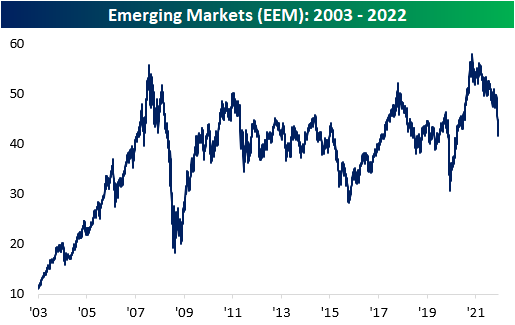

Craziness In Emerging Markets

Volatility in Chinese markets has caused the broader emerging markets ETF, EEM, to move aggressively to both the upside and downside over the last few trading days. Yesterday, EEM gained 8.05%, but the move came after the ETF moved 6.1% lower between last Thursday and Tuesday’s close. All-in-all, the ETF round-tripped to the levels seen on Wednesday of last week, but EEM is still down 8.5% year to date. Since EEM began trading in 2003, the ETF has gained a little over 300%, which constitutes annualized performance of 7.7%.

The move yesterday was high relative to historical daily moves, ranking as the 13th largest single-day upside move in its history. Larger moves were seen during the Financial Crisis and the COVID Crash. Obviously, these are not great periods to be compared to, but the occurrences were near the bottom of the pullbacks.

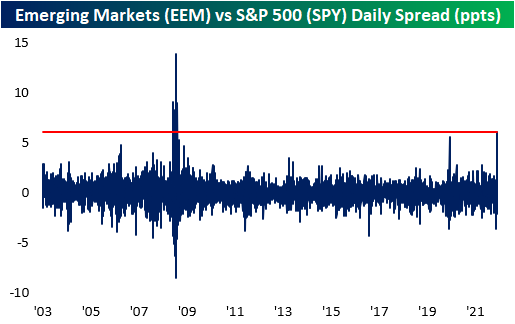

EEM’s daily spread versus the S&P 500 yesterday reached its highest positive level since the Financial Crisis. The last time the daily spread was above that of yesterday was on 11/21/08, in which the daily spread was +9.0%. The last time the spread even came close to this figure was during the COVID crash. Yesterday’s reading was 6.1%.

Bespoke’s Weekly Sector Snapshot — 3/17/22

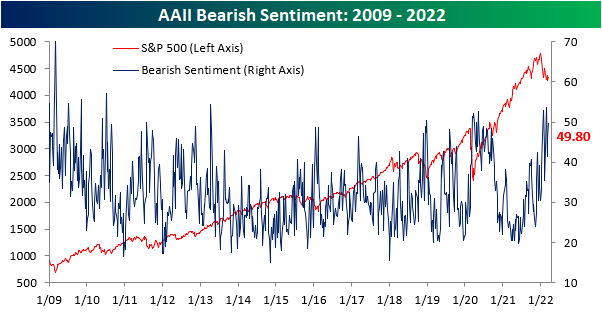

Bears Come Out of Hibernation in Spite of Rebound

In spite of the S&P 500 gaining back some ground in the past week, sentiment has continued to shift in an increasingly pessimistic direction. For a second week in a row, less than a quarter of respondents to the AAII sentiment survey reported a bullish. At 22.5%, however, current levels are still slightly above the low of 19.2% from one month ago.

Bearish sentiment meanwhile climbed another 4 percentage points with just under half of respondents reporting as such. Albeit elevated, bearish sentiment is not as high as the 50%+ readings reached in January and February. As for another reading on bearish sentiment from the Investors Intelligence survey, bearish sentiment is at the highest level since the March 2020 COVID low.

The bull-bear spread is extremely low at -27.3 but that is not quite as low as those past couple of weeks when over half of respondents reported as being bearish.

Not all of the increase to bears came from bulls. As shown below, neutral sentiment fell from 30.2% down to 27.8%. That is only the lowest level since the end of February. While bullish and bearish sentiment are both over a full standard deviation away from their historical averages, neutral sentiment is much more inline with its own historical average. Whereas all weeks since the start of the survey has seen neutral sentiment average a reading of 31.4%, this week’s reading was only a few percentage points away. Click here to view Bespoke’s premium membership options.

The Bespoke 50 Growth Stocks – 3/17/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Housing Starts and Building Permits Raise the Roof

The latest data on residential housing for the month of February generally came in better than expected today and showed some positive longer-term trends. Starting with the actual numbers, Housing Starts increased 6.8% m/m, and while growth in multi-family units was higher than the headline number, single-family units still showed healthy growth of 5.7%. Building Permits actually showed a modest decline in February, falling 1.9%, but single-family units barely even declined. On a regional basis, despite weaker sentiment from homebuilders in the Northeast in yesterday’s report from the NAHB, both Housing Starts and Building Permits in the Northeast grew more than 20% m/m which was easily the strongest showing of any region.

From a longer-term perspective, the 12-month average of Housing Starts made another post-financial crisis high in February rising to its highest level since March 2007. Typically, this reading starts to roll over well in advance of a recession, so the fact that it’s hitting multi-year highs now should provide some relief to those who are concerned about the flattening of the yield curve.

It isn’t just Housing Starts that are making new highs on a 12-month average basis. The 12-month average of Building Permits also ticked up to the highest level since February 2007.

Finally, the chart below shows the 12-month average of single-family Building Permits and Housing Starts. For much of the last year, the average of single-family units was starting to show signs of rolling over as supply chain issues slowed down activity in the sector. Given housing’s leading nature relative to the business cycle, this was somewhat concerning, even if the issue was more supply rather than demand-driven. February’s report, though, was encouraging in that both Permits and Starts showed increases again in their 12-month averages. Click here to view Bespoke’s premium membership options.