B.I.G. Tips – Energy Attempts to Catch its Breath After a Record Decline

Bespoke’s Morning Lineup – 7/8/22 – Jobs Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Our predecessors overcame many troubles and much suffering, but each time got back up stronger than before.” – Shinzo Abe

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

US futures have been negative most of the morning ahead of today’s jobs report, but they have been improving from earlier levels, and the Dow is even indicated to open slightly higher as we type this. This is all subject to change, though, as the June employment report will be released shortly. Expectations are for an increase of 268K, which would be the lowest monthly reading since the start of 2021, but the real focus will likely be on average hourly earnings which are expected to increase by 0.3%.

Outside of equities, US treasury yields are modestly lower, but the 2s10s yield curve remains inverted for the fourth straight day. Crude oil and gold are basically flat, and copper is down nearly 2%.

In today’s Morning Lineup, we discuss moves in Asian and European markets and economic data from around the world.

With a good deal of emphasis being placed on today’s employment report, we wanted to take a quick look at how the headline payrolls report has come in relative to expectations over the last year. In the last 12 monthly reports, the headline number has exceeded expectations seven times and missed forecasts five times. Looking at the chart, though, the margin of the misses has been much larger than the magnitude of the beats. In four of the five misses, the actual reading came in more than 250K below forecasts, and the overall average miss was 291K. In the seven beats, however, the average beat was just 143K or less than half of the magnitude of the average miss. Applying the average miss to today’s report, if the June report missed expectations by the ‘average’ amount of the last year, it would be a negative reading. A lot of ifs there, but just helps to put things in perspective.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Weekly Sector Snapshot — 7/7/22

B.I.G. Tips – On Pins and Needles Ahead of Earnings Season

We’re on the cusp of another earnings season as next Thursday will unofficially kick off the Q2 reporting period when the major banks and brokers start to report their results. After a second-quarter where commodity prices spiked, the dollar surged, and economic data slowed, investors have been looking ahead to earnings season like a cow feels walking into the slaughterhouse. The general consensus seems to be that overall expectations remain way too high given the tough macro backdrop.

For a more detailed rundown of the earnings schedule for the upcoming season, please see our Earnings Explorer Tool (available to all Institutional clients) on the Tools section of our website, and to see our quarterly preview of the upcoming earnings season with respect to analyst sentiment heading into it, start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: Earnings Still In Decent Shape

Bulls Back Below 20%

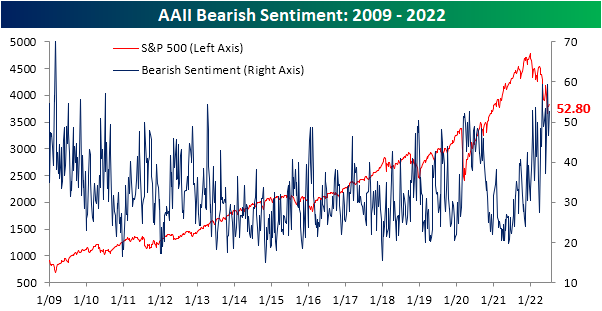

Even though the second half of June and first week of July have seen the S&P 500 climb back from its lows, sentiment appears to show that investors are not buying it. In today’s update of AAII sentiment survey, there was an overall push toward more bearish tones. For starters, the percentage of respondents reporting as bullish fell back below 20%. Even though that is not any sort of new low, this week is the fifth in a row with less than a quarter of respondents reporting as bullish. As shown in the second chart below, such a streak has been unprecedented with the last example of such an extended streak of depressed sentiment being May of 1993.

As bulls have been no where to be found, bears are plentiful with over half of respondents reporting bearish sentiment. This week’s reading came in at 52.8%, up from 46.7% last week. Mirroring bullish sentiment, that is not any sort of new pinnacle for bearish sentiment as there were even higher readings that closed in on 60% last month. Regardless, sentiment remains historically pessimistic with few other periods having seen such elevated readings for as extended of periods.

With inverse moves in bulls and bears, there is now a 33.4 percentage point gap between the two readings which is in the 2nd percentile of all readings since the survey began in 1987.

That leaves neutral sentiment to be the only normal reading of the survey. At 27.8%, neutral sentiment is in the middle of its pandemic range and only 3.6 percentage points below its historical average.

The more bearish turn at the expense of bulls witnessed in this week’s AAII survey was echoed by other readings on sentiment like the Investors Intelligence survey and NAAIM Exposure index. Combining all three of these sentiment readings into one composite, overall outlooks for the market took a further bearish turn this week with the average survey currently 1.8 standard deviations below its historical norm. That is slightly better than earlier this spring, but still, the only period since the mid-2000s with similarly pessimistic readings was in late 2008 and into 2009. Click here to learn more about Bespoke’s premium stock market research service.

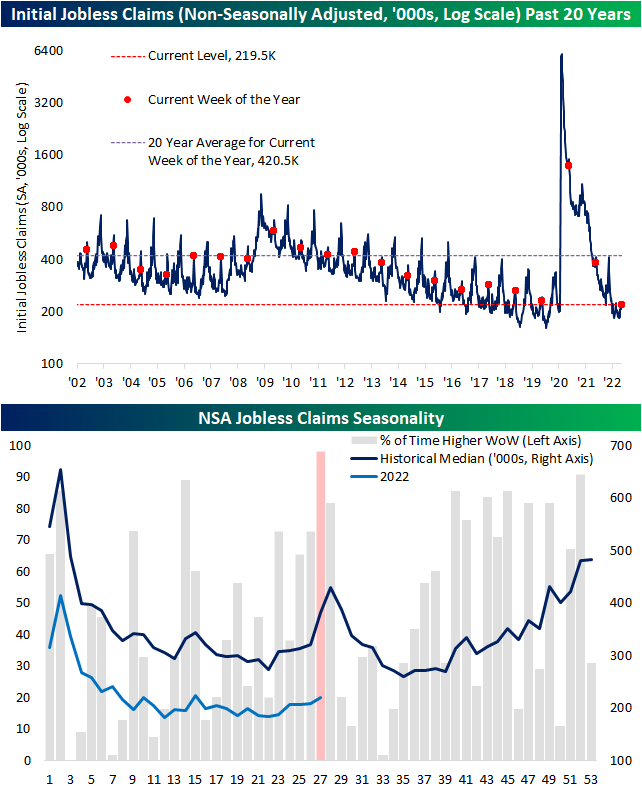

Worst Week of the Year For Claims

Initial jobless claims remain historically healthy in the low 200K range, but the most recent week’s data did mark one of the highest readings of the year. Coming off of last week’s unrevised 231K, claims rose 4K to the highest level since the second week of the year when they clocked in at 240K. That remains a much better reading than what was observed throughout much of the history of the data, but it is at the higher end of pre-pandemic readings (those from roughly 2017 through 2019).

As for the non-seasonally adjusted number, the current week of the year is essentially guaranteed to see a week-over-week increase. The current week has historically been the worst of the year in terms of week-over-week moves only having seen unadjusted claims fall once since 1967. That one decline was in 2020 when claims were working off unprecedented record highs. Given that historically consistent drift higher in claims during this point of the year, next week has historically averaged a temporary peak in claims. While that lends to the possibility of claims continuing to rise next week, the current reading is below that of comparable weeks of pre-pandemic years. In other words, claims are following standard seasonal patterns and are doing so at historically strong levels even if they have come off the absolute strongest levels of the pandemic.

Continuing claims have also begun to come off of the best levels of the pandemic. Adjusted continuing claims were expected to go unchanged at 1.328 million this week. Instead, they rose up to 1.375 million; the highest level since the week of April 22nd when claims were 12K higher. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke’s Morning Lineup – 7/7/22 – Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Politics is not a game, but a serious business.” – Winston Churchill

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Given the state of politics on both sides of the Atlantic, most would probably take issue with Churchill’s description of the political process, especially the second part. Anyway, it’s always interesting to see instances where a CEO announces his or her resignation from a company and its stock rallies. How must the individual leaving the company feel watching the market cap of the company rise now that they’re gone? Talk about a lack of a value-add! Anyway, as bad as it must make a CEO feel, how must Boris Johnson feel today that British stocks and the pound are all rallying on news of his resignation? There’s a reason you need a thick skin to be successful in politics.

Stocks aren’t just rallying in Europe this morning as major indices around Europe and the world along with US futures are all in positive territory. The S&P 500 has been higher in each of the last three trading days, and if early gains hold today would be the fourth straight day of gains. In order to get there, though, we’ll have to get through Jobless Claims at 8:30, Energy inventories at 10:30, and then two Fed speeches from Waller and Bullard this afternoon. Jobless claims came in at 235K which was slightly higher than expected and the highest level in nearly six months.

In today’s Morning Lineup, we discuss moves in Asian and European markets, reports of a $200+ stimulus plan in China, and economic data from around the world.

As mentioned above, if today’s early gains hold today would be the fourth straight day of gains for the S&P 500. That may not sound all that impressive (it isn’t), but in a year like 2022, it is enough to be tied for the longest winning streak of the year. Earlier this year in Q1, there were three other streaks of similar duration, but in Q2, the best the S&P 500 could do was three days.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Meaningless Minutes, Openings, Housing, Ag – 7/6/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of the minutes from the June FOMC meeting (page 1) followed by a look at job openings through today’s JOLTS report (page 2) and Indeed data (pages 3 and 4). We then pivot to housing data with the latest delinquency readings out of the Mortgage Monitor report from Black Knight (page 5) and realtor.com data covering inventories and prices (page 6). We then shift into the latest PMIs (page 7) before closing with a look into the declines in agriculture commodities (page 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!