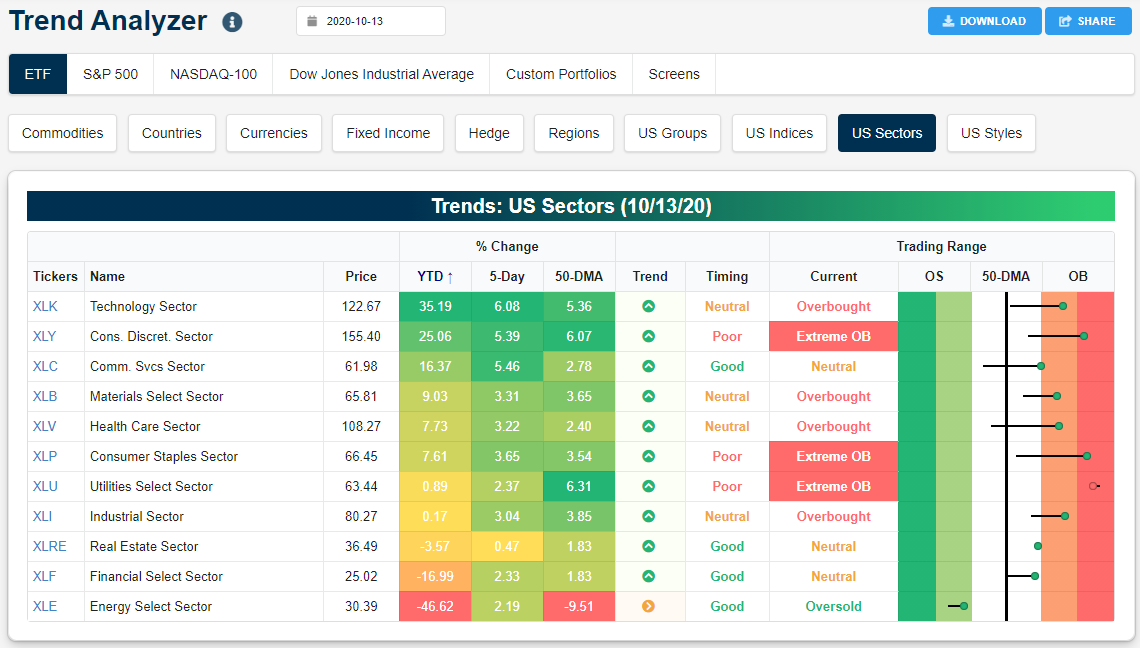

Year-to-Date Sector ETF Performance

The most popular S&P 500 ETF — SPY — is currently up 10% year-to-date. Below is a snapshot from our Trend Analyzer tool (available to Bespoke Premium subscribers) that shows S&P 500 sector ETFs and their year-to-date performance (among other stats). As shown, eight of the eleven major sector ETFs are in the green for the year, with Technology (XLK) leading the way at +35.2%. That’s a pretty incredible move in a pandemic year, and it shows just how powerful the Tech sector is regardless of how well the “physical” economy is doing. The Consumer Discretionary sector (XLY) ranks second with a year-to-date gain of 25.06%, but that gain is mostly buoyed by Amazon.com (AMZN), which is easily the largest stock in the cap-weighted sector. The only other sector that’s up more than 10% on the year is Communication Services (XLC) at +16.4%.

Materials (XLB), Health Care (XLV), Consumer Staples (XLP), Utilities (XLU) and Industrials (XLI) are the remaining sectors in the green in 2020 with gains between 0 and 10%. On the downside, Real Estate (XLRE) is only marginally in the red with a YTD decline of 3.57%, and then you get to the two big losers on the year — Energy (XLE) and Financials (XLF). The Financial sector (XLF) is down 17% so far this year while Energy (XLE) is down 46.6%. The gap of more than 80 percentage points between the year’s best and worst performing sectors is something that rarely happens, but then again, 2020 has been a year like no other! Try our Trend Analyzer tool with a two-week free trial to Bespoke Premium.

Bespoke’s Morning Lineup – 10/14/20 – Positive Earnings, Negative Reactions

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“A few solid pros are more powerful than dozens of cons,” – Steve Jobs

Bulls are looking to get back on track this morning following Tuesday’s weakness. Futures are trading modestly higher in the pre-market and have been building on those gains as we approach the open. In economic news, PPI came in hotter than expected on both a headline and core basis, rising 0.4% m/m versus expectations for growth of just 0.2%.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, industrial production in Europe, trends related to the COVID-19 outbreak, and much more.

It’s been a positive morning for earnings reports this morning. Of the eight companies reporting so far, the only one to miss EPS forecasts was Wells Fargo (WFC), while the only one to report weaker than expected sales was Bank of America (BAC). On the upside, Goldman (GS), PNC, and UnitedHealth (UNH) all had the biggest EPS beats while Goldman also saw a healthy beat on the revenue front as well.

All these strong results should set the market up for some strong performance this morning, right? Well, not necessarily. Yesterday we saw a similar story with a number of solid reports from S&P 500 companies, but when the stocks opened for trading, all but one traded lower for a median decline of over 2%. Hopefully, for the broader market, this doesn’t become a trend, but we’ll be watching it in real-time.

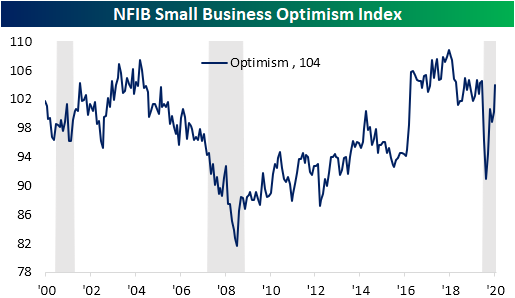

Small Businesses Cautiously Optimistic

In an earlier post, we highlighted the details of the September NFIB Small Business Optimism report. The report showed overall sentiment among small businesses has continued to improve as demand has bounced back (though it has not yet fully recovered as still more businesses report lower sales and earnings on a net basis) leading to low inventory levels, higher prices, and a need for more employment. While generally improved conditions have lifted optimism, that is not to say small businesses have given an all-clear. The Uncertainty Index from NFIB has risen each of the past three months with September’s 2-point increase bringing it back to the same level as March of this year. In other words, it is perhaps best to say that small businesses are cautiously optimistic.

From the pandemic to the Election, there are plenty of reasons for businesses to be uncertain. As for what they are reporting to be the biggest problems, labor remains at the top. 30% of businesses have reported that either cost (9%) or more predominately quality (21%) of labor are their biggest issues. While off the highs from the past few years, the current readings are still historically elevated.

Behind labor, government related problems also are largely on the minds of business owners. Government red tape and taxes combine to account for 29% of businesses’ biggest problems. While that is a large share, neither of those indices are at any sort of extreme.

Poor sales, on the other hand, remains as the third major concern for businesses. 12% of businesses reported poor sales as the single most important issue in September, down from 15% in August and 7-percentage points lower than the April peak. While improved, the number of businesses seeing demand as a major issue is still at some of the highest levels of the past several years. Click here to view Bespoke’s premium membership options for our best research available.

Small Business Smiles

Sentiment among small businesses continued to improve in the month of September according to the NFIB’s monthly Small Business Optimism Index. As shown below, the index rose 3.8 points to 104 which is now just half of a point below the levels prior to the pandemic in February. That was also better than expectations of a smaller improvement to 101.2. Small business sentiment has now risen in four of the past five months.

In the table below, we break down this month’s report by each of the ten components of the headline number as well as the many other indices included in the report such as those not used as inputs to the headline number and what small businesses are reporting to be their biggest problems.

Across all indices of the September report, breadth was solid with only a couple of indices falling month over month—Expected Credit Conditions and Credit Conditions Availability. Some of those that were higher saw record or near-record month-over-month increases.

Some of the most notable indices this month included those regarding inventories. The Current Inventories index which gauges the net percent of owners viewing current inventory levels as too low rose 2 points to a record high reading of 5. Given this, the index for Plans to Increase Inventories is tied with the reading from November of 2004 for a record high of 11. Indicating low inventory levels, the report is consistent with some other recent data like the regional Fed manufacturing surveys. Those low inventories are resulting in higher prices as that index’s 12-point increase in September marked the biggest one month gain on record. While the Higher Prices index is not at any sort of an extreme, September’s move indicates that a rising number of businesses are raising prices.

Additionally, those higher prices and lower inventory numbers appear to be a result of demand that continues to rapidly improve. The indices for Actual Sales and Actual Earnings Changes remain negative for a sixth and tenth month in a row, respectively, meaning a net number of businesses continue to see lower rather than higher top and bottom-line numbers. But these indices are seeing big moves higher. For the index of Actual Earnings Changes, the 13-point climb in September was the largest on record and the 9-point increase for Actual Sales Changes followed a 13-point increase in August; both being some of the largest one-month moves on record. In order to meet the needs of this demand, a higher number of businesses plan to increase employment with that index rising to 28; the highest level since December of 2018. Even though businesses seek to hire more, they also report it is hard to fill positions as the index of Job Openings Hard to Fill rose to the top 5% of all readings. Cost and quality of labor also were reported as two of the most pressing problems for businesses. Click here to view Bespoke’s premium membership options for our best research available.

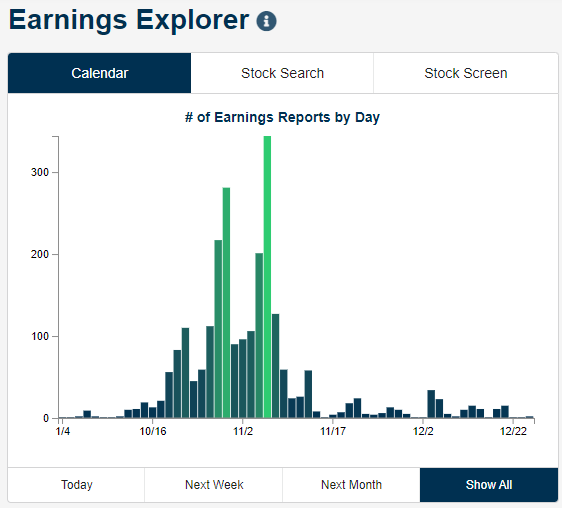

The Most Volatile Stocks on Earnings: Q3 2020

The Q3 earnings season began in earnest this morning with the first of the big banks (C and JPM) reporting. As shown below, the number of reports per day will get larger and larger over the next few weeks with the peak coming in the first week of November.

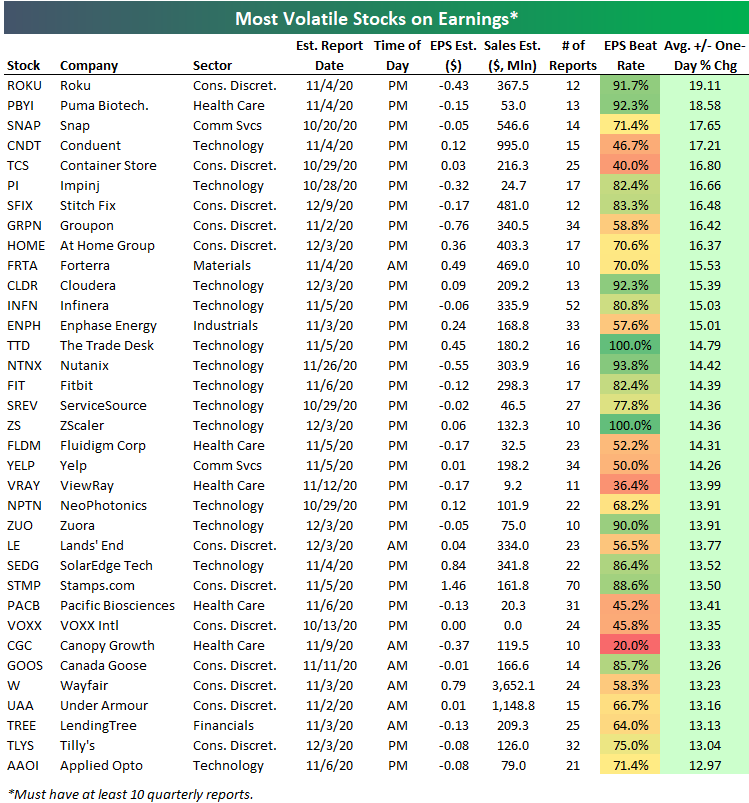

As we do at the start of each earnings season, below is our list of the most volatile stocks on earnings. These are stocks with at least ten years of quarterly earnings reports that have historically seen the biggest price moves on their earnings reaction days. (For a stock that reports after the close, its earnings reaction day is the next trading day’s change. For a stock that reports before the open, its earnings reaction day is that day’s change.)

As shown, Infinera (INFN) is the most volatile stock on earnings for those stocks with at least ten years of earnings reports. INFN has historically averaged a one-day change of +/-15% on its earnings reaction days. Stamps.com (STMP) ranks second with an average change of +/-13.5% on earnings, followed by Glu Mobile (GLUU) and Conn’s (CONN). Netflix (NFLX) ranks fifth on the list with an average one-day change of +/-12.29% on earnings. NFLX is by far the biggest stock on the list with sales estimates this quarter of $6.4 billion.

Other notables on the list of most volatile stocks include iRobot (IRBT), Overstock.com (OSTK), First Solar (FSLR), Align Tech (ALGN), and Booking Holdings (BKNG).

Most stocks on the list below don’t report earnings until later this month or in early November. Netflix (NFLX) and iRobot (IRBT) are the stocks on the list that will report first on October 20th.

If we broaden our list to include stocks that only have at least 10 quarterly earnings reports, a lot of new names show up that haven’t been public for very long. At the top of the list below is Roku (ROKU) which has had 12 quarterly reports in its history. ROKU has historically averaged a one-day change of just under 20% (19.1%) on its earnings reaction day. It’s pretty incredible for a company to average a 20% swing in its market cap on one day every three months.

The first eleven stocks on the list below are not on the list above because they don’t have more than ten years worth of quarterly earnings data. These include names like Snap (SNAP), the Container Store (TCS), Stitch Fix (SFIX), Groupon (GRPN), and At Home Group (HOME). Other well-known stocks that normally see huge moves in reaction to earnings include Fitbit (FIT), Yelp (YELP), Canopy Growth (CGC), Canada Goose (GOOS), Wayfair (W), and Lending Tree (TREE). Try out our Earnings Explorer tool for free with a two-week trial to Bespoke Institutional.

Chart of the Day: What Do Strong Beat Rates Mean For Q3 Earnings?

Bespoke’s Morning Lineup – 10/13/20 – Good First Impression

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Grow or die, that’s what I believed, no matter the situation.” – Phil Knight, Shoe Dog

With earnings season kicking off in earnest this morning, the above quote is probably the mantra of most CFOs of public companies. If you can’t show growth, kiss your stock price goodbye. Thankfully for the market this morning, the results we have seen so far as of this writing have been positive. With the exception of Fastenal (FAST), which reported inline EPS and AZZ, which missed revenue forecasts, every other company that has reported this morning has topped both EPS and revenue forecasts. Sure, it’s only eight companies, but it’s a good start.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, major earnings releases, economic sentiment, trends related to the COVID-19 outbreak, and much more.

Outside of the US, emerging market equities have generally lagged the S&P 500, but in the recovery off the September lows, emerging market equities have the distinction of taking out their early September highs before the S&P 500. Not only that but just yesterday, the Emerging Market ETF (EEM) managed to also make a marginal new 52-week high as well. If it can build on those gains in the days ahead, the breakout will be confirmed.

Speaking of breakouts, EEM has essentially been range-bound for the better part of thirteen years. Since making an all-time high in 2007, EEM has seen multiple rallies to the low to mid-$50s area only to pull back. EEM closed yesterday at $46.23, so it’s nowhere near testing resistance at multi-year highs yet, but it’s something to keep on the radar. When and if it makes new highs in the months ahead, it will mark a notable long-term breakout more than a decade in the making.

Big Banks Reporting This Week

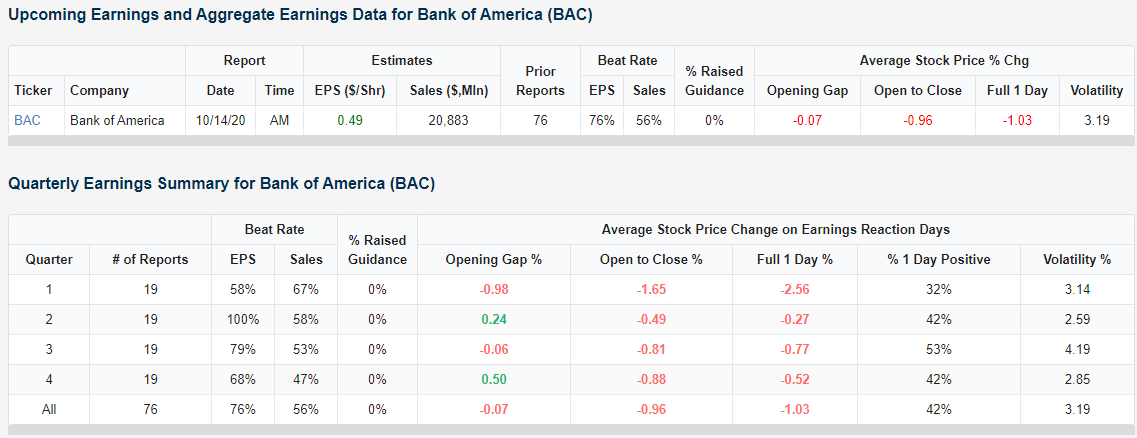

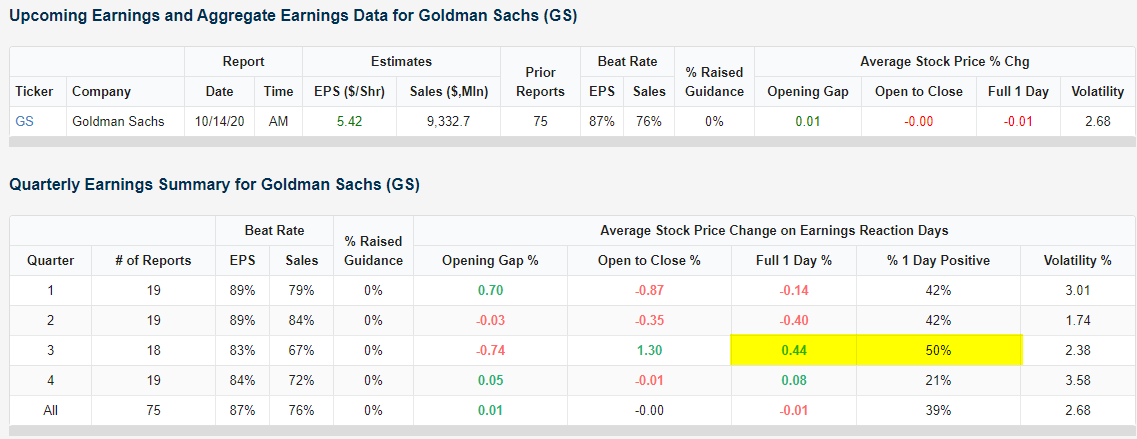

The third quarter earnings season begins this week with the first of the big banks set to report tomorrow morning. One feature of our Earnings Explorer tool is an interactive earnings calendar with detailed information on stocks set to report earnings in the days, weeks, and months ahead. Below is a snapshot of the calendar showing expected earnings reports through Wednesday morning. Notably, Citigroup (C) and JP Morgan (JPM) will report tomorrow morning, while Bank of America (BAC), Goldman Sachs (GS), and Wells Fargo (WFC) will report on Wednesday morning.

You can dig deeper into individual stocks with our Earnings Explorer tool to see their historical earnings reports and how investors reacted. Below we show aggregate earnings snapshots for both Citigroup (C) and JP Morgan (JPM), which report tomorrow ahead of the open.

Notably, the Q3 earnings release for Citigroup has seen the stock average a one-day gain of 0.87% in reaction to the news. That’s a better share price response than any other quarter. Following its historical Q4 earnings releases, for example, Citi shares have been very weak with an average one-day decline of 2.39%.

While Q3 earnings have been okay for Citigroup in terms of share price reaction, it has been the worst quarter of the year for JP Morgan (JPM) historically. Over the last 19 years, JPM has averaged a one-day decline of 0.73% on its Q3 earnings reaction day with positive returns just 26% of the time.

Bank of America (BAC) has the worst numbers of the five big banks reporting this week when it comes to share price reactions to earnings. As shown below, the stock has averaged a decline of 1.03% on its 76 earnings reaction days since 2001 with positive returns just 42% of the time. Goldman Sachs (GS) has also struggled on earnings historically with its share price rising in reaction to the news just 39% of the time. Goldman’s Q3 report, however, has been a bit more bullish with the stock averaging a one-day gain of 0.44% in reaction to past third quarter earnings releases. Finally, Wells Fargo (WFC) is also set to release Q3 earnings on Wednesday, and the stock has only gained in reaction to past Q3 releases 32% of the time. Try out our Earnings Explorer tool for free with a two-week trial to Bespoke Institutional.

Chart of the Day: AAPL Performance After iPhone Reveals

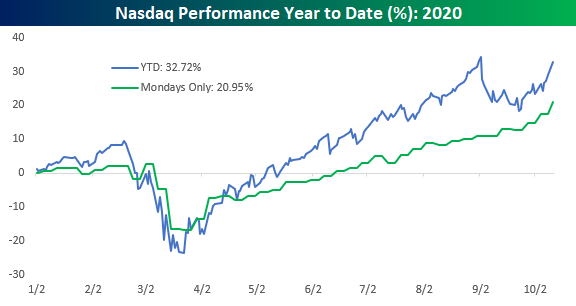

“Meet the Nasdaq”

Tim Russert used to sign off from each week’s episode of Meet the Press with the tagline, “If it’s Sunday, it’s Meet the Press.” Borrowing from that phrase, the Nasdaq’s tagline might as well be “If it’s Monday, it’s Meet the Nasdaq.” With a gain of over 3% today, the Nasdaq is doing what it always does on Mondays – rally! The chart below shows the year-to-date performance of the Nasdaq so far in 2020 as well as its performance if you only owned the index on Mondays. Year to date, the Nasdaq is up an impressive 32.7%, putting it on pace for the first back-to-back annual gain of over 30% since 1998 and 1999. Even crazier, though, is the fact that the Nasdaq is up over 20% year-to-date on Mondays alone! The weekday that most people love to hate has been responsible for more than 60% of this year’s Nasdaq gain.

In the table below we summarize the performance of the Nasdaq by weekday so far in 2020. Monday’s average daily gain of 0.57% with gains more than 75% of the time is both the best average daily return and the most consistent to the upside. Tuesdays and Wednesdays haven’t been particularly bad for the Nasdaq either. Both days have seen an average one-day gain of 0.30% or more, and Wednesday has been positive three-quarters of the time. While the first three trading days of the week have been strong, Thursday and Friday have been days to forget. Although both days have also experienced positive returns more than half of the time, the average one-day change for both is negative resulting in declines on a cumulative. Thursday has been the weakest with a cumulative decline of 11.53% while Friday’s cumulative decline has been more modest at just 3.46%. TGIM. Click here to view Bespoke’s premium membership options for our best research available.