Bespoke’s Morning Lineup – 11/16/20 – Groundhog Week

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“In investing, what is comfortable is rarely profitable.” – Robert Arnott

This week has kicked off looking very similar to last week as futures are surging on news of positive date related to a COVID vaccine. Last week it was Pfizer (PFE), but this morning it was Moderna (MRNA). Even the timing of the news announcements was similar! The MRNA news is very good as the headlines suggest the vaccine is more effective and can be stored in less extreme temperature conditions. What’s also important to note, however, is that futures were already considerably higher before the news, so the animal spirits were already out before the headlines.

In economic news, this week will be a relatively busy one on the data front, but the only report today was Empire Manufacturing for November which came in weaker than expected (6.3 vs 13.5). Also, don’t forget that earnings season will wind down this week with Walmart (WMT) reporting tomorrow.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, trends related to the COVID-19 outbreak, and much more.

Outside of the Nasdaq 100, last week was a positive one for every other major index ETF in our Trend Analyzer screen of major US indices. While QQQ was down just over 1%, the S&P 500 (SPY) was up over 2%, and small caps (IWM) surged over 6%. Those are impressive gains no matter how you look at it, but they also leave the majority of US indices at not only short-term overbought levels but ‘extreme’ overbought levels (at least 2 standard deviations above the 50-DMA). Again, this does not mean that equities have to trade lower from here, but from a timing perspective, conditions are poor.

Bespoke Brunch Reads: 11/15/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Election Analysis

The Polls Weren’t Great. But That’s Pretty Normal. by Nate Silver (538)

Polls were certainly off in 2020, but the national polling miss was far smaller – and less unusual – than the headlines might have indicated. [Link; soft paywall]

Nate Cohn Explains What the Polls Got Wrong by Isaac Chotiner (The New Yorker)

The NYT’s top voting analyst and pollster discusses why polls missed, with granular discussion of the specific factors and voting patterns that led pollsters to predict much larger Biden margins than those that actually appeared. [Link; paywall]

Election Showed a Wider Red-Blue Economic Divide by Jed Kolko (NYT)

This data-heavy column looks at the attributes of red and blue counties to offer some more detailed discussion 2020 vote patterns than simple results maps may indicate. [Link; soft paywall]

Fast Food

The Future of McDonald’s Is in the Drive-Thru Lane by Brian Barrett (Wired)

Machine-learning, transponders, and an emphasis on drive-thru dining are just some of the many innovations McDonalds is working on to power further growth. [Link; soft paywall]

Fast Food’s Bet on Breakfast Goes Bust During Covid-19 Pandemic by Julie Wernau (WSJ)

With more working from home and fewer commutes, fast food companies’ bets on the first meal of the day has gone sour at a grand scale. [Link; paywall]

China

China’s President Xi Jinping Personally Scuttled Jack Ma’s Ant IPO by Jing Yang and Lingling Wei (WSJ)

On October 24th, Alibaba controlling shareholder Jack Ma argued financial regulation is standing in the way of private market innovations that can solve China’s debt problem. President Xi Jinping didn’t take so well to that line of thinking, and a few days later the company’s IPO of Ant Group was pulled. [Link; paywall]

Hong Kong regulator clears funds and banks to implement US sanctions by Primrose Riordan and Nicolle Liu (FT)

In a sign of who really calls the shots in the global financial system, Hong Kong regulators have assured banks that complying with US sanctions that punish officials for enforcing anti-democratic measures designed by Beijing will not lead to a new round of penalties from Beijing. [Link; paywall]

TikTok says the Trump administration has forgotten about trying to ban it, would like to know what’s up by Sam Byford (The Verge)

The US government has gone silent on its directive for Chinese company ByteDance to sell video service TikTok’s US operations, leading the company to ask whether it’s still supposed to be complying with the original order. [Link]

Policy Cliffs

Federal Reserve’s Emergency Loan Programs at Center of Political Fight by Jeanna Smialek and Alan Rappeport (NYT)

Programs which underwrote the bottoming out of financial markets in March and would offer a critical backstop should fiscal policy fail to underwrite a rocky winter period may end up cancelled by the Trump Administration during its lame duck period. [Link; soft paywall]

Investors

Ackman places new bet against corporate credit by Ortenca Aliaj (FT)

After making $2.6bn betting against $71bn of notional corporate credit in late February, Bill Ackman is returning to the theme as he shorts the same market again; it should be noted, however, that he explicitly views this latest trade as a hedge against his equity longs. [Link; paywall]

The Tiny Hedge Fund That’s Loved on Twitter — And Now Backed by Greenlight by Leanna Orr (Institutional Investor)

A small hedge fund run by a Twitter personality has seen a sizeable investment from fund-of-funds Greenlight, offering the large firm’s imprimatur and prestige in addition to more assets. [Link]

The Investors Gambit by Michael Antonelli (Bull & Baird)

What investors large and small can learn from Netflix’s latest smash hit Queen’s Gambit: constant obstacles, many ups and downs, signs for a path, and a face down with rivals are all part of both successful investing and the series. [Link]

New York State of Mind

Richest New Yorkers Will Devastate City If They Leave With $133 Billion by Alexandre Tanzi and Ben Steverman (Bloomberg)

Income taxes account for less than 20% of New York City’s total receipts, but they are dominated by an extremely small and extremely high-income group of 30,000 households making in excess of $1mm/year. [Link; soft paywall]

The Bronx’s Little Italy is thriving amid the COVID-19 crisis by Lisa Fickenscher (NYP)

With New Yorkers stuck near home, Arthur Avenue has seen a boom in business that has kept footfalls at or above the levels that prevailed before COVID struck. [Link]

COVID

Life after COVID-19 hospitalization: Statewide study shows major lasting effects on health, work and more (Michigan Institute for Healthcare Policy & Innovation)

A new study shows that in the two months after leaving the hospital, 7% of severe COVID cases were dead, 15% returned to the hospital, and 12% were unable to carry out basic care of themselves, illustrating the “long tail” of COVID’s impact on the human body long after the acute infection period. [Link]

How Ticketmaster Plans to Check Your Vaccine Status for Concerts: Exclusive by Dave Brooks (Billboard)

The events company plans to use third-party services as well as health care providers to make sure that attendees either had a negative COVID test or vaccination in the past couple of days before any event they attend. [Link]

Animal Products

When Pigs Fly, They Want Drinks, Leg Room by Lucy Cramer (WSJ)

Faced with crashing passenger counts, airlines are scrambling to re-orient their fleets towards cargo hauling, and some of their passengers have even more finnicky than the human kind. [Link; paywall]

Where’s the meat? UK’s first vegan butchers launches (Reuters)

Soy and seitan-based proteins will be the focus in a new UK business that hopes to cater to customers who have completely forgone animal products. [Link; auto-playing video]

The Secrets of Deviled Eggs by Emily Strasser (The Bitter Southerner)

A uniquely Southern hors d’oeuvre (or maybe hors d’oeuf) is the focus of cravings and mouth-waterings all across the country, bringing with it a unique food history that is much more intense than many other favored foodstuffs. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Event Risk Off, Event Risk On

US equity performance this week was dominated by vaccine news. Good data from Pfizer early in the week sparked all-time highs for small caps and robust equity rallies around the world. Technical backdrops have improved dramatically both in the US and Europe versus where they sat just before the US election. The relief rallies in stocks around the world are indicative of just what can happen when risk events are taken off the table. Unfortunately for investors, the risk events moving off the table have been replaced by others: government funding deadlines in mid and late December, as well as more Phase 3 trial data from vaccine companies. In the background, the US economy is starting to slow as COVID prevalence explodes across the country. We discuss all the latest US data, earnings results, and more in this week’s Bespoke Report.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

A Very Good Ten

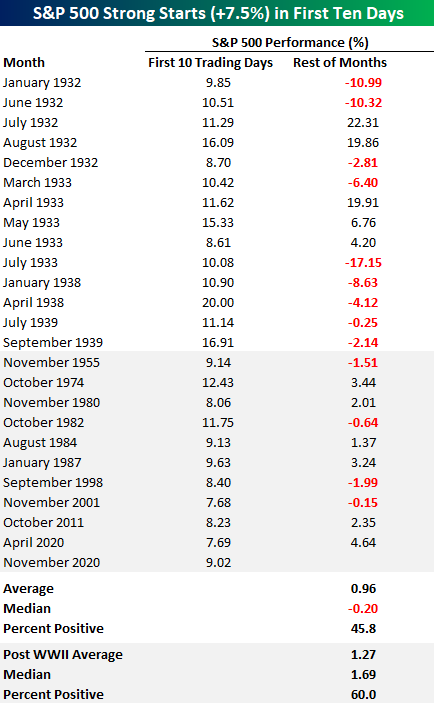

With nearly ten trading days under its belt for November, the S&P 500 is putting together quite a month. Through early morning Friday, the S&P 500 was up just over 9% which ranks as the best first ten trading days for a month since January 1987. In the entire history of the S&P, there have only been 17 other months where the S&P 500 was up over 9% in the first ten trading days of the month, and in the post-WWII period, there have only been five.

So, when a month starts off strong, does it usually finish that way? Or is there some sort of reversion to the mean? Unfortunately, prior experience isn’t particularly consistent in one direction of the other. The table below shows each month since 1928 where the S&P 500 was up at least 7.5% in the first ten trading days of a month. Overall, the S&P 500’s average rest of month performance has been a gain of 0.96%. That sounds good, but on a median basis, the rest of the month typically sees a decline of 0.2% with positive returns less than half of the time.

In looking at the chart above and the table below, you’ll notice that most of the strong starts for the S&P came during the Depression in the pre-WWII period. In 1932 and 1933, for example, there were five occurrences each year! Looking at the post-WWII period where the frequency of occurrences wasn’t nearly as common, strong starts to a month typically saw a more positive but still not a very consistent trend. In the ten prior months since the end of WWII, the S&P 500’s average rest of month performance was a gain of 1.27% (median: 1.69%) with gains 60% of the time. Click here for a free trial and full access to Bespoke’s research and interactive tools.

Bespoke’s Morning Lineup – 11/13/20 – Finishing Strong

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Formal education will make you a living; self-education will make you a fortune.” – Jim Rohn

With schools across the country either returning or continuing to operate in a virtual manner through at least the end of the year, the above quote is just as pertinent as ever. School is important, but if you don’t continue to teach yourself outside of the classroom, you’re missing the point.

Futures are pointing to a positive finish to the week. On the earnings front, Cisco (CSCO), Disney (DIS), and Applied Materials (AMAT) are all trading higher, but other than that there are no major catalysts to speak of, and the only economic data on the calendar today is October PPI and a preliminary read on Michigan Confidence. PPI came in slightly stronger than expected at the headline level but was weaker than expected on a core basis.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, earnings and market news out of Europe, trends related to the COVID-19 outbreak, and much more.

It’s been a strong month so far for equities around the world. In Europe, the STOXX 600 is already up 12.4%, which puts the index on pace for its second-best month in the last thirty years. What makes that even more impressive is the fact that the month isn’t even half over! Despite the surge in European equities, the strength has barely even put a dent in the long-term relative strength of the STOXX 600 relative to the S&P 500. If you look real closely (or at the enlarged chart below), though, Europe is attempting to make a move as the downtrend in relative strength that has been in place all year has recently been broken to the upside. There’s been a lot of false alarms in Europe over the years, but at least it’s a start.

Chart of the Day: Spectacular Sentiment

Claims Keep Grinding Lower

Initial claims have continued to fall with this week marking yet another low of the pandemic. Seasonally adjusted initial jobless claims came in at 709K this week, 21K below expectations. Although that reading is still well above levels from the start of the year, this new post-pandemic low is also now only 14K above the previous pre-pandemic record high of 695K in October of 1982. In other words, claims are still clearly elevated from a historical perspective but are at least closing in on re-entering what has historically been a more normal range.

In spite of this week’s improvement, last week’s reading was revised higher from 751K to 757K, but given that revised number the week over week decline of 48K was the largest since the first week of October. That decline also means claims have also declined in six of the past eight weeks.

On a non-seasonally adjusted basis, claims were likewise lower falling to 723.1K from 743.9K last week. While not as consistent as the seasonally adjusted number, non-seasonally adjusted claims have declined in all but three of the past eight weeks. Those declines are bucking seasonal trends as claims have had a tendency to drift higher at this time of year.

Not only have regular state claims continued to fall but so too have claims for Pandemic Unemployment Assistance (PUA). PUA claims saw the largest week over week drop (-63.8K) since the first week of October (-129.8K) as total PUA claims came in at the lowest level since the first week they were reported on April 17th. Combined with the regular state number, claims sit just above 1 million which is again the lowest of the pandemic.

Continuing claims, which are lagged one week to initial claims, are at the lowest level since the week of March 20th as they came in below 7 million. Continuing claims totaled 6.786 million which was down 436K from last week. With another week over week decline, claims by this measure have now declined in all but four weeks since the peak on May 8th. The current streak of weekly declines has grown to seven weeks long though this week’s drop was the smallest of these past nearly two months.

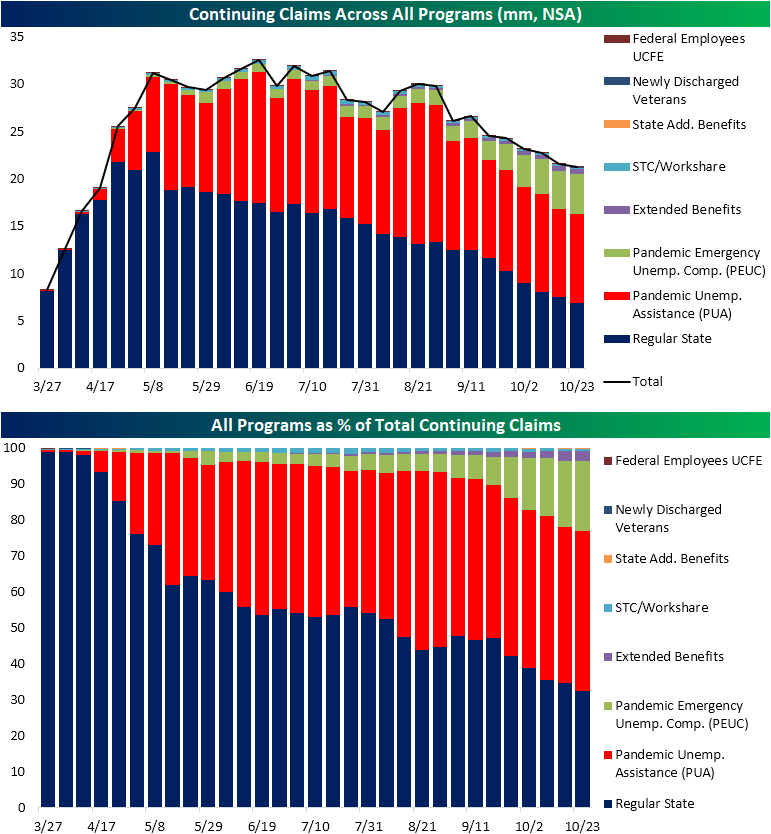

As with initial claims, regular state claims don’t tell the full picture given the several other programs in the unemployment insurance system. In the charts below, we show a breakdown of continuing claims by each program. This is lagged yet another week to regular claims. For the most recent week (October 23rd), total claims across all programs were lower at 21.2 million versus 21.6 million the prior week.

Regular state claims—the largest component—led those declines as PUA—the second largest—claims actually rose 0.1 million. Additionally, the recent trend of growth in extension programs has to an extent continued. PEUC claims, which provides several weeks of additional benefits after the expiration of regular unemployment insurance, rose from 3.98 million to 4.14 million; a new high for the pandemic. Given this, PEUC claims also make up the largest share of total claims yet at 19.5%, up 1 percentage point from the previous week. On the bright side, the extended benefits program—another program for additional weeks of UI once benefits run out—was slightly lower at 0.55 million (2.6% of all claims) compared to 0.57 million the previous week (2.7% of all claims). Overall, claims continue to improve and are broadly around some of the least bad levels of the pandemic, but there is evidence through the growth of PEUC claims that some people have yet to return to works and have now been unemployed for extended periods of time. Click here to view Bespoke’s premium membership options for our best research available.

Bespoke’s Morning Lineup – 11/12/20 – Retrenchment

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“I was reading in the paper today that Congress wants to replace the dollar bill with a coin. They’ve already done it. It’s called a nickel.” ― Jay Leno

Equity futures are getting hit relatively hard this morning following continued surges in COVID case counts as hospitalizations have now exceeded their peaks from the Summer. In response, states are instituting more restrictions on movement. While the broader market is lower, Nasdaq futures are bucking the trend and still indicated to open in positive territory as investors rotate back into the stay at home stocks.

Against a backdrop of rising COVID cases, economic data today was generally positive. CPI came in weaker than expected, so maybe instead of a nickel, the coin referenced in the quote above should be a dime instead. In terms of jobless claims, both initial and continuing claims came in lower than expected and fell to their lowest levels since the pandemic.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, economic data out of Europe, trends related to the COVID-19 outbreak, and much more.

The chart below is from the second page of our Morning Lineup and shows where the S&P 500 is trading on a daily basis relative to its 50-day moving average. Yesterday, the S&P 500 closed just shy of levels we consider to be extreme (>2 standard deviations from 50-DMA). This is the same level that the S&P 500’s rally ran out of steam back in early September. While extreme overbought levels hardly mean that a pullback is guaranteed, when the S&P 500 gets to these levels, it’s not uncommon for the market to take at least a short-term pause in order to catch its breath.

Bitcoin Going for the Gold

Topping the big gains in US equities since the election may sound like a tough task, but bitcoin has been up to the challenge. Since Election Day, bitcoin has now rallied more than 14% taking its price further outside of the upwardly trending range it has traded in for most of the last year. Outside of the last week, the only other time that bitcoin has deviated from its one-year range was at the depths of the COVID crisis back in the spring. The break of the trend back then proved to be short-lived, so we’ll see if this most recent breakout has staying power or ultimately loses steam. For reference, a retracement back into its prior range would take prices back down to $13,000 from the current level of $15,700.

One chart we like to keep tabs on is the ratio of bitcoin to physical gold. Both assets are essentially considered stores of value, so it’s interesting to see how accepting investors become of ‘digital gold’ over time. Obviously, there are a lot of other factors at play that impacts both assets, but the chart below provides a rough approximation. At current levels, one bitcoin will buy about 8.5 ounces of gold. That’s not far from the most recent peak of just under 9.0 back in July 2019. If and when the ratio breaks above that level, the next level to watch would be the record high of 14.8 in December 2017. Based on gold’s price now, that would translate to a price of about $27,500.

While there are plenty of arguments to be made in favor of the long-term prospects for bitcoin, we would note that even for a volatile asset like bitcoin, the rally of the last week or so has been on the extreme side. Just last week the ratio between bitcoin and gold was around 7.5, but in the span of a week, one bitcoin will buy once ounce more gold than it did just last week. Click here to view Bespoke’s premium membership options and sign up for a free trial.

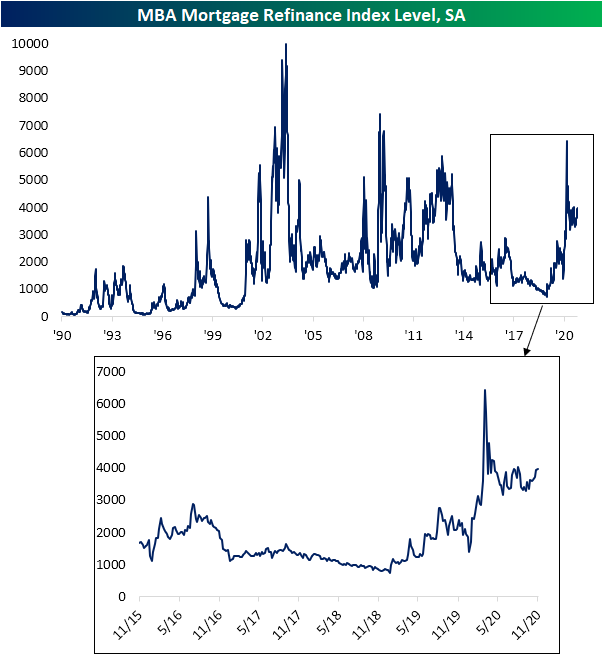

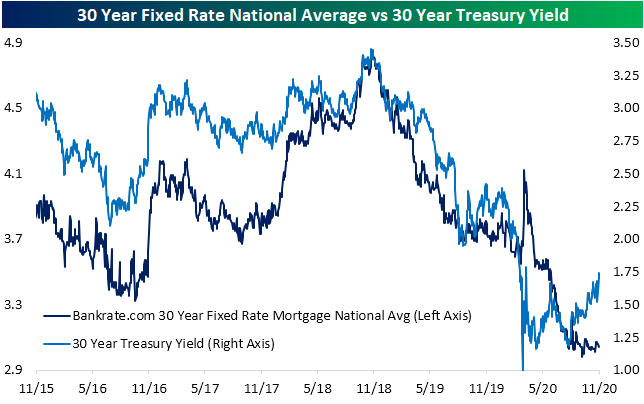

Mortgage Purchases Decline Barely Making a Dent

Rates have been on the rise over the past few months with the 30 year Treasury yield now hovering around its highest levels since March. Despite that general rise in rates, the 30-year national average for a fixed-rate mortgage has remained fairly stable without any significant uptick. The national average is currently at 3.04% which is basically in line with the average over the past three months.

Despite mortgage rates remaining relatively stable, there has been a downward move in purchase applications in recent weeks. Released this morning, the MBA’s weekly reading on purchases fell 2.56% week over week to the lowest level since May. This week also marked the sixth time in the past seven weeks that the seasonally adjusted purchase index has fallen. Despite this, that move lower since the peak in September has barely made a dent on a longer time horizon.

Those declines in the seasonally adjusted index come during what is typically one of the weaker times of the year for purchase activity. As shown in the charts below, the second half of the year typically sees purchases fall into year’s end. Those seasonal patterns are still very much holding true this year, though, purchases are still running well above the levels of the comparable weeks of the past decade and the annual peak (blue dot) came several weeks after what has typically been the norm.

Although purchases have been on the decline from what were very strong levels, refinancing activity has held up well. The Refinance Index rose for a fourth week in a row this week as it reached its highest level since early August. Click here to view Bespoke’s premium membership options for our best research available.