The Bespoke 50 Growth Stocks – 3/31/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Chart of the Day: Same Old Story As Stocks Move Off Their Highs

Bears Go Back Into Hibernation

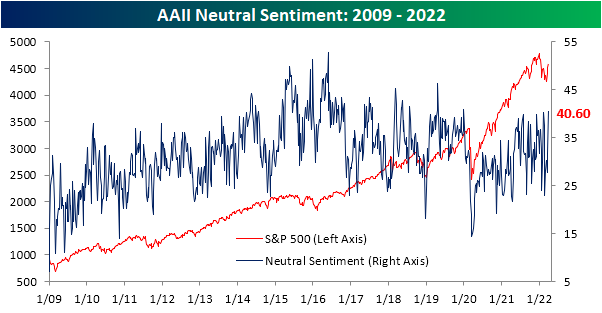

The last couple weeks of the first quarter have seen equities reverse a sizable portion of this year’s losses and sentiment has rebounded in sync, though, bullish sentiment turned slightly lower this week in spite of the S&P 500’s move higher. From the weekly AAII sentiment survey, bullish sentiment shed 0.9 percentage points coming in at 31.9%. Even after that decline, the current level of reported optimism remains above all others (outside of last week) since early January, but bullish sentiment still would need to rise another 6 percentage points to move back up to its historical average.

While more investors are not reporting much optimism, fewer are outright bearish. Bearish sentiment fell for a second week in a row falling another 7.9 percentage points to 27.5%. With a little over a quarter of respondents reporting as bearish, this sentiment reading is at the lowest level since November. That is also now the biggest two-week decline in bearish sentiment (22.3 percentage points) since November 2009 when it had fallen 23.74 percentage points in a two-week span.

Finally, we would note that given bearish sentiment has plummeted at a historic rate without much of an increase in bullish sentiment, neutral sentiment has picked up the difference. That reading clipped above 40% this week for the highest level since January 2020.

Other sentiment surveys like the Investors Intelligence one and NAAIM’s Exposure Index have also pivoted more bullish this week. As a result, our sentiment composite is close to zero meaning across these three indicators, sentiment is now only just slightly below the historical average. Click here to view Bespoke’s premium membership options.

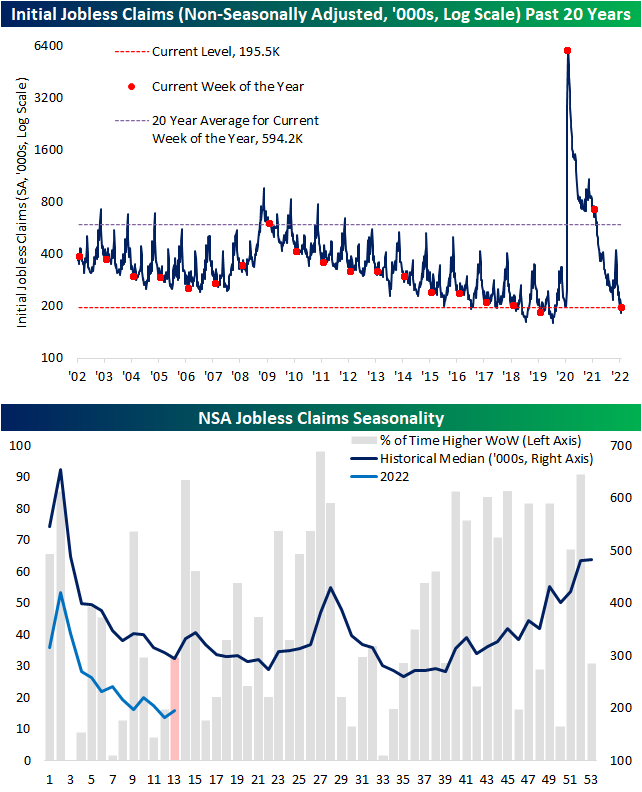

Continuing Claims At The Lowest Level Since 1969

Whereas last week’s release of initial jobless claims set a new multi-decade low, this week that number was revised up by 1K. That means last week’s revised reading of 188K matched the December low. Turning to this week, claims came off that low rising 14K. Albeit higher, at 202K initial claims remain at historically strong levels.

On a non-seasonally adjusted basis, claims had another sub-200K showing after rising 13.2K week over week. In terms of seasonality, the current week of the year has historically seen unadjusted claims fall sequentially more often than not, and the following couple of weeks have tended to see a seasonal uptick in claims. In other words, we’re likely to see claims rise on account of seasonal factors in the coming weeks.

Delayed one week to initial claims, the continuing claims number was the most impressive part of the most recent release. Coming in just above 1.3 million, seasonally adjusted claims hit the lowest level since the final week of 1969. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 3/31/22 – Au Revoir

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I ought to be jealous of the tower. She is more famous than I am.” – Gustave Eiffel

133 years ago today, the Eiffel Tower, one of the most iconic landmarks in the world today opened for business. It may sound hard to believe, but when the tower first opened a number of critics thought it would be an eyesore on the Paris landscape, and twenty years after it opened the Eiffel Tower was almost demolished when the lease on the land it stood on expired. The main reason it was spared was because of its utility as a radio antenna! More than 100 years later, the mere thought of Paris without the Eiffel tower would be considered a sacrilege. Just like in the stock market and everything else in life, one person’s (or generation’s) trash is another one’s treasure.

In markets this morning, investors want nothing to do with oil as WTI is trading down more than 5% on reports of a massive stockpile release from the US Strategic Petroleum Reserve (SPR). For more on this and how the SPR works, make sure to check out our explanation in today’s Morning Lineup. The weakness in futures has equity futures up modestly, but it’s the last day of the quarter, so expect to see a decent amount of volatility throughout the trading day.

In economic news, we just got a slug of economic data this morning, and there weren’t that many major outliers. Perhaps the biggest outlier was Personal Spending which rose 0.2% versus forecasts for an increase of 0.5%.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

There’s still a day left in the quarter, and despite the strong rally in the last couple of weeks, for the majority of stocks and sectors, it has been a quarter to forget. On a year-to-date basis, Energy is the clear leader with a gain of more than 40%, but over the last week, both Utilities and Financials have moved into positive territory for the year. At the other end of the spectrum, Communications Services, Consumer Discretionary, Technology, and Real Estate are all still looking at losses of more than 5%. Not great, but it could have been a lot worse were it not for the 3.5%+ gains in the last week.

While the vast majority of sectors are looking at YTD declines to close out Q1, they’re also trading at short-term overbought levels. All eleven sectors are currently above their 50-DMAs, and all but Financials and Communication Services are also ‘overbought’ (at least one standard deviation above their 50-DMA.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Chart of the Day: Sector Performance Before and After 2s10s Curve Inversions

Strong Performance at the Tail Ends of Breadth

While the index turned lower today on weaker breadth, the recent rally for the S&P 500 has come on strong breadth resulting in the 10-day advance/decline line to surge to some of the highest readings on record. Monday and Tuesday saw 99th percentile readings in the 10-day A/D line and even after the decline today, the current reading remains in the 96th percentile. At Monday’s high, the 10-day AD line reached the most elevated level since October 2020. On a sector level, in the past week Financials, Health Care, Materials, Real Estate, and Tech also all saw 99th percentile readings in their own 10-day advance-decline lines.

In the matrix below, we show the average forward performance of the S&P 500 broken down by the percentile range that the index’s 10-day AD line is in. Generally, lower readings in the 10-day AD line have been followed by stronger returns whereas higher readings have been followed by weaker returns. That is, except for the most elevated readings. Readings in the upper decile have actually been followed by more consistently positive and stronger than normal average returns for the S&P 500. In other words, strong breadth is typically a more negative signal for the S&P 500 going forward, but an extremely strong breadth reading has actually been positive.

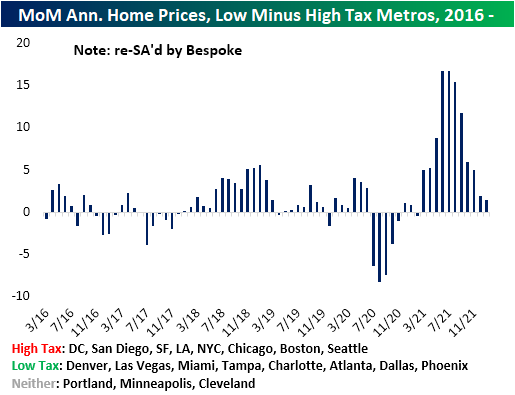

High Tax Home Price Appreciation Catching Up

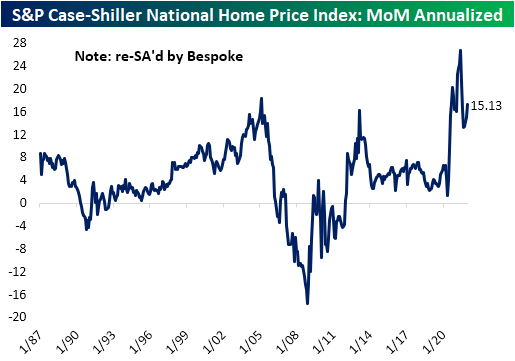

In last night’s Closer, we discussed recent trends in apartment and home prices. Case-Shiller data reported yesterday showed home price appreciation ramped back up in December and January with 15% annualized growth. That is a much slower pace compared to the 26% annualized appreciation back at the post-pandemic peak last spring but is still extremely high by any standard.

That appreciation has not been evenly felt across the country though. Since home prices inflected higher in the middle of 2020, four metros have been appreciated by more than 40% while Washington, Chicago, and Minneapolis are up at about half that price. In total, national home prices have risen almost 30% since the surge began or 18% annualized. It is worth noting that this data does not include the massive surge in mortgage rates that started at the end of last year which means that it is very unlikely that housing demand (and therefore home prices) can continue to run at such extreme levels given the huge hit to affordability brought on by higher rates.

Taking a more granular look at various metros, the huge surge in home prices had been more pronounced in lower-tax states relative to higher-tax states. But that trend has been unwinding. Click here to view Bespoke’s premium membership options.

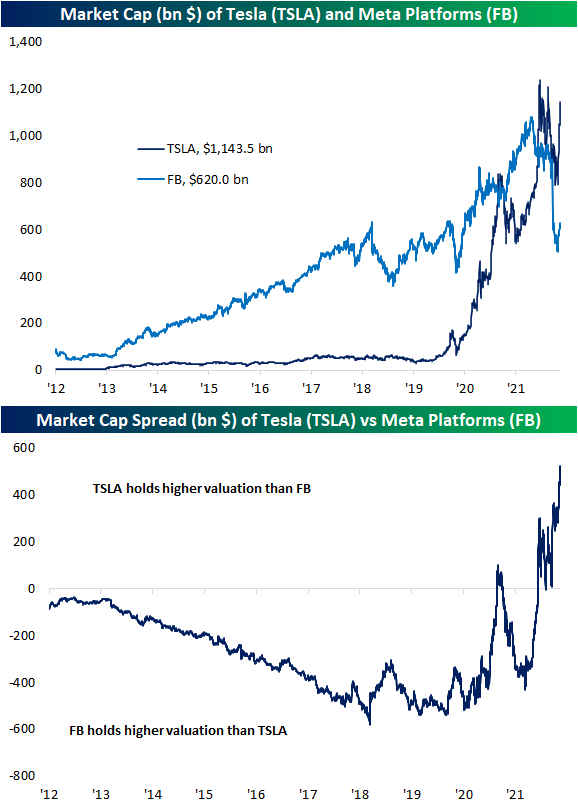

Tesla (TSLA) Closing in on Two Facebooks (FB)

Along with the rest of the market, two of the largest stocks, Tesla (TSLA) and Meta Platforms (FB), have been on substantial rallies this month. In the case of TSLA, the stock is roughly 10% away from its 52-week high after rising ~45% since its late February low. Facebook/Meta Platforms, on the other hand, peaked back in September with a massive drop in response to the last earnings report in February being the pinnacle of those declines. Losses continued until it put in a low on March 14th. Since then, the stock has rallied 22% but that still leaves it down over 40% from its 52-week high.

As shown below, Facebook had a much larger market cap than Tesla throughout the 2010s, but the 2020s have seen Tesla take the lead in a big way. While both have been members of the “trillion dollar market cap” club at various points in time, only Tesla holds that distinction right now. At the moment, Tesla’s market cap sits at nearly $1.15 trillion, while Facebook is just above the $600 billion level.

Below we show the ratio of the market caps of TSLA and FB. As shown, the massive distancing of the two stocks’ market caps means the value of Tesla (TSLA) is closing in on being worth 2 whole Facebooks. Click here to view Bespoke’s premium membership options.

Refinancing Plummets As Rates Continue to Rise

Mortgage rates continue to hone in on 5% as the reading on the national average of a 30-year fixed-rate mortgage via Bankrate.com hit 4.89% yesterday. That puts mortgage rates at the highest level since the spring of 2011. The extremely rapid 1.64 percentage point rise in rates over the past year also now stands as the largest year over year jump going back to at least the late 1990s per this data.

Given rates continue to climb, refinancing looks less attractive. The weekly reading on refinance applications from the Mortgage Bankers Association (MBA) has fallen over 14% two weeks in a row bringing the index to the weakest level since May 2019.

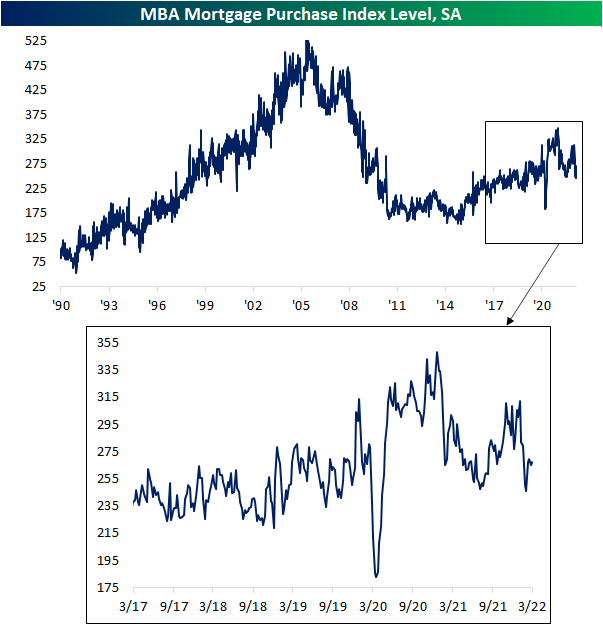

Purchase applications have also fallen to the low end of the post-pandemic range, though, there was a rebound this month with only last week seeing a decline followed by a minor uptick this week. While peaked, the current level of purchase applications is relatively healthy compared to other post-housing crisis years.

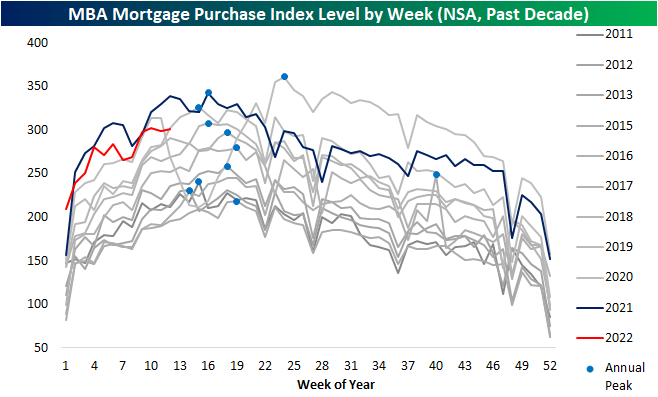

Taking a slightly different look at the data, in the chart below we show the non-seasonally adjusted purchase indices over the past decade. The first few months of the year tend to see purchases rise before hitting an annual peak (blue dots in chart below) sometime in mid-spring. Within the next several weeks, that seasonal peak is likely to be put in place. As mentioned above, while purchases are still running at the high end of the past decade, most of this year has run below last year’s pace, and that is likely to continue if not become more pronounced given the hit to affordability via higher rates and low inventories.

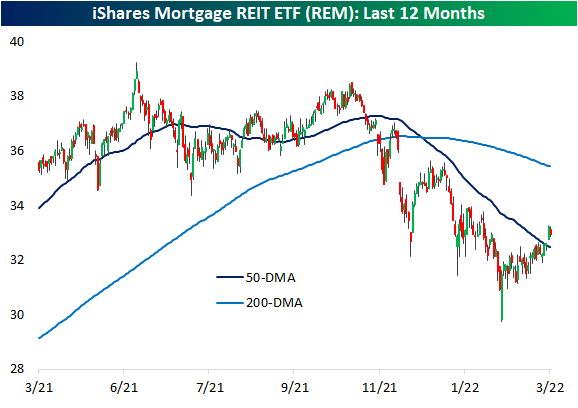

As for housing adjacent stocks, two ETFs have seen very different developments recently. As shown below, the iShares Home Construction ETF (ITB) set 52-week lows last week and with this week’s rebound it only hovers slightly above those levels. Mortgage REITs, proxied by the iShares Mortgage REIT ETF (REM), meanwhile, have actually been rallying off of 52-week lows set further back in February. That rally has broken the downtrend of the past several months and brought REM back above its 50-DMA. Click here to view Bespoke’s premium membership options.