Bespoke’s Morning Lineup – 8/26/22 – Going Back to the (Po) Well

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no risk-free path for monetary policy.” – Jerome Powell

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures have been digging out of their hole all morning, but still remain in negative territory ahead of Powell’s speech in Jackson Hole at 10 AM. Crude oil is modestly higher this morning while US Treasury yields are modestly lower. Outside of the Fed, one big story crossing the wires right now is from Bloomberg which is reporting that the US and China have reached a preliminary deal regarding audits that could avoid delistings of Chinese companies from US exchanges.

It’s also a busy morning for economic data, and for the 8:30 batch, Personal Income and Spending were both weaker than expected, but PCE inflation data came in weaker than expected. At 10 AM, we’ll get the Michigan Confidence report which will be interesting to watch as it will come out just as Powell starts speaking.

Ahead of Powell’s widely anticipated speech today, the equity market is following the technical playbook to a tee. After stalling out just short of its 200-DMA last week, the pullback that followed found support right at the June highs and the brief period of consolidation that occurred right before the August rally run to the 200-DMA. While not necessarily a technical term, the saying, “if at first, you don’t succeed, try again”, seems applicable to where the market is today relative to its 200-DMA. Now, we just have to wait to see if Powell’s speech will provide some fuel for that attempt or put on the brakes. We’ll know within the next couple of hours.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Big Buyer Steps Back, Income Investigation, Strong Sevens Sale – 8/25/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a look at what Blackstone’s (BX) announcement regarding home purchases implies for housing activity as well as a look at today’s Fedspeak (page 1). We then update GDP contributions with the second update of the Q2 release (page 2). We take more granular looks at inventories and corporate profits (page 3) as well as the discrepancy between GDP and GDI (page 4). Next, we take a look at freight rates and trade volumes (page 5) before turning to the latest update of our Five Fed Manufacturing Composite (page 6). We finish with a look into today’s historically strong seven year note auction (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 8/25/22

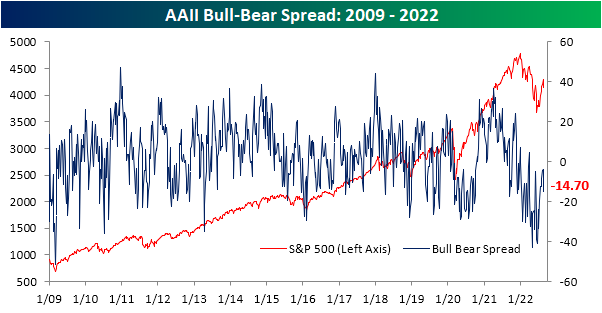

Sentiment Slide

With the S&P 500 pivoting lower in the past week, sentiment has reflected the move as the AAII sentiment survey showed bullish sentiment drop from 33.3% last week down to 27.7%. That marked the first time bullish sentiment fell in three weeks, and it was the largest single-week decline since an eleven percentage point drop the week of June 9th.

Bearish sentiment picked up the bulk of that decline as the reading topped 40% for the first time since the last week of July. At 42.4%, it is at the highest level since July 14th. Although that marks a shift toward more pessimistic sentiment, reversing a trend of improvement from the past few weeks, the current reading on bearish sentiment is well below the highs from throughout the spring and early summer.

Nonetheless, after coming within only a few points of a positive reading in the past month, the bull-bear spread took a sharp turn lower as a result of this week’s results. The spread fell to -14.7 which is the lowest reading since July 14th. That was also the first double-digit week-over-week drop in the reading since June. Additionally, with a move deeper into negative territory, the spread is a week away from becoming tied for the second-longest streak of negative readings on record. Click here to learn more about Bespoke’s premium stock market research service.

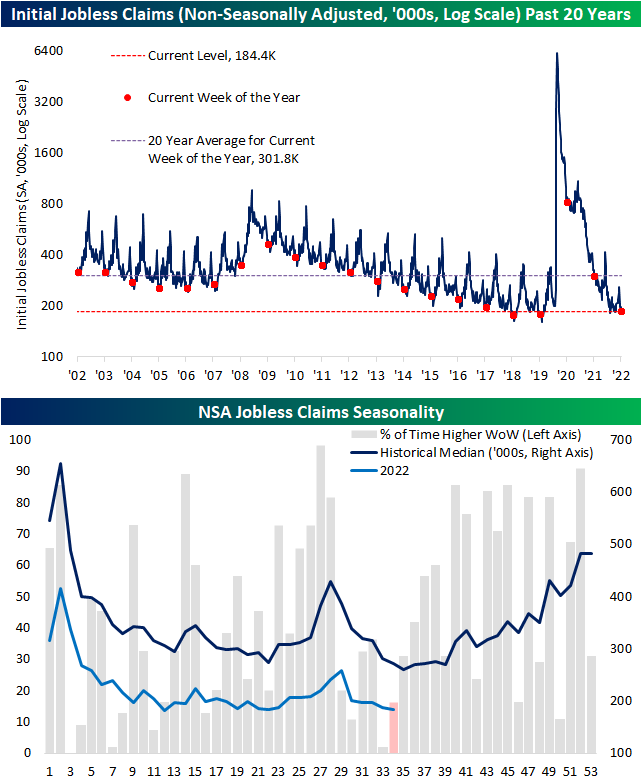

Claims’ Seasonal Low Draws Near

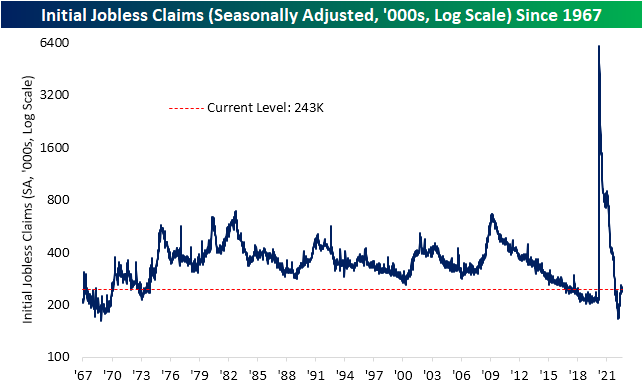

Initial jobless claims have come well off of the historic lows from earlier this year, but the past couple of weeks have also seen modest improvements. We’ve now seen back-to-back weeks of declines in claims for a total drop of 9K, leaving seasonally adjusted initial claims at 243K. That is the lowest reading since the week of July 22nd. However, that is still above the range from the two years prior to the pandemic.

Non-seasonally adjusted claims are nearing what is typically an annual low. The past couple of weeks have historically been two that have seen the most consistent declines on a week-over-week basis throughout the year. That has dropped NSA claims to 184.4K which is only slightly above the post-pandemic low of 183.6K from the final week of May.

Continuing claims came in lower than expectations this week dropping to 1.415 million versus forecasts for an increase to 1.441 million. Overall, continuing claims remain much stronger and less elevated off the lows than initial claims. Whereas initial claims are above their pre-pandemic range, current levels of continuing claims continue to come in at some of the lowest levels since the first few years of the data.

Given this, the ratio of initial to continuing claims continues to hover at levels that are well above the norm of the past few decades even after peaking last month. That would imply healthy turnover as those who are filing for unemployment are not remaining unemployed for long given the small amount of follow-through of initial claims into continuing claims. Click here to learn more about Bespoke’s premium stock market research service.

LIKS Report: 8/25/22

Bespoke’s Little Known Stocks (LIKS) report highlights a company that may not be on the traditional radar of most investors. In this report, we provide an in-depth analysis of the little known stock, including industry insights, growth lever analysis, insights to the competitive landscape, equity performance, relative valuation, operational efficiency, pros & cons, and more. Today’s report is about a company that helps governments and enterprises defend their cyber assets.

As always, this report is for informational purposes only and is not a recommendation to buy or sell any specific securities. Investors should do their own research and/or work with a professional when making investment decisions. Highlighting a stock doesn’t mean we are bullish or bearish on it. Our goal is simply to provide readers with facts to help them make informed decisions rather than just opinions.

Bespoke’s LIKS reports are available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our LIKS reports. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Jackson Hole Trends

Bespoke’s Morning Lineup – 8/25/22 – Mountain Jam

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s hard to live your life in color, and tell the truth in black and white.” – Gregg Allman

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We’re still a full day from Powell’s Jackson Hole speech, but futures have shown some resilience this morning indicating a positive start to the trading day. Interest rates are little changed but slightly biased to the upside. It’s a busy day for economic data for jobless claims, GDP, Personal Consumption, and Core PCE all at 8:30 with the KC Fed Manufacturing report coming out at 11 AM. The 8:30 data was just released and Jobless Claims came in lower than expected on both an initial and continuing basis. The revision to Q2 GDP came in at a decline of 0.6% which was slightly less worse than forecasts for a decline of 0.7%. Personal Consumption came in right in line with forecasts at 1.5% while Core PCE was 4.4% which was in line with consensus forecasts. All in all not much in the way of big surprises.

As investors gnaw on their fingernails in anticipation of Friday’s Powell speech in Jackson Hole, they remain anxious about the direction of interest rates. The yield on the 10-year US Treasury has gone from a multi-year high of just under 3.5% in late June down to 2.57% in early August. Since that low, yields have rocketed higher and closed yesterday at 3.10% which is right around the same levels they temporarily peaked at in the Spring. If yields continue higher in the coming days, a run to new highs will seem like a foregone conclusion which would act as a headwind for risk assets, but if yields start to stall out here, the chart of the 10-year yield will look more like a head and shoulders and provide a sigh of relief.

The two-year yield is another story. Just yesterday, the yield finished the day right at 3.39% which was just four basis points (bps) below its June 14th high. Like the 10-year, the direction of the 2-year yield in the coming days will likely play a big role in the stock market narrative for weeks to come.

Whichever way yields move, the 10-year/2-year Treasury yield curve remains firmly entrenched at inverted levels and is one of an increasingly growing number of indicators out there suggesting that the economy is either on the verge of or already in a recession.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke 50 Growth Stocks — 8/25/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

The Closer – Manufacturing Sales Versus Volumes, 5y Sale, EIA – 8/24/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a look at the overhead resistance for the S&P 500, regional currency moves, and credit spreads (page 1). We follow up with a dive into the details of the mixed durable goods report and how nominal activity translates to volumes (page 2 and 3). We then recap today’s 5 year note sale (page 4) and the latest weekly release of the petroleum status report (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!