Stabilized Sentiment

This week’s readings on sentiment through the American Association of Individual Investors‘ weekly survey was little changed following choppy price action over the past week. Bullish sentiment fell just 0.23 percentage points to 24.14% marking a second straight week with less than a quarter of respondents reporting as bullish and the lowest reading since May 14th’s 23.31%. That small drop this week on top of the declines the prior two weeks also marks the first back to back to back declines in bullish sentiment since the three weeks ending January 9th. That’s right, not even during the bear market did bullish sentiment fall for three consecutive weeks. While there may not have been another period since January with consistent declines like the current stretch, there were other three week spans with larger declines. From April 16th to May 5th there was an 11.19 percentage point decline and from February 20th to March 12th there was a 10.86 percentage point decline compared to the current 10.41 percentage point decline from the June 4th high to today.

Likewise, neutral sentiment moved slightly lower falling from 27.85% to 26.96%.

Meanwhile, bearish sentiment remains the predominant position among survey respondents, rising for a second straight week to 48.9%. Like bullish sentiment, this week did not see a particularly large move with the bearish camp only rising 1.12 percentage points. The current reading is now the highest since May 14th when more than half of respondents reported as bearish.

That has sent the bull-bear spread further into negative territory. Now at -24.76, the bull-bear spread is now at its widest level in favor of bears since May 14th.

While AAII’s survey holds a bearish bias at the moment, the Investors Intelligence survey is much more bullish. Bullish sentiment in this survey rose from 54.9% last week to 57.3% this week which is the highest level since January 22nd. That is also at the upper end of the past decade’s range in the 86th percentile. Bearish sentiment on the other hand fell for a 13th straight week which is its longest stretch of consecutive declines since at least 1997. Now at 18.4%, bearish sentiment is at its lowest level since January 22nd. Click here to view Bespoke’s premium membership options for our best research available.

Continuing Claims Back Below 20 Million

For a record 12th straight week, jobless claims declined this week. While they’re moving in the right direction, over those same 12 weeks, claims have actually exceeded consensus forecasts nine times. Seasonally adjusted claims totaled 1.48 million which was down 60K from a revised 1.54 million last week (the original release was 1.508 million). While that 60K decline was larger than the 26K decline the previous week, the rate of improvement in jobless claims remains toned down from what was observed over the past few months.

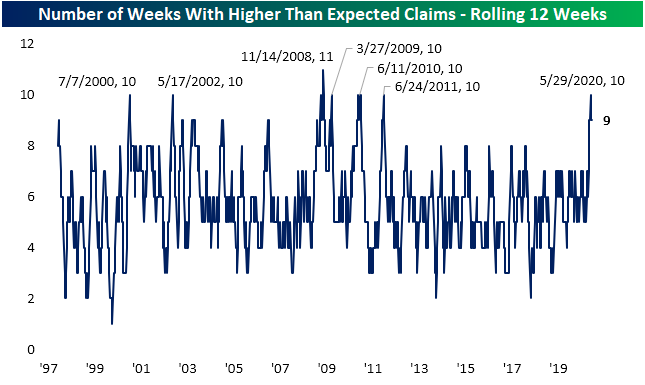

As previously mentioned, jobless claims have been consistently coming in above estimates. In the three months that jobless claims have declined, there have only been three weeks (April 10th, April 17th, and June 5th) that claims have come in better than expectations. In the chart below, we show the count of weeks in rolling a 12-week span that claims were above forecasts. The current reading of 9 weeks is actually just off the recent peak of 10 weeks thanks to the recent beat on June 5th. Prior to that, at the end of May, 10 of the 12 weeks had seen claims miss estimates. Before that, you would have to go all the way back to 2011 a stretch of weaker than expected reports that were this weak. The weakest 3-month span relative to estimates was back in the 12 weeks ending November 14th, 2008 when claims had missed estimates for 11 of 12 weeks.

To put it briefly, while any drop in jobless claims is welcomed and that has been observed over the past three months, claims have seemed to have hit a bit of a plateau in terms of improvement. Non-seasonally adjusted claims embody that dynamic of shrinking improvements. Non-seasonally adjusted claims only fell by 6K to 1.457 million this week. That 6K decline was actually the smallest weekly move in absolute terms since a 5.1K decline back in early February- back before the surges of the COVID era.

Unlike initial claims, continuing claims actually beat estimates this week falling below 20 million for the first time since mid-April. Continuing claims have now fallen for four of the past five weeks since the peak of 24.912 million claims on May 8th. Also unlike initial claims, this was actually a larger improvement than what has been observed in recent weeks. The first reading after the aforementioned peak in claims was the largest one week drop on record totaling 4.071 million claims. This week’s 767K decline to 19.522 million continuing claims was the second-largest on record. It was also more than double the prior week’s decline. Granted, even with those improvements more than a tenth of the US workforce is currently unemployed. Click here to view Bespoke’s premium membership options for our best research available.

Eight Was Enough

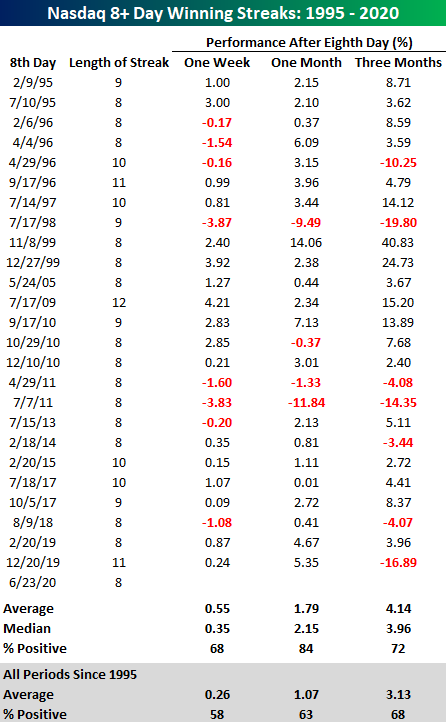

After eight straight days of gains, the Nasdaq looks like it’s ready for a breather today as the index is down over 1%. The current streak represented the longest string of back to back gains for the Nasdaq of 2020 and the longest streak since the 11-day streak that came to an end last December. Throughout the Nasdaq’s history going back to 1971, there have been over 80 streaks of at least eight trading days, but since the tech boom really took off in the late 1990s, these streaks haven’t been as frequent with just 26 now since 1995.

Once a winning streak of eight or more days comes to an end, one would think that short-term returns going forward would be below average. However, looking back at how the Nasdaq performed following prior eight-day winning streaks, more often than not, the index has actually tended to have better than average short-term forward performance. In the week that followed these prior streaks, the Nasdaq averaged a gain of 0.55 (median: 0.35%) with positive returns 68% of the time. One month later, the average gain increased to 1.79% (median: 2.15%) with positive returns 84% of the time. Three months later, the effect of an eight-day winning streak probably didn’t mean much, but even here the Nasdaq averaged a gain of 4.14% (median: 3.96%) with gains 72% of the time. What’s notable about all of these performance numbers is that they are all better and more consistent to the upside than the Nasdaq’s historical average one week, one month, and three-month returns. Today’s performance is ending the Nasdaq’s winning streak with a thud, but history shows that prior streaks have typically been part of longer periods of outperformance.

One item worth noting about today’s decline for the Nasdaq, though, is that with a decline of over 2%, the only other time where an eight-day winning streak ended with a decline of more than 2% was back in July 1986. Like What you see? Click here to view all of Bespoke’s membership options for access to the best research available.

Tech Overbought for Over 50% of the New Bull Market

Most sectors have drifted lower in the past week with defensives like Real Estate and Utilities having taken it on the chin the most down 4% and 3.16%, respectively. The move has brought the Utilities sector back below its 50-day moving average. At the moment, it is the only sector below its 50-DMA. On the other hand, Technology and Communication Services stocks have continued to press higher up 2.35% and 1.05% in the past week respectively. Now the Tech sector is over 10% above its 50-DMA and is easily the most overbought sector. Alongside Tech, Communication Services and Consumer Discretionary are the only other sectors that are currently overbought. Most of the other sectors were overbought within the past week but recent declines have left them in neutral territory.

As shown in the trading range charts from our Daily Sector Snapshot below, the majority of sectors have been consistently trading in overbought territory over the past couple of months. Before declines in the past few weeks, some of these had even traded at over 2 standard deviations above their 50-DMAs. With most having since returned to neutral territory, they broadly remain off their highs, though, Consumer Discretionary and Technology are trading around fresh 52 week highs.

As previously mentioned, Communication Services, Consumer Discretionary, and Technology are still overbought and that should not come as a surprise. These three sectors have consistently been overbought in the three months since the bear market low on March 23rd as shown in the charts above and below. Since that low, Technology has been overbought more than 50% of trading days and both Communication Services and Consumer Discretionary have been overbought for 47.06% of days. Given these three sectors account for just under half of the weight of the whole S&P 500, the broader index has not been far behind trading overbought for 38% of days since 3/23. Looking at the other end of the spectrum, Consumer Staples has been overbought the least at only 7.35% of days. Other groups that were stronger during the bear market but have since seen performance wane like Health Care and Utilities also have been overbought far less frequently. Click here to view Bespoke’s premium membership options for our best research available.

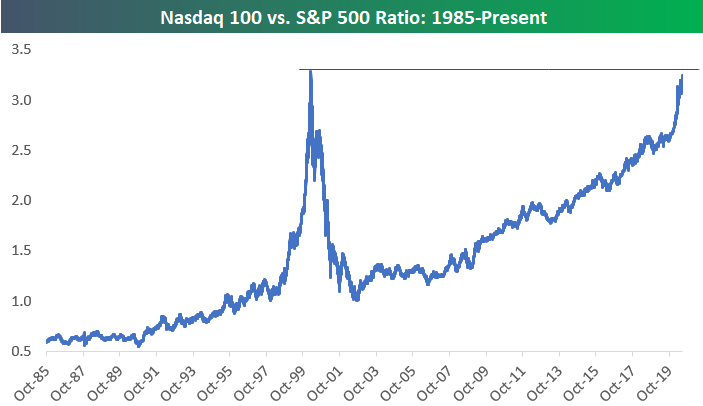

Nasdaq 100 to S&P 500 Ratio Nears Record

The ratio of the Nasdaq 100 to the S&P 500 rose to 3.26 as of yesterday’s close. As shown below, this is as high as the ratio has been since the peak of the Dot Com Bubble back in early 2000. In fact, there have only been two trading days in the history of the Nasdaq that have seen a higher ratio — March 9th and March 10th of the year 2000. March 10th, 2000 turned out to be the peak for the Nasdaq at the very top of the Dot Com Boom. The index would go on to fall 66% over the next two years. Click here to view Bespoke’s premium membership options for our best research available.

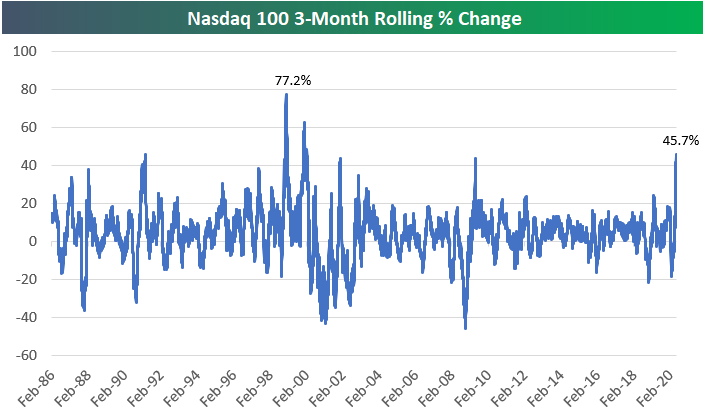

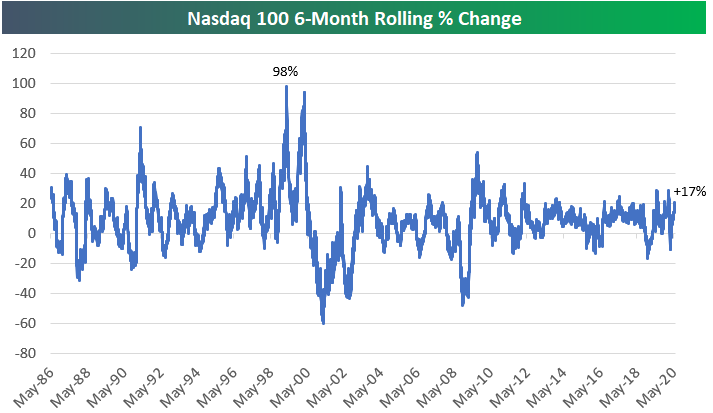

There has of course been a lot of discussion recently about the Nasdaq’s huge run higher since late March. We are now exactly three months past the low point of the COVID Crash on March 23rd, and as shown below, the Nasdaq 100 is up 45.7% since then. This three-month period has been the strongest run the Nasdaq 100 has experienced since the Dot Com Boom of the late 1990s.

While a 45.7% three-month gain is definitely huge, there were stronger three-month periods in 1999 and early 2000. On January 20th, 2000, the rolling 3-month return hit 62.63% for the Nasdaq 100, while on January 11th, 1999, the reading was +77.2%!

One important difference between the recent three-month run for the Nasdaq 100 and the runs experienced in the late 1990s is the level of the index at the start of the rally. Prior to the current 45% rally, the Nasdaq had fallen 20% over the prior three months. This leaves the index up 17% over the past six months. That’s still a strong six-month gain, but it doesn’t even register as an outlier when looking at the six-month rolling performance chart below. During the late 1990s, there were two six-month periods that each saw gains of nearly 100%.

Richmond Rebound

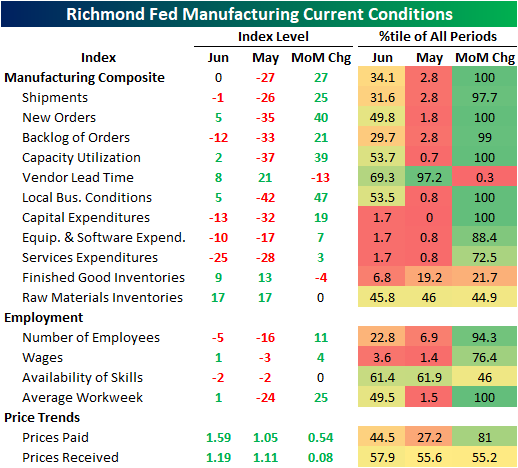

This morning, the Richmond Federal Reserve Bank updated its monthly data on manufacturing activity in the region. The report showed manufacturing activity was unchanged in June as the index rose to 0 from -27 in May. That was the first non-contractionary reading since March. Additionally, the 27 point month over month increase was the largest one month gain on record. That follows a very strong reading in May when it rose by 26 points which at the time tied March of 2016 for the largest on record.

As for the sub-indices of the report, there were five in addition to the headline index—Backlog, Capacity Utilization, Local Business Conditions, Capital Expenditures, and Average Workweek—that rose by the most in a single month. While a massive improvement, most of these readings sit at the lower end of their historical range and there are still roughly an equal amount of sub-indices for current conditions in contraction as expansion. Expectations, on the other hand, are much more optimistic with multiple categories now at the upper end of their historical ranges. For the indices for future expectations, those of Shipments, New Orders, Capacity Utilization, Local Business Conditions, Services Expenditures, Number of Employees, and Average Workweek also all rose by a record amount.

Looking at the service side of the economy, the results were less rosy. Every service index is still deep in contraction and at the lower end of their historical range and that is even after some of, if not the largest monthly increases on record. As with the manufacturing indices, though, expectations for the future are more optimistic after huge improvements in June. The only areas for expectations that remain notably weak and at the low end of their historical ranges are those of capital expenditures (all of which are in the bottom 2% of all readings) and employment. While employment is still low, the 24-point gain in June brought it into expansionary territory. Click here to view Bespoke’s premium membership options for our best research available.

Gold vs. Treasuries: Who’s the Better Hedge?

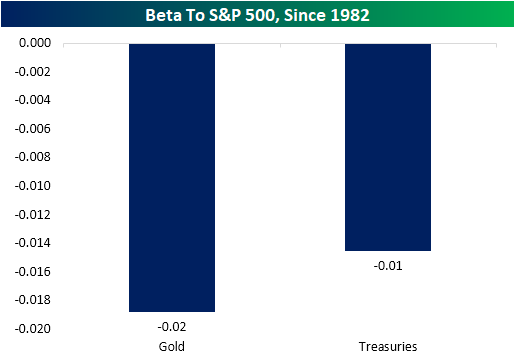

Given the high level of equity prices following the huge rally off March lows, investors may be looking for assets that can provide a hedge in case the recent rally cools. The two classic hedge assets are of course gold and Treasuries. We use roll-adjusted futures returns for both, using ten-year future returns for the Treasury series. Over the very long term, neither of these assets are actually very differentiated from equity markets; betas (volatility relative to the market) for both are very low. Of course, that doesn’t mean they don’t offer value as a source of diversification, just that daily returns from both don’t tend to move in opposite directions in the long term.

What about during periods of stress? In the chart below we show the average rolling 3 month beta for gold and ten-year notes versus the S&P 500 during periods when rolling 3-month S&P 500 returns are in the bottom 5% of all periods. In other words, this chart shows how much these hedge assets tend to move versus the S&P 500 when the S&P 500 is stressed. As shown, Treasuries consistently have more upside exposure when the S&P 500 is down, and that’s a stable relationship. Gold, which used to be an excellent hedge asset, has now flipped and is likely to fall with the S&P 500 during large declines.

On the flip side, large rallies in the S&P 500 tend to see a positive beta for gold, while Treasuries maintain their negative beta. An argument could be made that while gold often falls when the S&P 500 does, it might be a more attractive hedge asset because it incurs a lower cost to holding if the hedge doesn’t end up being necessary. Click here to view Bespoke’s premium membership options for our best research available.

Speculators Shorting USD

From its peak earlier this spring to its low earlier this month, the dollar had fallen over 7.5%. Around those recent lows there was a stretch of 12 straight days closing below its 200-DMA, as shown below. While the greenback managed to move back above its 200-DMA on Thursday and Friday of last week, it’s giving up the ghost this week falling around 0.5% yesterday and another 0.43% today as of this writing. Yesterday’s decline brought it back below its 200-DMA.

That decline comes on overall bearish sentiment for the dollar. In our Closer every Friday, we include the Commodity Futures Trading Commission’s data from the Commitments of Traders Report on speculator positioning. Last week’s report showed a massive shift in open interest getting short on the dollar. A net percentage of 26.9% are now short the dollar compared to +13.82% net long the prior week. That 40.71 percentage point shift was the largest move in favor of speculators getting short behind a 48.47 percentage point decline back in September 2005 as shown in the second chart below.

It is not just the dollar that speculators are short though. As for US equities, 31.13% of open interest are net short the Dow. That is the most pessimistic positioning speculators have taken on the index since August 2005. For other indices like the S&P 500, positioning is not as extreme but similarly holds a bearish bias. Click here to view Bespoke’s premium membership options for our best research available.

Real Estate and Rates Showing Good Timing

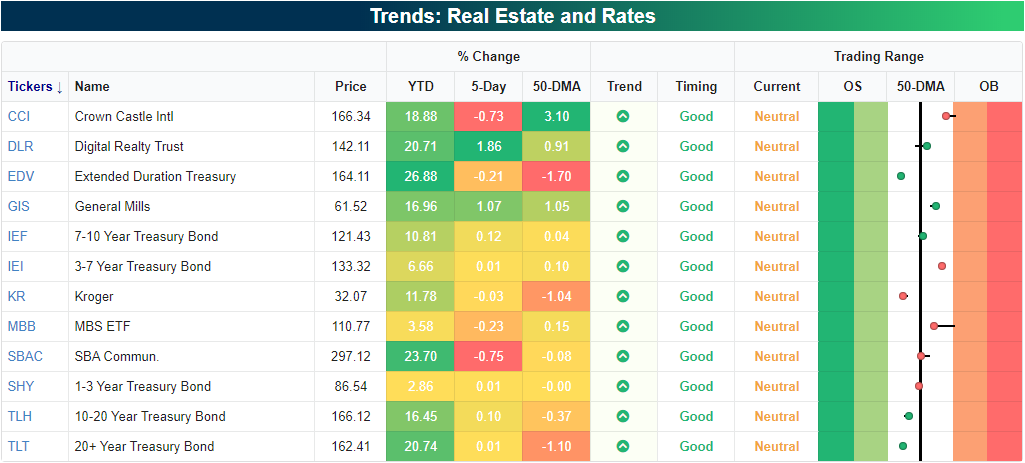

In our Trend Analyzer and Chart Scanner tools, we offer a number of different screens including ones for 52-week highs and lows and golden (rising 50-DMA moving above rising 200-DMA) and death crosses (falling 50-DMA moving below falling 200-DMA). Another screen we offer looks at the long term trends and timing scores from our algorithms. Typically, stocks that are overbought and in a downtrend will have poor timing while those in long term uptrends that are not overbought pose as better long ideas, and as a result, earn a good timing score. At the moment, due to the sharp declines and not everything having fully recovered from the bear market, there are still more stocks that are in downtrends and have poor timing (154) than those in uptrends and with good timing scores (21).

There is an interesting composition of stocks and ETFs that are currently in long term uptrends with good timing scores. The bulk of those 21 tickers are either Real Estate or Consumer Staples stocks or Treasury related ETFs as shown in the snapshot of our Trend Analyzer below. Typically seen as safe havens during market downturns, many of these held up during the bear market allowing them to not only maintain but also boost the picture for their long term uptrends. As risk appetite has improved over the past few months, the momentum of these names has slowed with each one now neutral rather than overbought which helps to earn their good timing scores.

As shown in the charts from our Chart Scanner below, all of these are in uptrends since the start of the year albeit with some volatility during the bear market. Broadly speaking for Treasury ETFs like EDV, IEI, IEF, TLH, and TLT in addition to a mortgage-backed security ETF (MBB), they have been in slight downtrends or trending sideways over the past few months after massive runs earlier this year. As a result, their 50-DMAs have caught up to price which now leaves them in neutral territory. Meanwhile, Real Estate names like Crown Castle (CCI) and SBA Communications (SBAC)—both in the business of cell towers—have pulled back to the bottom of their uptrends around their 50-DMAs.The same can be said for Consumer Staples names like General Mills (GIS) and Kroger (KR). These names have certainly sat out much of the rally in recent weeks, but any stress in the broader market from currently overbought levels will likely result in these stocks seeing increased interest. Click here to view Bespoke’s premium membership options for our best research available.

Nasdaq, Tech, Growth Keep Going

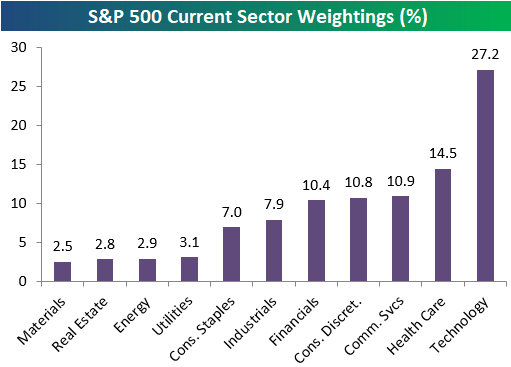

With Technology rallying and once again outperforming to start the new trading week, we wanted to note that the sector’s weighting in the S&P 500 has pushed above 27% recently up to 27.2%. That’s nearly twice as big as the next biggest sector in the S&P — Health Care — at 14.5%. Just three other sectors have weightings above 10%, and they’re all just only slightly above the 10% mark — Communication Services, Consumer Discretionary, and Financials. We’d note that Amazon (AMZN) makes up about a quarter of the Consumer Discretionary sector’s 10.8% weighting in the S&P, and while it is technically a retailer, between its web services division, and strong technology platform, you could argue that its just as much a Technology stock as it is Consumer Discretionary.

Industrials and Consumer Staples have seen their weightings dip below 8%, and the four smallest sectors each have weightings of just 2-3%.

At the moment, Tech’s 27.2% weighting in the S&P is larger than the weightings of the six smallest sectors combined.

The tech-oriented Nasdaq 100 continues to outperform as well. Below is a chart of the ratio between the index levels of the Nasdaq 100 vs. the S&P 500. The ratio has been on a non-stop march higher since the end of the Dot Com bust in late 2002.

There have only been three trading days in history where the Nasdaq 100 to S&P 500 ratio was higher than the 3.25 level it’s at right now. Those three days came on March 8th, March 9th, and March 10th of the year 2000 — the very peak of the Dot Com Bubble.

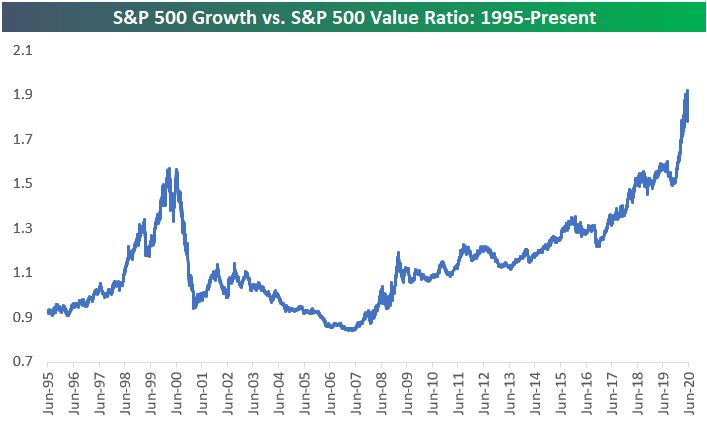

Finally, the Growth vs. Value trade remains lopsided towards growth. Below is a chart of the ratio between the S&P 500 Growth and S&P 500 Value index since 1995. This ratio actually took out its highs from the Dot Com Bubble in mid-2019, and it has exploded even higher over the last year. Value did outperform for a bit in May and early June, but over the last two weeks we’ve seen Growth soar and the ratio has once again made new highs. Click here to view Bespoke’s premium membership options for full access to all of our research.